The Impact of China’s Aging Population on Real Estate Prices – Based on 31 Provinces in China

- Wu Guixian

- Doris Padmini Selvaratnam

- 263-280

- Mar 7, 2025

- Education

The Impact of China’s Aging Population on Real Estate Prices – Based on 31 Provinces in China

Wu Guixian* & Doris Padmini Selvaratnam

Universiti Kebangsaan Malaysia

*Correspondent Author

DOI: https://dx.doi.org/10.47772/IJRISS.2025.915EC0015

Received: 04 February 2025; Accepted: 08 February 2025; Published: 07 March 2025

ABSTRACT

Housing and aging are both major issues that China needs to solve today. China’s real estate market continues to heat up, and the real estate industry has gradually become a pillar industry that affects China’s national economy. The central core of real estate market growth consists of both supply and demand. At present, the elasticity of China’s real estate supply market is low, and the demand market dictates the behavior of the real estate market to a greater degree. The main body of housing demand is people, and population factors are one of the basic core factors affecting housing prices. Aging is an important indicator of population structure. Today, China’s population aging is deepening year by year, and it has become an important trend in social development, which will have a profound impact on the future real estate market. As aging deepens and the number of older persons increases, the need for new housing is likely to wane, while the demand for elderly care real estate, community services and other fields will increase, triggering structural changes in the real estate market.

In this regard, based on the social phenomenon of rising house prices and an aging population in China, this article deeply analyzes the internal mechanism of how an aging population affects housing prices in China, which is not only conducive to optimizing the population structure and rationally coping with an aging population, but also helps to promote the sustainability of house prices. After combing through the literature on population aging and housing price fluctuations, this paper adopts a two-way fixed effect model and uses panel data from 31 provinces and cities in China from 2009 to 2019 to organize the analysis of how the aging population will affect the house prices. The empirical results show that as population aging deepens, it has a beneficial effect on the rise of house prices. Finally, the paper makes relevant policy recommendations to deliver the necessary reference and support for optimizing the population structure, rational development of the real estate market, and high-quality economic development.

Keywords: China; Population aging; Real estate prices; Panel data; two-way fixed effect model

INTRODUCTION

Introduction of the present status of population aging

Size and proportion of the aging population

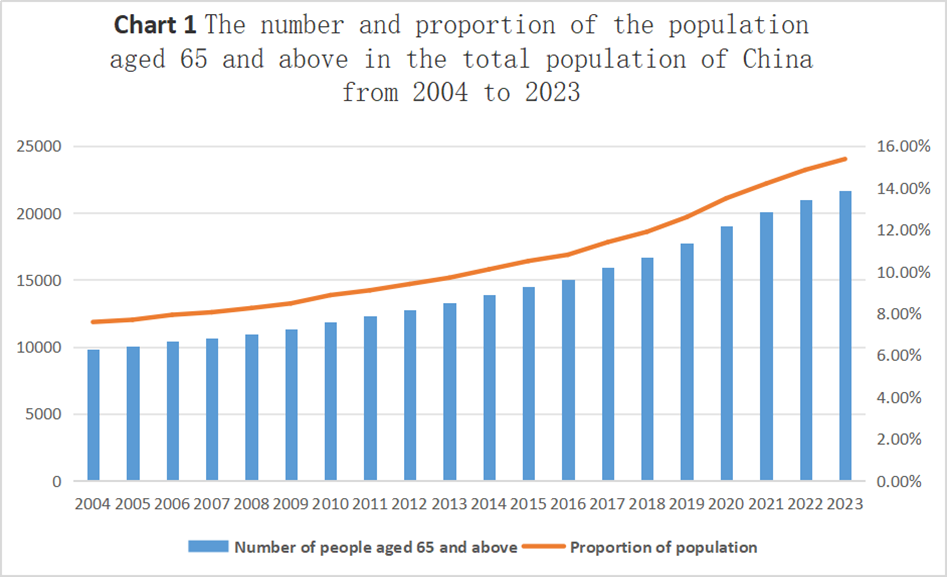

Source: Official website of National Bureau of Statistics of China

Chart 1 shows the number of people over the age of 65 in China and their proportion of the total population from 2004 to 2023. According to Figure 1, population aged 65 and over in China has been increasing year by year, accounting for 15.38% of the total population in 2023. As stipulated in the United Nations guidelines, when the proportion of people aged 65 and above exceeds 14%, it is called an “aging society”. It is obvious that China is already into the time of “ageing society”. Meanwhile, calculations show that from 2004 to 2013, the percentage of older Chinese population has grown from 7.58% to 9.7%, an average annual increase of 0.24 percent; the proportion of Chinese elderly population increased from 9.7% to 15.38% from 2013 to 2023. So Chinese population is aging at an accelerated rate, with an overall annual average growth rate of 0.57 percent.

