The Effect of Taxpayer Awareness on Tax Compliance in Rwanda (Case Study: Kigali Sector 2022)

- Eliezer

- 618-638

- May 2, 2024

- Accounting & Finance

The Effect of Taxpayer Awareness on Tax Compliance in Rwanda (Case Study: Kigali Sector 2022)

Eliezer NIYORUGIRA

Faculty of Economics Social Sciences and Management Department of Enterprise Management Masters of Sciences in Taxation

DOI: https://dx.doi.org/10.47772/IJRISS.2024.804047

Received: 07 March 2024; Revised: 25 March 2024; Accepted: 30 March 2024; Published: 02 May 2024

ABSTRACT

The study titled “The Effect of Taxpayer Education on Tax Compliance in Rwanda (Case Study: Kigali Sector 2022)” aims to investigate the influence of taxpayer education, media impact, and tax system fairness on tax compliance. The specific objectives include ascertaining the effect of tax education on tax-related compliance, examining the impact of the media on tax compliance, and assessing the influence of tax system fairness on tax compliance using SPSS Version 22. The findings of the study reveal important insights. The coefficient analysis indicates that a one-unit change in variable (Tax education), representing taxpayer education, leads to a significant increase in the log-odds of tax compliance by 0.694. Similarly, variable (media), denoting media impact, shows a 0.313 rise in the log-odds of tax compliance for a one-unit change, and this effect remains statistically significant. Variable (4), representing tax system fairness, demonstrates a 0.473 increase in the log-odds of tax compliance for every one-unit change, and this relationship is statistically significant. Furthermore, variable (8), related to tax information from other taxpayers, exhibits a 0.246 increase in the log-odds of tax compliance for a one-unit change, proving statistically significant. Variable (9), representing information from the radio, although not statistically significant, still indicates an important impact with a p-value of 0. 044.In summary, the study provides empirical evidence supporting the positive impact of taxpayer education, media influence, and tax system fairness on tax compliance in the context of Kigali Sector, Rwanda. These findings contribute to the existing literature on tax compliance behavior and offer valuable insights for policymakers and tax authorities.

GENERAL INTRODUCTION

This problem statement, the research’s aims, research questions, significance, restrictions, and boundaries are all included in this chapter.

Background of the study

Developing countries give a high priority to economic development; the source of funding may be of external or internal forms. The external funding is in form of loans and it is temporary obtained while the inside capitals are from local sources of national revenue. The internal funds decrease the need from outside capitals and provides capacity to the state to finance their expenditure using the income collected from both levy and non-levy revenues. The needs to maximize the tax revenue does not only rely to the tax administration but also take an active role of the taxpayer himself (Hagemann,2016).

Globally, tax education strategies are diverse, reflecting the unique economic, cultural, and administrative contexts of each country. Developed countries often integrate tax education into the school curriculum, aiming to instill tax awareness from a young age. For example, the United States and Australia have programs that introduce students to the basics of taxation and the importance of compliance. Developing countries, on the other hand, may focus more on public campaigns, leveraging media and technology to reach a broader audience. These efforts are supported by tax authorities, NGOs, and international organizations like the OECD, which promote tax education as a means to enhance voluntary compliance, reduce tax evasion, and support the overall development of a tax-paying culture. Despite these efforts, challenges remain, including ensuring the accessibility and relevance of tax education to all segments of society (Esther,2021).

Tax education policies, recognized globally as instrumental tools in enhancing compliance, have been implemented in Rwanda to educate taxpayers about their responsibilities and the broader significance of tax contributions. In the Kigali Sector, where diverse economic activities converge, the impact of these policies on tax compliance requires a nuanced exploration.

While the implementation of tax education policies in Rwanda is a positive step, understanding their specific impact within the unique dynamics of the Kigali Sector is imperative. Factors such as the sector’s economic diversity, demographic composition, and cultural intricacies contribute to the complexity of tax compliance behaviors. As such, there is a need for an in-depth case study to unravel the contextual nuances and assess the effectiveness of existing tax education initiatives.

In Africa, the achievement of the tax revenue objective depends in large part on paying tax on time and knowledge. The quantity of money collected increases with the rate of tax awareness and payment. money obtained. Maintaining accurate records of business transactions, reporting these operations in line with regulations, and adhering to all tax rules are all part of complying with tax laws. Maintaining correct records of commercial interactions, disclosing these operations in line with regulations, and adhering to all tax rules constitute tax-related compliance. Engagement and understanding of taxpayer to pay tax obligation heavily impacted tax compliance (Kelley & Michela, 1980).

In the East Africa, according to Rahayu et al. (2017), awareness of taxpayers and knowledge of tax laws both help ensure tax payers abide with the law. The approaches for tax collection and law enforcement, according to Mehari (2017), have a favorable impact on taxpayers’ voluntary tax observance behavior. Tax law knowledge with a crucial role in influencing taxpayer compliance behavior, together with tax education (Carroll and Goodman, 2011). Taxpayer awareness is an action or behavior that is accompanied with self-confidence and a readiness to uphold one’s legal obligations.

Taxpayer awareness, according to Munari (2005), is demonstrated when people are aware of their rights and obligations, are aware of their rights and obligations, are willing to keep track of, remit, and report their taxes, and accurately calculate, remit, and report their tax liabilities. Additionally, it shows that taxpayers value timely payment of their debts and the filing of taxes, which demonstrates formal conformity. Taxpayer awareness is evaluated based on their knowledge of tax procedures, awareness of their rights and obligations, and competence in tax computations, payment, and reporting. knowledge current tax laws in greater detail help one have a deeper knowledge of taxpayers.

Kirchler et al. (2008) and Richardson (2006) both emphasize the importance of tax knowledge in raising the level of tax compliance. So that everyone is ready to be informed taxpayers, it is crucial to offer people with tax education. According to Park & Hyun (2003), one of the best methods for getting taxpayers to comply more is tax education. On the other hand, individuals more inclined to cooperate if they thoroughly understand the principles of taxes (Marziana et al., 2010).

According to a study of Batrancea et al. (2013), Small company owners are not as inclined to pay their taxes on time requirements because they lack knowledge and comprehension of taxation. According to Ali et al. (2014), compliance with tax duties is influenced by tax knowledge and comprehension. Globally, both developing and developed nations have had difficulty enforcing taxation policy (Charlet and Owens, 2010). Due to the numerous barriers that prevent voluntary tax compliance, developing nations continue to have low levels of tax compliance.

There is a favourable, significant association between tax compliance and knowledge, according to past studies. For instance, research by Palil (2010) revealed that tax knowledge had a significant impact on tax compliance in Malaysia despite the fact that respondents’ degrees of tax knowledge varied substantially. Tax compliance is impacted by tax education., according to research done in Africa by Berhane (2011). Pratiwi and Siregar (2012) is only one of several studies conducted in Indonesia that look at how better tax understanding might boost tax payer compliance. Tax knowledge may be picked up through independent study, formal education, and unofficial learning. The government also makes several steps to publicize tax laws and regulations so that people may learn from them. Unfortunately, not everyone pays attention to rules and some of them believe that paying taxes is a hardship that should be avoided. The topic of tax resistance is supported by current tax controversies.

