Public Debt and Economic Growth: Empirical Evidence from Nigeria

- Callistus Tabansi Okeke

- Chinwe Ann Anisiobi

- Chinwe Monica Madueke

- 705-718

- Apr 13, 2023

- Economics

Public Debt and Economic Growth: Empirical Evidence from Nigeria

Callistus Tabansi Okeke, Chinwe Ann Anisiobi and Chinwe Monica Madueke

Department of Economics, Nnamdi Azikiwe University Awka, Nigeria

DOI: https://doi.org/10.47772/IJRISS.2023.7309

Received: 26 January 2023; Revised: 31 January 2023; Accepted: 02 February 2023; Published: 13 April 2023

ABSTRACT

This study examined the impact of public debt on economic growth in Nigeria using annual secondary data from 1981 to 2021 and the Auto-Regressive Distributed Lag technique. The variables used in the study were real gross domestic product (RGDP), which is the proxy for economic growth, gross fixed capital formation (GFCF), external debt (EXDT), exchange rate (EXCR), domestic debt (DODT) and debt service repayment (DSRT). The results of the findings show that the past value of RGDP, GFCF, EXDT and DSRT have positive impact on economic growth in Nigeria. Also, EXCR and DODT have negative impact on economic growth in Nigeria. Judging from the p values, the lagged value of RGDP, GFCF, EXDT and DSRT are statistically significant as their p values are lower than critical values at 5 percent level of significance, while EXCR and DODT have no significant impact on economic growth in Nigeria. Based on the findings, the study recommends that government should formulate and effectively implement policy that would boost domestic revenue generation by broadening the revenue base, improving capacity to tax and curtailing ineffective government spending. Also, borrowed funds should be utilized for the diversification of the productive base of the economy.

Keywords: ARDL, Domestic debt, External debt, Nigeria, Public debt

JEL Classification: H60, H63, C20

INTRODUCTION

Public debt is an important instrument for governments to fund public spending, particularly when it is difficult to raise taxes and reduce public expenditure. For many years, this process has left most governments with huge debt burden. Borrowings to finance capital infrastructural development are the solution to faster economic growth (Ogunjimi, 2019). But excess borrowings without appropriate planning for investment may lead to heavy debt burden and interest payment, which in turn may create several undesirable effects for the economy (Joy & Panda, 2020). Public debt is a financial incentive but when its buildup gets to a very substantial level, a reasonable proportion of government expenditure and foreign exchange earnings will be used to repay the debt with a high opportunity cost for upcoming generations.

Public debt could be either internal (domestic) or external (foreign). Adofu and Abula (2010), defined domestic debt as debt instruments issued by the Federal Government and denominated in local currency. As stated by Todaro and Smith (2011), external debt is the total private and public foreign debt owed by a country. Ajie, Akekere and Ewubare (2014), defined external debt as an unpaid portion of external resources acquired for developmental purposes and balance of payments support, which could not be repaid when they fell due. In other words, external debts are debts owed by a country to institutions of countries abroad, that is, the creditors are foreigners, which in case its servicing and repayment will mean a drainage of national resources in favour of those foreigners.

Some conventional economists states that public debt has a positive effect on economic growth in the short-run by stimulating effective demand and output. However, theoretical literature continues to point to a negative debt-growth relation in the long run by crowding out private investment. Public debt can crowd-out private investment and threaten economic growth through higher long-term interest rates, higher inflation, and higher future distortionary taxation (Mhlaba Phiri & Nsiah, 2019) . The increasing debt burden of Nigeria is pointing toward another debt crisis. It is evident that unsustainable public debt is discouraging investment and lowering growth in Nigeria, thereby reducing the country’s global competitiveness, and increasing financial market susceptibility to international shocks (Ogbonna, Ibenta, Chris-Ejiogu, &Atsanan, 2019). Moreover, debt sustainability can be explained using either debt to GDP or debt service to revenue ratio. Nigeria’s debt to GDP ratio is estimated at about 35.71%, one of the lowest in the world and much below what is obtainable in most emerging markets (DMO, 2021). For now, debt-to-GDP is not regarded as the best indicator of debt sustainability, especially in a country like Nigeria that has one of the lowest tax-to-GDP ratio (6.1%) in the world (DMO,2021). According to IMF (2021), a better indicator of debt sustainability is the debt service-to-revenue ratio, which is estimated at 86%, a metric that reveals whether the government is generating enough revenues to pay down its debts as they mature. The debt service to revenue ratio which in Nigeria has in recent years risen to worrying levels, leading investigators to ask if the country is broke or heading to insolvency.

