Public Budget Deficit and Economic Growth in Nigeria: Evidence from NARDL Approach

- USMAN, Jabir Muhammed

- AGUNBIADE, Olabode

- AKUSO, Jonah

- 3884-3896

- Sep 27, 2024

- Economics

Public Budget Deficit and Economic Growth in Nigeria: Evidence from NARDL Approach

USMAN, Jabir Muhammed, AGUNBIADE, Olabode (PhD), AKUSO, Jonah

Department of Economics, Mewar International University, Masaka Nigeria.

DOI: https://dx.doi.org/10.47772/IJRISS.2024.803281S

Received: 19 August 2024; Accepted: 26 August 2024; Published: 27 September 2024

ABSTRACT

The study examines public budget deficit financing and economic growth in Nigeria using time series data for the period of 1986 to 2021. The study uses Non-Linear Autoregressive Distributed Lag (NARDL) as its estimation technique. Dialectically, the study reveals that public budget deficit financing sources such as; treasury bills, treasury bonds, multilateral debt, bilateral debt, oil revenue to total revenue ratio, non-oil revenue to total revenue ratio and external reserve had significant positive and negative impacts on economic growth in the Nigerian economy within the study period. However, specifically, public budget deficit financing sources such as; treasury bills, treasury bonds, oil revenue to total revenue ratio, non-oil revenue to total revenue ratio and external reserve have asymmetric impacts on economic growth in the Nigerian economy within the period under review. The study concludes that the imposition of a linear symmetric in modeling public budget deficit financing in the country could be misleading as far as Nigerian economy is concerned. Hence, the use of NARDL model for public budget deficit financing contributes to the understanding of the nonlinear dynamics between public budget deficit financing and economic growth, thereby leading to more effective and efficient forecasting and policymaking. The study recommends that government at all tiers in the country should maintain high level of fiscal discipline in order to ensure optimal utilization of treasury bills, treasury bonds, oil revenue to total revenue ratio, non-oil revenue to total revenue ratio and external reserve towards realizing the desired level of economic growth in the Nigerian economy.

Keywords: Public, Budget, Deficit, Financing and Economic Growth.

INTRODUCTION

Increasing expenditure is one approach to addressing societal issues, according to governments, both military and civilian. The government, acting as the people’s representative, needs money to fund infrastructure projects, well-maintained roads, employment opportunities, and education. However, in carrying out this massive responsibility, the government’s spending and revenue requirements occasionally exceed its available funds; in these situations, deficit financing is used to close the funding gap.

Additionally, a lot of developing nations use budget deficit financing to accomplish their macroeconomic goals, particularly economic growth (Audu, 2021). In theory, a deficit occurs anytime expenses exceed income (Soludo, 2003). However, financing budget deficits still seems to be a tactic used in many developing nations, such as Nigeria, which has been driving away private sector investments and slowing economic growth (Joseph and Godwin, 2021).

It is important to understand that budget deficits are not unique to developing countries; rather, the economic development of the last ten years has reignited interest in monetary and fiscal policy issues. The growth and persistence of budget deficit financing in both industrialized and developing countries in recent years has brought the issue of budget deficits into sharp focus. It’s vital to remember that even some industrialized nations have had to deal with deficit finance at some point, even though many developing nations are heavily involved in it and some have worse deficits than others. For example, as of 1989, only West Germany and the United Kingdom reported having no net deficit financing as a percentage of GDP/GNP. Other developed countries, such as the United States, France, Sweden, and Italy, continued to report up to 10% of net deficit financing, while countries like Australia and Canada reported approximately 35%. Nevertheless, by the end of the 1990s, most developed countries had overcome such financing thanks to well-designed policies and institutional frameworks (Onwe, 2018).

The problem of budget deficit has also been brought up recently due to the growth and durability of deficit financing in Nigeria. Nwaeke and Korgbeelo (2018) believed that the problem was related to the developing economies’ low per capita income, unpredictable public revenue, weak government authority, and high rates of inflation. Following the adoption of the Keynesian-inspired public expenditure by Nigeria government to motivate macroeconomic performance is generally associated with the establishment of deficit financing (Anyanwaokoro, 2018). This policy is perceived as a weapon that the government uses to curb or terminate economic downturns. But in the process of carrying out this massive duty in the Nigerian economy, the government’s expenditure needs occasionally exceed its available earnings. Deficit financing follows, with the goal of bridging the gap between the nation’s revenue and spending requirements (Oladipo and Akinbobola, 2019).

The increase in public budget deficit financing is primarily caused by the need to increase the government’s capacity to carry out capital projects in the Nigerian economy. This is because deficits lead to high levels of internal and external borrowing to boost the flow of funds into the economy (Onwioduokit and Bassey, 2019). These borrowing practices have a negative impact on the economic performance of any nation whose economic activities are financed by long-term debt from foreign nations because they irritate lone investors because of the high interest rates. One tool of fiscal policy in the Nigerian economy is public budget deficit financing, which promotes borrowing to close the budget deficit caused by the government’s overall forecasted expenditure exceeding its projected revenue (Anyanwaokoro, 2018).