According to experimental results, more tax information may enhance taxpayers’ perceptions of the tax law and tax-related media campaigns may have an impact on voluntary tax compliance in Kasper et al. (2015)’study. Furthermore, Alm et al. (2010) give proof from laboratory studies that agency information can have a large and advantageous impact on people’s propensity to file a tax return and accurately report their income taxes. The FBR has launched widespread non-media information efforts since 2012. These programmes include top 100 taxpayer honour and award campaigns as well as public disclosure programmes that focus on tax remittance. The public disclosure effort raised tax payments, but Slemrod et al. (2018) found that the social recognition campaign was much more effective in doing so.

According to The OECD (2015), as the study makes clear about tax compliance, the initiative is particularly relevant in developing nations, those that are most affected by revenue loss. In order to ensure that their demands are satisfied, it seeks to involve them in the global tax agenda. The topic was also discussed throughout the Davos Annual Conference of the World Economic Forum this year. The topic of the discussion was taxes without borders. A fair number of multinational corporations considered the necessary steps, particularly in the aftermath of the Panama Papers leak, which revealed the widespread use of tax havens. The significance of the losses as a percentage of GDP is emphasized in the study: In comparison to other regions, Greater levels of loss intensity are present in low- and lower middle-income nations, sub-Saharan Africa, Latin America and the Caribbean, and South Asia.

The whole population of Africa was employed in the study, and a sample was chosen using a multi-stage technique. The analysis of the data revealed a strong negative association Tax rates and tax compliance were negatively correlated, demonstrating the negative impact of tax rates on tax compliance. Therefore, it is suggested that nations with above-average tax rates and noncompliance issues lower their tax rates to the average African tax rate of 29.1985%. In order to strengthen the dependability of results, it is also advised that future research on the issue think about increasing the sample size and observation years as data become available (Esther, 2021).

In Rwanda, the promotion of tax compliance can be greatly aided by tax reduction initiatives. The government may encourage voluntary compliance and deter tax evasion by taking actions that lessen the tax burden on people and corporations. Here are some tax-reduction ideas that might improve Rwanda’s tax compliance: Exemptions and deductions from taxes: Implement targeted exemptions and deductions from taxes to lessen the tax burden on particular industries or activities. For instance, offering tax breaks for investments in particular sectors or geographical areas might encourage companies to pay their taxes while fostering economic development. Simplifying Tax Procedures: Simplify tax procedures to make it simpler for taxpayers to comply with the law (Dusabe,2012). To lessen administrative hassles, automate procedures, streamline tax filing and payment systems, and cut back on paperwork.

To make tax rates more appealing and competitive for both people and corporations, consider lowering them. Lower rates of taxation may deter tax evasion and increase the likelihood that people pay their proportionate tax burden. Spend money on initiatives that educate taxpayers on their rights, obligations, and benefits. To assist tax payers in navigating the tax system and understanding their obligations, offer easily available information and resources.

Providing individualized guidance and help can boost compliance even further. and made stronger Measures to Enforce the Law and Prevent Evasion While tax reduction is the main objective, it is equally crucial to step up enforcement operations to successfully combat tax evasion. Improve data sharing and information interchange across government agencies, implement strong auditing procedures, and use cutting-edge technological tools for monitoring and identifying non-compliance.

Statement of the problem

In Rwanda, despite the government’s efforts to streamline tax processes and create a conducive business environment, issues related to tax compliance persist. One significant challenge revolves around a potential lack of taxpayer education, where businesses and individuals may not possess adequate knowledge about their tax obligations and the benefits of compliance. This gap in understanding can lead to inadvertent non-compliance, as taxpayers may not be fully aware of the legal requirements or the repercussions of non-payment. Moreover, the complexity of tax regulations and procedures may contribute to confusion among taxpayers, hindering their ability to navigate the system effectively. The problem statement underscores the critical need to assess the impact of taxpayer education initiatives on enhancing tax compliance in Rwanda (Dusabe,2012).

The problem in the Kigali Sector is the low level of tax compliance among taxpayers, indicating a need for effective tax education policies. Despite the presence of tax regulations and enforcement mechanisms, a significant number of individuals and businesses fail to meet their tax obligations. This problem necessitates a comprehensive examination of tax education measures’ effects on Kigali sector tax compliance.

Furthermore, the effectiveness of tax education programs in Rwanda remains uncertain, and there is a dearth of empirical evidence to ascertain their influence on taxpayers’ behavior. The lack of comprehensive research on this subject poses a challenge for policymakers seeking to refine strategies for improving tax compliance. It is imperative to understand the extent to which taxpayer education initiatives have been successful in increasing awareness, promoting voluntary compliance, and ultimately contributing to a more robust and transparent tax system in Rwanda. This research aims to address these gaps in knowledge and provide insights that can inform policy decisions and enhance the effectiveness of taxpayer education programs in the Rwandan context.

Performing a thorough investigation on how tax education initiatives affect tax compliance in Kigali Sector provide insights into the specific challenges and opportunities in improving compliance levels. The findings of such a study can guide the development of targeted tax education initiatives, strategies, and interventions that promote a culture of tax compliance, support economic growth, and contribute to the overall development of the Kigali Sector.

The theoretical research problem at the heart of investigating the effect of taxpayer awareness on tax compliance in Rwanda centers on understanding the complex interplay between taxpayers’ knowledge, their attitudes towards taxation, and their consequent compliance behaviors. Despite the Rwandan government’s efforts to enhance tax education and awareness as a means to boost compliance rates, there remains a significant gap in understanding the specific mechanisms through which awareness translates into compliance. Theoretical frameworks suggest that increased awareness should logically lead to higher compliance, as taxpayers better understand tax laws, their civic obligations, and the repercussions of non-compliance. However, the reality is often more nuanced, with factors such as perceived fairness of the tax system, trust in government, and the effectiveness of enforcement playing crucial roles. The research problem, therefore, involves dissecting these layers to ascertain how taxpayer awareness directly impacts compliance and what additional mediating factors might influence this relationship in the Rwandan context.

Objectives of the study

1.3.1. General Objective

To investigate and analyze the effect of media on tax awareness in Kigali Sector, in Nyarugenge District of Rwanda.

1.3.2 Specific Objectives

- i) To ascertain whether tax education affects tax related compliance

- ii) To investigate the impact of the media on tax related compliance;

iii) To assess the impact of the tax system’s fairness on tax compliance;

1.4 Research hypotheses

- a) There is Tax compliance among taxpayers and tax education have a substantial link.

- b) There is Media awareness and tax compliance among taxpayers have a substantial link.

- c) There is Tax compliance among taxpayers and tax fairness have a considerable link.

