Strategic Planning, Internal Control and Capability Toward Sustainable Performance of Cooperatives

- Noor Azaliah Jaafar

- Zuraidah Mohd Sanusi

- Norazida Mohamed

- Milen Baltov

- 1292-1315

- Mar 5, 2025

- Management

Strategic Planning, Internal Control and Capability Toward Sustainable Performance of Cooperatives

Noor Azaliah Jaafar1, Zuraidah Mohd Sanusi2, Norazida Mohamed3, Milen Baltov4

1,2Accounting Research Institute, Universiti Teknologi MARA, Shah Alam, Malaysia

3Faculty of Accountancy, Universiti Teknologi MARA, Shah Alam, Malaysia

4Faculty in Business Studies, Burgas Free University, Bulgaria

DOI: https://dx.doi.org/10.47772/IJRISS.2025.9020105

Received: 30 January 2025; Accepted: 03 February 2025; Published: 05 March 2025

ABSTRACT

This study examines the relationship between strategic planning, internal control, capability, and sustainable performance in Malaysian cooperatives. It focuses on the mediating role of capability in linking strategic planning to performance outcomes and examines the moderator effect of strategic planning between internal control and sustainable performance. This study employed Partial Least Squares Structural Equation Modelling (PLS-SEM) to examine data collected from 132 cooperatives in Malaysia, particularly in medium and large sizes. Results indicate that strategic planning and internal control do not directly impact sustainable performance, while capability has a positive effect. Capability significantly mediates the relationship between strategic planning and sustainable performance. While strategic planning moderates the relationship between internal control and sustainable performance, the effect is nonsignificant. This study is expected to contribute to the body of knowledge by supporting previous studies and advancing literature about the understudied variables. Despite its focus on Malaysian cooperatives and reliance on questionnaire-based data, which may introduce biases or inaccuracies, the findings provide valuable insights for advancing research on strategic planning, internal control, and capability. This study contributes to the theoretical understanding of these factors, supporting prior research and offering practical implications for enhancing performance in cooperative organisations.

Keywords: Strategic Planning, Internal Control, Capability, Sustainable Performance, Cooperatives

INTRODUCTION

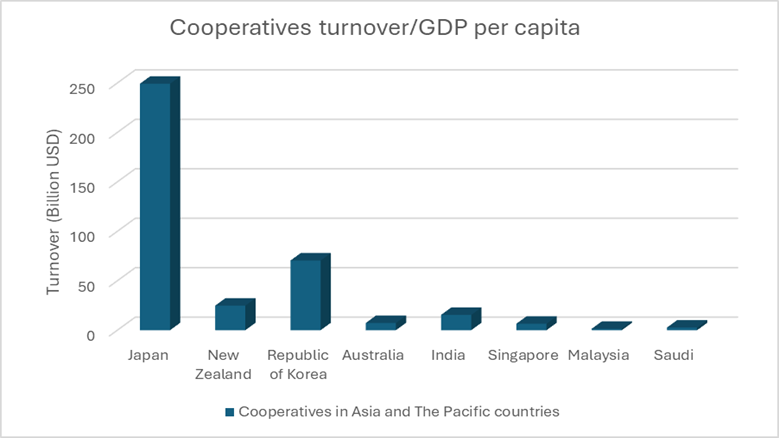

Cooperatives play a significant role in the global economy, with the top 300 cooperatives and mutuals having a turnover of over USD two trillion, equal to (2,409 billion USD), based on 2021 financial data (ICA, 2023). The top 300 cooperatives operate in various economic sectors, such as agriculture and insurance, which are leading the list, followed by wholesale and retail. Europe countries have a large number of cooperatives by turnover/GDP per capita, followed by Asia and the Pacific, such as Japan (21) (USD 249.27 billion), New Zealand (5) (USD 24.89 billion), the Republic of Korea (4) (USD 7051 billion), Australia (3) (USD 7.34 billion), India (3) (USD 15.51 billion), Singapore (2) (USD 6.59 billion), Malaysia (1) (USD 1.46 billion), and Saudi Arabia (1) (USD 2.72 billion) (ICA, 2023). Figure 1 shows the number of cooperatives in Asia and the Pacific by turnover/GDP per capita.

Figure 1 Number of cooperatives in Asia and the Pacific by turnover/GDP per capita

Source: (ICA, 2023)

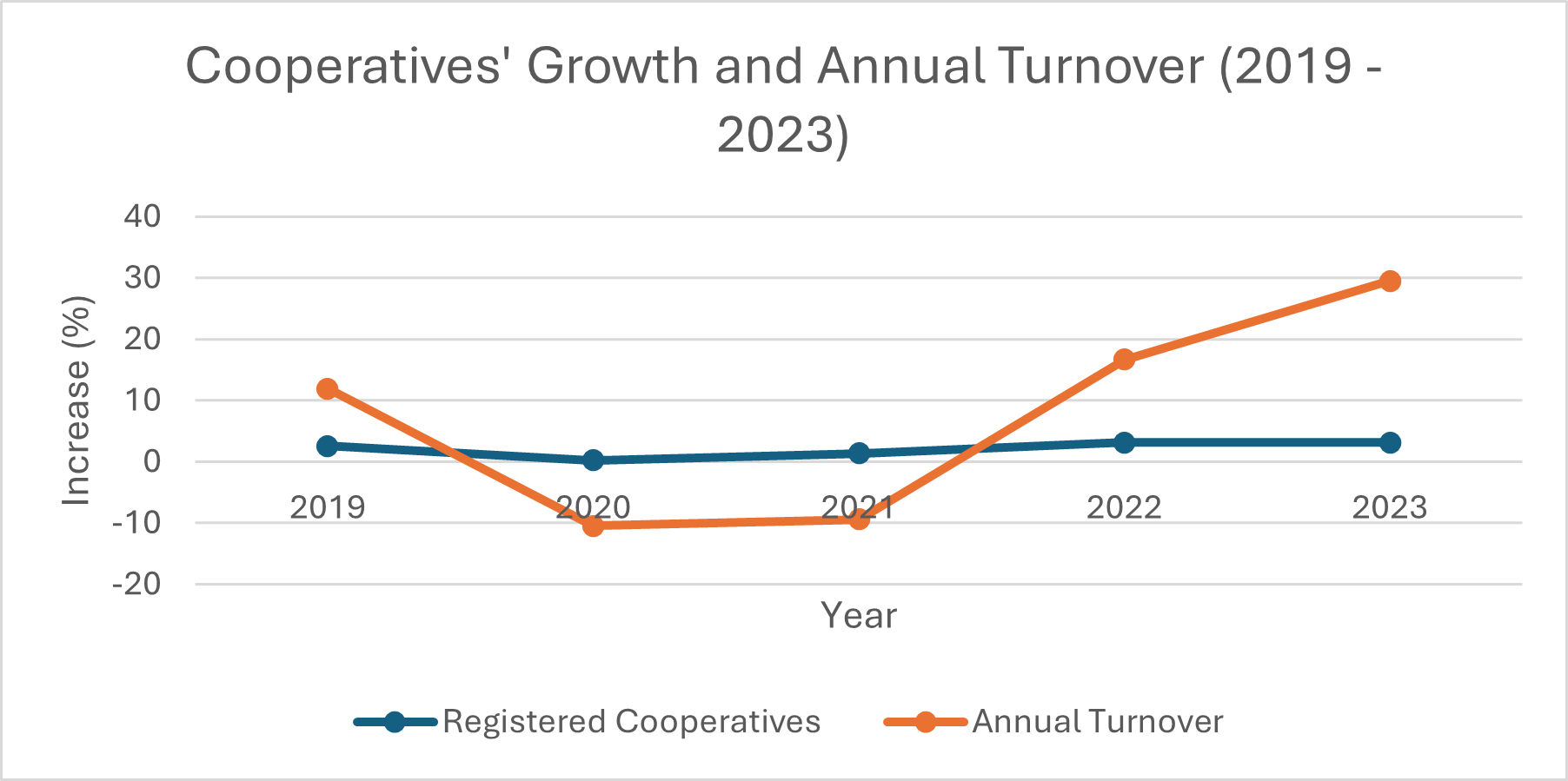

Compared with other ASEAN nations, Malaysian cooperatives have shown moderate growth, particularly in agriculture, retail, finance, and tourism. Despite that, the cooperative sector in Malaysia grew by 3.97% yearly from 2014 until 2019 (Bernama, 2020), pointing out that the cooperative sector’s contribution influences Malaysia’s GDP, and cooperatives play an important role in the national economic development. The Malaysian Cooperative Societies Commission (MCSC) regulates cooperatives under the Ministry of Domestic Trade, Cooperatives, and Consumerism. Registered cooperatives increased from 14,629 in 2020 to 15,809 by 2023. Due to this growth, turnover increased by 29.52% from RM45.5 million in 2022 to RM64.5 million in 2023 (SKM, 2023). Figure 2 illustrates registered cooperatives’ growth and annual turnover from 2019 to 2023 (SKM, 2019, 2020, 2021b, 2022, 2023a).