Empirical data suggests that initiatives to boost economic expansion in Nigeria resulted in a scenario where the nation repeatedly faced significant deficits, which eventually necessitated borrowing from both domestic and foreign sources to meet the required spending (Awe and Shina, 2017). Nigeria’s budget deficit financing growth rate was 68.2% in 2016, 70.7% in 2017, 79.8% in 2018, 82.9% in 2019, and 91.3% in 2020, indicating a clear and continuous development in the country’s public budget financing (Central Bank of Nigeria, 2020). The Nigerian economy continued to develop at a decreasing rate despite the rise in public budget deficit funding sources such as internal and external debt, government taxes, external aid, and external reserves (Siyan, 2020). It is clear that Nigeria’s economy has not performed well in terms of economic growth, since statistics show that growth was 8.2% in 1990 and decreased to 5.4%, 4.6%, and 3.5% in 2000, 2001, and 2002, respectively (World Bank, 2015). More so, economic growth measured by Gross Domestic Product (GDP) growth rate in Nigeria was recorded as 2.7% in 2015, -1.6% in 2016, 0.8% in 2017, 1.9% in 2018, 1.94% in 2019 and -1.79% in 2020 (World Bank, 2020). However, the economy grew by 3.6% in 2021 (African Development Bank Group, 2022).

In literature, most of the extant studies in this area of research such as; Oluwole, Solawon and Odueke (2020), Chukwu, Otiwu and Okere (2020), Sunday and Philomena (2020), Adofu, and Abula, (2010) and Aminu, and Musa (2013) focuses more on the nature of causality between budget deficit and macroeconomic performance with little attention given to budget deficit financing and inclusive growth in Nigeria. In addition, some of the previous studies such as; Sunday and Philomena (2020), Oluwole, Solawon and Odueke (2020), Chukwu, Otiwu and Okere (2020), Nwanna and Nkiruka (2019) and Nwaeke and Korgbeelo (2016) utilizes public budget deficit financing sources such as; domestic debt, external debt, external reserve and oil revenue. However, most of the past studies fail to disaggregate domestic debt and external debt into treasury bills, treasury bonds, multilateral debt and bilateral debt, respectively. More so, the previous studies fails to consider the case of controlled variables such as debt servicing and weak institutional quality in financing deficit despite the large magnitude of impact of variables play in budget deficit in Nigeria economy. Thus, it is against this background that this study assesses the impact of public budget deficit financing on economic growth in Nigeria.

LITERATURE REVIEW

Budget deficit is conceptualized as the period in time when government expenditure exceeds government revenue (Chimobi & Igwe, 2019). Deficit budgeting implies that the government intends to expend much more money than it earns from diverse income sources (Anyanwaokoro, 2018). Additionally, public budget deficit financing refers to excess spending over income as determines by government fiscal policy, which calls for the creation of a fund to finance deficits through borrowing from domestic or international sources that must be repaid with interest within a set timeframe (Muhammad, 2021). Public budget deficit financing is the process of using borrowed money from the general public to pay for the federal government’s excess fund of expenditures over receipt of revenue for a specific period (Audu, 2016) while Stiglitz (2005) views it as the federal government’s excess fund of expenditures over receipt of revenue for a given period which is financed by borrowing money from the general public. According to Sameh (2017), economic growth refers to the gradual process by which the economy’s productive capacity is raised over time to result in rising levels of national output and income. Increasing a nation’s potential Gross Domestic Product (GDP) is how the World Bank (2014) conceptualized economic growth, though this varies depending on how national product has been measured.

Oladejo (2019) conceptualizes economic growth as a continual rise in the national income over a range of time of not less than five years. Since inflation has a distorting effect on economic growth, economic growth in economic theory is typically calculated in real terms, or inflation-adjusted terms, which is why Real Gross Domestic Product (RGDP) is used in the majority of growth literature. This suggests that rising RGDP is a proof of a booming economy. According to Taiwo (2018), economic growth is the long-term increase in a nation’s ability to provide its population with an increasing variety of economic goods. This growth capacity is based on advancing technology as well as the necessary institutional and ideological change (Ohiaeri, 2017). Acha and Essien (2018) viewes economic growth as the percentage or proportionate increase in real income during a given period, usually a year. Economic growth is a positive increase in economic variables, real or nominal, normally persisting over successive periods.

Adebowale (2021) empirically investigates the asymmetries in the relationship between Nigeria’s budget deficit and economic growth from 1986 to 2020. The Central Bank of Nigeria Statistical Bulletin (2020) was the source of the time series data used in the study. For data analysis, the study utilizes the Non-linear ARDL model developed by Shin et al. (2014). The findings show that budget deficit affect economic growth both in the short and long run negatively which makes this work a landmark since previous studies were unable to capture this aspect of non-linearity.

Oluwole, Solawon and Odueke (2020) examines budget deficit on economic development in Nigeria from 1981 to 2018. The study made used secondary data sourced from the Central Bank of Nigeria Statistical Bulletin (2018). The study used budget deficit, inflation, money supply, total government debt and per capita income as variables of interest. Autoregressive Distributed Lag technique was employed to examine the relationships among the variables used. The result of the ARDL coefficient indicated that budget deficit as a percentage of gross domestic products and inflation rate had negative and significant effect on per capital income both in the short and long run.

Chukwu, Otiwu and Okere (2020) explores the impact of budget deficit on economic growth of Nigeria, covering the period,1980-2019.The study uses time series data sourced from the Central Bank of Nigeria Statistical Bulletin (2019). The unit root, granger causality, and co-integration tests were used in two Stage Least Square Data analyses to produce five statistically significant models: the budget deficit and economic growth model, the budget deficit and real interest rate effect model, the budget deficit and inflation rate effect model, the budget deficit and investment effect model, and the budget deficit and real exchange rate effect model. Budget deficits were discovered to have a significant negative relationship with GDP growth rate, real private investment, inflation rate, real exchange rate, and a significant positive relationship with real interest rates.