LITERATURE REVIEW

This chapter deals with review of literature associated the variables of the research. It gives the over view of researches that had been done on tax awareness and help the researcher to analyze and expand the knowledge on the topic. It broadly aims at reviewing the existing literature for conceptual understanding. It expands on the definitions of key terms.

2.1. Definition of key concepts

2.1.1 Tax Education

The oversight of taxes is a crucial public sector duty that affects people’s daily lives and those of their enterprises. Because most individuals avoid paying taxes because they are unsure of what they should be paying and why, there is less compliance when the tax system is not understood. Most SAS (self-assessment system) countries, such as the United States (even via online education22), Canada, and the United Kingdom, have established taxpayer-specific tax educational initiatives (Eriksen, 1996). One of the major advances in tax administration aimed at relaxing the execution of tax rules and regulations is the provision of taxpayer education and services.

The aim is to enhance voluntary compliance by educating taxpayers about their rights and responsibilities. The URA completes the process by setting up taxpayer service desks, which are responsible with handling questions and grievances from taxpayers. The desk makes sure that taxpayers have access to spoken explanations, tax leaflets, tax booklets, and telephone-based tax information. They provide tax information to the URA’s tax heads that taxpayers are required to know and act upon regarding their tax issues. They inform customers of the various tax forms and returns that must be filed, the deadlines for filing them, and the different tax payment due dates. (Annah, 2006).

Tax administrations might send messages that emphasize the need of compliance in an effort to educate taxpayers and foster the development of positive personal norms. Young individuals (those of working age or younger) who interact with tax administrations may have an influence on personal norms, which aids in long-term tax compliance (Walsh, 2012). To promote tax literacy and voluntary tax compliance, high-quality taxpayer services are provided.

Higher educated taxpayers are thought to be within a stronger judging position the degree of conformity since they have a better understanding of tax rules and fiscal connections. Taxpayers with greater education tend to be kinder to others than their less educated counterparts. They now comprehend more clearly how the state government employs tax funds for everyone’s advantage (Olowookere, 2013). Tax education refers to any informal or formal training offered by the tax authorities or other independent groups to assist taxpayers in correctly completing tax returns and raising awareness of their responsibilities surrounding the tax system (Eriksen, 1996).

This is done by providing clear, accurate, and timely tax information to taxpayers and their representatives, streamlining Taxpayers’ rights are upheld by providing tax forms and tax legislation in their native tongues and ensuring that all taxpayers are treated with respect, promptly responding to every taxpayer’s inquiry, complaint, or request, outlining the factors used to determine each tax assessment, and providing the necessary technical assistance.

2.1.2 Tax Compliance

Standard tax compliance models presuppose that taxpayers are completely aware of all the details pertaining to the tax reporting procedure. The level of information and knowledge may play a significant role in how taxpayers act. According to taxation literature, the fiscal policies of the government, the systems in place for enforcing taxes, the attitudes of taxpayers toward taxes, the advantages and fairness of the tax system that government receives in return all influence whether or not taxpayers comply with the law (Olowookere, 2013).

When considering the high level of tax compliance and low amount of deterrence can be explained in large part by tax morale, or the innate desire to pay taxes. A rising number of researchers contend that societal norms or some type of tax morale must be responsible for the high rate of tax compliance. Many researchers have suggested that tax morale may help to explain the high incidence of tax compliance. Tax morale examines people’s views rather than their actions, in contrast to tax evasion (Torgler, 1999)

The majority of taxpayers, according to several experts, are always truthful. Certain taxpaying individuals are “simply predisposed not to evade” (Long, 1991). According to the experimental findings When individuals have a voice, tax compliance is higher in how their taxes are spent than when they have no say at all. When people have the option to choose the public sector expenditure programme, they are more inclined to honour the tax payment obligation. On the other side, when subjects lack choice over how their tax contributions are used, tax compliance is lower. Therefore, how individuals are treated by the authorities has an impact on how they view these authorities and how eager they are to cooperate. (Tyler, 1989).

2.1.3 The Benefits from Taxes Compliance

The fundamental purpose of subnational government taxation is to generate revenue to cover allocated expenditures needs. If a tax base that cannot generate sufficient revenues at reasonable rates is allocated, the outcome is likely to be both inadequate public services and a hasty gap-filling method that includes the imposition of a variety of undesirable and distorting fees, levies, and informal charges (Bahl, 2010). A large proportion of small company taxpayers acknowledged that tax compliance actions enhanced record keeping and their understanding of their financial situation. But it seems that respondents were generally unwilling to embrace the notion that there may be advantages to paying taxes (Lignier, 2009).

Smaller tax policy frameworks have the benefit of better accommodating citizen choices than those that result from the creation of a unified tax code for a population with diverse interests. Additionally, there is frequent daily engagement between taxpayers and regional officials, including politicians and bureaucrats. This proximity between the local government, the tax administration, and the people may foster confidence, so boosting tax morale. Politicians and government officials are more knowledgeable about the preferences of the local populace. Additionally, there is a politico-institutional aspect: local elections provide elected officials an incentive to consider the wishes of their constituents and use local tax money in line with those interests. (Frey, 1999).

Local government revenues serve a variety of purposes, including increasing citizen involvement in public affairs, stabilizing the economy, encouraging or discouraging certain types of investment, regulating economic activity, redistributing wealth, and reducing reliance on aid while increasing autonomy. (Kagarama, 2013).

Theoretical Review

A theoretical review in the context of examining the effect of taxpayer awareness on tax compliance involves a comprehensive exploration of existing theories and conceptual frameworks that explain why and how taxpayer awareness impacts compliance behaviors. This review not only synthesizes the findings from previous studies but also identifies the theoretical underpinnings that inform these relationships.

It is a common idea that two things in life cannot be avoided: death and taxes. People, however, despise paying taxes and would do anything to reduce their tax burdens, as history has shown. To interpret tax regulations in a way that is advantageous to them is one such action. Taxpayers’ concerns that governments are not held accountable for the taxes they voluntarily collect have been cited as a major justification for not adhering to such restrictions. The low rates of tax compliance in developing nations have generally been attributed to poor levels of taxpayer education. Lack of knowledge and education among taxpayers, according to Azubike (2009), is a serious problem since it leaves them inadequately informed about the terms of the numerous tax laws.

Research on tax compliance challenges persist as long as there are taxes since they are as ancient as taxes themselves. Nearly all civilizations have had taxes. The phrase “There were the tax collectors” was carved on clay cones in Sumer, which is when taxes were first mentioned (Adams, 1993). “History shows that tax avoidance has been practiced ever since records have been kept. The fact that the taxpayer does not always see any benefits to parting with his hard-earned money accounts for a big portion of this mentality. However, the majority of people are aware that expenditure by the government is important to develop or maintain the country’s infrastructure, such as services and roads. However, citizens grumble about having to cover unnecessary government costs. There are many different ways that people define what is unnecessary. The majority of taxpayers feel that their taxes are squandered and that the government frequently fails to uphold its social commitments. The government’s poor reputation as a result of its inability to perform its obligations considerably deters taxpayers from doing so.

