The Effect of Debt Service Ratio and Exchange Rate on Public Debt Sustainability in Kenya

- Yabesh Ombwori Kongo

- Elvis Kimani Kiano

- Joash Ogolla Ogada

- Peter Isaboke Omboto

- 302-312

- Nov 30, 2023

- Sustainability

The Effect of Debt Service Ratio and Exchange Rate on Public Debt Sustainability in Kenya

Yabesh Ombwori Kongo*, Elvis Kimani Kiano, Joash Ogolla Ogada and Peter Isaboke Omboto

Department of Economics, Moi University, Kenya

*Corresponding Author

DOI: https://dx.doi.org/10.47772/IJRISS.2023.7011024

Received: 31 October 2023; Revised: 08 November 2023; Accepted: 13 November 2023; Published: 30 November 2023

ABSTRACT

This study investigated the impact of the debt service ratio and exchange rate on the sustainability of Kenya’s debt. Since the 1970s, governments worldwide have struggled with unsustainable fiscal conduct. Kenya’s overall governmental debt rose close to 69 percent of GDP by the end of 2022 from 48.6 percent in 2015. For a nation’s macroeconomic and financial health, debt sustainability means the government can satisfy its financial obligations without special help or defaults and provides citizens with trust in the government’s financial management. Conversely, unsustainable debt diverts tax income from vital social and development projects, compromising government spending. The choice of debt service ratio and exchange rate lies in their role as crucial indicators that reflect a nation’s fiscal well-being and its ability to successfully handle its debt. The study applied time series data (1990-2021) and the Vector Error Correction Model to establish the relationship between the study variables. The study established a statistically significant negative association between Kenya’s debt sustainability and debt service ratio. At greater levels, the debt service ratio hurts public debt sustainability. The study further established that exchange rate depreciation negatively affects public debt sustainability. Considering the findings, the government may consider monitoring and manage the debt-service ratio to sustain the public debt level. Negotiating better borrowing conditions or debt repayment plans can lower this ratio and assist maintain a sustainable debt level. Public debt sustainability requires exchange rate stability. To lessen the negative impact on public debt sustainability, policymakers may employ foreign exchange reserves or hedging options. Finally, economic diversification and debt management that supports sustainable development may improve long-term resilience and public debt repayment while boosting economic growth.

Keywords: Public Debt Sustainability, Debt Service Ratio, Exchange Rate, Kenya

BACKGROUND INFORMATION

To achieve its objectives outlined in Vision 2030, Kenya has undertaken ambitious infrastructure initiatives, such as the Lamu Port South Sudan-Ethiopia Transport Project (LAPSSET) and the Standard Gauge Railway (SGR). The Standard Gauge Railway (SGR) was constructed between October 2016 and January 2018, at a total expenditure of US$3.6 billion. The project was financed mostly by a loan from the Exim Bank of China, accounting for 90 percent of the finances, while the Kenyan government contributed the remaining 10 percent. Furthermore, the nation embarked on the development of geothermal power generation, requiring significant financial resources that beyond the government’s capacity for revenue collection. To address the disparity between revenue and spending, the government opted to engage in borrowing (GOK, 2019).

Due to the implementation of these ambitious initiatives and the worldwide impact of the COVID-19 pandemic in the year 2020, Kenya experienced a substantial increase in its overall public debt. Specifically, Kenya’s total public debt has risen from 48.6 percent of GDP at the end of 2015 to an estimated 72.3% percent of GDP by the end of 2022 (IMF, 2022). As of May 2023, the public debt stock in Kenya amounted to Kshs. 9.6 trillion, which accounts for 96 percent of the Kshs. 10 trillion PFM Act Debt Limit. It is also estimated that Kenya’s domestic debt was Kenya Shillings 4.36 trillion, external public debt was Kenya Shillings 4.33 trillion, representing 50.1% and 49.8% respectively. (CBK, 2023).

According to the International Monetary Fund (IMF), it is recommended that emerging countries maintain public debt-to-GDP ratios below 40% (IMF, 2010). The public debt to GDP ratio of Kenya experienced a decline from 64.1 percent in June 2003 to 38.1 percent in June 2012. However, it subsequently exhibited an increase, mostly attributed to expenditures on infrastructure development and the financial burdens incurred because of the COVID-19 pandemic. The stabilizing effect and potential for economic growth associated with external debt have been emphasized by Mohsin, et al., (2021). Nonetheless, the reimbursement of both interest and principal on external debt takes place in a foreign currency, which has the potential to exhaust foreign exchange reserves and result in a devaluation of the local currency.