Nigeria’s public debt hit N38.005 trillion by third quarter of 2021. The government spent about 4.2 trillion Naira on debt servicing in 2021, out of total revenue of N5.51 trillion. The rising debt profile of Nigeria reached a new milestone with the country’s debt service as a percentage of revenue rising to 76.2% in 2021(NBS,2021). This shows that 76.2% of the revenue generated in 2021 was used for debt servicing. The government constant borrowing from the domestic market limits the private businesses from assessing funding for business growth and development (Ogunjimi, 2019). When a country spends significant parts of its revenue on servicing huge debts, it has very little left to fund critical infrastructures which in turn affect growth negatively. Furthermore, the National Bureau of Statistics (NBS) 2019 Poverty and Inequality report in Nigeria indicated that 40.09% of the total population lives below the country’s poverty line showing the low levels of opulence in Nigeria. Over the years, the governments of Nigeria have enunciated several debt management approaches to reduce the burden of foreign debt on the economy and ensure sufficient economic growth and development. Such approaches include rescheduling the debt, debt conversion or liquidation. Available evidence revealed that the various strategies used in managing Nigeria’s public debt have not achieved their desired objectives.

Even with the declining revenue, recurrent expenditure of the government has been high and aligned with financial expectations while capital expenditure continues to decline over the years. The decrease in Nigeria’s revenue brings about doubt if Nigeria is financially competent or not. It raises questions regarding the country, if the nation is facing a revenue problem or a debt problem? With the growing insecurity and induced recession in the economy, government revenues, in particular, non-oil revenues could remain low for a longer period. This means the government will still need to rely on borrowing to fund its operations, putting more pressure on Nigeria’s debt service to revenue ratio.

Nigeria is a preference for this study because of the rapid increase in government debt, declining revenue generation and the decrease in the nation’s foreign reserve. The conflict between increase in government debt and debt service payment surrounded by low growth rate in Nigeria is of particular interest to researchers and policy makers. This inspired this study to investigate the long run and short run impact of the accelerating public debt on Nigeria’s economic growth. The findings of this study would have direct policy implications, especially on government fiscal measures and investment decisions. The results are expected to guide policymakers in the design of an effective public debt strategy that is conducive for Nigeria’s economic growth. The remaining parts of this paper were structured into literature review, methodology, results and discussion, as well as conclusion and recommendations.

REVIEW OF RELATED LITERATURE

Public debt in Nigeria has hindered growth and development, including worsening social issues. Nigeria’s expected debt service is seen to be increasing function of her output and as such resources that are to be used for developing the economy are indirectly taxed away by foreign creditors in form of debt service payments. This has further increased uncertainty in the Nigerian economy which discourages foreign investors and also reduces the level of private investment in the economy. Debt burden is the financial crisis arising from debt repayment due to constant interest payment from government revenue and foreign reserves. The use of government revenue to finance interest payments on public debt directly hinders the disposable income and domestic savings in the indebted country (Balago, 2014). Similarly, Sachs (1989) indicated that in a situation where revenue mobilization was geared towards debt servicing; economic instability was likely to occur since it created much leakage in the domestic economy; Nigeria has accumulated huge debt with rising cost of debt service which has undermined economic stability as domestic investments are being crowded out by rising cost of debt servicing. This implies that constant debt servicing diverts investments from economically productive activities, since government revenue is used to cushion interest payments on borrowed funds, thus hindering budget implementation, creating further budget deficit and debt burden. The need to explain the problem of public indebtedness of both developed and developing countries have given rise to a number of theoretical postulates over the years. The outstanding theory that has gained popularity in economics and literature is the debt over hang hypothesis.

Debt Overhang Hypothesis

Debt-overhang theory states that a country’s debt is more than its debt repayment ability. Ezirim (2005) explains the debt overhang hypothesis as one where the accumulated stock of debt acts as a tax on future income and production, and thereby acts to impede investments by turning away the private sector (foreign and domestic) investors. The “debt overhang effect” comes into play when accumulated debt stock discourages investors from investing in the private sector for fear of heavy tax placed on them by government. This is known as tax disincentive. The tax disincentive here implies that because of the high debt and as such huge debt service payments, it is assumed that any future income accrued to potential investors would be taxed heavily by government so as to reduce the amount of debt service and this scares off the investors thereby leading to disinvestment in the overall economy and as such a fall in the rate of growth (Ayadi & Ayadi, 2008). According to Krugman (1988), accumulated public debt act as a tax on future output as well as reduces the incentive for savings and investment. In particular, the theory argued that the requirement to service debt reduces funds available for investment purposes; hence, a binding liquidity constraint on debt would restrain investment and further retard growth.

The theory holds that both the stock of public debt and its service affect growth by discouraging private investment or altering the composition of public spending. Debt service may discourage growth by squeezing the public resources available for investment in infrastructure and human capital (Coccia, 2017). When a country’s debt service burden is huge that a large proportion of output accrues to foreign lenders it will create disincentive to invest. Moreover, when investments are discouraged in an economy, the rate of capital accumulation will be reduced, and so the rate of economic growth would decline in real terms. Through this channel, high debt stock is said to have a negative influence on economic growth and development (Iyioha, 1977). The theory further suggests that public debt may have non-linear effects on growth, either through capital accumulation or productivity growth. Coccia (2017) argued that the resources used to service massive public debt represent resource drain that should have been available to invest in critical sectors that sustain growth. The cost of servicing huge public debts could take a greater part of government scarce revenue leading to distortions and lower levels of growth in developing countries. Debt overhang is a primary cause of stunted economic growth in heavily indebted countries. As Àkos and Istvàn (2019) explained in the context of poor countries, servicing of high public debts depletes the revenue of the indebted country to such an extent that the ability to return to growth paths is dim, even if the country implement strong reform programmes. According to Kakain (2019), debt overhang states that in future, a country’s debt will exceed the country’s ability to repay. Therefore, the expected debt service will be an aggregate function of the output of the economy. As in Ezirim (2005), high debt stock is harmful and damaging to economic growth and development, especially, in poorer countries. But a decrease in the current debt service will lead to an increase in current investment for any given level of future indebtedness.