An approach for teaching individuals on the overall tax system and the reasons they must pay taxes is taxpayer education. Taxpayer education enables individuals to satisfy their financial responsibilities to the government. One of the main goals of taxpayer education is to encourage taxpayers’ voluntary compliance. When the responsibilities of enforcement and education are balanced to reach the intended outcome in tax compliance, taxpayer compliance is more likely to increase willingly (Misra, 2004). The process of carrying out a tax payer’s legal obligation to pay taxes is known as tax compliance., file tax returns, and produce the essential documentation and other materials as asked by the tax authority on time (Olowookere and Fasina, 2013).

2.2.1. Attribution Theory

Attribution Theory, by analyzing how individuals ascribe causes to behaviors and outcomes, offers a nuanced framework for understanding variables like tax education, media, and tax fairness in the context of tax compliance. Specifically, it posits that taxpayers’ compliance decisions are influenced by their perceptions and attributions: tax education shapes compliance through attributions of knowledge and capability, suggesting that better-informed taxpayers feel more equipped and responsible for complying. Media influences through the shaping of social norms and the source credibility effect, where taxpayers’ perceptions of tax compliance are molded by the information they consume, attributing their compliance or non-compliance to societal expectations and the trustworthiness of the information source (Kelley and Michela, 1980).

Attribution theory can assist in explaining how people perceive and evaluate tax-related behavior in the setting of tax awareness. For instance, people may attribute their tax compliance behavior to internal factors like their own moral beliefs or external factors like the complexity of tax laws or the equity of the tax system.

Furthermore, attribution theory can help people understand how others view their tax-related conduct. For example, if a neighbor or acquaintance is audited by the tax authorities, that person’s lack of tax awareness or willful tax evasion may be charged. Applying attribution theory to the study of tax compliance in the Kigali Sector enriches our understanding of the cognitive processes influencing taxpayers’ decisions. This framework provides a robust foundation for tailoring tax education policies, fostering compliance, and advancing Rwanda’s economic resilience through an informed and psychologically attuned approach to tax administration.

2.2.2. Planned Behavior theory

This psychological theory seeks to explain why people act in certain ways by connecting thoughts and behaviour. Icek Ajzen in 1975 came up with the concept to increase the predictive power of the theory of reasoned action. This theory holds that several factors that have purposeful beginnings and preset causes influence how people behave in social situations. To be able to engage in a specific behaviour, a person must have the desire to do so. Three elements that affect behavioral intention are attitude towards the behaviour, subjective norms, and perceived behavioral control. Additionally, behavioral attitudes, normative beliefs, and control beliefs all have an impact on these three factors. As a result, the morals and ethics of the taxpayer form the basis of this idea. The theory holds that a taxpayer may abide by the law even when there is little chance of being detected.

The concept of planned behavior is that all acts carried out with a person’s assistance are driven by a certain objective. Fischbein and Ajzen (1975) identified three elements that affect the development of an intention to act. These include: a. behavioral beliefs ideals about the normative expectations of others and the drive to uphold them; b. normative beliefs ideals about one’s own expectations of others and the drive to manage behavior. Beliefs are the notion that things could be living and engaging in be haveiours that benefit or harm them, as well as the perception of how effectively those things might be viewed to conduct electricity. Several earlier studies have used this idea to gauge the extent of tax compliance, among other things (Arum ,2012).

Attribution Theory and the Theory of Planned Behavior (TPB) both offer valuable insights into understanding human behavior, including tax compliance, yet each has its limitations when considered in isolation. Attribution Theory focuses on how individuals attribute causes to their behavior and the outcomes they experience, emphasizing the role of perception in behavior motivation. However, it may overlook the structured processes through which intentions are formed, failing to account for the planned aspect of behavior that TPB highlights. On the other hand, TPB outlines how attitudes, subjective norms, and perceived behavioral control shape individuals’ intentions and behaviors, offering a systematic approach to predicting behavior. Yet, TPB can underestimate the impact of past experiences and the dynamic nature of how individuals interpret and react to their actions and outcomes, an area where Attribution Theory provides deeper insights. Together, these theories can offer a more comprehensive framework by integrating the influence of perceptions, attributions, and planned behavioral components in understanding and predicting behaviors like tax compliance. (Kamil, 2015).

2.2.3. Social Learning Theory

According to the social learning concept, which was put forward by Bandura in 1977, a person can learn through comments and direct enjoyment. the methods of motoric duplication, interest, retention, and reinforcement. The attentiveness technique is a method through which someone does study through other people or a known model while paying close attention to the opposing character or model. Retention method is a way of thinking about how a model moves even while there are issues with the model. A motor replica technique translates a statement into movement. While the strengthening process, the technique with which people are given an effective or punishing stimulus for acting in accordance with the version (Bandura, 1977)

According to Jatmiko (2006), the social learning theory may be used to explain how taxpayers behave when fulfilling their tax obligations. People continue to pay their taxes on time if they feel (based on observation and enjoyment) that taxes collected by the government significantly contribute to the development in their area. One may also be willing to pay their tax burden if they have been paying attention to the taxation system, especially the services it offers. It appears to be crucial in regard to the process of strengthening, where individuals are provided a good or punishment’s stimulus for operating in accordance with the version, given how tax fines effect taxpayer behaviour.

By applying the Social Learning Theory to the study of tax compliance in the Kigali Sector, this research aims to unravel the complex interplay of social influences on taxpayers’ behavior. Through an in-depth exploration of observational learning, modeling, and reinforcement mechanisms, we seek to contribute valuable insights that can inform policy interventions and foster a culture of voluntary tax compliance in the region.

2.3 Empirical Literature

2.3.1. Effect of tax education on tax compliance

Gitaru’s (2017) research findings highlight the significance of stakeholder involvement, print media taxpayer education, and electronic taxpayer training in enhancing tax compliance among SMEs in Nairobi’s CBD. The correlation matrix revealed a strong positive correlation (0.810) between taxpayer training for accurate tax computation and stakeholder sensitization, underscoring the importance of comprehensive educational initiatives. Conversely, Trawule et al. (2022) observed that fear-inducing messages hinder tax compliance efforts, emphasizing the need for communication strategies that foster a sense of ease and comfort in tax compliance processes.

Furthermore, Oladipo et al. (2022) found that taxpayers’ perception of equity and their understanding of taxes significantly influence their willingness to pay taxes, indicating the importance of promoting tax education and awareness initiatives. Given these insights, this study aims to explore the direct impact of tax education on tax compliance in the Kigali Sector, Rwanda, with a focus on tailored educational interventions to enhance compliance rates within the local context.

RESEARCH METHODOLOGY

This section reviewed the various methodological approaches that were employed during the field visited. It highlighted the methods and techniques that were used as per the researcher under coverage. It clarifies the population with its sample size, data collection and analyzes techniques to be used.