Sunday and Philomena (2020) examines the implications of federal government fiscal deficits on the macroeconomic variables in Nigeria from 1986-2019.The study uses time series data sourced from the National Bureau of Statistics and Central Bank of Nigeria Statistical Bulletin (2019). Using Auto-Regressive Distributed lag (ARDL) approach, the study finds that there is significant long run relationship between fiscal deficit and selected macroeconomic variables in Nigeria. It establishes that federal government deficit does not have significant impact on external reserve in Nigeria in the short-run period, and also that there is no significant influence of federal government deficits on inflation in Nigeria within the period under study.

Nwanna and Nkiruka (2019) Studied the effect of deficit finance on Nigeria economic growth. The study uses secondary data from CBN statistical bulletin on various issues as relevant for the period under study (1981-2016). Augmented Dickey Fuller (ADF) unit root test, Johanson Co-integration test and normality test were employed for the analysis. The research findings revealed that deficit financing through external debt borrowing has a significant negative effect on Nigeria’s economic growth. Also, domestic debt has a positive significant effect on Nigeria’s economic growth, while debt service has no significant effect on Nigeria’s economic growth. Also, Okah, Chukwu and Ananwude (2019) examines the effect of deficit financing on economic growth of Nigeria from 1987 to 2017.The study uses time series data sourced from the National Bureau of Statistics Bulletin (2017).The Vector Autoregressive Estimates was use in estimating the model. The analysis performed reveals that deficit financing has positive but insignificant effect on Nigerian economic growth.

George and Kosimbei (2019) assesses budget deficits and economic growth in Nigeria. The study uses annual time series data sourced from World Development Indicator (2017) for the period 1963 to 2017. The study utilizes current account of the balance of payments, private consumption, private investments, money supply, treasury bill rates, and real GDP as variables of interest. The study underpinned Mundel- Fleming model and Vector Auto-Regressions (VARs). The study establishes that the budgeting process had loop holes which perpetrated budget deficits. Also, the sources of budget deficits includes: level of economic development, growth of revenues, instability of government revenues, government control over expenditures and the extent of government participation in the economy. The Impulse Response Functions (IRFs) reveals that budget deficits have a significant effect on: private consumption, private investments, money supply (M3), treasury bills rate, current account and real GDP.

Aero and Ogundipe (2018) evaluates the effects of budget deficits on Nigeria economic growth from 1981-2014. The study uses time series data sourced from Central Bank of Nigeria Statistical Bulletin (2015).The study establishes an optimal budget deficit level using the Threshold Autoregressive model. The empirical analysis supports the existence of a significant positive relationship between economic growth and the regressors, capital, labour, inflation rate, and trade openness. On the other hand, the study finds that a significant negative relationship exists between fiscal deficits, financial depth and economic growth in Nigeria.

Kasasbeh and Alzoub (2018) observes the effect of deficit financing on economic stability in Jordan during the period 2005-2017. The study uses time series data sourced from Central Bank of Nigeria Statistical Bulletin (2017).The study uses Vector Error Correction Model (VECM) as its estimation technique. The result shows that external borrowing (EBDT) and domestic bank (BANK) negatively affect economic stability in Jordan. Also, Public Debt is mainly channeled to current expenditures at the expense of capital expenditures, which has a minimal impact on growth. Interest rate (REPO) effect is in line with the theory as higher rates lead to lower growth.

Munir, Binta and Alhaji (2018) reviews the effect of deficit financing on economic growth in Nigeria for the period 1981-2016 using data from the Central Bank of Nigeria Statistical Bulletin. The study uses the Augmented Dickey Fuller technique to test for the stationarity properties of the time series variables and the ARDL technique for the regression analysis. The results shows that domestic financing, exchange rate and domestic private investment have negative and significant impact on growth while interest rate, surprisingly, has a positive impact.

Theoretical Framework

There are many theories that explained budget deficit financing and economic growth. According to Neo-classical theory, budget deficit leads to higher interest rates which discourage output growth. Ricardian theory states that governments may either finance their spending by taxing current taxpayers, or may borrow money to boost output growth. The study is anchored on Keynesian theory of deficit financing. This is because Keynesianism becomes associated with an increase level of government intervention in the economy, mostly through deficit financing and other fiscal measures to manage aggregate demand in an attempt to achieve best policy performance. The theory also adopted because it sees the economy as inherently unstable and needs to be stabilized through active government intervention and/or appropriate policies of government. This theory is also relevant to this study because according to it, an increase in government spending through the use of borrowed money cause an upward shift on the aggregate demand curve. Thus, the theory considered the assumption of full employment by the classical theory as unrealistic. Hence, if the economy is working at less than full employment level of national income so that output gap exists in the economy, the increase in debt financed government expenditure will bring expansion on output and income.