Figure 2 Registered cooperatives’ growth and annual turnover from 2019 to 2023

Source: (Suruhanjaya Koperasi Malaysia, 2019, 2020, 2021, 2022, 2023a)

Despite the regulatory framework provided by the Cooperative Societies Act 1993, many Malaysian cooperatives face compliance challenges, particularly highlighting the weaknesses of cooperatives without strong strategic planning and internal controls. The cases that illustrate mismanagement and lack of internal control, for instance, the secretary of Koperasi Global and National Skill Development, Seremban Bhd, misused his position to obtain projects worth RM360,250 (Sinar Harian, 2020), emphasizing a lack of internal controls and improper management due to abuse power. Likewise, cases of fraud and mismanagement, such as the Koperasi Telekom Malaysia (KotaMas) suffered an RM23 million loss due to fraudulent activities by its chairman, secretary, and treasurer (The Star, 2017), demonstrated a lack of internal control and may have caused eroded public trust on cooperative management.

As can be seen for global cooperatives such as Mondragon cooperatives that were a large cooperative group in Spain, have struggled to adjust to ever-changing and increasing market pressure before meeting with much success by implementing continuous improvement through various strategic initiatives focusing on education, training, and innovation to enhance member capabilities (Altman, 2008; Kasmir, 2016). Likewise, in Malaysia cooperatives, Bank Kerjasama Rakyat Malaysia (Bank Rakyat) and Koperasi Permodalan Felda Berhad (KPFB) have shown progress in adopting sound business strategies in a dynamic environment (Musa et al., 2020); however, many cooperatives still struggle due to weak managerial capabilities and low entrepreneurial orientation affect organisation performance. Strengthening capability through improved strategic planning, strong internal control, fostering an entrepreneurial mindset, and enhancing knowledge development is essential for the sustainable performance of cooperatives. Thus, it emphasizes the need for regulators to rethink regulatory frameworks and enforcement, such as effective strategic planning to align their social goals with business objectives, ensuring they can continue to operate and grow while delivering social impact.

In the context of cooperatives, insufficient training, lack of updated information, difficulties obtaining necessary documents, and lack of support among members significantly impede cooperatives’ sustainable development (Junges et al., 2022). The failed implementation of the strategic planning process is due to corruption and fraud, poor management skills, lack of strong organisational culture and strategic planning, poor internal control, and lack of communication and motivation within organisations (Dlamini et al., 2020).

Although cooperatives are the third contributor to the Malaysian economy, the relationships between strategic planning, internal control, and capability toward sustainable performance in cooperatives are still limited. Likewise, the mediating role of capability in the relationship between strategic planning and sustainable performance and the moderating role of strategic planning in the relationship between internal control and sustainable performance in cooperatives have yet to be examined as much. Therefore, this study examines the relationships between strategic planning, internal control, and capability toward sustainable performance in cooperatives. Particularly to identify the mediating role of capability in the relationship between strategic planning and sustainable performance and the moderating role of strategic planning in the relationship between internal control and sustainable performance. By addressing this research gap, the study aims to answer the following questions:

RQ1. Does strategic planning influence the sustainable performance of cooperatives?

RQ2. Does internal control influence the sustainable performance of cooperatives?

RQ3. Does capability influence the sustainable performance of cooperatives?

RQ4. How does capability mediate the relationship between strategic planning and the sustainable performance of cooperatives?

RQ5. How does strategic planning moderate the relationship between internal control and the sustainable performance of cooperatives?

This study examines the relationships between strategic planning, internal control, and capability toward sustainable performance in cooperatives. Secondly, the study examines the mediating role of capability in the relationship between strategic planning and sustainable performance in cooperatives. Third, this study examines strategic planning as a moderating role in the relationship between internal control and sustainable performance. The remainder of the paper proceeds as follows. Section 2 describes the literature reviews and hypothesis development to support the foundation of this study. Section 3 outlines the methodology of the study. Section 4 describes the results of the measurement and structural model and the discusses of the empirical evidence for the study. Finally, Section 5 concludes the study with future recommendations and highlights this paper’s limitations.

LITERATURE REVIEW AND HYPOTHESIS DEVELOPMENT

Sustainable performance

Sustainable performance refers to an organisation’s ability to achieve long-term success while balancing economic, environmental, and social goals. It is a genuine mechanism for organisations to increase their financial success involving generating financial returns while maximizing environmental impacts and fostering social well-being (Rahman et al., 2022). In line with Elkington (1998), the definition of sustainable performance, which considers economic, social, and environmental performance, also aligns with the triple bottom line concept. The concept of ”triple bottom line” (TBL) has been extended to corporate performance and is known as ”sustainable corporate performance” which involves the economic (profit), social (people), and environmental (planet) (Fauzi et al., 2010).

In the context of profit organisation, achieving sustainable performance require a more detailed understanding of how the framework and practices adopted by organisations to make the business truly sustainable, which consider the economy, people’s well-being, and the environmental quality (Comin et al., 2019). Contrary to cooperatives, sustainability concerns the uniqueness of the cooperatives model rather than just economic performance. Notably, setting indicators enables cooperatives to assess their sustainability performance and serve as strategies and performance measurements (Aris et al., 2018). Sustainable performance encompasses economic, social, and environmental dimensions important for management effectiveness and organizational development.

Strategic planning and sustainable performance

Effective strategic planning is needed to align their social goals with business objectives, ensuring they could continue to operate and grow while delivering social impact. What strategic planning is and how it influences cooperative operations are two questions that attract growing research interest. For cooperatives, it is important to generate income and assist members with effective management systems and strong leadership (Ismail et al., 2019).

Previous studies indicate that strategic planning significantly impacts organisational performance. As can be seen, Donkor et al. (2018) highlights that strategic planning positively influences the performance of SMEs could improve decision-making, resource allocation, and long-term growth. Tarigan & Siagian (2021) emphasized the important role of strategic planning in maintaining supply chain efficiency and enhancing operational performance study found that effective strategic planning supports process and product innovation, meets customer requirements, and improves overall operational outcomes.

While, Chungyas & Trinidad (2022) have argued that strategic management practices are important for the success and sustainability of cooperatives in the Philippines. Likewise, Morshidi et al. (2021) studies strategic orientation (SO) consisting of entrepreneurial orientation (EO), market orientation (MO), learning orientation (LO) elements, and organisational commitment (OC) on cooperative performance in Malaysia. The relationship between these elements positively impacts SO and cooperative performance, showing that with the unique organisation of the cooperative, applying SO and OC added advantages to enhance cooperative performance.

However, a few previous studies have found that strategic planning has a negative impact on performance. Rau et al. (2020) found that while strategic planning alone may not directly influence performance, its integration with organisational learning significantly enhances outcomes. Further, Mathibe et al. (2023) supports that strategic planning alone may not enhance social enterprise performance. Instead, value co-creation mediates the relationship between strategic planning and performance, which is key for greater performance, including social and financial outcomes in social enterprise. Similarly, Nowak (2021) argued that when combined with cognitive diversity, strategic planning is essential for achieving cohesive organisational performance for meeting an organization’s mission and strategic objectives.

Consistent with Dynamic Capability View (DCV) theory, organisations that engage in strategic planning are better equipped to develop and deploy resources dynamically, enabling them to respond to environmental changes and competitive pressures effectively (Teece et al., 1997). Resources are the main drivers for organisational performance, and sustainable competitive advantages are created through unique bundles of resources (J. Barney, 1991; Wernerfelt, 1984). This theory posits that strategic planning facilitates creating and reconfiguring internal and external resources, fostering sustainable competitive advantages over time (Winter, 2003). This shows that coordinating strategic planning with the organisation’s resources and external environment improves organisational performance.

Despite this, the impact between strategic planning and organisational performance is complex; some studies report a positive or direct relationship, while others report a negative or indirect relationship. Few studies have focused on cooperative performance such as strategic planning and members’ participation (‘Aini et al., 2012), strategic planning implementation on the cooperative members’ participation (Caska & Indrawati, 2017), and strategic orientation and organisational commitment (Morshidi et al., 2021), however, as for strategic planning in the cooperative and its impacts on sustainable performance, it remains unexplored. Based on the discussions above, the following hypothesis is made:

H1: There is a relationship between strategic planning and sustainable performance.

Internal control and sustainable performance

According to the Committee of Sponsoring Organizations of the Treadway Commission, (COSO 2013), internal control comprises policies and procedures established by an organisation to manage risks related to achieving its operations, reporting, and compliance objectives, thereby sustaining overall performance. Internal control is safeguarding a company’s assets, ensuring the accuracy and reliability of accounting records and information, enhancing productivity in the firm’s operations, and ensuring compliance with management’s policies and procedures (Fadzil et al., 2005; Hall et al., 2004; Sulaiman et al., 2008). According to IFAC (2011), internal control supports organisations in achieving their strategic objectives through effective and efficient operations, safeguarding resources, providing reliable information, and ensuring conformance with laws and regulations.

Dynamic Capability View (DCV) theory provides a framework highlighting organisations’ importance in developing and maintaining strategic resource utilization and capability in environmental change (Winter, 2003), while institutional theory posits that organisations should understand organisational behaviour, such as enduring rules, practices, and structures that set conditions for action (Lawrence & Shadnam, 2008). In this regards, internal control is important to ensure effective management control, enhancing organisational performance.

A study by Yeniaras & Kaya (2021) examines how relational governance, characterized by trust, collaboration, and long-term relationships between firms and their partners, impacts firm performance. The finding highlights that relational governance fosters a cooperative environment, enhancing the effectiveness of strategic planning processes. Akisik & Gal (2017) studied how CSR and internal controls impact stakeholders’ views of the firm and influence decisions on its financial performance. The results indicate that the effectiveness of internal control influenced the decision-making process, which positively affects financial performance. Similarly, Tetteh et al. (2020) conducted a study on the impact of internal control systems on the performance of listed firms in Ghana, with responses from 49 companies on the Ghana Stock Exchange, while 249 questionnaires were distributed. Their findings indicate that internal control systems positively impact organisational performance, with information technology as a moderator that strengthens this relationship.