Empirical Literature Review

Didia and Ayokunle (2020) disaggregated total public debt into external debt and domestic debt, to investigate whether these two forms of debts had a varying impact on the economic growth in Nigeria. Utilizing the Vector Error Correction Model (VECM) and data covering the period of 1980–2016, the study revealed that domestic debt had a statistically significant positive relationship with economic growth in the long run, while external debt exhibited a negative relationship with economic growth, which was not statistically significant. Udoh, Ekeowa, Okechukwu, Obiora-Okafor and Nwonye (2020) used quarterly data from 2006 to 2018 to explore the influence of inter-generational debt burden on economic prosperity in Nigeria. It was found that debt overhang and debt burden in Nigeria were due to the usage of borrowed funds into unproductive activities such as payment of salaries and allowances, which had hindered economic growth.

Mhlaba Phiri and Nsiah (2019) employ the ARDL method and quarterly data from 2002 to 2016 to examine the long-run and short-run effects of public debt on economic growth for South Africa. The study modelled GDP as a function of gross and net debt, investment, inflation and terms of trade. The empirical results indicated a significant negative impact of public debt on economic growth. The study was based on South African data and provided a basis to examine the impact of government debt on economic growth from a Nigerian-specific perspective. Obayori, Krokeyi and Kakain (2019) investigated the impact of external debt on economic growth in Nigeria for the period 1980 to 2016 using Generalized Method of Moments (GMM). The GMM result revealed a positive and significant relationship between external debt and economic growth in Nigeria.

Saungweme and Odhiambho (2019) explored the causal relationship between government debt, debt servicing and economic growth in Zambia for the period 1979 to 2017 using a dynamic multivariate ARDL approach. To achieve this objective, RGDP was modelled as a function of stock of public debt, fiscal balance and savings as a share of GDP. The empirical results indicated a unidirectional causal relationship from economic growth to public debt in Zambia. The study findings supported the hypothesis that the pace of economic growth matters in defining the level of public sector indebtedness. The study setting was in Zambia thereby creating a geographic gap and the need for a Nigerian- specific study. Ochuko and Idowu (2019) investigated the effect of national debts on economic enhancement in Nigeria from 1981 to 2018. The estimation showed that external debt contributed less to the Nigerian economy, while domestic debt significantly enhanced economic growth. On the other hand, debt servicing cost had a negative and significant influence on economic growth.

Elom-Obed, Odo, Elom-Obed and Anoke (2017) using the Vector Error Correction Model (VECM) and annual data from 1980 to 2015, analyzed the relationship between public debt and economic growth in Nigeria. The study findings revealed a significant negative impact of foreign and domestic debt on economic growth in Nigeria. The study suffered from significant variable omission bias and adopted an inadequate estimation technique that cannot generate reliable coefficient estimates about the study variables. Gómez-Puig and Sosvilla-Rivero (2017) explored the relationship between government debt and economic growth of Euro Area countries using time series data for the period 1961–2013 and the ARDL method. The results indicated a significant negative influence of public debt on long-run performance of the Euro Area member states while the short-run effects may be positive depending on the country. The study looked at Euro countries and provided a basis to examine the impact of public debt on economic growth from a Nigerian-specific perspective.

Udeh, Ugwu and Onwuka (2016) using OLS method and annual data spanning the period 1980–2013 examined the impact of external debt on economic growth in Nigeria. The study modelled GDP as a function of external debt stock, debt service payments and exchange rate. The empirical results indicated that external debt stock and debt service payments impacted growth negatively while exchange rate showed a positive impact. The study concentrated on external debt which is a fraction of total debt stock and used the OLS estimation technique that cannot separate the long- and short-run effect of external debt on growth. Hussain et al. (2015) estimated the linkages between government debts on economic growth of Sub-Saharan Africa from 1995 to 2012. The study applied panel OLS, which indicated that rising debt burden triggered negative trends in an economic growth rate. In a study of South Asian economies, Akram (2013) explored the nexus between public debt and economic growth of Bangladesh, India, Pakistan and Sri Lanka from 1975 to 2011 using panel data estimation techniques. The results showed that both external debt and the cost of debt servicing as well as domestic debt negatively affected economic growth and investments, which showed evidence of debt overhang effect in the economy.

Empirical Gap

The empirical works reviewed shows that most of the study like Didia & Ayokunle (2020), Elom-Obed et al. (2017), Udeh et al. (2016) made use of VECM, OLS and VAR estimation techniques which are not adequate in generating consistent and robust coefficient estimates about the study variables, thereby providing a gap in the methodology used. This study adopted the more advanced ARDL method, which allows for a more robust co-integration and methodologically possible to deal with model selection, estimation, inference and to determine the long run and short run effects of public debt on economic growth in Nigeria. Also, the ARDL method posits the speed of adjustment to restore the economy to long run equilibrium growth path after a shock.