The Republic of Kenya is currently facing substantial hurdles in its development and debt sustainability endeavors due to its notable external debts and the increasing burden of debt. According to KIPPRA (2023), the public debt stock stood at Ksh 9.4 trillion as of March 2023, which was below the Ksh 10 trillion limit. The proportion of external debt in the whole public debt stock is 51.7%, with multilateral debt being the dominant component at 46.3%. Commercial debt and bilateral debt make up 25.8% and 24.7% of the total, respectively. Rising levels of debt give rise to a range of potential concerns, such as heightened taxation, devaluation of the local currency, elevated borrowing expenses, and, most significantly, the displacement of the private sector.

Kenya’s public debt level is significantly higher in comparison to other member states of the East African Community (EAC). Tanzania’s debt-to-GDP ratio stood at roughly 41%, while Uganda’s was around 42%. Although Kenya has a greater debt level compared to these countries, the debt-to-GDP ratio can be influenced by the individual economic conditions and fiscal policies of each nation. Kenya’s debt ratio was comparatively lower than that of several other African countries on a broader African scale. As an example, Egypt had a notably higher debt-to-GDP ratio of around 89%, which indicates a greater burden of debt. Ethiopia had a debt level of approximately 55%, whereas Nigeria’s debt level was at 34% (IMF, 2021). The fluctuations in these ratios can be ascribed to disparities in economic structures, borrowing behaviors, and governmental policies. In comparison to countries outside of Africa, Kenya’s debt level was relatively lower. Japan’s debt-to-GDP ratio in 2020 was roughly 241%, which was one of the highest globally. The United States and the United Kingdom had ratios of approximately 128% and 97%, respectively. In 2020, China’s ratio stood at approximately 66%. (World Bank, 2022). It should however be noted that the sustainability of debt is not exclusively defined by the ratio of debt to GDP. It also relies on elements such as the structure of debt, interest rates, forecasts for economic growth, and the capacity to repay the loan. The high ratios observed in Kenya and certain non-African countries are a result of intricate economic processes and enduring structural issues.

Based on the above arguments, the study was guided by the following specific objectives:

- To determine the effect of debt service ratio on public debt sustainability in Kenya

- To evaluate the effect of exchange rate on public debt sustainability in Kenya

EMPIRICAL LITERATURE REVIEW

Debt Service Ratio and Public Debt Sustainability

The study conducted by Koh, Kose, Nagle, Ohnsorge, and Sugawara (2020) aimed to examine the impact of debt accumulation on 100 emerging and developing economies from 1970 onwards. The research findings indicated that the rapid accumulation of debt, regardless of whether it was incurred by the public or private sector, heightened the probability of a financial crisis. Additionally, a greater proportion of short-term external debt, increased debt servicing obligations, and diminished reserve coverage also contributed to this possibility.

The association between new borrowing, debt service, and the transmission of credit booms was investigated in a study done by Drehmann, Juselius, and Korinek (2023). The research findings suggest that the practice of obtaining financial resources through borrowing has a favorable effect on economic activity, as it contributes to the enhancement of growth. Nevertheless, it is crucial to acknowledge that this act of borrowing also sets a predetermined path for debt repayment, thereby reducing future economic productivity. The prolonged duration of debt service can be ascribed to two key analytical characteristics of credit booms, as indicated by their study findings: the positive relationship between new borrowing and the extended duration of loan contracts. The researchers’ investigation substantiated the data characteristics, providing evidence that the repayment of debt reaches its highest point four years after a surge in credit, and is correlated with a notable decrease in economic production and an elevated likelihood of experiencing a crisis.

Research has further demonstrated that fiscal mismanagement leads to instability in the realms of economy, politics, and society, particularly when governments enforce elevated tax rates on citizens as a means to address public debts (Remeikienė & Gaspareniene, 2023). Fosu (1999) and Green and Villanueva (1991) argue that allocating borrowed public funds towards consumptive expenditures leads to a situation of debt overhang, wherein debt service payments impede private investment and long-term economic growth rates. Furthermore, Clements et al. (2003) argue that elevated levels of foreign public debt servicing expenses lead to a significant rise in the government’s interest payments, ultimately leading to fiscally unsustainable deficits. According to Clements et al. (2003), an increase in government expenditure on foreign public debt repayments leads to a decrease in public savings and an elevation in domestic interest rates. Consequently, the escalation of borrowing expenses displaces private investment, so decelerating the pace of economic expansion. Clements et al. (2003) argue that the service costs of foreign public debt have a negative impact on economic growth. This is mostly due to the deterioration of the debtor country’s terms of trade, which leads to an increase in domestic tax rates and a decrease in returns on investment. In instances of utmost severity, when nations utilize natural resources, specifically minerals and agricultural yield, to settle external debts, the pace of resource depletion will be accelerated.