3.1 Research design

In order to identify alternative methods to address issues and reduce variations, a research’s plan, structure, and strategy are referred to as its “research design.” (Kothari, 2004). Both qualitative and quantitative research were used to examine the effect of media on tax awareness. Kigali Sector was selected as one of local government Authority in charge of collecting rental tax; property tax and trading license and based on its location and subdivision it represents both urban and rural areas on tax issues locally collected.

3.2 Target Population

In Kigali city, there are 120960 taxpayers. However, in my case of study which is Kigali Sector only 129 were the target population (taxpayers) under the present research located in Kigali Sector and Kigali sector tax officials in charge of collecting property taxes, rental taxes and trade licence fees. The researcher approached them and inquired about them using both open-ended and closed-ended inquiries.

3.3 Sampling procedure

The strategy or act of choosing an appropriate sample and time frame is known as the sampling procedure. With the random sampling approach, every member of the population have an equal chance of being chosen by the researcher.

3.4 Sample Size

Determining an appropriate sample size is one of the key aspects that influence both accuracy and precision of the results. The sample size was used for the study.

n=![]()

Where Zc is the value for chosen alpha level of 0.05 is to be equal to 1.96, e is the acceptable margin of error and p is expected proportion. Macfarlane et al. (2006) asserted where there is doubt about the value of p, it is best to error towards 50 percent as it would lead to a greater sample size.

For SRSWOR it can be shown that

![]()

This implies that

3.5 Research instrument and data Collection procedures

To provide useful results for this study, both primary and secondary sources of data was used.

3.5.1 Primary Data Sources

i. Questionnaire

The researcher used questionnaires to collect the required data from Kigali sector taxpayers where open-ended questions were used to allow respondents answering by using their own words and closed-ended questions which to allow them to choose among multiple answers predetermined by the researcher.

ii. Interview

An interview guide also was conducted to Kigali Sector tax officials to obtain relevant data to the way tax information are provided to taxpayers and how they get support from tax officials in case of complaints to influence taxes payment compliance.

3.6.2 Secondary data sources

The researcher reviewed the existing literature of the previous researchers, scholars and academicians on the concerned issue for proper understanding of the problem and other theoretical issues concerning to this research.

3.6 Reliability and Validity

Under this study, questionnaire was used addressed to Kigali sector taxpayers and to make sure the precision and consistency of the information, the researcher conducted a sample survey to ensure that questions to be asked are clearly established and understandable by the respondents to provide needed information to research questions and also considering time taken to answer questionnaire.

To achieve reliability in this study on the effect of taxpayer awareness on tax compliance in Rwanda, several steps were taken. Firstly, the research utilized well-established and validated measurement scales to assess taxpayer awareness and compliance. These scales have been rigorously tested in previous studies, ensuring that the constructs measured are reliable and valid. Additionally, the study employed a systematic sampling technique to select a representative sample of taxpayers in the Kigali Sector, enhancing the generalizability of the findings.

3.7 Data analysis Procedure

The task of data collection is not an end in itself, unless the data can be treated, analyzed and transformed into data in a format that can be useful to the operator. The analysis was done based on research finding from various taxpayers and tax officials in relation to the research objectives. For easy analysis and interpretation of findings the researcher used SPSS while coding responses provided by various respondents. This was accomplished by editing and tabulation, and a binary logistic regression model was used to determine how tax compliance is impacted by tax knowledge.

RESULTS AND DISCUSSIONS

4.0 Descriptive statistics of profile of respondents

Table 1: Reliability result

For this table above, the Cronbach’s alpha was 0.752, which means that 75.2% of the variance in the scores which accepted because the normal range for Cronbach’s alpha is from 0.7 and more.

Table 2: Gender of Respondents

Source: Primary data, 2023

From the table above, it indicates that in 99 respondents, there are 4 respondents were between 18-25 years old and 2 were men against 2 women, 45 respondents were between 26- 35 years old with 21 women and 24 men.40 respondents were between 36-45 years old with 20 women and 20 men. The result also shows that only 10 were between 46-64 years old with 2 women and 8 men.

4.1 Effect of tax education on tax compliance

Table 3: Model Summary

Source: Primary data, 2023

In this table above, the result showed a Cox and Snell R Square of 0.822 based on the R-square. Therefore, the researcher concluded that the model is good enough to be used since it is good at 82.2% hence 82.2% of independent variables are explaining the dependent variable.

Source: Primary data, 2023

Data is the foundation for Table’s statistics. I_1 had an average value of 0.1717 with a maximum and lowest value range of 1 and 1. With a standard deviation of 0.3790, it can be seen that the data cluster deviated from the mean. II_2 has a mean of 0.2020 with a sample size that ranges from 0 to 1. In the series, I_3 had a greater standard deviation of 0.4244. I_3 recorded a minimum and maximum value of 0 and 1, respectively, as well as a mean value of 0.2323.

Source: Primary data, 2023

The model equation presented in the study suggests that three independent variables – trainings offered to taxpayers (I_1), electronic taxpayer education (I_2), and taxpayer education on new laws (I_3) – significantly influence tax compliance. The coefficient for I_1 is 1.734, indicating that a one-unit change in I_1 leads to a 1.734 increase in the log-odds of tax compliance, holding other variables constant. Similarly, I_2 and I_3 have coefficients of 0.212 and 0.744 respectively, signifying their positive impact on tax compliance. These results are statistically significant, as evidenced by the low p-values of 0.000 for I_1, 0.012 for I_2, and 0.025 for I_3, all below the conventional threshold of 0.05.

These findings are consistent with previous research, such as Olowookere’s (2013) study in Lagos State, Nigeria, which found that tax education initiatives significantly improved voluntary compliance among taxpayers. By educating taxpayers on the socioeconomic implications of tax fraud and promoting transparent use of tax resources, similar to the efforts in Rwanda, tax education programs can effectively enhance compliance levels. Therefore, the results suggest that investing in taxpayer education and training programs, both through traditional means and electronic platforms, can play a vital role in promoting tax compliance and fostering a culture of tax responsibility among citizens.

4.2 Effect of media on tax compliance

Source: Primary data, 2023

Data is the foundation for Table’s statistics. I_1 had an average value of 0.1327 and a maximum and lowest value range of 1 and 0. With a standard deviation of 0.3594, it can be seen that the data cluster deviated from the mean. II_2’s sample size ranges from 0 to 1, with a mean of 0.1720. In the series, I_3 had a larger standard deviation of 0.4534. I_3 recorded a minimum and maximum value of 0 and 1, respectively, as well as a mean value of 0.2412. II_4’s sample size ranges from 0 to 1, with a mean of 0.1723. I_5 had a standard deviation between 0 and 1 of 0.4412 throughout the series, with an average of 0.2523.