As well, most of the empirical studies were more focused on examining the impact of external debt ( Udeh et al (2016); Obayori et al (2019), on economic growth. Therefore, carrying out a study on only a fragment of a whole would not give an accurate result of the relationship that exists between public debt and economic growth in Nigeria as external debt compose only a portion of government debt stock. Likewise, most of the empirical work chose their control variables at random in modelling the relationship between public debt and economic growth thereby showing their shortcoming by not using most of the important variables stated in the literature. This study incorporated more government debt and growth-related variables in its empirical model to overcome variable omission bias and guide against the identified gap in variables used from previous studies. This study therefore, conducted a multivariate analysis of the relationship between public debt indicators and economic growth in Nigeria that will assist in recommending whether domestic debt or external debt helps to stimulate the level of investment and economic activities in Nigeria. The study also will help to find out if there are evidences of debt overhang in Nigeria. Furthermore, the study uses a relatively long data spanning 41 years than those used in many previous studies. The importance of a longer time series data set in any co-integration analysis cannot be over-emphasized. Also, relying on the findings, this study proffers valuable, pertinent, and practical recommendations for improved policy formulation.

RESEARCH METHODS AND PROCEDURE

This study employed annual secondary data between 1981 and 2021. The data were collected from Central Bank of Nigeria (CBN), the Debt Management Office (DMO), World Bank and IMF statistical database. The macroeconomic variables which data were collected include the Real Gross Domestic Product (RGDP), External Debt Stock (EDS), Domestic Debt Stock (DDS), Debt Service Payments (DSP), Foreign Reserve Position (FRP) all in millions of United States Dollars, Exchange Rate (EXR) and Gross Fixed Capital Formation as a percentage of GDP (GFCF).

Model Specification

This study employed a multivariate debt-growth model to study the relationship between public debt and economic growth in Nigeria. It adopted some key variables specified in the work of Gómez-Puig and Sosvilla-Rivero (2017) with slight changes to suit the requirements of the current study. The choice of the dependent and independent variables used in this study considered underlying economic theories and empirical literatures on the effect of public debt on economic growth in developing countries. The dependent variable used in this study to proxy economic growth was the real GDP growth rate, for the debt variables, the indicators of government debt were separated into domestic and external debts components. This separation was to help evaluate the individual effects of various indicators of government debt on the long run and short run economic growth of Nigeria. Other than the debt variables, different explanatory variables were used as controlling factors that influence economic growth. These control variables were used in this study to moderate the relationship between public debt and economic growth in Nigeria. Such variables included debt service repayment, exchange rate and gross fixed capital formation. The model of Gómez-Puig and Sosvilla-Rivero (2017) is specified as;

Yt = AF(K, L, H, D) (3.1)

Where,

Y is the level of output, A is an index of technological progress, K is the stock of physical capital,

L is labour input, H is human capital, D is public debt stock

The functional relationship of this study’s model is specified as;

RGDP = f(EXDT, DODT, DSTR, EXCR, GFCF) ……………………….(3.2)

Where:

RGDP – Proxy for economic growth, EXDT – External debt, DODT – Domestic debt

DSRT – Debt service repayment, EXCR – Exchange rate, GFCF – Gross fixed capital formation

The econometric form of this model is therefore specified thus;

RGDPt= βo + β1EXDTt + β2DODTt + β3DSTRt + β4EXCRt + β5GFCFt + ut…………… (3.3)

Estimation Technique

The study employed the Autoregressive Distributed Lag (ARDL) methods to examine the relationship between public debt and economic growth in Nigeria. Autoregressive Distributed Lag (ARDL) is a long-established method of estimating co-integrating relationships, such as Engle-Granger (1987) method which requires all variables to be I(1), or require prior knowledge and specification of which variables are I(0) and which are I(1). To alleviate this problem, Pesaran, Shin and Smith (2001) showed that co-integrating systems can be estimated as ARDL models, with the advantage that the ARDL cointegration technique is adopted irrespective of whether the underlying variables are I(0), I(1) or a combination of both, and cannot be applied when the underlying variables are integrated of order I(2). However, to avoid crashing of the ARDL technique and effort in futility, unit roots test of variables were conducted to eliminate any variable that may be integrated at order I(2) which otherwise would have led to the crashing of the technique. In order to establish a long run relationship among the variables the first thing to do is to check the existence of the long run relation between the variables under investigation by computing the Bounds F-statistic (bounds test for cointegration). Also, estimates provided by ARDL method avoid problems such as autocorrelation and endogeneity, they are unbiased and efficient and can accommodate greater number of variables in comparison to vector autoregressive (VAR) models and more flexible with respect to lag structure since it can accommodate different optimal lag structure for different variables in the model, which is not applicable in the other cointegration methods (Rahman & Islam, 2020).