Increase in elderly dependency ratio

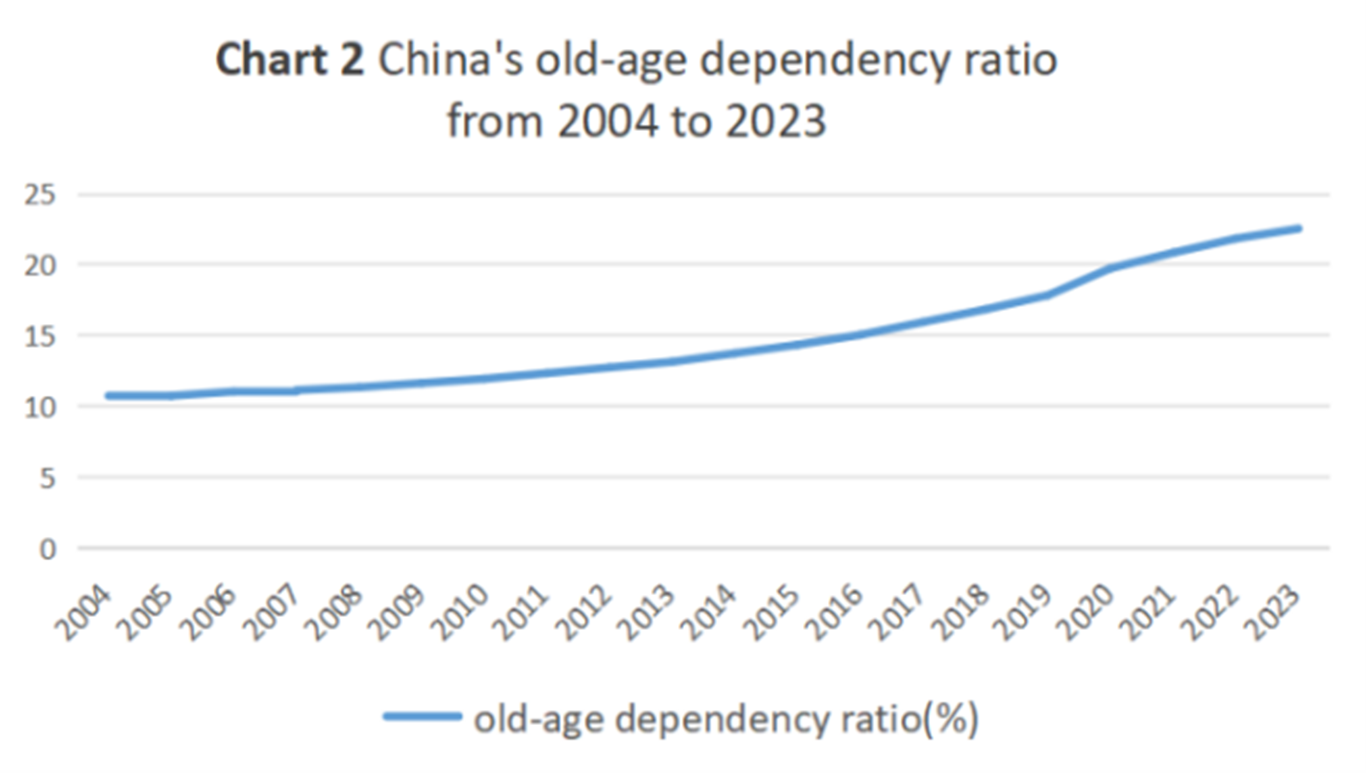

Source: Official website of National Bureau of Statistics of China

According to chart 2, On the basis of the figures announced by the National Bureau of Statistics, By 2023, Chinese old aging dependency ratio will increase to 22.5 percent. The Population and Labor Green Book: China’s Population and Labor Issues Report No. 19, released by the Population Institute of the Chinese Academy of Social Sciences, predicts that the reduction of the working-age population will hasten as the substantial number of people born in the 1950s grows beyond working age. The elderly old-age dependency ratio will keep on growing until 2060 and will outpace the dependency ratio for children as the dominating factor in deciding the trend of the aggregate dependency ratio by around 2028. The outcome of demographic aging will contribute straightaway to the escalating dependency ratio of the aged population. With a higher dependency ratio, there are more people to be supported by the average labor force, in other words, the burden of supporting the labor force is more serious.