Source: Primary data, 2023

In this table above, the results found a Cox and Snell RSquare of 0.835 based on the R-square. Therefore, the researcher concluded that the model is good enough to be used since it is good at 83.5% hence 83.5% of independent variables are explaining the dependent variable.

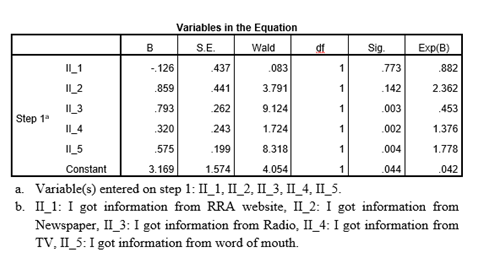

Source: Primary data, 2023

The model equation indicates that three independent variables – II_3, II_4, and II_5 – have significant effects on tax compliance. Specifically, II_3 has a coefficient of 0.793, suggesting that a one-unit change in II_3 results in a 0.793 increase in the log-odds of tax compliance, holding other variables constant. This effect is statistically significant, as indicated by the p-value of 0.03. Similarly, II_4 and II_5 have coefficients of 0.575 and 0.744 respectively, implying their positive impact on tax compliance. The p-value of II_4 is below 0.05, indicating statistical significance, while the p-value of II_5, although slightly higher at 0.044, still suggests a meaningful impact on tax compliance. These findings align with previous research, such as Fiar et al.’s (2020) study on media bias and tax compliance, which found a significant association between positive media coverage and increased compliance levels. Therefore, the media plays a crucial role in influencing taxpayer behavior and promoting tax compliance in the Kigali sector, Rwanda.

4.3 Impact of fairness of tax system on tax related compliance

Source: Primary data, 2023

Based on facts, Table’s numbers are accurate. III_1 had an average value of 0.281 and a max value of 1 and a min value of 1. Its std of 0.4563 shows that the data cluster deviated from the average. With a sample size of between 0 and 1, III_2 has a mean of 0.225. III_2 has the highest standard deviation in the series at 0.4733.

Source: Primary data, 2023

In this table above, the results revealed a Cox and Snell R Square of 0.80 based on the R-square. Therefore, the researcher concluded that the model is good enough to be used since it is good at 80% hence 80% of independent variables are explaining the dependent variable.

Source: Primary data, 2023

The model equation reveals that the independent variable III_1, representing tax fairness, has a coefficient of 0.038. This suggests that for every one-unit change in tax fairness (III_1), we can expect a 0.038 increase in the log-odds of tax compliance, with all other variables held constant. The statistical significance of this effect is confirmed by the p-value of 0.007, which is below the conventional threshold of 0.05. This indicates that tax fairness indeed positively influences tax compliance. This finding is consistent with research conducted by Alshadli (2015), who investigated the relationship between tax fairness and tax compliance in Libya. Alshadli’s study revealed a significant association between tax compliance and various aspects of tax fairness, further supporting the notion that fairness in taxation plays a crucial role in promoting compliance. Therefore, fostering perceptions of fairness in the tax system may contribute to enhanced compliance levels among taxpayers.

General Model

Source: Primary data, 2023

In this table above, the results found a Cox and Snell R Square of 0.853 based on the R-square. Therefore, the researcher concluded that the model is good enough to be used since it is good at 85.3% hence 85.3% of independent variables are explaining the dependent variable.

Source: Primary data, 2023

Log (p/1-p) =2.239 +0.694 (3) + 0.313 (4) +0.473 (5) +0.246(8) +665(9)

The regression analysis reveals significant relationships between tax compliance and several independent variables. Variable (3) demonstrates a coefficient of 0.694, indicating that a one-unit change in this variable leads to a 0.694 increase in the log-odds of tax compliance. The associated p-value of 0.013 confirms the statistical significance of this impact. Similarly, variable (4) shows a coefficient of 0.313, suggesting that a one-unit change results in a 0.313 rise in the log-odds of tax compliance, although its p-value is 0.022. Variable (5) exhibits a coefficient of 0.473 with a significant p-value of 0.014. Variable (8) is associated with a coefficient of 0.246, indicating a 0.246 increase in log-odds for every unit change, with a p-value of 0.023. Variable (9) has a coefficient of 0.665, suggesting a 0.665 rise in log-odds for a one-unit change, with a p-value of 0.044. Although the impact of radio information was not statistically significant, with a p-value above 0.05, it still holds importance due to its p-value of 0.044. Overall, tax education emerges as a significant factor influencing tax compliance, supported by the statistically significant relationships observed in the regression analysis. Thus, effective tax education initiatives can play a crucial role in promoting compliance with tax regulations.

CONCLUSION AND RECOMMANDATIONS

Conclusion

This study presents the findings, draws conclusions, offers guidance, and proposes lines of inquiry for additional investigation in this chapter. The major objective of this study was to ascertain the relationship between tax awareness and tax compliance among taxpayers in the Kigali Sector. The findings of this study may lead one to draw the conclusion that tax education can raise tax compliance in Rwanda. In conclusion, those who learn about taxes are more likely to obey the law and pay their taxes on time. Tax education may increase taxpayers’ understanding of tax duties and their awareness of related topics.

It is extremely difficult to address the issue of inadequate access to tax education in Rwanda, especially in rural regions. The government and other stakeholders may think about using a number of techniques to address this issue. These tactics can entail working with local authorities to interact with taxpayers in far-flung communities and making efficient use of a variety of media outlets. It’s critical to emphasize that improving tax compliance in Rwanda could not depend entirely on tax education. Other elements, such as the difficulty of code of tax, the efficiency of tax collection, and tax payers’ sense of justice, may also have an impact on compliance. As a result, improving tax compliance in Rwanda necessitates a diversified strategy.

Recommendations

The government wants payment. The modern government has several financial requirements. Given that there are several incentives for tax evasion, collecting this money is a difficult problem. To solve this issue, the government has attempted a number of different approaches. The report suggests the following regulations to deal with the problem: Positive incentives: Financial rewards are frequently given through lotteries. For instance, Taiwan has conducted a receipt-based tax lottery since the 1950s to improve compliance with sales tax (VAT).

In order to promote taxpayer education, the Ministry of Education should work to incorporate a public finance and taxes curriculum into each academic area. Because taxes are a major source of income for governments and are frequently used to pay for public costs, this project is crucial. Given that tax awareness can affect taxpayers’ attitudes towards paying their fair share of taxes, it is essential to implement a standardized tax education course that is open to all students and comparable to courses in civics and ethics.

Since knowledgeable taxpayers are better aware of their obligations and the potential consequences of breaching the law, more knowledge can promote tax compliance. The level of understanding has a big impact on how successfully tax compliance is managed internationally. Making sure that taxpayers have the knowledge, abilities, and assurance to properly carry out their tax duties is one method to promote voluntary compliance.

REFERENCES

- Abdul, F. (2019). Tax Compliance Behaviour and Tax System Fairness of Corporate Taxpayers in Kenya. European Journal of Business and Management, 11 (6), 33-42.