ΔlnRGDP = α0+ ΔlnEXDTt-1 + ΔlnDODTt-1 + ΔlnDSTRt-1 + ΔlnEXCRt-1 + ΔlnGFCFt-1 + α7lnRGDPt-1 + α8lnEXDTt-1 + α9lnDODTt-1 + α10lnEXCRt-1 + α11lnGFCFt-1 + μt (3.4)

Where,

Δ is the first difference operator, p is the optimal lag length for the dependent variable, q is the optimal lag length for the regressors, α1,2,3……6 represent short-run dynamics of the model, α7, α8, α9, α10 and α11 represent the long-run elasticities.

PRESENTATION AND INTERPRETATION OF RESULTS

Lag Selection Criteria

Table 1: Var Lag Selection Criteria

| Endogenous variables: RGDP GFCF EXDT EXCR DSRT DODT | ||||||

| Exogenous variables: C | ||||||

| Sample: 1981 2021 | ||||||

| Included observations: 40 | ||||||

| Lag | LogL | LR | FPE | AIC | SC | HQ |

| 0 | -1871.150 | NA | 2.33e+33 | 93.85750 | 94.11084 | 93.94910 |

| 1 | -1534.712 | 555.1233* | 7.12e+26* | 78.83559* | 80.60891* | 79.47676* |

Source: Researcher’s Computation using Eviews 10.

The optimum lag length for this time series data was selected based on Akaike Information Criterion because it has the lowest value among all the criteria. The decision rule is to select the model that gives the lowest value of these criteria. Lag one is therefore chosen for this model.

Test of Stationarity

Table 2: Summary of Augmented Dickey-Fuller Unit Root Test

Source: Researcher’s Computation using Eviews 10

| Variables | ADF Stat. | Critical Value (5%) | Order of Integration | Prob | Remarks |

| RGDP | -2.966085 | -2.938987 | I (1) | 0.0471 | Stationary |

| GFCF | -3.255320 | -2.936942 | I (0) | 0.0240 | Stationary |

| EXDT | -3.894287 | -2.938987 | I (1) | 0.0047 | Stationary |

| EXCR | -5.847215 | -3.529758 | I (1) | 0.0001 | Stationary |

| DSTR | -4.033150 | -3.529758 | I (1) | 0.0001 | Stationary |

| DODT | -3.697137 | -3.529758 | I (1) | 0.0437 | Stationary |

The first step to analyze time series data is to ensure the variables are stationary so as to avoid misleading result. To do this, ADF unit root test was conducted and the result is shown in table 2. From the result, gross fixed capital formation (GFCF) is stationary at level because the t-statistics (-3.255320) and its corresponding probability value of 0.0240 leads to rejection of null hypothesis that gross fixed capital formation has unit root and conclude that the series is integrated of order zero. Furthermore, real gross domestic product (RGDP), external debt (EXDT), exchange rate (EXCR), debt service repayment (DSRT) and domestic debt (DODT) are all stationary at first difference, that is, integrated at order one I(1) indicating that the aforementioned variables are free from unit root. It is therefore concluded that all the variables are stationary since their ADF statistics are greater than the critical values at 5 per cent level of significance. Thus, there is mix order of integration among the variables. In order to test for cointegration among the variables, bound test was carried out through autoregressive distributed lag model as proposed by Pesaran et al (2001).

Cointegration Test

Table 3: Summary of ARDL Bounds Test

| Null Hypothesis: No long-run relationships exist | ||

| Test Statistic | Value | k |

| F-statistic | 13.80965 | 5 |

| Critical Value Bounds | ||

| Significance | I0 Bound | I1 Bound |

| 10% | 2.26 | 3.35 |

| 5% | 2.62 | 3.79 |

| 2.5% | 2.96 | 4.18 |

| 1% | 3.41 | 4.68 |

Source: Researcher’s Computation using Eviews 10

The result of the ARDL Bonds test is presented in table 3. From the result, the F-Statistic of 13.80965 is found to be greater than lower and upper bound of 2.62 and 3.79 respectively at 5 per cent level of significance. It is therefore concluded that there is long run relationship among all the variables. Thus, the null hypothesis of no cointegration is rejected. Based on this, the long run elasticities based ARDL-ECM model was conducted and the result is presented in table 4.

Long Run Elasticities Based Ardl-Ecm Model

Table 4: Summary of ARDL-ECM TEST

| Dependent Variable: D(RGDP) | ||||

| Method: Least Squares | ||||

| Date: 02/27/22 Time: 09:30 | ||||

| Sample (adjusted): 1983 2021 | ||||

| Included observations: 39 after adjustments | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 48.58933 | 245.7322 | 0.197733 | 0.8445 |