Increased life expectancy

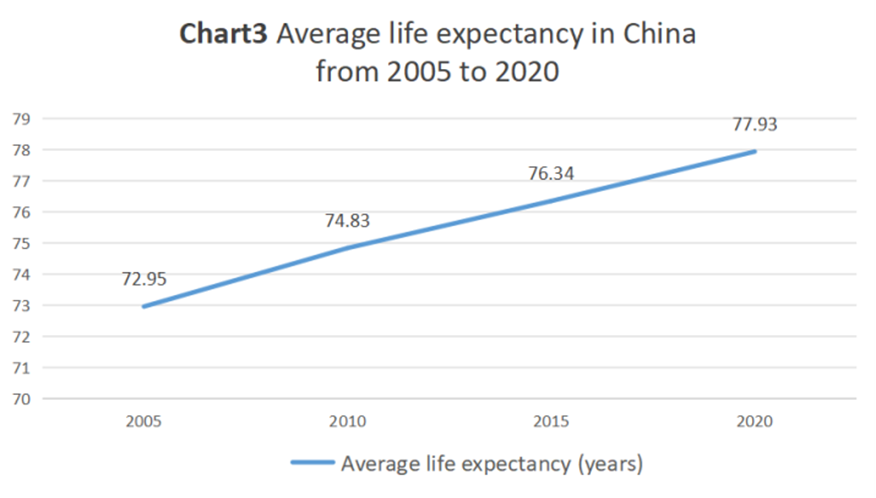

Source: Official website of National Bureau of Statistics of China

Chart 3 shows Chinese average lifespan from 2005 to 2020. It can be seen that As healthcare improvements and the standard of living improve, the expected lifetime of China’s residents has increased significantly, increasing from 73 years in 2005 to 78 years in 2020. The extension of average lifespan means that more people are entering the elderly stage, leading to an aggravation of aging.

Introduction of the current status of real estate prices

Source: Official website of National Bureau of Statistics of China

As shown in Chart 4, along with the recent years of fast property market expanding in China, commercial house price of selling in average has continued to rise, from RMB 2,778/ square meter in 2004 to RMB 10,323/ square meter in 2021, a 2.7-fold increase. Except for 2008, when it showed negative growth subject to the effects of the American subprime mortgage crisis, the rest of the years showed positive growth. As a result, China has implemented a series of measures to stimulate investment to ensure a higher inflow of money entering the property market, with growth reaching a peak of 23.2% in 2009. Subsequently, housing price growth rate began to slow down, but it still rose steadily every year.

Introduction of the influence of Chinese older population on housing prices

Property Prices are directly dependent on changes in supply and demand in the housing market, while population ageing has an indirect effect on it. This paper briefly describes the impact path from both the demand and supply side. Theoretically, the impact is both positive and negative, and in order to further prove how population aging affects house prices and its underlying mechanisms, further empirical studies are needed next.

supply side

Older people are likely to sell their excess housing in order to finance their retirement, thus increasing market supply while at the same time, a population that has purchased multiple homes in their younger years will be more likely to choose to sell their existing homes in their later years in exchange for old age wealth, which will increase the supply of housing on the market and thus have a dampening effect on real estate prices. Meanwhile, aging reduces the supply of young labor, leading to a slowdown in housing development, which reduces the supply of housing. Moreover, local governments may reduce the supply of land for housing, leaving limited resources for the construction of age-friendly public facilities.

demand side

The housing demand of the elderly population tends to fall into two categories: one is the rigid demand for their own housing, such as purchasing an apartment suitable for the elderly; the other is to use savings to purchase housing for their children out of traditional considerations. The influence of the senior population on property prices is also affected by the degree of their wealth accumulation. If the elderly population has accumulated a certain amount of wealth, the elderly support ratio at this time will have a more obvious promoting effect on housing prices. However, if the elderly population at this stage has not accumulated a certain amount of wealth, it will have a suppressive effect due to the cost of elderly care. Secondly, an aging population leads to a reduction in the supply of employment for the market-age working population, which increases wage income, improves the ability of young people to purchase homes, and expands the demand for housing.