Likewise, the current body of theoretical literature provides evidence in favour of the proposition that the repayment of domestic public debt has an adverse effect on the growth trajectory of an economy. The allocation of government spending can be adversely affected by increased domestic debt service payments, leading to a reduction in resources allocated to industrial, infrastructure, human capital, and welfare endeavors. Consequently, this can result in a decline in economic growth (Soydan and Bedir, 2015; Abbas and Christensen, 2007). According to Teles and Mussolini (2014), long-term economic growth rates are negatively affected by the decrease in productive government spending capacity resulting from the rise in interest payments on domestic public debt. Considering the context, this study incorporates a variable that has received minimal attention in most of the literature reviewed. The significance of debt service ratios lies in their role as crucial indications of a nation’s capacity to meet its debt obligations.

Exchange Rate and Debt Sustainability

The research undertaken by Naveed and Islam (2022) investigated the determinants of public debt in Pakistan and evaluated its long-term viability using the debt dynamic methodology. The objective of the study was to examine the factors influencing the variations in debt levels and assess the sustainability of the nation’s public debt over an extended period. Furthermore, the study utilized the Autoregressive Distributed Lag (ARDL) methodology to analyze the temporal patterns of debt in both the immediate and extended periods. The dataset employed in this investigation encompassed past data from 1975 to 2021. The findings of the study indicate that there is a positive and statistically significant relationship between budget deficits, currency rate depreciation, and interest rates, and the level of public debt in Pakistan. On the other hand, Piscetek (2019) created a conceptual framework aimed at decomposing alterations in the public debt ratio of New Zealand into four distinct constituents, namely the primary balance, real GDP growth, real interest rates, and exchange rates. The study examined the debt dynamics of New Zealand across three distinct temporal intervals: the ten-year period after the Global Financial Crisis (2008-2018), a set of five-year estimates (2019-2023), and medium-term estimations spanning from 2024 to 2033. The research findings revealed a notable imbalance in the impact of several factors on the dynamics of public debt ratio in New Zealand. Based on the findings of the study, it is evident that the primary balance has a significant role in determining the public debt ratio, irrespective of whether it is positive or negative. In contrast, factors such as automatic debt dynamics, interest-growth differentials, and currency rates are comparatively less concerning in their impact on the public debt ratio.

In their study, Karadam and Özmen (2021) investigated the influence of real exchange rates on economic growth in a significant number of advanced and developing economies. To estimate conventional growth models that were enhanced with global financial conditions variables, the researchers employed panel autoregressive distributed lag (PARDL) and PARDL mean group (PARDL-MG) models. The research revealed that the conclusions drawn on the expansionary depreciation of developing economies are often rooted in a misreading of the coefficient of the error correction mechanism. The study proceeded to examine the correlation between the real exchange rate and economic growth in a more comprehensive manner, considering the often-neglected factors of balance sheet or foreign debt vulnerabilities in traditional literature on economic growth. The estimation findings of Fully Modified Ordinary Least Squares (OLS) analysis indicated that several external variables, which encompass global financial and monetary conditions, as well as conventional domestic variables like trade openness, human capital, and savings, exhibited a high level of significance in elucidating the growth patterns observed in developing economies. Additionally, the results of their study demonstrated that the depreciation of the real effective exchange rate has a contractionary effect on developing economies with large levels of external debt, whereas it has an expansionary effect on advanced economies. In contrast, increased trade openness mitigates the negative effects of real effective exchange rate depreciation on both advanced economies and developing economies.