However, some studies have found that internal control does not significantly affect performance. As can be seen, Bruwer et al. (2018) analysed how internal control activities and managerial conduct impact the sustainability of small, medium, and micro enterprises (SMMEs) in South Africa indicated that internal control activities and managerial conduct as internal control mechanisms have a negative effect on the relationship between SMME business sustainability. A study by Alam et al., (2019) revealed that internal control systems did not significantly impact accountability practices, contradicting the common belief that internal control systems are important for improving accountability.

A few studies have focused on cooperative performance, including the effect of internal control systems on cooperative profitability (Shabri et al., 2016), the impact of internal control on operational performance in cooperatives (Damina Makut & Abbas Ibrahim, 2021), and determinants of internal control effectiveness on cooperative employees (Rizki & Anisykurlillah, 2018). Despite that, there are limited studies on the relationship between internal control and sustainable performance, particularly in Malaysia’s cooperative context. Therefore, this study hypothesizes that:

H2: There is a relationship between internal control and sustainable performance.

Capability and sustainable performance

Capability is essential for survival and business success (Prahalad, 1993). In strategic management, capabilities are defined as adapting, integrating, and reconfiguring internal and external organisational skills, resources, and functional competencies to meet the needs of a changing environment (Teece et al., 1997). Ulrich & Lake (1991) state that capability encompasses resources, skills, and competencies that an organisation should leverage to implement its strategies effectively. It is consistent with Dynamic Capability View (DCV), which argues that integrating, building, and reconfiguring internal and external competencies is essential to rapidly changing environments for maintaining performance and achieving long-term success (Teece et al., 1997). Instead, RBV theory emphasizes capabilities that include market orientation (Day, 1994), entrepreneurship, innovativeness, and organisational learning (Hult & Ketchen, 2001) that enhance organisational performance by generating new opportunities, ideas, products, or processes in line with technological and market changes.

Wang et al. (2020) argues on how strategy and capabilities influence the organisation’s performance and study finds that strong organisational capabilities benefit business groups’ marketing or operations, and diversification moderates the relationship between strategy and performance. Kwalanda et al. (2017) indicate that dynamic managerial capabilities positively affect performance, and it supports the idea that dynamic managerial capability is an important strategy for enhancing performance. Violinda & Sunjian (2018) performed a study of dynamic capabilities and organisational culture in the performance of agriculture cooperatives in Indonesia. The findings indicate that organisational culture positively affects the performance of agriculture.

Despite previous studies’ positive influence on the relationship between capability and organizational performance, a study by Salisu & Abu Bakar (2020) emphasizes the mediating role of learning capability in the relationship between technological capability, relational capability, and performance of small and medium enterprises (SMEs). The study indicates the negative relationship affects direct or mediating relationships. Similarly, Wardhiani et al. (2023) examines the impact of capability on cooperative performance and sustainability of cooperatives in several coffee cooperatives in West Java.

Meanwhile, previous studies have examined capability and cooperatives’ performance; for instance, Violinda & Sunjian (2018) studied dynamic capabilities and organisational culture in the performance of agriculture cooperatives, and Pavão & Rossetto (2015) referred to stakeholder management capability and performance in Brazilian cooperatives. Still, the relationship between capability and sustainable performance has not been extensively examined. Therefore, this study hypothesizes that:

H3: There is a relationship between capability and the sustainable performance of cooperatives.

The mediating role of capability on the relationship between strategic planning and sustainable performance

The concept of mediating variables, also known as intervening or intermediate variables, is crucial for explaining complex causal relationships between two variables. A mediator variable “accounts for the relationship between the predictor and the criterion” (Baron & Kenny, 1986, p. 1176 ). This approach seeks a more accurate explanation of how an independent variable affects a dependent variable. While RBV focuses on leveraging existing resources to maintain a niche market, this study uses the dynamic capability view (DCV) to emphasize the organisation’s ability to integrate, build, and reconfigure internal and external competencies in response to rapidly changing environments (Teece et al., 1997). As such, capability is a critical factor that is functional to the organisation in achieving long-term success. The capability involved in an organisation’s activities results in sustained competitiveness (Winter, 2003).

Ali et al. (2021) finds that competitive capabilities positively influence sustainable performance and competitive competencies’ mediating role positively impacts the relationship between SMPs and sustainable performance, emphasizing the importance of resource adoption and capability awareness for building a sustainable competitive advantage. Thanh Nhon et al. (2020) views how the dynamic capabilities of learning, integration, and reconfiguration mediate the relationship between intellectual capital, including human, social, and organisational capital, and the performance of Vietnam’s information and communications technology firms. Based on the resource-based view theory, this study finds that dynamic capabilities mediate between intellectual capital and performance, with learning capability having the most significant mediating effect. Acosta-Prado & Tafur-Mendoza (2022) reviews the mediating role of dynamic capabilities in the relationship between information and communication technology (ICT) and sustainable performance. The result supported the direct relationship between ICT and sustainable performance. Likewise, the mediating effect of dynamic capability in the relationship between ICT and sustainable performance is significantly positive.

The mediating factor has been identified as an important factor that could improve performance effectiveness. Past empirical studies have reported positive effects on a mediating role such as dynamic capabilities, resource management capabilities, competitive capabilities, innovation capability on sustainable performance (Abbas et al., 2019; Acosta-Prado & Tafur-Mendoza, 2022; Ali et al., 2021; Fahim & Baharun, 2017; Shang et al., 2020), innovation capability, dynamic capabilities on organisational performance (Liu et al., 2020; Odeh Al-Husban et al., 2021; Thanh Nhon et al., 2020). Yet, limited studies have been conducted on the mediating role of capability, particularly in the relationship between strategic planning and sustainable performance in the cooperative context. This study examines how capability mediates this relationship by enabling organisations to innovate, adapt, and manage resources effectively. Hence, the following hypothesis is proposed:

H4: Capability mediates the relationship between strategic planning and the sustainable performance of cooperatives.

The Rationality of the Expected Moderation of Strategic Planning between Internal Control and Sustainable Performance

Moderator variables significantly influence the direction and strength of the relationship between independent (internal control) and dependent (sustainable performance) variables (Baron & Kenny, 1986). These include not only firm size and industry type constraints (Kylaheiko et al., 2016) but also considering the changing environment and market conditions (Korkmaz, 2020), as well as the challenges to successfully implementing strategic planning (Dlamini et al., 2020). Similarly, the occurrence and effects of internal control depend on the level of control activities and the degree of monitoring in the organisation (Agbejule & Jokipii, 2009). The dynamic capability view (DCV) suggests that organisations continually seek to adapt their internal control systems to rapidly changing environments (Teece et al., 1997) and align with institutional norms and expectations to gain legitimacy and ensure long-term viability (DiMaggio & Powell, 1983) fostering sustainable performance.

A study by Muhsin Thaji et al. (2022) views strategic leadership practices and crisis management in government institutions in Iraq, with strategic planning as the moderator role. This study demonstrated that strategic planning increases the effectiveness of strategic leadership in effectively managing crises, where strong strategic leadership and effective strategic planning systems suffer less damage during crises and recover more quickly. Sinnaiah et al. (2023) argued that different decision-making styles affect the strategic management process (such as planning, formulation, implementation, and evaluation of strategies) and organisational performance. Based on the findings, decision-making styles act as a moderator role in the strategic management process and have a direct impact on determining organisational performance. It can be concluded that organisation with decision-making styles practices (intuitive and rational) has better performance, and instead, if there is an absence of decision-making styles, they are associated with lower performance.

For example, St-Hilaire (2019) stresses that strong corporate governance and appropriate strategic planning are essential to ensure the effectiveness of organisation management. Instead, Ojha et al. (2019) indicates that strategic planning alone may not directly affect performance effectiveness. Still, the mediating effect, such as organisational capabilities, is important in ensuring strategic planning plays a mediating role in guiding, controlling, and monitoring the organisation to ensure objectives are met, effective resource allocation, and competitive advantage, thus enhancing organisational performance.

Previous studies focusing on strategic alliances in moderating the link between innovation capabilities and performance in Malaysian SMEs (Kamalrulzaman et al., 2021), strategic planning as the moderator role between strategic leadership and crisis management (Muhsin Thaji et al., 2022), decision-making styles as moderator role in the strategic management process and organisational performance (Sinnaiah et al., 2023), leadership styles in the relationship between corporate governance and employee engagement (Koeswayo et al., 2024). However, there are limited studies on the moderation effect in the relation between internal control and sustainable performance focused specifically on the cooperative context. Therefore, the following hypothesis is proposed:

H5: Strategic planning moderates the relationship between internal control and the sustainable performance of cooperatives.

Conceptual framework

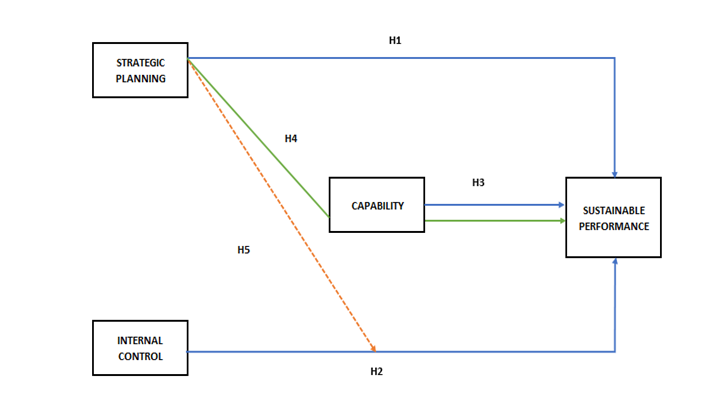

Figure 3 below is the conceptual framework illustrated to represent the model of this study. The study is comprised of strategic planning, internal control, capability, and sustainable performance.