| D(RGDP(-1)) | 1.226221 | 0.152315 | 8.050587 | 0.0000 |

| D(GFCF) | 0.266906 | 0.117987 | 2.262163 | 0.0308 |

| D(EXDT) | 108.2886 | 34.72035 | 3.118880 | 0.0039 |

| D(EXCR) | -7.167448 | 7.768578 | -0.922620 | 0.3633 |

| D(DSRT) | 0.086797 | 0.058218 | 1.490889 | 0.1461 |

| D(DODT) | -0.858898 | 0.326948 | -2.627013 | 0.0133 |

| ECM(-1) | -1.192382 | 0.217620 | -5.479180 | 0.0000 |

| R-squared | 0.749150 | Mean dependent var | 1472.015 | |

| Adjusted R-squared | 0.692507 | S.D. dependent var | 1517.948 | |

| S.E. of regression | 841.7332 | Akaike info criterion | 16.48949 | |

| Sum squared resid | 21963956 | Schwarz criterion | 16.83073 | |

| Log likelihood | -313.5450 | Hannan-Quinn criter. | 16.61192 | |

| F-statistic | 13.22572 | Durbin-Watson stat | 1.822998 | |

| Prob(F-statistic) | 0.000000 | |||

Source: Researcher’s Computation using Eviews 10

After establishing that there is long run relationship among the variables, the ARDL-ECM was conducted. From the result in table 4, the past value of real gross domestic product (RGDP) of 1.226221 implies that 1 percent increase in the past value of real gross domestic product (RGDP) will increase the value of real gross domestic product at current time with about 1.23 percent. This shows a positive relationship and statistically significant at 5 percent level since the p value of 0.0000 is less than 0.05 percent. The coefficient of gross fixed capital formation (GFCF) of 0.266906 with p value of 0.0308 is positive and statistically significant. This indicates that 1 percent increase in gross fixed capital formation (GFCF) will increase RGDP by 0.27 percent. Similarly, the coefficients of external debt (EXDT) and debt service repayment (DSRT) which stood at 108.2886 and 0.086797, with their p values of 0.0039 and 0.0133 respectively reveals a positive and significant impact between external debt, debt service repayment and real gross domestic product in Nigeria. It implies that 1 percent increase in EXDT and DSRT will increase RGDP by 108.3 and 0.09 percent respectively. The coefficients of exchange rate and domestic debt are however negative with the values of -7.167448 and -0.858898 respectively. This means that 1 percent increase in exchange rate and domestic debt will decrease the real gross domestic product by 7.17 and 0.86 percent respectively. Judging from their p values, exchange rate is statistically insignificant with p value of 0.3633 while domestic debt is significant at 5 percent level of significance. All these variables however, conform to apriori expectation except domestic debt and debt service repayment.

The value of ECM of -1.192382 captures the speed of adjustment of the model, implies that about 1.19 percent of the divergence or disequilibrium from the long run is being corrected for in the current period. The ECM coefficient is correctly signed and also statistically significant at 5 percent level. The constant value of 48.58933 means that if all the variables are held constant or fixed (zero), real gross domestic product will be valued at 48.59. Thus, the a-priori expectation is that the intercept could be positive or negative, so it conforms to the theoretical expectation.

The R-Squared of 0.749150 which is approximately 0.75 indicates that about 75 percent variations in real gross domestic product (RGDP) are explained by gross fixed capital formation (GFCF), external debt (EXDT), domestic debt (DODT), exchange rate (EXCR) and debt service repayment (DSRT) while the remaining 25 percent is attributed to other variables that are not explicitly captured in the model but also influence RGDP.

The F-Statistic of the model is 13.225 with probability value of 0.000000. This implies that the variables are jointly statistically significant at 5 percent level since the F-calculated is greater than the F-tabulated, even with the p value which is practically zero. This model is thus well-specified. The Durbin-Watson statistic is 1.822998, which is approximately 2. It implies that the model is not suffering from autocorrelation.

Diagnostic Tests

This subsection shows the results of the residual diagnostic tests conducted after estimation.

Serial Correlation Test

| Table 5: Breusch-Godfrey Serial Correlation LM Test | ||||

| F-statistic | 0.802339 | Prob. F(1,30) | 0.3775 | |

| Obs*R-squared | 1.015872 | Prob. Chi-Square(1) | 0.3135 | |

Source: Researcher’s Computation using Eviews 10

From the result in table 5, the F-Statistic and Obs*R-squared values of 0.802339 and 1.015872 with p values of 0.3775 and 0.3135 respectively are greater than the critical values at 5 percent level of significance. Hence, we conclude that there is no serial correlation in the model.

Heteroscedasticity Test

| Table 6: Heteroskedasticity Test: Breusch-Pagan-Godfrey | ||||

| F-statistic | 1.279267 | Prob. F(7,31) | 0.2927 | |

| Obs*R-squared | 8.740859 | Prob. Chi-Square(7) | 0.2718 | |

| Scaled explained SS | 5.402983 | Prob. Chi-Square(7) | 0.6109 | |

Source: Researcher’s Computation using Eviews 10

Table 6 presents the result of heteroscedasticity test. From the result, the F-statistic and Obs*R-squared have the values of 1.279267 and 8.740859 with corresponding p values of 0.2927 and 0.2718 respectively. These values are greater than the critical values at 5 percent level of significance. It means that the model is free from heteroscedasticity, that is, the mean, variance and covariance are constant over time.

Stability Test

To test whether the model is stable or not, both the cumulative sum and the cumulative sum of squares tests are conducted.