Cahyadin and Ratwianingsih (2020) utilized the Autoregressive Distributed Lag Error Correction Model (ARDL-ECM) and conducted a Granger Causality test to examine the empirical model concerning external debt, currency rate, and unemployment within a designated group of ASEAN countries during the time frame from 1980 to 2017. The findings of their research indicated that the empirical models, particularly those pertaining to foreign debt, exchange rate, and unemployment, had short-term impacts. The results of the Granger causality analysis reveal a statistically significant relationship between foreign debt, exchange rate, and unemployment, particularly in the unique situation of Indonesia. Moreover, a significant correlation was observed in the interplay among external debt, exchange rate, and unemployment in specific ASEAN nations. Based on the findings of the study, it is recommended that governments give precedence to macroeconomic policies, including but not limited to ensuring stability in exchange rates, effectively managing external debt risks, and implementing policies that address the needs of the impoverished population.

The study conducted by Aleme (2019) investigated the factors influencing the sustainability of Ethiopia’s foreign debt by analyzing annual time series data spanning from 1980 to 2016. The findings of a log-linear regression analysis revealed that the debt service to GDP ratio and the real effective exchange rate exhibited statistically significant and positive correlations with debt sustainability in Ethiopia. The study conducted in Ethiopia revealed that the variables of terms of trade and foreign real interest rates exhibited statistical significance and demonstrated a negative correlation with debt sustainability. The research proposed the implementation of cautious domestic macroeconomic strategies to prevent the overvaluation of the real effective exchange rate and the deterioration of trade conditions.

In their study, Odera (2015) employed quarterly data to analyze the influence of external public debt on the volatility of the currency rate in Kenya. The time frame for the investigation spanned from 1993 to 2013. The Ordinary Least Square (OLS) technique was employed to construct a linear model, wherein the relationship between exchange rate volatility and several economic factors like inflation, interest rates, GDP growth rate, money supply to GDP ratio, and external debt to GDP ratio was examined. Based on the research findings, it was observed that the ratio of foreign debt to GDP exhibited a statistically significant negative impact on the volatility of the real exchange rate. Conversely, interest rates were shown to have a statistically significant positive influence. Moreover, the excessive and unmanageable foreign public debt of Kenya has been associated with significant fluctuations in the real exchange rate.

Ryan and Maana (2014) conducted a study on the sustainability of Kenya’s state debt by analyzing annual data from 1983 to 2013. The researchers employed both the co-integration and stochastic debt sustainability methodologies in their investigation. The results of the study indicate that the national debt is within manageable limits. Moreover, it was observed that during the study duration, the depreciation of currency rates did not provide any noteworthy impact on the average interest rates associated with external debt.

The study conducted by Basu, Basu, and Nag (2022) examined the impact of an unanticipated unfavorable shock, such as the COVID-19 pandemic, on the actual value of public debt in a small open economy characterized by both traded and non-traded sectors. Additionally, the researchers put out a crisis management strategy involving fiscal and monetary expansion. The research findings indicate that variations in the rates of adjustment in the real exchange rate, interest rate, and real value of debt, along with their numerous cross effects, influence the impact of policy-induced and external shocks. Moreover, the occurrence of an unanticipated adverse shock, such as the COVID-19 pandemic, leads to a contraction in both the traded and non-traded sectors. This contraction subsequently results in a reduction in consumption expenditure, investment expenditure, employment, and the real value of aggregate income in the short term. On the other hand, fiscal expansion leads to an increase in the real value of debt and a decrease in the real exchange rate.

RESEARCH METHODOLOGY

Target Population, Data Types and Sources

The paper targeted data from the period spanning 1990-2021 for all the study variables; dependent and independent. This paper used mainly annual secondary time series data which were sourced from Kenya National Bureau of Statistics Economic Surveys, and the Central Bank of Kenya. A nexus between the variables was investigated by analyzing the time series data on the study variables within the study period. The choice of this period was motivated by the availability of data and by the fact that it consists of the period where Kenya’s economy in the recent years, it has been characterized by high levels of fiscal deficits and increasing public debt to finance the deficits; and therefore, it is necessary for policymakers to know how sustainable this public debt is to the Kenyan economy and measures to contain the same. Further, the explanatory research design was adopted in this study since it provides a framework for investigating variables with the goal of either supporting or refuting the contention that the variables have a cause-and-effect relationship (Salkind, 2010). A positivist research philosophy was also adopted in this research.

Measurement of Variables

Public debt sustainability: The term “debt sustainability” refers to a country’s capacity to repay its debts without resorting to debt relief or building up penalties. The measurement of public debt is done in both absolute and relative terms. In absolute terms, public debt is defined as the total value of liabilities that obligate a borrowing government to pay the principal and chargeable interest. Public debt sustainability is assessed by considering the country’s economic potential, namely its capacity to repay the debt. The study utilized the debt to GDP ratio as an indicator of debt sustainability, in line with Dabrowski (2016).