RESEARCH SIGNIFICANCE

The government level

Clarifying the influence of the senior population on property prices allows governments to have an overall grasp of the issue at the beginning of the relevant policy formulation, which can effectively mitigate the real estate price turbulence caused by population aging and, to a certain extent, avoid the negative effect of excessive fluctuations in property prices on the entire national economic system, which is conducive to providing policy recommendations at the theoretical level to the government for the regulation of property prices, the improvement of the property market, and the solution of the problem of older population. This is helpful in providing policy recommendations to control property prices for the government , improve the housing market, and address problems of population aging from the theoretical level.

The companies level

Clarifying the relations between the older population and the price of accommodation and exploring the impact of aging on housing demand can guide the housing market at the development stage, rationalize the supply of the housing market, and contribute to the healthy, orderly, and efficient development of the property market. Effectively reduce the economic losses brought about by demand-supply imbalance in the property market, which can largely avoid the situation of blind development and over-development by real estate enterprises, save the cost of housing development and construction, and maximize the benefits.

In the following sections, I will discuss in detail about the literature review, methodology, data analysis, research findings and conclusion.

LITERATURE REVIEW

Research on real estate prices

During recent decades, China’s real estate market has experienced large fluctuations, influenced by multiple factors such as policy regulation and changes in the economic situation. According to Wang Haiyan et al. (2022), since 2020, the policy regulation of the property market has been continuously strengthened, aiming at curbing speculative home purchases and stabilizing market expectations. There are four main factors affecting the housing prices.

The first is the relationship between supply and demand. According to Zhang Ming (2022), the balance of supply and demand in the property market directly determines price fluctuations. In first-tier cities, due to the scarcity of land resources and the strong demand for housing, house prices continue to rise high. While in some third- and fourth-tier cities, house prices face downward pressure due to oversupply and population outflow.

Second, policy regulation. According to Li Qiang et al. (2023), the government regulates the market by restricting purchases, loans, land auctions, and other policy tools with the intention of curbing speculation and over investment. In 2021, the implementation of the “double-limit policy” has had a major impact on house prices in many places, especially in hotspot cities, where house price increases have slowed down significantly.

Third, the macroeconomic situation. According to Zhou Jun (2021), slowing economic growth, increasing inflation, and changes in interest rates all have an impact on the property market. In 2023, Growth rate of Chinese gross domestic product (GDP) is 4.5%, and the lack of economic recovery has led to a lack of confidence among home buyers, which affects the activity of the property market.

Fourth, market expectations. According to Chen Wei (2022), home buyers’ psychological expectations and investors’ market judgment affect their home buying decisions. If homebuyers believe that home prices will continue to rise, they may accelerate their home purchase decisions, and conversely, they may wait and see, leading to changes in market turnover.

Research on population aging in China

China is undergoing a profound demographic transition characterized by population aging, with multiple implications for its society and economy. By 2023, about 18.7 percent of China’s population will be of age 60 and older, and that number is expected to rise to nearly 35 percent by 2050(United Nations, 2019). The rate of population aging is accelerating. Zeng and Huang (2019) noted in their study that senior population growing rate is much higher than the growth rate of the population of other age groups and that the aging problem will become an important challenge for society in the future. According to the projections of the United Nations, China’s aging process is among the most rapid in the world.

The first main reason for the acceleration of aging is the decline in fertility rate. China’s childbearing rate has been declining since the 1980s. According to the National Bureau of Statistics, China’s childbearing rate at 1.3% by 2020, far below the replacement level (2.1). The root cause of this phenomenon is the rising cost of living brought about by economic development, higher education levels, and accelerated urbanization, (besides the already existing government’s Family Planning Policy) with many young families choosing to delay childbearing or opting not to have children. Zhou Ying et al. (2020) pointed out that the continued decline in fertility has led to a gradual decline in the proportion of younger people and the increasing number of aging populations.

The second reason is the extension of lifespan expectancy. With the improvement of living standards and advances in medical technology, the lifespan expectancy of the average China’s person has increased significantly. According to the World Health Organization (WHO), the average length of life in China has grown from 67 years in 1981 to 77 years in 2020. This trend has resulted to a growth in the elderly people, as well as increased pressure on social services such as pensions and medical care.