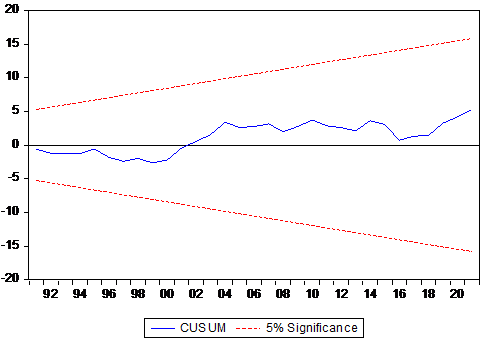

Figure 1: Cumulative Sum Plot

Source: Researcher’s Computation using Eviews 10

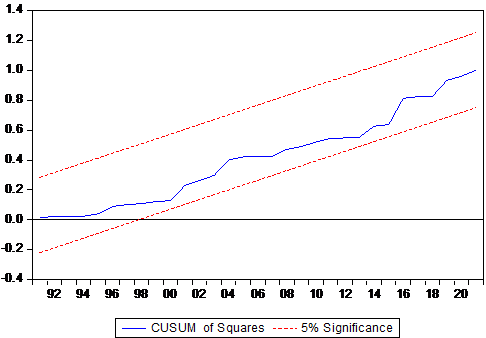

Figure 2: Plot of Cumulative Sum of Squares

Source: Researcher’s Computation using Eviews 10

From the results in figures 1 and 2, Figure 1 shows that the model and the estimated parameters are stable given that the graph moves within the 0.05 critical values. Similarly, figure 2 is the cumulative sum of square test which shows that the model and the estimated parameters are largely stable throughout the period under investigation since the blue line veers within the two red lines indicating 5% level of significance.

CONCLUSION AND RECOMMENDATIONS

This study examined debt overhang hypothesis, theory and empirical evidence in Nigeria spanning from 1981 to 2021. The study used ARDL method of data analysis. The empirical findings showed that the past value of real gross domestic product (RGDP), gross fixed capital formation (GFCF), external debt (EXDT) and debt service repayment (DSRT) have positive impact on economic growth in Nigeria. This shows that government borrowing external sources has been utilized efficiently in expanding productive base of the economy. Also, exchange rate (EXCR) and domestic debt (DODT) have negative impact on economic growth in Nigeria. This shows that government borrowing from the domestic capital market reduces funds available for private investment. Judging from the p values, the lagged value of RGDP, GFCF, EXDT and DSRT are statistically significant as their p values are lower than critical values at 5 percent level of significance, while EXCR and DODT have no significant impact on economic growth in Nigeria. The R-Squared of the 75 percent shows that the model is a good fit as 75 percent variations in RGDP are explained by GFCF, EXDT, EXCR, DODT and DSRT. It is therefore concluded that the model is correctly specified.

Based on this, the following recommendations were made.

- Government should formulate and effectively implement policy that would boost domestic revenue generation and reduce ineffective government spending.

- Government should also use the borrowed funds to put in place infrastructural facilities required for development as this will help create enabling environment for investment to thrive well.

REFERENCES

- Ademola, S. S., Tajudeen, A. O. & Adewumi, Z. A. (2018). External debt and economic growth of Nigeria: An empirical investigation. South Asian Journal of Social Studies and Economics, 1(2), 1-11.

- Adofu, I., & Abula, M. (2010). Domestic debt and the Nigerian economy. Current Research Journal of Economic Theory, 2(1), 22–26.

- Ajie, H. A., Akekere, J. &Ewubare, D. B. (2014).Praxis of Public Sector Economics and Finance. Port Harcourt: Pearl Publishers. [4]

- Àkos, D., &Istvàn, D. (2019). Public debt and economic growth: What do neoclassical growth models teach us? Applied Economics, 51(29), 104–121.

- Akram, N. (2013). Empirical Examination of Debt and Growth Nexus in South Asian Countries. Asia-Pacific Development Journal, 20(2), 29–52. https://doi.org/10.18356/0cbbc6e3en.

- Ayadi, F.S,.& Ayadi, F.O. (2008). The Impact of External Debt on Economic Growth: A Comparative Study of Nigeria and South Africa, Journal of Sustainable Development in Africa, Vol. 10, No.3, 234-264.

- Coccia, M. (2017). Asymmetric paths of public debt and of general government deficits acros countries within and outside the European monetary unification and economic policy of debt dissolution. The Journal of Economic Asymmetries, 17(2017), 17–31. https://doi. org/10.1016/j.jeca.2016.10.003.

- Didia, D., & Ayokunle, P. (2020). External Debt, Domestic Debt and Economic Growth in Nigeria. Advances in Economics and Business, 8(2), 85–94. https://doi.org/10.13189/aeb.2020.080202.

- DMO (2021). Report of the Annual National Market Access Country (MAC) Debt Sustainability Analysis (DSA).

- Elom-Obed, F. O., Odo, S. I., Elom-Obed, O., & Anoke, C. I. (2017). Public debt and economic growth in Nigeria. Asian Research Journal of Arts & Socia Sciences, 4(3), 1–16. https://doi.org/10.9734/ARJASS/2017/36095.