Figure 3. The conceptual framework

The conceptual framework is constructed to clearly understand testable relationships identified through a literature review and tested with relevant data (Sekaran & Bougie, 2016). The conceptual framework is also instrumental in constructing viable hypothesis to be examined and further strengthening the research questions. Sekaran & Bougie (2016) stress that the conceptual framework is important for a clear picture of the association of study variables. Two main theories, namely Dynamic Capability View (DCV) (Teece et al., 1997) and Institutional Theory (DiMaggio & Powell, 1983), were used in this study. The dynamic capability view (DCV) focuses on the organisation’s ability to renew its resources in a fast-changing environment involving integrating, building, and reconfiguring processes (Teece et al., 1997). The institutional theory of DiMaggio & Powell (1983) emphasizes the external pressures and norms, rules, and practices that shape organisational behaviour. The central idea of both theories is to explain how the organisation applies resources and capability to create and implement strategies to ensure all activities comply with laws, thus achieving competitive advantage and effective performance outcomes.

The conceptual framework for this study examines the relationships between strategic planning, internal control, capability, and sustainable performance in cooperatives. In this study, the independent variables are strategic planning, internal control, and capability; the dependent variable is sustainable performance. Besides examining the direct effect of the variables on strategic planning, internal control, capability, and sustainable performance, this conceptual framework also indicates variables as mediators and moderators. Capability plays a mediation role in the relationship between strategic planning and sustainable performance. Instead, strategic planning acts as a moderator between internal control and sustainable performance.

METHODOLOGY

Research design and instrument

The study uses a quantitative approach, which involves collecting and analysing numerical data. This method is chosen for its cost-effectiveness and time efficiency, particularly when investigating correlations among variables in large samples (Al-Ababneh, 2020). The study employs SEM as an empirical technique to examine the hypotheses. SEM is advantageous because it integrates exploratory factor analysis and structural path analysis, making it suitable for analysing both latent (unobserved) and observed variables, and for testing entire theories (J.F. Hair et al., 2011; Hair Jr. et al., 2017). There are two main SEM approaches: Covariance-Based SEM (CB-SEM) and Partial Least Squares SEM (PLS-SEM) (Hair Jr. et al., 2017; Henseler et al., 2016).

CB-SEM is typically used for theory confirmation and requires assumptions like multivariate normality, while PLS-SEM is preferred for prediction, especially with small sample sizes, non-normal data, or complex models (Joseph F. Hair et al., 2012). PLS-SEM is chosen for this study due to its efficiency, flexibility with data, and ability to handle the study’s objectives, including evaluating complex models with mediating and moderating effects (Hair Jr et al., 2014).

In order to measure strategic planning properly, this study used the scale measurement developed by Fahed-Sreih & El-Kassar (2017), Kylaheiko et al. (2016), and Tasleem et al. (2019), which considers how setting goals, decision-making, and the quality and effectiveness execution of strategic planning in a cooperative. The internal control variables examined include control environment, control activities, risk assessment, information and communication, and monitoring adopted from the COSO (2013) framework. These internal control items have been developed by (Alam et al., 2019; Länsiluoto et al., 2016; Said et al., 2020). In order to measure capability properly, the measurement scale was developed by (Attia & Salama, 2018; Camisón-Zornoza et al., 2020; Latifah et al., 2021). In this study, the sustainable performance in a cooperative is a dependent variable. The scale developed by (Baumgartner, 2014; Baumgartner & Rauter, 2017; Tasleem et al., 2019) was used to measure this study’s variables. This measurement instrument comprises 12 items, four for each dimension: economic, social, and environmental (Belhadi et al., 2021). This study using the Likert format with a 5-point Likert scale to assess respondents’ agreement with responses ranging from “strongly disagree” to “strongly agree” (Sekaran & Bougie, 2016).

Participation and data collection procedures

The study uses a stratified random sampling method, a type of probability sampling, to ensure the generalizability of the results (Saunders et al., 2009). This method is particularly suitable for ensuring that different subgroups within the population are adequately represented. The population of this study is comprised of cooperatives in Malaysia. The main reason cooperatives were chosen as respondents in this study is that the cooperative sector contributes 3% to 4% of Malaysia’s GDP, which plays a critical role in national economic development (Malaysia’s Official Statistics, 2021). The data is collected through individual respondents, specifically senior managers and executives. The respondents are the most knowledgeable individuals responsible for controlling and overseeing the entire organisation, establishing organisational goals, strategies, and policies, and making decisions on the direction of cooperatives.

The primary data collection instrument is a questionnaire, designed to gather quantitative data. Part A is self-developed on the organisation profile regarding the size, turnover and age of the firm, state registered, and type of cooperatives. Part B is self-developed on the respondent profile about the gender, years of employment, age of respondent, and education. Part C is a factor associated with sustainable performance. When deciding to become sustainable, cooperatives should adopt several specific sustainable practices such as strategic planning, internal control, and capability. Part D: Dependent variables, measuring sustainable performance across economic, social, and environmental dimensions.

The questionnaire was distributed through various channels by electronically, by mail, or in person to reach a broad range of participants. The questions are clear and logically structured, with each question’s purpose defined to ensure accurate measurement of the variables. The questionnaire was made available in both English and Malay to accommodate respondents’ language preferences. Out of 285 questionnaires distributed, 138 were completed and returned, yielding a usable response rate of 48.4 percent (Yu & Cooper, 1983). During outlier detection and CMV, data were deleted and adjusted. Specifically, 6 out of 138 usable questionnaires were deleted to ensure that unusual observations did not significantly impact the results (Joseph F. Hair et al., 2022). The sampling frame of this study will be drawn from the Malaysia Cooperative Societies Commission’s (MCSC) comprehensive list.

A pilot study was conducted to evaluate the factor loadings, which met the threshold of 0.5, ensuring convergent validity (with AVE, of 0.5 and CR, of 0.7). Discriminant validity was also confirmed, with the ratio of HTMT not exceeding 0.85. The preliminary statistical tests on the pilot study variables successfully met these minimum criteria. Data were then analysed using path modelling through the Partial Least Squares (PLS) approach, utilizing Smart PLS software (Wong, 2013). Specifically, the study employed Smart-PLS 4 (Cheah et al., 2024) to assess the mediating effects of capability on the relationship between strategic planning and sustainable performance.

RESULTS AND DISCUSSIONS

Data analysis

The data analysis in this study was analysed using the Smart PLS version 4.1.0.7. PLS-SEM has the added advantage of estimating the measurement and structural models (Hair Jr. et al., 2017).

Participants demographics

The demographic profile of the respondents, as shown in Table 1, provides a clear overview of their gender, years of employment, age distribution, and educational qualifications. Most respondents are female, making up 89 (67.42%), while 43 (32.58%) were male.

Table 1 Demographic Profile of the Respondents

| Profile of respondents | Frequency | (%) |

| Gender | ||

| Male | 43 | 32.58 |

| Female | 89 | 67.42 |

| Total | N = 132 | |

| Years of Employment | ||

| Less than 3 years | 28 | 21.21 |

| 3 – 5 years | 27 | 20.46 |

| 6 – 10 years | 21 | 15.91 |

| More than 10 years | 56 | 42.42 |

| Total | N = 132 | |

| Age | ||

| NA | 29 | 21.97 |

| Less than 25 years old | 3 | 2.27 |

| 25 -34 | 32 | 24.24 |

| 35 – 44 | 30 | 22.73 |

| 45 – 54 | 25 | 18.94 |

| 55 – 64 | 12 | 9.1 |

| 65 onwards | 1 | 0.76 |

| Total | N = 132 | |

| Academic qualification | ||

| NA | 1 | 0.76 |

| SPM | 12 | 9.1 |

| Diploma | 38 | 28.79 |

| Bachelor’s degree | 63 | 47.73 |

| Master’s degree | 15 | 11.36 |

| PHD | 1 | 0.76 |

| Other | 2 | 1.52 |

| Total | N = 132 |

Assessment of the measurement

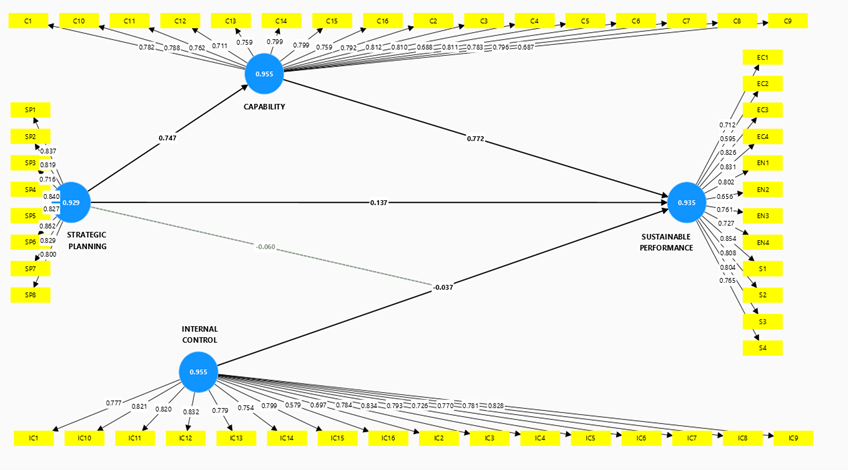

Data were analysed through path modelling using the PLS approach and the Smart PLS software. The analysis begins with assessing the measurement models (Hair Jr. et al., 2017). A vital advantage of the PLS approach compared to the covariance-based structural equation modelling is its ability to deal with situations where knowledge about the distribution of the latent variables is restricted, requirements about the closeness between estimates and the data should be met (J.F Hair et al., 2021). In our research model, all constructs are specified with reflective indicators, as depicted in Figure 4.