METHODOLOGY

The research employs time series data from 1986 to 2021, chosen due to the country policy shift in 1986, also known as the structural adjustment era. This period of time allows for the necessary statistical testing to determine the significance effect of public deficit financing on economic growth in Nigeria. The data was obtained from the Central Bank of Nigeria (CBN) Statistical Bulletin 2021, the National Bureau of Statistics (NBS), the World Bank Development Indicator (WDI, 2020), and the World Governance Indicator (2020). Real Gross Domestic Product (RGDP) was the dependent variable, while the control variables were the tax to GDP ratio [TGR], corruption perception index [CPI], political stability index [PSI], oil price fluctuation [OPF], and exchange rate fluctuation [ERF]. The domestic debt consisted of treasury bill [TEB] and treasury bond [TRB]; the external debt consisted of bilateral and multilateral debt [MLD]; and the oil revenue to total revenue ratio [OTR], non-oil revenue to total revenue ratio [NOR], and external reserve [ETR].

Model Specification

This kind of research utilized the model from Nwanna and Nkiruka’s (2019) work, which makes use of relevant variables including real GDP, domestic debt, and external debt. With some modifications, the current study divided the debt into two categories: domestic debt, which was divided into Treasury bills and Treasury bonds, and external debt, which was divided into bilateral and multilateral debt. Additionally, other variables were added, including the ratio of oil revenue to total revenue, the ratio of non-oil revenue to total revenue, the external reserve, and other control variables like the tax to GDP ratio, the corruption perception index, the political stability index, the fluctuation in oil prices, and the exchange rate.

The Non-Linear Autoregressive Distributive Lag (NARDL) is used in this study. The reason for this is because although the typical ARDL (Linear ARDL) model makes it possible to assess the long-term relationships between time series variables, it only makes the assumption that these relationships would be linear or symmetric. Because of this, the linear ARDL model, which is based on the assumption of symmetric dynamics, is unable to account for the potential Non-linearity or asymmetry that exists in the relationship between the sources of government deficit funding and the chosen, volatile macroeconomic variables. In light of this, this study adopts the Nonlinear ARDL (NARDL) approach, which was developed by Shin et al. (2014) as an asymmetric extension to the linear ARDL model. The NARDL model was designed to capture both short run and long run asymmetries in a variable of interest, while reserving all merits of the linear ARDL approach (Cheah, Yiew and Ng, 2017).

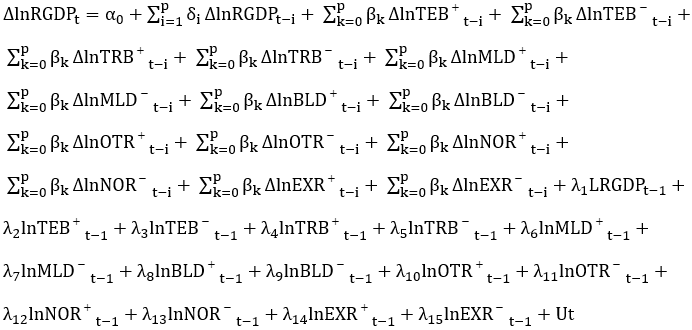

In the N-ARDL model, asymmetric/non-linear explanatory variables were split into their positive and negative partial sum series. However, the positive partial sum series captures the increase of the explanatory variable while the negative partial sum series reflects the decrease of the explanatory variable (Pal and Mitra, 2016). In order to develop a NARDL model, the independent variables TEB, TRB, MLD, BLD, OTR, NOR, EXR are assumed to have nonlinear relationship with the dependent variable RGDP is split into two parts: TEB+, TRB+, MLD+, BLD+, OTR+, NOR+, EXR+; and TEB–, TRB–, MLD–, BLD–, OTR–, NOR–, EXR–as partial sums corresponding to the positive and negative changes of independent variables.

Following the splitting of the independent variables, the NARDL model for this study were specified as showed below: In order to determine the impact of public budget deficit financing on economic growth in Nigeria, The NARDL model specification is shown in Equation [1]

RESULTS AND DISCUSSION OF FINDINGS

Descriptive Statistics

Table 1

| Variable | Mean | Std | Max | Min | Skewness | Jarque-Bera | Probability |

| RGDP | 1.562 | 0.034 | 58.815 | 24.456 | 1.264 | 5.955 | 0.140 |

| TEB | 8.457 | 2.983 | 4.933 | 1.454 | 0.115 | 4.603 | 0.010 |

| TRB | 3.452 | 1.785 | 14.002 | 13.503 | 1.109 | 9.666 | 0.030 |

| MLD | 2.454 | 0.299 | 92.271 | 56.345 | 0.170 | 5.827 | 0.000 |

| BLD | 3.678 | 1.110 | 18.068 | 5.676 | 0.021 | 4.762 | 0.010 |

| OTR | 8.509 | 2.401 | 68.939 | 23.452 | 0.145 | 6.044 | 0.027 |

Source: Researcher’s Computation using Eviews 10.0

Note: * indicates significant at five percent level of significance.

Table 4.1 indicates that all the variables of interest were not normally distributed. This is evidence as the results of the JB test confirmed the rejection of the null hypothesis at 5% level of significance, which means that all the variables were not normally distributed. The absence of normality in the variables is evident as all the variables of interest probability values were less than 0.05 level of significance except for RGDP which is above 0.14. Thus, since the variables were not normally distributed, there was a need to carryout unit root test for stationarity.