Research on the impact of population aging on real estate prices

Many existing researchers have studied the relationship between property prices and population aging. The conclusions drawn from these studies can be divided into three different perspectives, as elaborated below:

Significant negative correlation between population aging and property prices.

Wang Chongrun and Zhao Chang (2021) used the mediation effect model to examine from 2004 to 2019 for 30 provinces and cities in China. The results showed that aging of the population has a comprehensive disincentive impact on house price increases, among which risk-free asset preference inhibits house price increases, while inheritance motivation promotes house price increases. At the same time, the effects of the older population on home prices have more pronounced geographical variability. From the perspective of the mediating effect of aging population, the mediating effect of inheritance motivation is significantly greater than the mediating effect of risk-free asset preference in the regions of the east and west, in contrast, the situation is reversed in the center of the region.

According to the relations of Chinese older population, land policy changes and property prices, Xilin Zhang (2024) explores the influence of the aging of the population and land policy changes on house prices, and constructs relevant variables and VEC models to further study the dynamic correlation between the three. The empirical results show that in the long run, China’s population aging and increased land finance will increase the risk of falling housing prices; in the short term, influence of the older population on the cost of houses is a dampening effect, and this effect is more significant than the long-term effect.

Xiguang Cao (2023) first constructed an extended overlapping generation (OLG) model and an econometric model. The data used in this theory is the database of panel data of 287 prefecture-level or Chinese higher cities and time is since 2005 to 2018, the objective is to investigate the influence of the older population on city property prices, and through the evidence of the results of the analysis found that the older population remarkably reduces the city property prices. It further shows that urban housing demand, residents’ consumption and labor supply are important mechanisms for understanding the effects of ageing populations on urban house prices.

Significant positive correlation between aging population and housing prices.

Due to differences in cultural diversity, population size, and disparity between rich and poor, in Scotland, Japan and South Korea, research on house prices and aging populations has generated differing results. Taking China as an example, Jiayi Jin and Weiyi Dai (2021) collected data from China from 2004 to 2019, and then used economic methods such as OLG to calculate the correlation between the two factors. Based on fixed effect tests and data analysis, the findings suggest that there is indeed a direct association between the aging of the population and house prices.

In order to explore the influence of the older population and inter-urban migration on urban properties prices, Xinrui Wang (2018) selected and utilized the panel data of 294 Chinese prefecture-level cities for the analysis. The experimental results show that each one percentage point increase in the old-age dependency ratio leads to a 0.368 percentage point increase in property prices. In response to this result, the driving causes between the elderly population and house prices are analyzed, and it is concluded that the diversification of housing demand and the release of the purchasing power of the elderly will contribute to a rise in urban house prices.

Zihan Zeng (2022) analyzes the influence of changes in dependency ratios on property prices using panel data from China’s provinces from 2002-2019, based on a regression model of single variable linear regression, and in turn, adopts a grouping approach for the analysis of heterogeneity to conduct a regression analysis of different dependency ratios in China. Evidence-based results indicate that the child-rearing ratio is negatively associated with the annual average selling price of commodities in China, while the old-age population’s rearing ratio is actively correlated with the overall average sales price of Chinese commodities.

Uncertain impact of population aging on property prices

The third view holds that the impact of the older population on property prices is not certain and may have different impacts on property prices based on factors such as regional differences, differences in aging levels, and time effects. Scholars have chosen different regions, time periods, and research methods and have reached different research conclusions.

Using China’s provincial panel data from 2000 to 2019, Jipeng Liu (2021) empirically shows that as China’s aging population has deepened, it has progressively become a factor affecting changes in China’s house prices at the countrywide level. Hierarchically, population aging in under-developed regions has no obvious association with commodity home prices, population aging in developed regions has a remarkable negative impact on commodity home prices, and in developing regions population aging has a remarkable forward impact on commodity home prices. Because of the variation of geographical differences, the impact of the elderly population on the purchase price of housing shows notable differences.

Ma Yao (2023) uses data from Shaanxi Province from 1994 to 2020 as a research sample and studies the relationship between population aging and property prices through a multivariate regression model. The study found that population aging has a suppressive influence on property price increases, but as the older population increases, population aging gradually shows a positive influence on property prices and can explain generational transfers.

Shihong Zeng (2019) conducted an empirical study based on a portfolio regression model using census data from prefecture-level cities in China using the two-stage least squares method, and showed through an interaction analysis that the impact of older population on property prices in this case is different, subject to various family savings levels, meaning that older population affects house prices through family savings, for example, the release of the savings of the elderly can gradually dampen the house prices.