The study ensured the validity and reliability of the constructs by testing for outer loadings (≥ 0.7), composite reliability (CR ≥ 0.7), average variance extracted (AVE ≥ 0.5), and heterotrait–monotrait (HTMT) ratio (≤ 0.85). These tests confirmed that the measurement instruments were reliable and valid for the study. The results demonstrate that all reflectively measured constructs are both reliable and valid. Table 2 presents measurement assessment of item loadings helps to measure the indicator reliability of the measurement model. The measurement model with loadings above 0.708 is recommended at a significant level of 0.05 (Joe F. Hair et al., 2019), thus achieving satisfactory item reliability. However, J.F. Hair et al. (2011), recommended that indicators with loadings between 0.40 and 0.70 should be considered for deletion only if the deletion will increase CR and AVE above the threshold value. In this study, IC2 (0.697), IC16 (0.579), C5 (0.688), C9 (0.687), EC2 (0.595), and EN2 (0.656) indicators loading have not achieved the recommendation threshold value. Nonetheless, these indicators are important to maintain the content validity of the construct. Removing them might alter the meaning or coverage of the construct (Joseph F. Hair et al., 2012).

Figure 4. Path model and PLS estimates

Tables 3 and 4 depict the assessment of discriminant validity of both the Fornell & Larcker (1981) and the heterotrait-monotrait ratio of correlations (HTMT) based on the multitrait-multimethod matrix suggested by Henseler et al. (2015) providing a comprehensive examination of construct distinctiveness. Based on Table 3, the capability-internal control construct, capability-sustainable performance construct, and internal control-strategic planning construct have few disputes. These conclude that the Fornell-Larcker criterion has a low sensitivity, which means it is unable to detect a lack of discriminant validity (Henseler et al., 2015). Hence, to better assess discriminant validity, (Henseler et al., 2015) suggests assessing the correlations’ heterotrait-monotrait ratio (HTMT) as a solution to the issue.

To address this limitation, this study assessing discriminant validity using the Heterotrait-Monotrait Ratio (HTMT) criterion as alternative, and suggests that threshold value should remain less than 0.85 (Henseler et al., 2015) Instead, Gold et al. (2001) argued that a correlation coefficient of less than 0.90 is indicative of acceptable discriminant validity to confirm that constructs are empirically distinct. In addition, HTMT values close to 1 indicate a lack of discriminant (Ab Hamid et al., 2017). As shown in Table 4.12, the construct of capability-internal control and capability-sustainable performance slightly exceeds the recommended threshold, indicating a potential lack of discriminant validity between these constructs, suggesting only a marginal concern for discriminant validity. According to the HTMT0.85 and HTMT0.90 criteria, all the values fulfil the criteria, which means that discriminant validity has been achieved, and it has been confirmed that all constructs are indeed distinct from each other.

Table 2 Convergent Validity

| Variables | Items | Loadings | CR | AVE | Convergent Validity (AVE > 0.5) |

| Strategic Planning | SP1 | 0.837 | 0.941 | 0.668 | YES |

| SP2 | 0.819 | ||||

| SP3 | 0.716 | ||||

| SP4 | 0.84 | ||||

| SP5 | 0.827 | ||||

| SP6 | 0.862 | ||||

| SP7 | 0.829 | ||||

| SP8 | 0.8 | ||||

| Internal Control | IC1 | 0.777 | 0.96 | 0.602 | YES |

| IC2 | 0.697 | ||||

| IC3 | 0.784 | ||||

| IC4 | 0.834 | ||||

| IC5 | 0.793 | ||||

| IC6 | 0.726 | ||||

| IC7 | 0.77 | ||||

| IC8 | 0.781 | ||||

| IC9 | 0.828 | ||||

| IC10 | 0.821 | ||||

| IC11 | 0.82 | ||||

| IC12 | 0.832 | ||||

| IC13 | 0.779 | ||||

| IC14 | 0.754 | ||||

| IC15 | 0.799 | ||||

| IC16 | 0.579 | ||||

| Capability | C1 | 0.782 | 0.959 | 0.596 | YES |

| C2 | 0.792 | ||||

| C3 | 0.812 | ||||

| C4 | 0.81 | ||||

| C5 | 0.688 | ||||

| C6 | 0.811 | ||||

| C7 | 0.783 | ||||

| C8 | 0.796 | ||||

| C9 | 0.687 | ||||

| C10 | 0.788 | ||||

| C11 | 0.762 | ||||

| C12 | 0.711 | ||||

| C13 | 0.759 | ||||

| C14 | 0.799 | ||||

| C15 | 0.799 | ||||

| C16 | 0.759 | ||||

| Sustainable Performance | EC1 | 0.712 | 0.944 | 0.586 | YES |

| EC2 | 0.595 | ||||

| EC3 | 0.826 | ||||

| EC4 | 0.831 | ||||

| S1 | 0.854 | ||||

| S2 | 0.808 | ||||

| S3 | 0.804 | ||||

| S4 | 0.765 | ||||

| EN1 | 0.802 | ||||

| EN2 | 0.656 | ||||

| EN3 | 0.761 | ||||

| EN4 | 0.727 |

Note: CR = Composite Reliability; AVE = Average Variance Extracted

Table 3 Discriminant validity (Fornell and Larcker)

| Construct | Capability | Internal Control | Strategic Planning | Sustainable Performance |

| Capability | 0.772 | |||

| Internal Control | 0.821 | 0.776 | ||

| Strategic Planning | 0.747 | 0.792 | 0.817 | |

| Sustainable Performance | 0.852 | 0.723 | 0.698 | 0.765 |

Table 4 Discriminant validity (HTMT)

| Construct | Capability | Internal Control | Strategic Planning | Sustainable Performance |

| Capability | ||||

| Internal Control | 0.853 | |||

| Strategic Planning | 0.782 | 0.838 | ||

| Sustainable Performance | 0.889 | 0.748 | 0.728 |

Structural model of the study

Collinearity

Variance Inflation Factor (VIF) is used to assess the degree of multicollinearity among independent variables in a regression model in line with the structural model assessment procedure outlined in (Joe F. Hair et al., 2019). We are assessing the structural model for collinearity issues by examining the VIF values to determine whether there is multicollinearity among the independent latent constructs that influence the dependent constructs in the model. All the VIF values are below 5, suggesting no serious concern about multicollinearity affecting the regression model. A rule of thumb is that VIFs between 1 and 5 indicate moderate multicollinearity (Henseler et al., 2009). So, collinearity is not at critical levels (Table 5), and the VIF values appear well-specified without causing issues in estimating regression coefficients.

Table 5 Collinearity Statistics (VIF)

| Independent Variables | Capability | Sustainable Performance |

| Capability | 3.468 | |

| Internal Control | 4.249 | |

| Strategic Planning | 1 | 2.913 |

Significant and relevance of the path coefficient

In line with Henseler et al. (2009), the bootstrapping procedure was applied in PLS path modelling (108 cases, 5,000 samples, two-tailed) to evaluate the structural model and determine the statistical significance of path coefficients. By supporting the PLS structural model assessment, different criteria are considered, including R², the goodness-of-fit (GoF) index, and the Stone–Geiser Q² test for predictive relevance (Chin, 1998; Hair Jr et al., 2014; Sarstedt et al., 2017). Chin (1998) described R² values of 0.25 as acceptable. While the model fit is relatively tiny according to absolute standards (Joseph F. Hair et al., 2022), we consider it suitable for this study because of the model’s low complexity. Moreover, the standard root mean squared residual (SRMR) met the required threshold of SRMR < 0.08, indicating that the model fit was satisfactory. The goodness-of-fit criterion proposed by Hu & Bentler (1998) indicates that it confirmed the data fit the theory well.

As shown in Table 6, the assessment of the path coefficient shows that H3 is supported out of three hypotheses, while the other two hypotheses that are not supported include H1 and H2. The path related to hypothesis H3 was found to be statistically significant; the results indicate that (t-value = 7.673, p < 0.05), suggesting a strong positive effect of construct C on SPO (ꞵ= 0.772). Thus, H3 is supported. In contrast, regarding the relationship between SP and SPO, the results revealed that SP (ꞵ= 0.137, t-value = 1.519, p>0.05) is not significantly related, and H1 is not supported. Similarly, IC (ꞵ= -0.037, t-value = 0.292, p>0.05) is negatively associated with the SPO and contradicts the proposed hypothesis in this study; thus, H2 is also not supported. Such non-significant results may imply that these predictors (SP and IC) do not have a measurable impact on SPO within this study’s sample.