- Engle, R., & Granger, C. (1991). Long-run economic relationships: Readings in cointegration. Oxford University Press.

- Ezema, C. A., Nwekwo, N. M., &Agbaji, B. C. (2018). Impact of External Debt and Its Services Burden to Economic Growth in Africa: Econometric Evidence from Nigeria. International Journal of Academic Research in Economics and Management Sciences, 7(3), 232–250. https://doi.org/10.6007/IJAREMS/v7- i3/4643

- Ezirim, C. B. (2005). Finance Dynamics: Principles, techniques and application 3rd Edition Markowitz Centre for Research and Development University of Port Harcourt.

- Gomez-Puig, M., &Sosvilla-Rivero, S. (2015). Short-Run and Long-Run Effects of Public Debt on Economic Performance: Evidence from EMU Countries (RIAE Working Paper 1/37). Research Institute of Applied Economics. https://doi.org/10.2139/ssrn.2660117.

- Hussain, E., Haque, M., &Igwike, R. S. (2015). Relationship between Economic Growth and Debt: An Empirical Analysis for Sub-Saharan Africa. Journal of Economics and Political Economy, 2(2), 262–275.

- Iyoha M. A. (1997). An econometric study of debt overhang, debt reduction, investment and economic growth in Nigeria. National centre for economic management and administration (NCEMA) monograph series No 8 Ibadan.

- Joy, J., & Panda, P. K. (2020). Pattern of public debt and debt overhang among BRICS nations: An empirical analysis. Journal of Financial Economic Policy, 12(3), 345– 363. https://doi.org/10.1108/JFEP-01- 2019-0021.

- Krugman, P. (1988). Financing versus forgiving a debt overhang. Journal of Development Economics, 29(1), 253–268. https://doi.org/10.1016/0304- 3878(88)90044-2.

- Mhlaba, N., Phiri, A., & Nsiah, C. (2019). Is public debt harmful towards economic growth? New evidence from South Africa. Cogent Economics & Finance, 7(1), 1603653. https://doi.org/10.1080/23322039.2019. 1603653

- National Bureau of Statistics (2021). Labor force statistics: Unemployment and underemployment report (Q4 2021). Abuja: NBS

- Obayori, J. B., Krokeyi, W. S. &Kakain, S. (2019). External debt and economic growth in Nigeria. InternationalJournal of Science and Management Studies (IJSMS), 2(2), 1-6.

- Ochuko, A. S., & Idowu, E. (2019). Effect of Public Debt on Economic Growth in Nigeria: An Empirical Analysis. International Journal of Business and Economic Development, 7(2), 10–17.

- Ogbonna, K. S., Ibenta, S. N., Chris-Ejiogu, U. G., &Atsanan, A. N. (2019). Public debt services and Nigerian economic growth: 1970-2017. European Academic Research, 6(10), 22–34.

- Ogunjimi, J. A. (2019). The impact of public debt on investment: Evidence from Nigeria. Development Bank of Nigeria Journal of Economic and Sustainable Growth, 3(2), 1–28. https://www.researchgate.net/publication/335992571.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of long-run relationship. DAE Working Paper 962, University of Cambridge

- Rahman, M., & Islam, A. (2020). Some dynamic macroeconomic perspectives for India’s economic growth: Applications of linear ARDL bounds testing for cointegration and VECM. Journal of Financial Economic Policy, 12(4), 641– 658. https://doi.org/10.1108/JFEP- 11-2018-0165

- Sachs, J. (1989), “The debt overhang of developing countries”, in G. Calvo, R. Findlay, P. Kouri and J. Macedo (eds.) Debt, Stabilization, and Development: Essays in Memory of Carlos Diaz Alejandro (Oxford: Basil Blackwell).

- Saungweme, T., & Odhiambo, N. M. (2020). The Impact of Domestic and Foreign Public Debt on Economic Growth: Empirical Evidence from Zimbabwe. International Journal of Economics, 73(1), 77–106.

- Siddique, A., Selvanathan,E.A. & Selvanathan, S. (2015). The Impact of External Debt on Economic Growth: Empirical Evidence from Highly Indebted Poor Countries. Discussion Paper 15.10. University of Western Australia Department of Economics.

- Todaro, M. P. & Smith, S. C. (2011). Economic development. Eleventh edition. Pearson Education Limited, Edinburg. Grate, Harlaw, England.

- Udeh, S. N., Ugwu, J. I., & Onwuka, I. O. (2016). External debt and economic growth: The Nigeria experience. European Journal of Accounting Auditing and Finance Research, 4(2), 33–48.

- Udoh, B. E., Ekeowa, L. K., Okechukwu, I. S., Obiora-Okafor, C. A., & Nwonye, A. C. (2020). Effect of International Debt Burden on Economic Growth in Nigeria. Humanities and Social Sciences Letters, 8(2), 133–144. http://dx.doi.org/10.18488/journal.73.2020.82.133.144

- Umo, J. U. (2012). Economics: An African Perspective 2nd Edition. Millennium text publishers limited Plot 6B, Block 22, Humanities Road, Unilag Estate, Magodo, Isheri, Lagos, Nigeria.