- Akinboade, & Grobler. (n.d.). An Analysis of Taxpayer Service needs of Private Sector Tax Practitioners from South Africa Revenue Service. Journal of Administrative Sciences and Policy Studies, 3 (1), 27-44.

- Aksnes, F. (2011). Tax compliance, Enforcement and Taxpayer Education” Being a paper presented at workshop organised by International Centre for Tax and Development.

- AL SEDDIG ALSHADLI, A. R. (2015). EXAMINING THE INFLUENCE OF TAX FAIRNESS ON TAX COMPLIANCE IN LIBYA (Doctoral dissertation, School of Business, Universiti Utara Malaysia).

- Ali, M., Fjeldstad, O. H., & Sjursen, I. H. (2014). To pay or not to pay? Citizens’ attitudes toward taxation in Kenya, Tanzania, Uganda, and South Africa. World development, 64, 828-842.

- Alm, J. (2012). Designing alternative strategies to reduce tax evasion. In Tax evasion and the shadow economy. Edward Elgar Publishing.

- Alma, B. (2011). Marketing Management and Service Marketing. Bandung. Bandung: Alfabeta Publisher.

- Ashish, B. (2004). Financial Accounting for Business Managers. New Delhi: Prentice Hall of India Pvt. Ltd.

- Authority, R. R. (2021). Annual activity report. Kigali: Telecommunication Authority.

- Azubike, J. U. (2009). Challenges of tax authorities, tax payers in the management of tax reform processes. Niger Account, 42 (2), 36-42.

- Bahl, R. W. (2010). Challenging the conventional wisdom on the property tax. Lincoln Institute of Land Policy.

- Bain, L. J., & Engelhardt, M. (2017). Statistical analysis of reliability and life-testing models: theory and methods. Routledge.

- Batrancea, L. M., Nichita, R. A., & Batrancea, I. (2013). Understanding the determinants of tax compliance behavior as a prerequisite for increasing public levies. The USV Annals of Economics and Public Administration, 12 (1 (15)), 201-210.

- Berhane, Z. (2011). The influence of tax education on tax compliance attitude. Addis Ababa, Ethiopia.

- Murphy, R. (2019). The European tax gap. A report for the Socialists and Democrats Group in the European Parliament. Global Policy.

- Beckert, J. (2008). Why is the estate tax so controversial? Society, 45 (6), 521-528.

- Bobek, D. D., Hageman, A. M., & Kelliher, C. F. (2013). Analyzing the role of social norms in tax compliance behavior. Journal of business ethics, 115 (3), 451-468.

- Bonett, D. G., & Wright, T. A. (2015). Cronbach’s alpha reliability: Interval estimation, hypothesis testing, and sample size planning. Journal of organizational behavior, 36 (1), 3-15.

- CHARLET, A., & OWENS, J. (2010). An International Perspective on VAT. Tax notes International, 59 (12): 943-954. Tax Analysts.

- Carroll, D. A., & Goodman, C. B. (2017). Assessing the influence of property tax delinquency and foreclosures on residential property sales. Urban Affairs Review, 53 (5), 898-923.

- Dusabe, P. (2012). The Contribution of Ubudehe Program to Poverty Reduction in Bugesera District, Rwanda (Doctoral dissertation, Kampala International University, College of Humanities and social sciences.).

- Kamil, N. I. (2015). The Effect of Taxpayer Awareness, Knowledge, Tax Penalties and Tax Authorities Services on the Tax Complience: (Survey on the Individual Taxpayer at Jabodetabek & Bandung). Research Journal of Finance and Accounting, 6 (2), 104-111.

- Easterly, W., Rebelo, S., & Mundial, B. (1992). Marginal income tax rates and economic growth in developing countries (No. 1050). Country Economics Department: World Bank.

- Eriksen & Fallan. (1996). Tax knowledge and attitudes towards taxation; A report on a quasi-experiment. Journal of economic psychology, 17 (3), 387-402.

- Esther, F. (2017, January 1). Tax evasion most prevalent financial crime in Rwanda. The New Times. https://www.newtimes.co.rw/article/188779/News/tax-evasion-most-prevalent-financial-crime-in-rwanda

- Fišar, M., Reggiani, T., Sabatini, F., & Špalek, J. (2020). Media bias and tax compliance: Experimental evidence.

- Frey, B. S. (2003). Deterrence and tax morale in the European Union. European Review, 11 (3), 385-406.

- (2008). How to Understand High Food Prices. Journal of gricultural Economics, 61 (3), 123-136.

- Gitaru, K. (2017). The Effect of taxpayer education on tax compliance in Kenya. (a case study of SME’s in Nairobi Central Business District).

- Gumo, M. S. (2013). The effect of tax incentives on foreign direct investments in kenya (Doctoral dissertation, University of Nairobi).

- Gurama, Z. U., & Mansor, M. (2015). Tax administration problems and prospect: A case of Gombe state. International Journal of Art and Commerce, 4 (4), 187-196.

- Hagemann, R. P., Brian, J. R., & Montador, R. B. (2017). OECD tax policy studies tax policy reform and economic growth. OECD Publishing.

- Haig, R. M. (2020). The concept of income—economic and legal aspects. Routledge, 140-167.

- Hannam, J. (2017). What everyone needs to know about tax: An introduction to the UK tax system. London: John Wiley & Sons.

- Ibrahim, M. I. M., & Mohamed, N. A. E. M. (2016). Towards sustainable management of solid waste in Egypt. Procedia Environmental Sciences, 34, 336-347.

- James, S., & Alley, C. (2002). Tax compliance, self-assessment and tax administration.

- Joshi, A., Prichard, W., & Heady, C. (2014). Taxing the informal economy: The current state of knowledge and agendas for future research. The Journal of Development Studies, 50 (10), 1325-1347.

- Hofmann, E., Hoelzl, E., & Kirchler, E. (2008). Preconditions of voluntary tax compliance: Knowledge and evaluation of taxation, norms, fairness, and motivation to cooperate. Zeitschrift für Psychologie/Journal of Psychology, 216 (4), 209-217.

- Kadenge, J. M. (2021). Effect of Taxation on Economic Performance: A Case of Kenya.

- Kagarama, B. (2013). National Taxation Policy and Government Revenue.

- Kasper, M., Kogler, C., & Kirchler, E. (2015). Tax policy and the news: An empirical analysis of taxpayers’ perceptions of tax-related media coverage and its impact on tax compliance. Journal of behavioral and experimental economics, 54, 58-63.

- Kasipillai, J. (2003). The influence of education on tax avoidance and tax evasion. eJTR, 1, 134.

- Kelley, H. H., & Michela, J. L. (1980). Attribution theory and research. Annual review of psychology, 31(1), 457-501.

- Khramov, M. V. (2013). The Economic Performance Index (EPI): an intuitive indicator for assessing a country’s economic performance dynamics in an historical perspective. International Monetary Fund, 3(6), 123-134.