Table 2: Augmented Dickey Fuller (ADF) Statistic Results for Unit Root

| Variables | ADF Statistic at level | ADF Statistic at first difference | Critical values of 5% at level | Critical values of 5% at first difference | P-values at level | P-values at first difference | Order of integration |

| RGDP | -1.211 | -7.345 | -2.965 | -2.973 | 0.456 | 0.000* | I(1) |

| TEB | -2.349 | -9.234 | -2.965 | -2.973 | 0.366 | 0.000* | I(1) |

| TRB | -1.587 | -6.123 | -2.965 | -2.973 | 0.238 | 0.001* | I(1) |

| MLD | -3.454 | – 2.056 | -2.965 | -2.973 | 0.010* | 0.471 | I(0) |

| BLD | -1.345 | -7.435 | -2.965 | -2.973 | 0.450 | 0.000* | I(1) |

| OTR | -1.322 | -7.345 | -2.965 | -2.973 | 0.456 | 0.001* | I(1) |

| NOR | -1.208 | -9.221 | -2.965 | -2.973 | 0.071 | 0.034* | I(1) |

| EXR | -3.590 | – 1.689 | -2.965 | -2.973 | 0.000* | 0.791 | I(0) |

| TGR | -1.349 | -7.123 | -2.965 | -2.973 | 0.131 | 0.000* | I(1) |

| CPI | -3.454 | – 3.098 | -2.965 | -2.973 | 0.021* | 0.520 | I(0) |

| PSI | -1.345 | -6.435 | -2.965 | -2.973 | 0.521 | 0.000* | I(1) |

| OPF | -3.454 | -2.456 | -2.965 | -2.973 | 0.000* | 0.492 | I(0) |

| ERF | -1.345 | -5.789 | -2.965 | -2.973 | 0.560 | 0.000* | I(1) |

Source: Researcher’s Computation using Eviews 10.0

Note: * indicates significant at five percent level of significance.

The study carries out ADF unit root test as shows in Table 2 to determine whether the variables are stationary or not using the Augmented Dickey Fuller (ADF) Statistic. Obviously, the ADF unit root test results on Table 4.2 shows that all the variables of interest (Real Gross Domestic Product [RGDP] as proxy for economic growth being the dependent variable while domestic debt (treasury bill [TEB] and treasury bond[TRB]), external debt (multilateral debt [MLD] and bilateral debt [BLD]), oil revenue to total revenue ratio[OTR], non-oil revenue to total revenue ratio [NOR], external reserve [EXR] which formed the independent variables as proxy for public budget deficit financing including other variables of interest like; tax to GDP ratio [TGR], corruption perception index [CPI], political stability index[PSI], oil price fluctuation [OPF] and exchange rate fluctuation [ERF]) maintained mixed order of stationarity as some were stationary at level while others were stationary at first difference. This is established by comparing the ADF value with their respective critical value at 5% level of significant. Judging by the order of integration I(0) and I(1) its suggest that there may be existence of long-run relationship between the variables. Thus, Autoregressive Distributive Lag Bound Co-Integration Test is employed to ascertain the existence of long-run relationship between the variables in the model.

Table 3: NARDL Bounds Co-integration Test Results

| F-Bounds Test | Null Hypothesis: No levels relationship | |||

| Test Statistic | Value | Signif. | I(0) | I(1) |

| F-statistic | 27.884 | 10% | 1.894 | 2.891 |

| K | 17 | 5% | 2.175 | 3.237 |

| 1% | 2.738 | 3.912 | ||

Source: Researcher’s Computation using Eviews 10.0.

Table 3 shows that the F-statistic (27.884) was greater than both the lower bound and upper bound critical values at 5% level of significance, which implies that there is the existence of long run relationship at 5%level of significance. This means that the Null Hypothesis will be rejected, thereby accepting the alternative; thus, implying that there is existence of long-run relationship public deficit financing and economic growth in Nigeria. Therefore, we employed both the Long-run and the short estimate to ascertained the relationship between the variables and the adjustment speed within the short run which is presented in table 4

Table 4: Estimated Short Run NARDL Result

| Dependent Variable: D(lnRGDP) | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 0.659 | 1.598 | 0.412 | 0.322 |

| D(lnRGDP) | 0.346 | 0.024 | 13.963 | 0.000* |

| D(lnTEB+) | 0.530 | 0.084 | 6.278 | 0.028* |

| D(lnTEB–) | -0.475 | 0.109 | -4.368 | 0.016* |

| D(lnTRB+) | 0.401 | 0.064 | 6.227 | 0.002* |

| D(lnTRB–) | -0.304 | 0.076 | -4.003 | 0.003* |

| D(lnMLD+) | -0.588 | 0.087 | -6.720 | 0.017* |

| D(lnMLD–) | -0.742 | 0.631 | -1.176 | 0.765 |

| D(lnBLD+) | -0.212 | 0.023 | -9.217 | 0.043* |

| D(lnBLD–) | -0.482 | 0.079 | -6.093 | 0.004* |

| D(lnOTR+) | 0.348 | 0.054 | 6.407 | 0.000* |

| D(lnOTR–) | -0.374 | 0.080 | -4.651 | 0.009* |

| D(lnNOR+) | 0.097 | 0.056 | 1.728 | 0.107 |

| D(lnNOR–) | -0.536 | 0.631 | -0.850 | 0.410 |

| D(lnEXR+) | 0.732 | 0.322 | 2.273 | 0.032* |

| D(lnEXR–) | -0.710 | 0.098 | -7.211 | 0.000* |

| ECT(-1) | -0.645 | 0.092 | -7.044 | 0.009* |

Source: Researcher’s Computation using Eviews 10.0

Note: * indicates significant at five percent level of significance.