Debt Service Ratio: Debt Service Ratio, which is a ratio of current debt service payments to revenues was measured as a ratio of accumulated debt service payments, including both partial debt redemption and interest payments, to current revenues. This is according to (Chugunov & Markuts, 2019; Drehmann and Juselius (2012). This ratio is regarded as an important indicator of a country’s debt burden (IMF, 2004).

Exchange Rate: The exchange rate is the rate at which currencies are exchanged between countries. It is also known as the value of one country’s currency in terms of other countries’ currencies (Alotaibi, 2016). According to Khan, Azim, and Syed (2014), the exchange rate is the price of a currency in relation to the other currencies. It expresses the national currency’s quotation in respect to foreign ones. In this study, the Kenya shilling in relation to the US dollar was used.

Pre-Estimation and Post-Estimation Tests

The study tested several requisites tests before estimating the VECM econometric model. These tests were stationary property of the data and assumptions of multivariate regression such as normality, multicollinearity, heteroscedasticity, and autocorrelation.

Stationarity Test: As discussed earlier VECM estimation requires vector of unique and non-constant elements to be stationary and ergodic stochastic process and that the VECM is suitable when data is integrated of order zero I (0) or order one (I(1)). Time series data are trending in nature and therefore prior to undertaking estimation, the trending effect must be removed. The conventional way of de-trending a non-stationary time series separates the trending from the cyclical component and removes the unit root (Bleikh, & Young, 2016). There are many tests used to detect the stationarity property of the data. In this paper, Augmented-Dickey-Fuller unit root test was used.

Dickey-Fuller GLS Test: Dickey–Fuller Generalized Least (GLS) square tests for a unit root in which the series has been transformed by a generalized least-squares regression (Elliott, Rothenberg, and Stock, 1996). This test is carried out on nested time series model to accommodate serial autocorrelation, auto covariance and covariance. Initially, the test is an augmented Dickey–Fuller test, except that the time series is transformed via a generalized least squares (GLS) regression before performing it (Dickey and Fuller 1979; Hamilton, 1994). Augmented Dickey-Fuller test involves fitting a regression model as follows.

Δyt=α+βyt-1+δt+ζ1 Δyt-1+ζ2 Δyt-2+⋯+ζk Δyt-k+εt………………..……..……1

Where, Δyt: Represents first difference of each variable, β: Represents the co-efficient of the lagged variable, k is the number of lags that were specified using lags() option during estimation, α is constant (the nonconstant option removes the constant term α from regression during estimation), δt is the time trend (the trend option includes the time trend δt which by default is not included). Its null hypothesis was that β=0 .

The DG-GLS test is performed on GLS detrended data with H0=yt is a random walk possible with drift against alternative hypothesis that Ha=yt is stationary about a linear time trend. Under this alternative hypothesis, the DF-GLS test was performed by first estimating the intercept and trend via GLS and this this test has significantly been proved to have greater power than the previous versions of the augmented Dickey–Fuller test (Stock and Watson, 2011). The null hypothesis of non-stationary is rejected if the test statistic is greater than the MacKinnon’s critical values. Therefore, the decision is taken, and null hypothesis is rejected if the test statistic in absolute terms is greater than the critical value at different levels of significance as 5%.

Model Specification

The paper used the Vector Error Correction model for estimation of the relationship after confirmation of the existence of long run relationship between the study variables. Vector Error Correction Modeling (VECM) is one of the modeling techniques used in multivariate time series. Error correction terms are incorporated into VAR models as part of the definition of VECM models. If the system’s variables have a long-term connection, or if they are co-integrated, the VECM methodology is employed.

The general VECM for k variables with ρ lags was represented as follows.

Δyt=α1 β1‘ yt-1+α2 β2‘ yt-2+⋯+αρ βρ‘ yt-ρ+εt……………………………………………….2

Where Δyt represents the first differences of the k variables, αi are coefficient vectors corresponding to the lagged differences, βi‘ are cointegrating vectors representing the long-term relationships among the variables and εt is the error term, which is assumed to be white noise.