Meng Li, Kunrong Shen (2013) studied the impact of demographic change on housing consumption, and using the generational overlap model, found that there is a nonlinear relationship between housing consumption and the old-age dependency ratio in China. Specifically, as the population ages, the consumption of purchasing houses shows an upward trend, but when the old-age dependency ratio reaches a certain inflection point, housing consumption begins to decline. Meanwhile, they predict that the inflection point of this non-linear curve will occur in 2025, when China’s old-age dependency ratio will reach 32%, which means that China will be required to continuously expand the supply of the property market over the next decade.

METHODOLOGY

Selection of variables

Explained Variables

The explanatory variable of this paper is house price. On the foundation of established surveys, this article uses the annual commercial house average sales price (p) of each province in China as a substitute variable, and logarithmically treats this variable in the experimental period (lnp).

Explanatory Variables

The article chooses China’s population aging as the core explanatory variable and selects the elderly dependency ratio (epr) to measure it. Old-age dependency ratio usually presented as a proportion, representing number of older people to be supported by every 100 working-age people. It is calculated as (number of older persons over 65 years of age/persons aged 15-65 years)*100%. This indicator can capture the extent of population ageing from an economistic point of view.

Control Variables

Considering the impact of many factors on house prices, such as gender ratio, regional population density, pension system, medical level, green development, etc., this paper selects the following control variables for estimation to minimize the bias of omitted variables.

PCGDP: Per capita GDP is an efficient indicator of the performance of a country or region’s macroeconomy. GDP per capita = aggregate output of social goods and services/total population. An increase in per capita income increases home ownership and housing demand.

SR: Sex ratio is percentage of males and females in the population of an area or country, referring to number of men for every 100 women. The formula is: sex ratio = male population/female population.

PI: Number of participants in basic urban pension insurance at the end of the year (10,000 people). This is an important indicator of the effectiveness and the influence of the application of the old-age assurance program in the various regions. Increasing the audience and coverage of the pension system indicates the improvement of the revenue level and employment stability of the residents, which in turn enhances the ability to pay for the purchase of houses and increases the demand in the property market, which in turn pushes up the house prices.

GCR: Greening coverage rate of built-up areas (%). As people’s quality of life increases, the pursue of high quality of living is also becoming more and more high. Urban environmental factors have an important effect on the price of property, so this paper takes the green coverage rate of urban built-up areas as an indicator of urban environmental factors.

UPD: Urban Population Density. It reflects the sparseness of population in a certain area. When an area is densely populated, it often means that more people need housing. Since the supply of housing resources is relatively fixed and limited, this high demand directly pushes up housing prices.

MHI: Number of healthcare facilities. It reflects the level of healthcare and health services capacity in the area. The abundance of medical resources will enhance the attractiveness of settlement and drive up the demand for housing.

Data Sources

This paper selects the statistical data of 31 provinces in China from 2009 to 2019 for empirical analysis. The data sources are mainly from the official website of the National Bureau of Statistics of China (NBS) and the statistical yearbooks of Chinese provinces and the CSMAR database.

Building the Model

The research model of this paper is a fixed effect model, which is as follows:

LnP = β0+β1* lnEPR+βi* Xit +ε

whereby, P is the real estate price in each province and is the explained variable. EPR, the old-age dependency ratio is the main explanatory variable. Xit is the control variable, including PCGDP, SR, PI, GCR, UPD, MHI. The above eight variables are all processed logarithmically. β0 is the intercept, β (i=1,2,3,4,5,6,7,8) is the coefficient, ε represents the error, which includes the impact of factors such as consumer psychological expectations and national policies on housing prices.

Empirical Analysis

Descriptive statistics

Table1 : Descriptive statistics

| N | Mean | SD | Min | Max | |

| lnp | 324 | 8.688 | 0.499 | 7.805 | 10.489 |

| lnepr | 324 | 2.58 | 0.237 | 1.947 | 3.171 |

| lnmhi | 324 | 10.055 | 0.861 | 8.326 | 11.351 |

| lnpcgdp | 324 | 10.623 | 0.496 | 9.289 | 11.994 |

| lnsr | 324 | 4.652 | 0.031 | 4.584 | 4.717 |

| lnpi | 324 | 6.578 | 1.019 | 2.223 | 8.534 |

| lngcr | 324 | 3.652 | 0.107 | 3.235 | 3.894 |

| lnupd | 324 | 7.858 | 0.434 | 6.354 | 8.669 |

Table 1 shows the descriptive statistics. The mean value of the explanatory variable lnp is 8.688 and the mean value of the core explanatory variable lnepr is 2.58.