Table 6 Structural Model Assessment

| Hypothesis | Std Beta (ꞵ) | Std Error | t-value | p-value | LL | UL | Decision |

| H1 SP → SPO | 0.137 | 0.09 | 1.519 | 0.129 | -0.038 | 0.317 | Rejected |

| H2 IC → SPO | -0.037 | 0.126 | 0.292 | 0.77 | -0.269 | 0.213 | Rejected |

| H3 C → SPO | 0.772 | 0.101 | 7.673 | 0 | 0.58 | 0.973 | Supported |

Notes:

Two-tailed test was conducted on the hypothesis direct relationships

A=Accepted

R=Rejected

LL = Bias corrected interval lower limit, UL = Bias corrected interval upper limit

Mediating effects of capability

Table 7 depicts the bootstrapping results, demonstrating the organisational competence mediating effect on the relationship between strategic planning and organisational performance. The mediating effects showed significant results in 5,000 repetitions of bootstrapping since 0 was not included between the lower and upper bounds of the bias-corrected confidence interval. In particular, the significance was maintained by using the Bootstrap techniques. It is confirmed as partial mediation (p < 0.05); strategic planning → capability → sustainable performance showed moderately strong partial mediation, with a capability of 77.24% of the relationship between strategic planning (SP) and sustainable performance (SPO) exists, signifying that capability plays a critical role in strengthening this relationship.

Table 7 Significance testing of mediating effects with bootstrap

| Relationship | Direct Effect | Indirect Effect | Total Effect | VAF | Remarks |

| H4 SP → C → SPO | 0.747 | 0.577 | 0.747 | 77.24% | Significant |

Note (s):

Threshold limit of VAF

0 – 20%: No Mediation

20 – 80%: Partial Mediation

Above 80%: Full Mediation

(Baron & Kenny, 1986; Zhao et al., 2010)

Moderating effects of strategic planning

One hypothesis was developed to examine the moderating effect of strategic planning on the relationship between internal control and sustainable performance. To assess the moderating effect of a construct in PLS-SEM, a study is required to develop an interaction effect between the moderator and the predicting variables and examine its effect on the endogenous variable. Table 8 shows the result of the moderating effect assessment. The interaction effect result (β = -0.060, t-value = 1.274) suggests that strategic planning does not moderate the relationship between internal control and sustainable performance. Implying strategic planning (SP) negatively moderates the relationship between internal control (IC) and sustainable performance (SPO), meaning that the influence of IC on SPO diminishes as SP increases. Thus, H5 is not supported.

Table 8 Moderation Assessment

| Hypothesis | Std Beta (ꞵ) | Std Error | t-value | p-value | LL | UL | Decision |

| H5 SP x IC → SPO | -0.06 | 0.047 | 1.274 | 0.203 | -0.164 | 0.021 | Rejected |

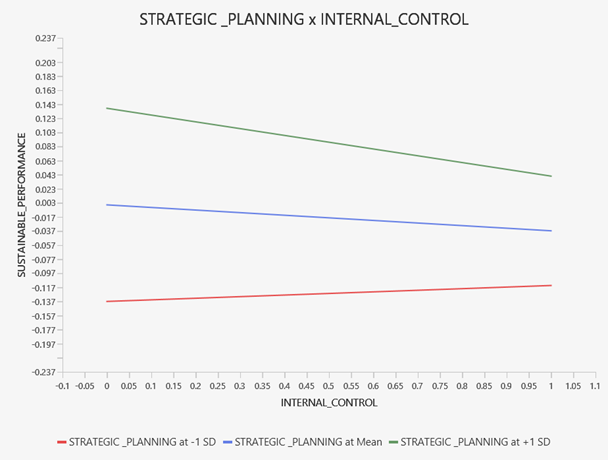

Figure 5 represent the relationship between IC (x-axis) and SPO (y-axis). The middle line represents the relationship for an average level of the SP. The other two lines represent the relationship between IC and SPO for higher (i.e., the mean value of SP plus one standard deviation unit) and lower (i.e., the mean value of SP minus one standard deviation unit) levels of the moderator variable SP. As can be seen, the relationship between IC and SPO varies depending on the SP level, indicating that SPO tends to decrease as IC increases. Due to the negative moderating effect, at high levels of the moderator SP, the effect of IC on SPO is weaker, while at lower levels of moderator SP, the effect of IC on SPO is stronger. These results clearly support that SP exerts a significant and negative moderating effect on the relationship between IC and SPO. The higher the strategic planning, the weaker the relationship between internal control and sustainable performance.

Figure 5. The moderating effect of strategic planning on internal control and sustainable performance

CONCLUSION

Summary of the research

The current study examined strategic planning, internal control, and the capability of cooperative sectors in Malaysia to achieve sustainable performance. Specifically, performance was measured using subjective measurement for non-financial indicators encompassing economic, social, and environmental dimensions. The findings show that capability significantly and positively affects sustainable performance, while strategic planning and internal control do not. Further, capability was proposed to mediate the relationship between strategic planning and sustainable performance. The findings show that capability has mediated the relationship between strategic planning and sustainable performance. In addition, strategic planning was proposed to moderate the relationship between internal control and sustainable performance. However, strategic planning has a nonsignificant moderating effect on the relationship between internal control and sustainable performance.

Theoretical Implications

First, this study examined strategic planning, internal control, and capability toward sustainable performance in the context of cooperatives, which is still limited. This study offers new perspectives on this relationship, particularly in cooperatives. The empirical findings contribute to the literature suggesting that the relationship between strategic planning, internal control, and capability in achieving sustainable performance paid a little attention, particularly in the context of cooperative. This fills a gap in the literature, as most studies focus on for-profit or non-profit organisations. Therefore, it enriches the knowledge to enhance the understanding of how cooperatives operate and what factors contribute to their performance.

Moreover, this study contributes to the literature by highlighting the mediating and moderating roles of capability and strategic planning to the sustainable performance of cooperatives in Malaysia, which lack attention has focused on. The findings reveal that a positive mediating relationship supports the Dynamic Capability View (DCV) theory, which emphasizes the important role of capabilities in achieving organisational success. DCV posits that organisational capabilities such as adaptability, learning, and innovation are essential for achieving competitive advantage and sustainability. This empirical support underscores the value of dynamic capabilities within cooperatives, reinforcing that these organisations can benefit from developing capabilities to drive performance and resilience in a changing market by finding a positive direct and indirect relationship between capability and sustainable performance.

Capability is an important factor in organisational performance (Karman & Savanevičienė, 2021; Taghizadeh et al., 2020). The capability to respond to market demands, utilize resources efficiently, and build trust among cooperative members may achieve sustainable growth and performance. In the context of this study, capability is a mediator in the relationship between strategic planning and sustainable performance. This implies that the effectiveness of strategic planning may depend significantly on the organisation’s capabilities, and without sufficient capability, even well-structured plans may not lead to sustainable performance. Our results support the role of capability in a direct relationship between sustainable performance and as a mediator in the relationship between strategic planning and sustainable performance. Therefore, this study contributes to the new literature by studying beyond previous studies that have examined capability as an independent variable or as a mediator, but not between strategic planning and sustainable performance.

In contrast, the study found a negative moderating relationship between internal control and sustainable performance through strategic planning, suggesting there is no interaction to enhance cooperative performance. This finding differs from some expectations in the literature, indicating that strategic planning alone may not enhance sustainable performance when internal controls are weak or misaligned with cooperative objectives. Therefore, this study fills a gap in the literature by providing a nuanced understanding of the complex relationships between strategic planning, capability, internal control, and sustainable performance in the cooperative sector.

Practical Implications

The findings show important implications for practice. First, this study highlights that strategic planning is less effective in cooperatives than for-profit organisations. Cooperative leaders should reconsider how strategic planning is integrated into their operations to provide quality products and services, create opportunities that respond to market changes, and advance technology utilization, processes, and business models to perform better. As a result, it may lead to effective strategic planning implementation appropriate to the internal control structure of a unique cooperative. Despite some studies, like George et al. (2019), showing that strategic planning significantly impacts organisational performance and disputes the argument that strategic planning is ineffective, which causes the organisation to become inflexible. However, the empirical evidence in this study revealed insignificant direct and moderating effect results. This shows that organisations tend to focus on resource allocation, long-term goals, and market positioning while paying less attention to ensuring the effectiveness of strategic planning, leading to inefficient management. Therefore, managers should adopt a more balanced approach, ensuring strategic planning actively informs decision-making processes and operational controls.

Second, internal control systems are typically designed to ensure compliance, mitigate risks, and safeguard assets. In cooperatives, it often focuses on governance, transparency, accountability, and motivation to members. Bakar et al. (2020) affirm that all internal control components in cooperatives contribute significantly to risk management. This stated that implementing strong internal control is appropriate to ensure cooperative productivity and operations are secured from fraud or unethical activities within cooperative business operations. Consistent with this, Shabri et al. (2016) argued that the impact of an internal control system on cooperatives is significant, contributing to their profitability, stability, and growth, thereby helping achieve objectives and improving organisational performance. When internal control is adequate, the financial statement report produced is compliant and functions as a monitoring procedure (Russo, 2019). This highlights the need for cooperative leaders to create internal control frameworks that are more concise to ensure they can assess directly and practice it in a cooperative context. Internal control is important in cooperatives, as it leads to better performance. Despite the importance of internal controls, the findings from this study reveal that internal control systems do not significantly affect sustainable performance in cooperatives. The findings illustrate that not all cooperatives in Malaysia have implemented effective and efficient internal control, which has led to increased cooperative performance. It was recommended that cooperatives implement how to create a good and functioning internal control system that focuses on stability and risk mitigation, which may hinder innovation and adaptability.