RESULTS AND DISCUSSIONS

According to Table 1, the cointegrating equation coefficient of 0.1713 was significant at a 5 percent level. This implies the existence of a long-run relationship. The deviations from equilibrium or partial adjustments of the debt service ratio and exchange rate can be corrected with this coefficient. The inverse of 0.1713, that is 1/0.1712=5.84 approximates 6 years for these partial adjustments to come back to equilibrium. Chi square is 19.094 and its P value is significant (0.001>0.005). This allowed the researcher to use the results for interpretation. The debt-service ratio exhibited a negative and statistically significant coefficient (-0.35102, PV=0.000). Exchange rate was also found to have a negative and significant effect on debt sustainability in Kenya (-0.0054, PV=0.000).

Table 1: Vector Error Correction Results

| Equation | Parms | Chi2 | P>Chi2 | |||

| _cel | 2 | 19.094 | 0.001 | |||

| Variables | Coefficient | Std. Err | Z | p>|z| | 95% confidence interval | |

| Cointegrating equation | .1713265 | .0466888 | 3.67 | 0.000 | .079818 | .2628349 |

| Debt sustainability | ||||||

| Debt-service-ratio | -0.35102 | 0.0083 | -4.25 | 0.000 | -.05129 | -.01890 |

| Exchange rate | -0.0054 | 0.0016 | -3.23 | 0.000 | -.00863 | -.00211 |

| Constant | 0.5853 | – | – | – | – | |

Source: Data analysis results, 2023

Misspecification of the model series analysis may lead to biased results and therefore testing for model is essential hence it is important to test for the reliability of the generated coefficients in the model. This is done by checking the Eigen stability condition of the VECM model. Figure 1 indicates the roots of the companion matrix are inside the unit circle. Indicating stability of the generated VECM coefficients.

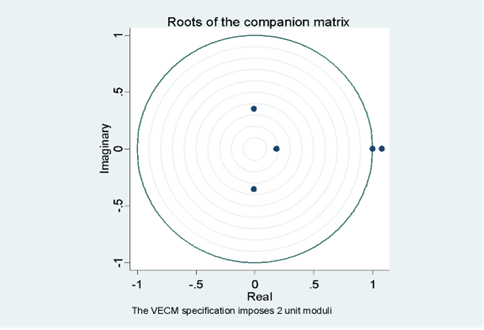

Figure 1: Eigen stability condition of the VECM model

Source: Data analysis results, 2023

The study established that debt serving ratio negatively and significantly influenced debt sustainability and implies Kenya faces a debt overhang problem. Thus, in the long run increasing the public debt service slows the sustainability of public debt. The results of the paper agree with the findings of Handra & Kurniawan (2020) who concluded that debt overhang has adverse effect on Indonesia’s public debt sustainability. These findings support the notion that fiscal irresponsibility and poor governance led to the debt overhang and that history will repeat itself in the absence of real systemic reforms. However, the results by Uma, Eboh & Obidike (2013) disagree with the findings of the study. Their study findings revealed that a rise in debt service ratio in an economy will have an effect of reducing the debt accumulations and arrears and therefore enhancing debt sustainability of a country.

The study findings also established that exchange rate had a negative effect on debt sustainability. Results are similar to the findings of Mathieu, (2022). The negative effect of exchange rate on debt sustainability in Kenya means that an increase of exchange rate volatility makes debt unsustainable. The explanation is straightforward: Kenya has a huge foreign debt and therefore its debt load in terms of domestic currency rises because of the nation’s currency depreciation. The financial account of the balance of payments will be pushed to lose capital due to the rise in debt burden, which will ultimately put additional downward pressure on the exchange rate. Thus, a vicious cycle develops when a weak currency causes a shift in exchange rate assumptions, which then raises the debt load and makes the currency even weaker. In such a scenario, maintaining the real exchange rate stability appears to be necessary for debt viability as well as to prevent a potential currency crisis brought on by the unsustainable nature of foreign debt.