Correlation analysis

Table2 : Correlation analysis

| lnp | lnepr | lnmhi | lnpcgdp | lnsr | lnpi | lngcr | lnupd | |

| lnp | 1 | |||||||

| lnepr | 0.319*** | 1 | ||||||

| lnmhi | -0.323*** | 0.429*** | 1 | |||||

| lnpcgdp | 0.876*** | 0.392*** | -0.157*** | 1 | ||||

| lnsr | -0.406*** | 0.062 | 0.396*** | -0.477*** | 1 | |||

| lnpi | 0.359*** | 0.651*** | 0.607*** | 0.494*** | -0.038 | 1 | ||

| lngcr | 0.462*** | 0.298*** | 0.243*** | 0.531*** | 0.047 | 0.521*** | 1 | |

| lnupd | -0.062 | 0.068 | 0.189*** | -0.115** | 0.182*** | 0.135** | -0.123** | 1 |

| *** p<0.01, ** p<0.05, * p<0.1 | ||||||||

The correlation coefficients of the core explanatory variable, elderly population dependency ratio, and the explanatory variable, house price, are positive and significant at the 1% level, which is basically consistent with the research hypothesis. At the same time, there is a clear correlation between the variables, which allows for further regression.

Multicollinearity test

Table3: Multicollinearity test

| Variable | VIF | 1/VIF |

| lnpi | 4.220 | 0.237 |

| lnpcgdp | 3.600 | 0.278 |

| lnmhi | 3.160 | 0.317 |

| lngcr | 2.010 | 0.498 |

| lnepr | 1.950 | 0.512 |

| lnsr | 1.800 | 0.554 |

| lnupd | 1.130 | 0.884 |

| Mean | VIF | 2.550 |

The VIF in the table are all less than 10, indicating that there is no multicollinearity and the test passes.

Model Selection

F-test

The p-value is less than 0.05, so the fixed effects model is better than OLS.

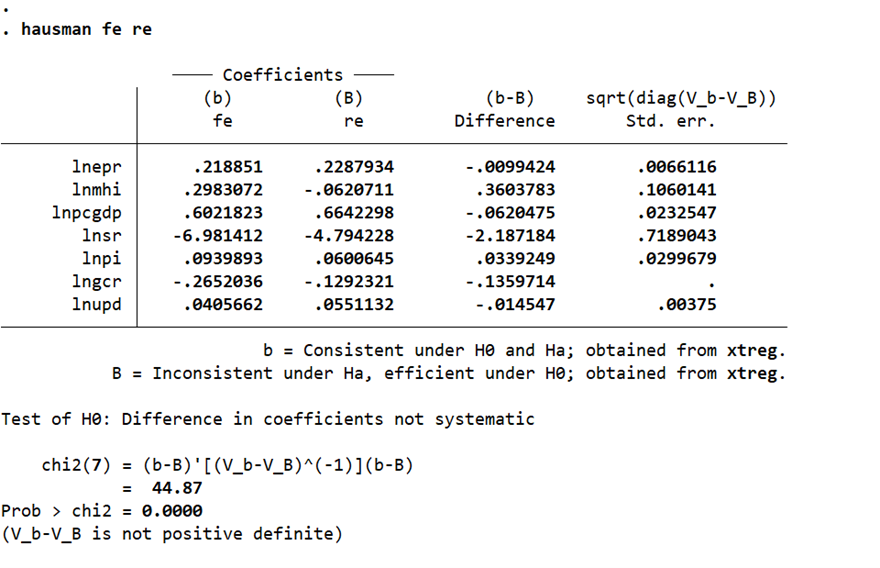

Hausmann test

The P-value is less than 0.05, so fixed effects are better than random effects and a two-way fixed effects model is chosen.