The short run form of the NARDL estimate in Table 4 accounted for the speed of adjustment to long run equilibrium of the variables used. For this reason, the speed of adjustment of the model to long run equilibrium was determined by the coefficient of the first lag of the Error Correction Term (ECT(-1)). The Error Correction Term (-0.65) has the right a priori sign and it was statistically significant. Hence, the result of the ECT (-1) shows that 65% of the deviation of the variables in the short run would be restored in the long run within one year.

Table 5: Estimated Long Run NARDL Result

| LnRGDP | 0.329 | 0.288 | 1.143 | 0.621 |

| lnTEB+ | 0.458 | 0.085 | 5.377 | 0.004* |

| lnTEB– | -0.538 | 0.075 | -7.225 | 0.015* |

| lnTRB+ | 0.483 | 0.053 | 9.043 | 0.006* |

| lnTRB– | -0.506 | 0.064 | -7.859 | 0.000* |

| lnMLD+ | -0.622 | 0.074 | -8.375 | 0.000* |

| lnMLD– | -0.394 | 0.087 | -4.507 | 0.000* |

| lnBLD+ | -0.568 | 0.088 | -6.447 | 0.001 |

| lnBLD– | -0.710 | 0.098 | -7.211 | 0.000 |

| lnOTR+ | 0.541 | 0.066 | 8.092 | 0.000 |

| lnOTR– | -0.454 | 0.079 | -5.722 | 0.009 |

| lnNOR+ | 0.366 | 0.087 | 4.200 | 0.002 |

| lnNOR– | -0.345 | 0.024 | -3.963 | 0.000 |

| lnEXR+ | 0.474 | 0.108 | 4.367 | 0.016 |

| lnEXR– | -0.401 | 0.064 | -6.226 | 0.001 |

| R-squared | 0.816 | Durbin-Watson stat | 1.746 | |

| Adjusted R-squared | 0.707 | |||

| F-statistic | 17.375 | |||

| Prob(F-statistic) | 0.000 | |||

Source: Researcher’s Computation using Eviews 10.0

Note: * indicates significant at five percent level of significance.

Table 5 above shows the long run coefficients of treasury bill [TEB] and treasury bond[TRB], multilateral debt [MLD] and bilateral debt [BLD], oil revenue to total revenue ratio[OTR], non-oil revenue to total revenue ratio [NOR] and external reserve [EXR], respectively. Based on the long run results of the NARDL, all the variables are statistically significant at 5% level and are asymmetric in nature unless for bilateral debt [BLD] which is symmetric and positive in nature, implying that a positive changes in bilateral debt led to 57% increase in economic growth and the negative changes in bilateral debt led to 71% decrease in economic growth in the Nigerian economy. Also the result also show that a policy change on treasury bills, treasury bond [TRB], multilateral debt [MLD], oil revenue to total revenue ratio [OTR], non-oil revenue to total revenue ratio [NOR] and external reserve [EXR] will have a direct effect on economic growth in the long run in Nigeria. Meaning it has the potential of impacting on economic growth in the Long-run if fully utilized. This is evident as the positive changes in treasury bills led to 46% increase in economic growth and the negative changes in treasury bills led to 54% decrease in economic growth in the Nigerian economy.

Also a positive changes in multilateral debt led to 62% increase in economic growth and the negative changes in multilateral debt led to 39% decrease in economic growth in the Nigerian economy, while a positive changes in bilateral debt also led to 57% increase in economic growth and the negative changes in bilateral debt led to 71% decrease in economic growth in the Nigerian economy, a positive changes in oil revenue to total revenue ratio will also led to 54% increase in economic growth and the negative changes in oil revenue to total revenue ratio led to 45% decrease in economic growth in the Nigerian economy. Also, the positive changes in non-oil revenue to total revenue ratio led to 37% increase in economic growth and the negative changes in non-oil revenue to total revenue ratio led to 35% decrease in economic growth in the Nigerian economy, while a positive changes in external reserve led to 47% increase in economic growth and the negative changes in external reserve led to 40% decrease in economic growth in the Nigerian economy respectively.

Finally, the result also indicates that the independent variables such as; treasury bill [TEB] and treasury bond [TRB], multilateral debt [MLD] and bilateral debt [BLD], oil revenue to total revenue ratio [OTR], non-oil revenue to total revenue ratio [NOR] and external reserve [EXR] explained about 82% of the total variation in Real Gross Domestic Product (RGDP) as proxy for economic growth while the remaining 18% unexplained was captured by the error term. Considering the prob (F-statistic) of 0.000, which is less than 0.05, it implies that all the parameter estimates in the long run NARDL model are statistically significant. The Durbin Watson statistic of 1.746 showed absence of autocorrelation or serial correlation in the model. This is because it is approximately less than ‘2’ being the rule of thumb.

DISCUSSION OF FINDINGS

The trust of this research work is to examine the effect public budget deficit financing and performance of selected macroeconomic indicators in Nigeria. The study uses NARDL estimation technique and Granger Causality test. The study discovers that all the variables used in the study had an asymmetric impact on economic growth in Nigeria accept of Treasury Bonds which happen to be symmetric in nature. This is evident as the positive variables used in the study led to increase in economic while negative changes in variables led to decrease in economic growth in the Nigerian economy.