Third, the capability is fundamental for managing organisations. Generally, capability is defined as skills, processes, and knowledge that enable a cooperative to execute its goals effectively. By developing capability, cooperatives can achieve operational efficiency, innovation, and adaptability, leading to better performance. According to this study, empirical findings stated that capability has the largest either direct or mediate effect on cooperative performance. Moreover, although capability is significant in improving performance, organisations must be careful of its possible dark side effects unless the organisation has a strong entrepreneurial culture. Organisations should also foster a common understanding of their objectives. This study demonstrates how important capability is for sustainable performance. When cooperative capability is high, this will lead to an increase in performance. By that, cooperatives must focus on developing and strengthening core capabilities, such as leadership, innovation, and operational efficiency, to ensure long-term sustainable performance. For instance, they invest in leadership development, employee training, and technology adoption to improve decision-making and operational efficiency. This aligns with the unique cooperative context and, in turn, remains competitive and sustainable in changing market conditions.

Limitation

Despite its multifaceted contribution, our study has the following limitations: Firstly, since it focuses on selected top 100 and 350 medium or large cooperatives in Malaysia, there is not enough evidence to describe the importance of strategic planning, internal control, and capability toward enhancing sustainable performance. Lastly, as this study uses a questionnaire as the research instrument, the results are based on the data collected, which may affect the answer’s accuracy. Therefore, the answers provided by the respondents might not reflect the real practices of the cooperatives.

Future research

On the other hand, more research related to this topic with different variables could be carried out for future research. In addition, there are not many studies which examine the strategic planning, internal control, and capability of cooperatives in Malaysia. Thus, this provides some opportunities for future research.

REFERENCES

- ‘Aini, Y. M., Hafizah, H. A. K., & Zuraini, Y. (2012). Factors Affecting Cooperatives’ Performance in Relation to Strategic Planning and Members’ Participation. Procedia – Social and Behavioral Sciences, 65, 100–105. https://doi.org/10.1016/j.sbspro.2012.11.098

- Ab Hamid, M. R., Sami, W., & Mohmad Sidek, M. H. (2017). Discriminant Validity Assessment: Use of Fornell & Larcker criterion versus HTMT Criterion. Journal of Physics: Conference Series, 890(1). https://doi.org/10.1088/1742-6596/890/1/012163

- Abbas, J., Raza, S., Nurunnabi, M., Minai, M. S., & Bano, S. (2019). The impact of entrepreneurial business networks on firms’ performance through a mediating role of dynamic capabilities. Sustainability (Switzerland), 11(11). https://doi.org/10.3390/su11113006

- Acosta-Prado, J. C., & Tafur-Mendoza, A. A. (2022). Examining the mediating role of dynamic capabilities in the relationship between information and communication technologies and sustainable performance capabilities. VINE Journal of Information and Knowledge Management Systems. https://doi.org/10.1108/VJIKMS-10-2021-0257

- Agbejule, A., & Jokipii, A. (2009). Strategy, control activities, monitoring and effectiveness. Managerial Auditing Journal, 24(6), 500–522. https://doi.org/ 10.1108/ 02686900910966503

- Akisik, O., & Gal, G. (2017). The impact of corporate social responsibility and internal controls on stakeholders’ view of the firm and financial performance. Sustainability Accounting, Management and Policy Journal, 8(3), 246–280. https://doi.org/10.1108/SAMPJ-06-2015-0044

- Al-Ababneh, M. M. (2020). Linking Ontology, Epistemology and Research Methodology. Science & Philosophy, 8(1), 75–91. https://doi.org/10.23756/sp.v8i1.500

- Alam, M. M., Said, J., & Abd Aziz, M. A. (2019). Role of integrity system, internal control system and leadership practices on the accountability practices in the public sectors of Malaysia. Social Responsibility Journal, 15(7), 955–976. https://doi.org/10.1108/SRJ-03-2017-0051

- Ali, H., Chen, T., & Hao, Y. (2021). Sustainable manufacturing practices, competitive capabilities, and sustainable performance: moderating role of environmental regulations. Sustainability (Switzerland), 13, 1–18. https://doi.org/10.3390/su131810051

- Altman, M. (2008). Cooperatives, History and Theories of. International Encyclopedia of Civil Society. https://doi.org/10.1007/springerreference_75642

- Aris, N. A., Marzuki, M. M., Othman, R., Rahman, S. A., & Ismail, N. H. (2018). Designing indicators for cooperative sustainability: The Malaysian perspective. Social Responsibility Journal, 14(1), 226–248. https://doi.org/10.1108/SRJ-01-2017-0015

- Attia, A., & Salama, I. (2018). Organizational learning, knowledge management capability and supply chain management practices in the Saudi food industry. Business Process Management Journal, 22(6), 1217–1242. https://doi.org/10.1108/JKM-09-2017-0409

- Bakar, N. M., Rahman, R. A., & Ibrahim, Z. (2020). Client protection and sustainable performance in microfinance institution. International Journal of Productivity and Performance Management, 69(4), 651–665. https://doi.org/10.1108/IJPPM-03-2019-0127

- Baron, R. M., & Kenny, D. A. (1986). The Moderator-Mediator Variable Distinction in Social Psychological Research. Conceptual, Strategic, and Statistical Considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Baumgartner, R. J. (2014). Managing corporate sustainability and CSR: A conceptual framework combining values, strategies and instruments contributing to sustainable development. Corporate Social Responsibility and Environmental Management, 21(5), 258–271. https://doi.org/10.1002/csr.1336

- Baumgartner, R. J., & Rauter, R. (2017). Strategic Perspectives of Corporate Sustainability Management To Develop A Sustainable Organization. Journal of Cleaner Production. https://doi.org/10.1016/j.jclepro.2016.04.146.

- Belhadi, A., Kamble, S., Gunasekaran, A., & Mani, V. (2021). Analyzing the mediating role of organizational ambidexterity and digital business transformation on industry 4.0 capabilities and sustainable supply chain performance. Supply Chain Management. https://doi.org/10.1108/SCM-04-2021-0152

- Bernama (2020). Cooperatives can contribute more than 3-4 % to GDP. Focus Malaysia, 2020.

- Bruwer, J. P., Coetzee, P., & Meiring, J. (2018). Can internal control activities and managerial conduct influence business sustainability? A South African SMME perspective. Journal of Small Business and Enterprise Development, 25(5), 710–729. https://doi.org/10.1108/JSBED-11-2016-0188

- Camisón-Zornoza, C., Forés-Julián, B., Puig-Denia, A., & Camisón-Haba, S. (2020). Effects of ownership structure and corporate and family governance on dynamic capabilities in family firms. International Entrepreneurship and Management Journal, 16(4), 1393–1426. https://doi.org/10.1007/s11365-020-00675-w

- Caska, & Indrawati, H. (2017). The Impacts of the Strategic Planning Implementation on the Cooperative Members′ Participation. Mediterranean Journal of Social Sciences, 8(3), 99–107. https://doi.org/10.5901/mjss.2017.v8n3p99

- Cheah, J. H., Magno, F., & Cassia, F. (2024). Reviewing the SmartPLS 4 software: the latest features and enhancements. Journal of Marketing Analytics, 12(1), 97–107. https://doi.org/10.1057/s41270-023-00266-y

- Chin, W. W. (1998). The partial least squares approach to structural equation modeling. Modern methods for business research. Modern Methods for Business Research, 295(2),295-336.http://books.google.com.sg/books?hl=en&lr=&id=EDZ5AgAAQBAJ&oi=fnd&pg=PA295&dq=chin+1998+PLS&ots=47qB7ro0np&sig=rihQBibvT6S-Lsj1H 9txe9dX6Zk#v=onepage&q&f=false

- Chungyas, J. I., & Trinidad, F. L. (2022). Strategic Management Practices and Business Performance of Cooperatives in Ifugao, Philippines: Basis for Strategic Planning Model. International Journal of Management & Entrepreneurship Research, 4(2), 84–104. https://doi.org/10.51594/ijmer.v4i2.293

- Comin, L. C., Aguiar, C. C., Sehnem, S., Yusliza, M. Y., Cazella, C. F., & Julkovski, D. J. (2019). Sustainable business models: a literature review. Benchmarking, 27(7), 2028–2047. https://doi.org/10.1108/BIJ-12-2018-0384

- Damina Makut, M., & Abbas Ibrahim, U. (2021). Effect of Internal Control on Performance of Cooperatives in Nigeria: A Case Study of CSM Cooperative Society Abuja, Nigeria. Science Journal of Business and Management, 9(3), 197. https://doi.org/10.11648/j.sjbm.20210903.16

- Day, G. S. (1994). The Capabilities of Market-Driven Organizations. Journal of Marketing, 58(4), 37–52. https://doi.org/10.1177/002224299405800404

- DiMaggio, P. J., & Powell, W. W. (1983). The iron cage revisited institutional isomorphism and collective rationality in organizational fields. American Sociological Review, 48(4), 147–160. https://doi.org/10.1016/S0742-3322(00)17011-1

- Dlamini, N., Mazenda, A., Masiya, T., & Nhede, N. T. (2020). Challenges to strategic planning in public institutions: A study of the Department of Telecommunications and Postal Services, South Africa. International Journal of Public Leadership, 16(1), 109–124. https://doi.org/10.1108/IJPL-10-2019-0062

- Donkor, J., Donkor, G. N. A., & Kwarteng, C. K. (2018). Strategic planning and performance of SMEs in Ghana. Asia Pacific Journal of Innovation and Entrepreneurship, 12(1), 62–76. https://doi.org/10.1108/apjie-10-2017-0035

- Elkington, J. (1998). Accounting for Triple Bottom Line. Measuring Business Excellence, 2(3), 1–240. https://doi.org/10.4324/9780203996737

- Fadzil, F. H., Haron, H., & Jantan, M. (2005). Internal auditing practices and internal control system. Managerial Auditing Journal, 20(8), 844–866. https://doi.org/ 10.1108/02686900510619683

- Fahed-Sreih, J., & El-Kassar, A. N. (2017). Strategic Planning, Performance and Innovative Capabilities of Non-Family Members in Family Business. International Journal of Innovation Management, 21(7), 1–24. https://doi.org/10.1142/S1363919617500529

- Fahim, N. A., & Baharun, R. (2017). Analyzing the mediating effect of innovation capability on strategic orientations in agricultural Malaysia. WSEAS Transactions on Business and Economics, 14, 253–262.