- Kimaru, T., & Jagongo, A. (2014). Adoption of Turnover Tax in Kenya: A Snapshot of Small and Medium Enterprises in Gikomba Market, Nairobi Kenya. International Journal of Social Sciences and Entrepreneurship, 3(1), 18-30.

- Koumpias, A. M., & Martínez-Vázquez, J. (2019). The impact of media campaigns on tax filing: Quasi-experimental evidence from Pakistan. Journal of Asian Economics, 63, 33-43.

- Lignier, P. (. (n.d.). 7, 106.

- Lignier, P. (2009). The managerial benefits of tax compliance: perception by small business taxpayers. eJTR, 7, 106.

- Marziana, H. M., Ahmad, N., & Deris, S. M. (2010). Perceptions of taxpayers with level of compliance: A comparison in the East Coast Region, Malaysia. Journal of Global Business and Economics, 1(1), 241-257.

- Mascagni, G., & Nell, C. (2022). Tax Compliance in Rwanda: Evidence from a Message Field Experiment. Economic Development and Cultural Change, 70(2), 587-623.

- McKenzie, D., & Sakho, Y. S. (2010). Does it pay firms to register for taxes? The impact of formality on firm profitability. Journal of Development Economics, 91(1), 15-24.

- Misra, R. (2004). The impact of taxpayer education on tax compliance in South Africa (Doctoral dissertation).

- Mehari, R. (2019). Taxation of Significant Digital Presence: an evaluative study on draft EU proposal to tax significant digital presence in context of EU primary Law.

- Munari, F. (2005). Creative destruction? Evidence that buyouts shed jobs to raise returns. Venture Capital, 13(1), 1-22.

- Modebe, N., Okoro, O., Okoyeuzu, C., & Uche, C. (2014). The (ab) use of import duty waivers in Nigeria. ASC Working Paper Series, 113.

- Mpambara, F. (2013). Assessment of challenges faced by tax collectors and tax payers in rural areas: A case study of Nyaruguru Distric. East African Journal of Science and Technology, 2(2), 1-18.

- Murray, B., & Rivers, N. (2015). British Columbia’s revenue-neutral carbon tax: A review of the latest “grand experiment” in environmental policy. Energy Policy, 86, 674-683.

- Newman, W., Mwandambira, N., Charity, M., & Ongayi, W. (2018). Literature review on the impact of tax knowledge on tax compliance among small medium enterprises in a developing country. International Journal of Entrepreneurship, 22(4), 1-15.

- (2014). Statistical Year Book.

- (2017). The OECD principles of corporate governance. Contaduría y Administración, (216).

- Ogbonna, G. N., & Appah, E. (2016). Effect of tax administration and revenue on economic growth in Nigeria. Research Journal of Finance and Accounting, 7(13), 49-58.

- Ojede, A., & Yamarik, S. (2012). Tax policy and state economic growth: The long-run and short-run of it. Economics Letters, 116(2), 161-165.

- Okello, A. K. (2001). An Analysis of Excise Taxation in Kenya.

- Oladipo, O. A., Nwanji, T. I., Eluyela, F. D., Godo, B., & Adegboyegun, A. E. (2022). Impact of tax fairness and tax knowledge on tax compliance behavior of listed manufacturing companies in Nigeria. Problems and Perspectives in Management, 20(1), 41-48.

- Olowookere & Fasina. (2013). Taxpayers’ education: A key strategy in achieving voluntary compliance in Lagos State, Nigeria. European Journal of Business and Management, 5(10), 146-154.

- Österberg, E. L. (2011). Alcohol tax changes and the use of alcohol in Europe. Drug and Alcohol Review, 30(2), 124-129.

- Otieno, D. E. (2003). An Empirical assessment of the link between Kenya’s Indirect Taxation and economic growth: 1970-2000 (Doctoral dissertation, MA Thesis, University of Nairobi).

- Palil, M. R. (2010). Tax knowledge and tax compliance determinants in self-assessment system in Malaysia (Doctoral dissertation, University of Birmingham).

- Park, C. G., & Hyun, J. K. (2003). Examining the determinants of tax compliance by experimental data: A case of Korea. Journal of Policy Modeling, 25 (8), 673-684.

- Pratiwi, I. S., & Siregar, S. V. (2019). The effect of corporate social responsibility on tax avoidance and earnings management: The moderating role of political connections. International Journal of Business, 24 (3), 229-248.

- Rahayu, Y. N., Setiawan, M., & Troena, E. A. (2017). The role of taxpayer awareness, tax regulation and understanding in taxpayer compliance. Journal of Accounting and Taxation, 9 (10), 139-146.

- Richardson, G. (2006). Determinants of tax evasion: A cross-country investigation. Journal of international Accounting, Auditing and taxation, 15 (2), 150-169.

- Saruç, N. T., Tunalı, Ç. B., Yavuz, H., & İnce, T. (2020). The effect of media on tax compliance: Hypothetical scenarios study. In Behavioral Public Finance (pp. 277-289). Routledge.

- Slemrod, J. (2018). Is this tax reform, or just confusion? Journal of Economic Perspectives, 32 (4), 73-96.

- Soled, J. A. (2010). Call for the Gradual Phase-Out of All Paper Tax Information Statements. FLORIDA TAX REVIEW, 10 (5), 5.

- Sommers, A. L., & Phillips, K. L. (1995). Assessing the Tax Administration Law of the People’s Republic of China. Loy. LA Int’l & Comp, LJ, 18, 339.

- Torgler, B. (2006). Russian attitudes toward paying taxes–before, during, and after the transition. International Journal of Social Economic, 2 (3),123-124.

- Trawule, A. Y., Gadzo, S. G., Kportorgbi, H. K., & Sam-Quarm, R. (2022). Tax education and fear-appealing messages: A grease or sand in the wheels of tax compliance? Cogent Business & Management, 9 (1), 2049436.

- Tsindeliani, I., Kot, S., Vasilyeva, E., & Narinyan, L. (2019). Tax system of the Russian Federation: Current state and steps towards financial sustainability. Sustainability, 11 (24), 69-94.

- Walsh, K. (2012). Understanding taxpayer behavior–new opportunities for tax administration. The Economic and Social Review, 43 (3, Autumn), 451-475.

- Wanyagathi Maina, A. (2019). The Kenyan tax regime for the oil and gas sector: An international tax perspective to policy and practical challenges. Revista Derecho Fiscal, 14.

- Wasylenko, M. J. (1997). Taxation and economic development: The state of the economic literature.

- Wawire, N. H. (2014). Effects of tax reforms on buoyancy and elasticity of the tax system in Kenya: 1963–2010.

- Wenzel, M. (2006). A letter from the tax office: Compliance effects of informational and interpersonal justice. Social Justice Research, 19 (3), 345-364.

- Yin, R. K. (2013). Design and methods. Case study research. 3 (9.2).