This finding agrees with the conclusion of Nwanna and Nkiruka (2019) who reveals that deficit financing through external debt borrowing has a significant negative effect on Nigeria’s economic growth. Also, it is similar to that of Okah, Chukwu and Ananwude (2019) who discloses that deficit financing has positive but insignificant effect on Nigerian economic growth. In addition, the finding conforms to the outcome of Nwaeke and Korgbeelo (2016) who observes that deficits financed from external loans have insignificant negative influence on economic growth while deficits financed from domestic sources stimulate economic growth in Nigeria. In the same way, according to Monogbe, Dornubari and Emah (2015), deficit financing through foreign borrowing has a significant association to economic performance in the Nigerian context but a contagious implicating effect. In summary, the study reveals that the positive and negative changes in public budget deficit financing had significant impact on economic growth in the Nigerian economy.

CONCLUSION

Based on the specific objectives of this research work as regards to the empirical, expectations and NARDL estimates. Public budget deficit financing is necessary to enhance economic growth in the Nigerian economy. However, dialectically, public budget deficit financing sources such as; treasury bills, treasury bonds, multilateral debt, bilateral debt, oil revenue to total revenue ratio, non-oil revenue to total revenue ratio and external reserve had significant positive and negative impacts on economic growth in the Nigerian economy within the study period. However, specifically, public budget deficit financing sources such as; treasury bills, treasury bonds, oil revenue to total revenue ratio, non-oil revenue to total revenue ratio and external reserve had asymmetric impacts on economic growth in the Nigerian economy within the period under review. Particularly, multilateral debt and bilateral debt had symmetric impact on economic growth in the Nigerian economy.

Finally, the research work conclude that tax to GDP ratio, corruption perception index, political stability index, oil price fluctuation and exchange rate fluctuation had asymmetric impacts on budget deficit financing in Nigeria. This was because the positive and negative changes in tax to GDP ratio, corruption perception index, political stability index, oil price fluctuation and exchange rate fluctuation had significant impact on budget deficit financing in the Nigerian economy. Hence, it was concluded that tax to GDP ratio, corruption perception index, political stability index, oil price fluctuation and exchange rate fluctuation were significant determinants of the magnitude of budget deficit financing in Nigeria within the period of the study. Generally, the study concludes that the imposition of a linear symmetric in modeling public budget deficit financing in the country could be misleading as far as Nigerian economy is concerned. Hence, the use of NARDL model for public budget deficit financing contributes to the understanding of the nonlinear dynamics between public budget deficit financing and the performance of selected macroeconomic indicators, thereby leading to more effective and efficient forecasting and policymaking.

RECOMMENDATIONS

The following policy recommendations were made based on the findings in the study.

- Government at all tiers in the country should maintain high level of fiscal discipline in order to ensure optimal utilization of treasury bills, treasury bonds, oil revenue to total revenue ratio, non-oil revenue to total revenue ratio and external reserve towards realizing the desired level of economic growth in the Nigerian economy. This can be achieved if government budget deficit sources of financing are contracted for economic stability reasons and not for political reasons, and properly channeled to productive sector of the economy that will enhance economic growth target of the country.

- Government at all tiers in the country should adhere to fiscal discipline through efficient use of tax to GDP ratio, reduction in corruption, maintenance of political stability, optimal control of oil price and exchange rate fluctuations towards achieving sustainable level of economic growth in Nigerian economy.

REFERENCES

- Acha, I.A & Essien, J. M (2018). Economic growth imperative of foreign portfolio investment for Nigeria. Noble International Journal of Economics and Financial Research, 3(6), 71-77.

- Adofu, I and Abula, M (2010): “Domestic Debt and the Nigerian Economy”. Current Research Journal of Economic Theory, 2(1), 22-26.

- African Development Bank Group, 2022). https://www.afdb.org/en/countries-west-africa-nigeria/nigeria-economic

- Audu F.O. (2021). Relationship between budget deficit and economic growth in Nigeria. Nigerian Journal of Economics Development Matters, 4 (6),103-112.

- Aero, O. & Ogundipe A.A (2018).Fiscal deficits and Nigeria economic growth. International Journal of Economics and Financial Issues, 8(3), 296-306.

- Ayodele, B. & Tunde O. (2012), budget deficit and economic performance in Nigeria. Arabian Journal of Business and Management Review 1(10), 45-62

- Adebowole S. O. (2021). The relationship between government deficit financing and economic growth in Nigeria. British Journal of Economics, Management and Trade, 4(11), 1624-1643.

- Anyawakoro, N.E. (2018). Effect of budget on trade deficit in Pakistan: A Time Series Analysis. Journal of Finance and Economics, 2(5): 145-148.

- Aminu, Hamidu and Musa (2013),’’ External Debt and domestic debt impact on the growth of the Nigerian economy‘’- International journal of educational research 2013, volume 1 issue 2.

- Awe, A.A., & Shina, O.S. (2017).The nexus between budget deficit and inflation in the Nigerian economy. Research Journal of Finance and Accounting, 3(10), 78-92.

- Barro, R.J. (2020). Government spending, interest rates, prices and budget deficits in the United Kingdom, 1701-1918.Journal of Monetary Economics, 2(20), 221-247.

- Central Bank of Nigeria (2020).Economic and Financial Review, Abuja, CBN

- Chimobi, E.A & Igwe, J.H (2019). Deficit financing and its implication on private sector investment: The Nigerian experience. Arabian Journal of Business and Management Review.1(10),15- 23.