- Fauzi, H., Svensson, G., & Rahman, A. A. (2010). “Triple bottom line” as “sustainable corporate performance”: A proposition for the future. Sustainability, 2(5), 1345–1360. https://doi.org/10.3390/su2051345

- Fornell, C., & Larcker, D. F. (1981). Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.2307/3151312

- George, B., Walker, R. M., & Monster, J. (2019). Does Strategic Planning Improve Organizational Performance? A Meta-Analysis. Public Administration Review, 79(6), 810–819. https://doi.org/10.1111/puar.13104

- Gold, A. H., Malhotra, A., & Segars, A. H. (2001). Knowledge management: An organizational capabilities perspective. Journal of Management Information Systems, 18(1), 185–214. https://doi.org/10.1080/07421222.2001.11045669

- Gupta, S., Meissonier, R., Drave, V. A., & Roubaud, D. (2019). Examining the impact of Cloud ERP on sustainable performance: A dynamic capability view. International Journal of Information Management, 1–13. https://doi.org/10.1016/j.ijinfomgt.2019.10.013

- Hair, J.F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hair, J.F, Hult, G. T. ., Ringle, C. ., Sarstedt, M., Danks, N. ., & Ray, S. (2021). Partial Least Squares Structural Equation Modeling. In Handbook of Market Research. https:// doi.org/10.1007/978-3-319-57413-4_15

- Hair, Joe F., Risher, J. J., Sarstedt, M., & Ringle, M. C. (2019). When to use and how to report the results of PLS-SEM. European Business Review.

- Hair, Joseph F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2022). A Primer on Partial Least Squares Structural Equation Modeling. SAGE Publications, Inc. https://doi.org/10.1016/j.lrp.2013.01.002

- Hair, Joseph F., Sarstedt, M., Pieper, T. M., & Ringle, C. M. (2012). The Use of Partial Least Squares Structural Equation Modeling in Strategic Management Research: A Review of Past Practices and Recommendations for Future Applications. Long Range Planning, 45(5–6), 320–340. https://doi.org/10.1016/j.lrp.2012.09.008

- Hair Jr., J. F., Matthews, L. M., Matthews, R. L., & Sarstedt, M. (2017). PLS-SEM or CB-SEM: updated guidelines on which method to use. International Journal of Multivariate Data Analysis, 1(2), 107. https://doi.org/10.1504/ijmda.2017.10008574

- Hair Jr, J. F., Sarstedt, M., Hopkins, L., & Kuppelwieser, V. G. (2014). Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review, 26(2), 106–121. https://doi.org/10.1108/EBR-10-2013-0128

- Hall, J. A., Systems, A. I., & Hall, J. A. (2004). Ethics, fraud, and internal control.

- Henseler, J., Hubona, G., & Ray, P. A. (2016). Using PLS path modeling in new technology research: Updated guidelines. Industrial Management and Data Systems, 116(1), 2–20. https://doi.org/10.1108/IMDS-09-2015-0382

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Henseler, J., Ringle, C. M., & Sinkovics, R. R. (2009). The use of partial least squares path modeling in international marketing. Advances in International Marketing, 20(2009), 277–319. https://doi.org/10.1108/S1474-7979(2009)0000020014

- Hu, L. T., & Bentler, P. M. (1998). Fit Indices in Covariance Structure Modeling: Sensitivity to Underparameterized Model Misspecification. Psychological Methods, 3(4), 424–453. https://doi.org/10.1037/1082-989X.3.4.424

- Hult, G. T. M., & Ketchen, D. J. (2001). Does market orientation matter?: A test of the relationship between positional advantage and performance. Strategic Management Journal, 22(9), 899–906. https://doi.org/10.1002/smj.197

- International Cooperative Alliance. (2023). Exploring the Co-operative Economy.

- International Federation of Accounting (IFAC). (2011). Global survey on risk management and internal control. In Professional Accountants in Business Committee (Issue February). http://www.ifac.org/sites/default/files/publications/files/global-survey-on-risk-manag.pdf

- Ismail, M., Zainol, F. A., Yusoff, M. N. H., & Rusuli, M. S. C. (2019). The driving force of the business sustainability model among co-operatives in Malaysia. Journal of Social Sciences Research, 5(3), 826–829. https://doi.org/10.32861/jssr.53.826.829

- Junges, I., Dias, F. T., França, B., & Osório de Andrade Guerra, J. B. S. (2022). Sustainable Development and Climate Change Adaptation: a Case Study About Strategic Planning and Challenges in a Family-Farmers’ Cooperative. MIX Sustentável, 9(1), 109–125. https://doi.org/10.29183/2447-3073.mix2023.v9.n1.109-125

- Kamalrulzaman, N. A., Ahmad. A, Ariff, A. M., & Muda, M. S. (2021). Innovation Capabilities and Performance of Malaysian Agricultural SMEs: The Moderating Role of Strategic Alliance. International Journal of Business and Society, 22(2), 675–695. https://doi.org/10.33736/ijbs.3751.2021

- Karman, A., & Savanevičienė, A. (2021). Enhancing dynamic capabilities to improve sustainable competitiveness: insights from research on organisations of the Baltic region. Baltic Journal of Management, 16(2), 318–341. https://doi.org/10.1108/BJM-08-2020-0287

- Kasmir, S. (2016). The Mondragon Cooperatives: Successes and Challenges. Global Dialogue.

- Koeswayo, P. S., Haryanto, H., & Handoyo, S. (2024). The impact of corporate governance, internal control and corporate reputation on employee engagement: a moderating role of leadership style. Cogent Business and Management, 11(1). https://doi.org/10.1080/23311975.2023.2296698

- Korkmaz, G. (2020). The Moderating Effect of Internal Audit in Strategic Planning Implementation Success. Istanbul Management Journal, 88, 57–84. https://doi.org/10.26650/imj.2020.88.0003

- Kwalanda, J. W., Mukanzi, C. D., & Onyango, R. (2017). Effect of Dynamic Managerial Capabilities on Organizational Performance: A Survey of Western Kenya Sugar Industry. Journal of Business and Management, 19(12), 13–20. https://doi.org/10.9790/487X-1912061320

- Kylaheiko, K., Puumalainen, K., Sjögrén, H., Syrjä, P., & Fellnhofer, K. (2016). Strategic planning and firm performance: A comparison across countries and sectors. International Journal of Entrepreneurial Venturing, 8(3), 280–295. https://doi.org/10.1504/IJEV.2016.078965

- Länsiluoto, A., Jokipii, A., & Eklund, T. (2016). Internal control effectiveness – a clustering approach. Managerial Auditing Journal, 31(1), 5–34. https://doi.org/10.1108/MAJ-08-2013-0910

- Latifah, L., Setiawan, D., Aryani, Y. A., & Rahmawati, R. (2021). Business strategy – MSMEs’ performance relationship: innovation and accounting information system as mediators. Journal of Small Business and Enterprise Development, 28(1), 1–21. https://doi.org/10.1108/JSBED-04-2019-0116

- Lawrence, T. ., & Shadnam, M. (2008). Institutional theory. In Institutional Theory. The International Encyclopedia of Communication. https://doi.org/doi:10.1002/ 9781 405186407.wbieci035

- Liu, C. H., Chang, A. Y. P., & Fang, Y. P. (2020). Network activities as critical sources of creating capability and competitive advantage: The mediating role of innovation capability and human capital. Management Decision, 58(3), 544–568. https://doi.org/10.1108/MD-08-2017-0733

- Malaysia’s Official Statistics. (2021). Malaysia Economic Performance Fourth Quarter 2020 (Issue February).

- Mathibe, M. S., Chinyamurindi, W. T., & Hove-Sibanda, P. (2023). Value co-creation as a mediator between strategic planning and social enterprise performance. Social Enterprise Journal, 19(1), 23–39. https://doi.org/10.1108/SEJ-08-2021-0062

- Morshidi, M. H., Hilman, H., & Mohd Yusoff, Y. (2021). Strategic Orientation and Organisational Commitment on Co – Operative Performance in Malaysia : a Conceptual Framework. Journal of Management Information and Decision Sciences, 24(1), 1–17.

- Muhsin Thaji, M. K., Qasim Hasan, D. H., Raad Ibrahim, D. I., Ali Hussein, M. S., & Hussein, M. T. (2022). the Role of Strategic Leadership in Crisis Management Through Strategic Planning As a Moderator Variable. International Journal of Research in Social Sciences & Humanities, 12(04), 680–698. https://doi.org/10.37648/ijrssh.v12i04.036

- Musa, D., Musa, I., & Muhammad, N. (2020). Business Performance of Cooperatives in Malaysia : Issues , Challenges and Future Direction Background of the Study. Technical and Vocational Education (JTVE), 5(1), 27–40.