CONCLUSION AND RECOMMENDATIONS

The analysis reveals a significant negative correlation between the debt-service ratio, exchange rate and public debt sustainability. According to the study findings, debt-service ratio has a statistically significant negative effect on debt sustainability. This suggests that an increase in the debt-service ratio is associated with a decrease in public debt sustainability. To enhance debt sustainability, it is crucial for the government to monitor and manage the debt-service ratio. Reducing this ratio can help maintain a sustainable debt level, which may involve negotiating favorable borrowing terms or improving debt repayment strategies. Further, the study findings also suggest that exchange rate changes have a statistically significant negative impact on public debt sustainability. This indicates that a depreciation in the exchange rate negatively affects the level of public debt sustainability. Exchange rate stability is vital for public debt sustainability. Policymakers therefore may consider implementing measures to manage exchange rate fluctuations, such as foreign exchange reserves or hedging strategies, to reduce the negative impact on public debt sustainability. Lastly, promoting economic diversification and aligning debt management with sustainable development objectives may further contribute to long-term resilience and the capacity to meet public debt obligations while fostering overall economic growth.

REFERENCES

- Abbas, S. M., & Christensen, J. E. (2007). International Monetary Fund. WP/07/127.

- Aleme, T. (2019). An econometric analysis of determinants of debt sustainability in Ethiopia. Financial Studies, 23(1 (83)), 39-55

- Alotaibi, K. (2016). How the exchange rate influences a country’s imports and exports. International Journal of Scientific & Engineering Research, 7(5), 131-138.

- Basu, M., Basu, R., & Nag, R. N. (2022). A Dependent Economy Model of Employment, Real Exchange Rate and Debt Dynamics: Towards an Understanding of Pandemic Crisis. Foreign Trade Review, 57(1), 85-113.

- Biase, P., Dougherty, S., & Lorenzoni, L. (2022). Ageing and the long-run fiscal sustainability of health care across levels of government.

- Bleikh, H. Y., & Young, W. L. (2016). Time series analysis and adjustment: Measuring, modelling, and forecasting for business and economics. CRC Press.

- Cahyadin, M., & Ratwianingsih, L. (2020). External debt, exchange rate, and unemployment in selected ASEAN countries. Jurnal Ekonomi & Studi Pembangunan, 21(1), 16-36.

- Central Bank of Kenya. (2023).Economic Indicators. https://www.centralbank.go.ke/publications-and-reports/financial-market-reports/economic-indicators/

- Chugunov, I., & Markuts, Y. (2019). Budgetary policy of the emerging countries in conditions of institutional transformations. Problems and Perspectives in Management, 17(4), 252.

- Clements, Benedict and Bhattacharya, Rina, and Nguyen, Toan Quoc, External Debt, Public Investment, and Growth in Low-Income Countries (December 2003). IMF Working Paper No. 03/249, Available at SSRN: https://ssrn.com/abstract=880959

- Dabrowski, M. (2016). Currency crises in post-Soviet economies—a never ending story? Russian Journal of Economics, 2(3), 302-326.

- Dickey, D. A., & Fuller, W. A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American statistical association, 74(366a), 427-431.

- Drehmann, M., & Juselius, M. (2012). Do debt service costs affect macroeconomic and financial stability? BIS Quarterly Review September.

- Drehmann, M., Juselius, M., & Korinek, A. (2023). Long-term debt propagation and real reversals. Bank of Finland Research Discussion Paper, (5).

- Elliott, G., Rothenberg, T. J., & Stock, J. H. (1992). Efficient tests for an autoregressive unit root.

- Fosu, A. K. (1999). The external debt burden and economic growth in the 1980s: evidence from sub-Saharan Africa. Canadian Journal of Development Studies/Revue canadienne d’études du développement, 20(2), 307-318.

- Government of Kenya. (2019). Economic Survey 2019. http://www.knbs.or.ke/survey/economic/economic-surveys/

- Greene, J. and Villanueva, D. Private Investment in Developing Countries: An Empirical Analysis. IMF Staff Papers, 1991, 33-58.

- Haggard, S., & Kaufman, R. R. (2018). The politics of economic adjustment: international constraints, distributive conflicts, and the state: Princeton University Press.

- Hamilton, J. D. (1994). State-space models. Handbook of Econometrics, 4, 3039-3080.

- Handra, H., & Kurniawan, B. (2020). Long-run Relationship Between Government Debt and Growth: The Case of Indonesia. International Journal of Economics and Financial Issues, 10(1), 96.

- IMF. (2004). Kenya: Debt sustainability analysis (IMF Country Report No. 03/400).

- International Monetary Fund. (2010). Public Debt Sustainability: The IMF’s Approach and Record. https://www.imf.org/en/Publications/Policy-Papers/Issues/2016/12/31/Public-Debt-Sustainability-The-IMFs-Approach-and-Record-PP4475

- International Monetary Fund. (2021). Kenya: 2020 Article IV Consultation-Press Release; Staff Report; Staff Supplement; and Statement by the Executive Director for Kenya (No. 21/257).