- Chukwu, L.C, Otiwu, K. & Okere P.A. ACIB (2020). Impact of budget deficit on macroeconomic variables of Nigeria. International Journal of Science and Management Studies, 3(4), 135-150.

- Joseph, C., & Godwin, K. (2021). Relationship between budget deficit and economic growth: evidence. Journal of Economic Cooperation among Islamic Countries, 29(2): 1-14.

- Kasasbeh, A. & Alzoub P. (2018). Effect of deficit financing on economic stability in Jordan. International journal of business and economic review, 3(7), 1234-1260

- Kemi, F. A. & Dayo, B. O. (2020). Unemployment and economic growth in Nigeria. Journal of Economics and Sustainable Development, 5(4): 138-144.

- Keynes J.M (1936). The general theory of employment, interest and money. London and New York: Macmillan,

- George, A. & Kosimbei, G.K (2019). Budget deficits and macroeconomic performance in Nigeria. A thesis submitted to the School of Humanities and Social Sciences, in fulfillment of the requirements for the award of Doctor of Philosophy Degree in Economics of Kenyatta University.

- Muhammad, Z. (2021), Budget deficit and interest rate: an empirical analysis of Pakistan.

- Munir, B.A Binta, M. & Alhaji, I.M (2018). Impact of deficit financing on economic Growth in Nigeria. Global Journal of Management and Business Research,18(3), 28-36.

- Najid, A. (2021). The role of budget deficit in the economic growth of Pakistan. Global Journal of Management and Business Research Economics and Commerce, 13(2) 1-5.

- Natalia, A. (2018). An Assessment of the relationship between budget deficit and Economic growth in Namibia.(Master’s thesis).University of Namibia.

- Nwaeke, G.C & Korgbeelo, C. (2016). Budget deficit financing and the Nigeria Economy. European Journal of Business and Management, 8(22), 206-214

- Nwambeke G.C (2020). Empirical analysis of the impact of fiscal policy on economic growth in Nigeria. International journal of economics and finance, 6(6), 1916-9728

- Nwanna, I.O & Nkiruka, U.G (2019). Effect of deficit finance on Nigeria economic growth. International Journal of Economics and Financial Management, 4(1) 28-49.

- Ohiaeri, N.V. (2017). Economic growth, capital flight and capital market performance in Nigeria. International Journal of Economics, Commerce and Management United Kingdom, 5(9), 352-567.

- Okah, J.O., Chukwu, K.O. &Ananwude, A.C. (2019). Effect of deficit financing on economic growth of Nigeria. Asian Journal of Economics, Business and Accounting, 12(1): 1-13.

- Oladejo, T.B. (2019). Empirical evaluation of the effect of budget deficit on Nigerian economic growth. International Journal of Comparative Studies in International Relations and Development, 4(1), 161-174.

- Oladipo, S. O. & Akinbobola T.O. (2019). Budget deficit and inflation in Nigeria: A causal relationship, Journal of Emerging Trends in Economics and Management Sciences. 2(1), 1-8.

- Oluwole, F.O., Solawon, M.D. & Odueke, H.A. (2020). Budget deficit and inflation on economic development in Nigeria. Journal of Economics and Finance, 11(3), 16-23.

- Onwioduokit, E.A. & Bassey, G.E. (2019). Fiscal deficit and economic growth in the Gambia. International Journal of Current Research and Review, 5(22), 162-181.

- Onwe, M. N. (2018). Debt Burden (Sustainability) Indicators. Paper Presented at Regional Course on Debt Recording and Statistical Analysis, Organizedby WAIFEM, Lagos,

- Pal, D., & Mitra, S. K. (2016). Asymmetric Oil Product Pricing in India: Evidence from a Multiple Threshold Nonlinear ARDL Model. Economic Modelling, 59, 314-328.

https://doi.org/10.1016/j.econmod.2016.08.003 - Sameh, A.T. (2017).The budget deficit, public debt and endogenous growth. Journal of Economics, 63 (41),1-15

- Shin, Y., B. Yu, & Greenwood-Nimmo, M.J. (2014). Modelling asymmetric cointegration and dynamic multipliers in a Nonlinear ARDL Framework. In Sickles R., Horrace W. (eds). Festschrift in Honor of Peter Schmidt. Springer, New York, NY.

- Sriyan, J. (2020). Fiscal policy and economic growth: An empirical evidence from Malaysia and Indonesia. Journal Ekonomi Pembangunan, 7(2): 143-155.

- Siew-Pong Cheah & Thian-Hee Yiew & Cheong-Fatt Ng, 2017. “A nonlinear ARDL analysis on the relation between stock price and exchange rate in Malaysia,” Economics Bulletin, AccessEcon, 37(1), 336-346.

- Stiglitz J. E (2005). Fair Trade for all: how trade can promote economic growth and development, International Journal of Business, 23: 54

- Sunday O. & Philomena (2020). Fiscal deficits and macroeconomic variables in Nigeria. International Journal of Accounting Research, 6(1), 1-13.

- Soludo, C.C. (2003) The Debt Trap in Nigeria: Towards a Sustainable Debt Strategy. Africa World Press, New Jersey.

- Taiwo, A.S & Agbatogun, K.K (2012).Government expenditure in Nigeria: A Sine Qua Non for Economic Growth and Development. Journal of Research in National Development, 9(2), 155-162.

- World Bank (2020). Economic growth at a Glance. World Bank Report, Washington