- International Monetary Fund. (2022). World Economic Outlook Database. https://www.imf.org/en/Publications/WEO/weo-database/2022/October/WEOreport

- Karadam, D. Y., & Özmen, E. (2021). Real Exchange Rates and Growth: Contractionary Depreciations or Appreciations? Ege Academic Review, 21(2), 111-123.

- Kenya Institute for Public Policy Research and Analysis (2023), Kenya Economic Report 2023. Nairobi: KIPPRA.

- Khan, A. J., Azim, P., & Syed, S. H. (2014). The impact of exchange rate volatility on trade: a panel study on Pakistan’s trading partners. The Lahore journal of economics, 19(1), 31.

- Kose, M. A., Ohnsorge, F., & Sugawara, N. (2022). A mountain of debt: Navigating the legacy of the pandemic. Journal of Globalization and Development, 13(2), 233-268.

- Mathieu, A. (2022). International Political Economy and Exchange Rate Regime: A Question of Sustainability. Review of Political Economy, 1-12.

- Mawejje, J., & Odhiambo, N. M. (2020a). The determinants of fiscal deficits: a survey of literature. International Review of Economics, 67, 403-417.

- Mawejje, J., & Odhiambo, N. M. (2020b). The Dynamics of Fiscal Deficits in Kenya: A Review of Reforms, Trends, and Determinants. African Journal of Business & Economic Research, 15(2).

- Mohsin, M., Ullah, H., Iqbal, N., Iqbal, W., & Taghizadeh-Hesary, F. (2021). How external debt led to economic growth in South Asia: A policy perspective analysis from quantile regression. Economic Analysis and Policy, 72, 423-437.

- Naveed, S., & Islam, T. U. (2022). An empirical investigation of determinants & sustainability of public debt in Pakistan. Plos one, 17(9), e0275266.

- Odera, Q. A. (2015). An analysis on the effect of external public debt on exchange rate volatility in Kenya. University of Nairobi.

- Piersanti, G. (2000). Current account dynamics and expected future budget deficits: some international evidence. Journal of international money and Finance, 19(2), 255-271.

- Piscetek, M. (2019). Public debt dynamics in New Zealand: New Zealand Treasury Working Paper.

- Porzecanski, A. C. (2018). Debunking the Relevance of the Debt-to-GDP Ratio. World Economics, March.

- Remeikienė, R., & Gaspareniene, L. (2023). Effects of Economic and Financial Crime on the Government Budget and the Quality of Public Services. In Economic and Financial Crime, Sustainability and Good Governance (pp. 173-204). Cham: Springer International Publishing.

- Renjith, P., & Shanmugam, K. (2018). DEBT SUSTAINABILITY: EMPIRICAL EVIDENCE FROM INDI S AN STATES. Public Finance & Management, 18(2).

- Renjith, P., & Shanmugam, K. (2020). Dynamics of public debt sustainability in major Indian states. Journal of the Asia Pacific Economy, 25(3), 501-518.

- Ryan, T., & Maana, I. (2014). An assessment of Kenya’s public debt dynamics and sustainability. Central Bank of Kenya, Nairobi.

- Salkind, N. J. (2010). Encyclopedia of research design (Vol. 1): sage.

- Soydan, A., & Bedir, S. (2015). External debt and economic growth: New evidence for an old debate. Journal of Business Economics and Finance, 4(3).

- Stock, J. H., & Watson, M. W. (2011). Dynamic factor models.

- Tarek, B. A., & Ahmed, Z. (2017). Governance and public debt accumulation: Quantitative analysis in MENA countries. Economic Analysis and Policy, 56, 1-13.

- Teles, V. K., & Mussolini, C. C. (2014). Public debt and the limits of fiscal policy to increase economic growth. European Economic Review, 66, 1-15.

- Uma, K. E., Eboh, F. E., & Obidike, P. C. (2013). Debt and debt service: Implications on Nigerian economic development. Asian journal of social sciences & humanities, 2(2), 275-284.

- World Bank and IMF (2018) Debt vulnerabilities in emerging and low-income economies. Report Prepared for the Development Committee meeting October 13, 2018, Washington DC.

- World Bank. (2022). Kenya Economic Update: COVID-19 Shocks Push Kenya’s First Recession in Decades. World Bank.