Model comparison

Table4: Model comparison

| (1) OLS | (2) FE | (3) RE | |

| lnp | lnp | lnp | |

| lnepr | 0.180*** | 0.219*** | 0.229*** |

| (0.068) | (0.047) | (0.046) | |

| lnmhi | -0.234*** | 0.298** | -0.062 |

| (0.024) | (0.119) | (0.054) | |

| lnpcgdp | 0.703*** | 0.602*** | 0.664*** |

| (0.044) | (0.041) | (0.034) | |

| lnsr | 1.132** | -6.981*** | -4.794*** |

| (0.496) | (1.165) | (0.917) | |

| lnpi | 0.074*** | 0.094* | 0.060 |

| (0.023) | (0.050) | (0.040) | |

| lngcr | 0.419*** | -0.265** | -0.129 |

| (0.153) | (0.116) | (0.118) | |

| lnupd | 0.076*** | 0.041 | 0.055* |

| (0.028) | (0.031) | (0.031) | |

| _cons | -4.775** | 31.234*** | 23.615*** |

| (2.287) | (5.833) | (4.289) | |

| N | 324.000 | 324.000 | 324.000 |

| r2 | 0.831 | 0.913 | |

| r2_a | 0.828 | 0.901 | |

| Prob > chi2 = 0.0000 | |||

Standard errors in parentheses

* p < 0.1, ** p < 0.05, *** p < 0.01

Comparing the three columns in the table, it can be seen that lnepr is a positive contributor to lnp regardless of the OLS test, fixed effects or random effects test, and all of them are at 1% level of significance, which further confirms the credibility of the conclusions. Therefore, next, among the three models, we choose the most suitable fixed effect model for regression.

Regression to the base line

Table5: Regression results

| (1) | (2) | |

| lnp | lnp | |

| lnepr | 0.1796*** | 0.1351** |

| (0.0656) | (0.0637) | |

| lnmhi | -0.2339*** | 0.3620*** |

| (0.0272) | (0.1135) | |

| lnpcgdp | 0.7033*** | 0.1185 |

| (0.0434) | (0.0810) | |

| lnsr | 1.1316** | -1.2501 |

| (0.4457) | (1.2965) | |

| lnpi | 0.0737*** | 0.0462 |

| (0.0219) | (0.0748) | |

| lngcr | 0.4192** | -0.1639 |

| (0.1743) | (0.1689) | |

| lnupd | 0.0764*** | 0.0098 |

| (0.0272) | (0.0278) | |

| i.year fe | NO | YES |

| i.id fe | NO | YES |

| _cons | -4.7753** | 9.4735 |

| (1.9064) | (6.0319) | |

| N | 324.0000 | 324.0000 |

| r2_a | 0.8277 | 0.9776 |

Standard errors in parentheses

* p < 0.1, ** p < 0.05, *** p < 0.01

The first column reports the results of the regression of the elderly population dependency ratio on house prices; the regression coefficient for the elderly population dependency ratio is 0.1796 and is significant at the 1 percent level. The second column shows the regression results with the addition of control variables, and the regression coefficient for the elderly population dependency ratio is 0.1351 and significant at the 5% level.

Comparing the two columns, it can be seen that the lnepr regression coefficient is significantly positive regardless of whether the year fixed effect and province fixed effect are added or not, i.e., China’s elderly population dependency ratio has a significant positive promotion effect on the average sales price of commercial properties. This is because as China’s aging deepens, the demand for age-appropriate housing continues to increase. At the same time, elderly families in China are often willing to use their own savings to buy houses for their children, which to some extent also leads to rising demand and pushes up house prices.

Robustness testing

Table6: Robustness testing

| (1) | (2) | |

| lnp | lnp | |

| lnepr | 0.1789*** | 0.1210* |

| (0.0612) | (0.0619) | |

| lnmhi | -0.2920*** | 0.2459** |

| (0.0281) | (0.1038) | |

| lnpcgdp | 0.6473*** | 0.1527* |

| (0.0433) | (0.0776) | |

| lnsr | 1.9419*** | -0.9838 |

| (0.5059) | (1.2122) | |

| lnpi | 0.1637*** | -0.1600** |

| (0.0287) | (0.0667) | |

| lngcr | 0.3286* | -0.2883** |

| (0.1860) | (0.1225) | |

| lnupd | 0.0848*** | -0.0103 |

| (0.0252) | (0.0291) | |

| i.year fe | NO | YES |

| i.id fe | NO | YES |

| _cons | -7.7018*** | 11.0573** |

| (2.0943) | (5.6001) | |

| N | 315.0000 | 315.0000 |

| r2_a | 0.8339 | 0.9809 |

Standard errors in parentheses

* p < 0.1, ** p < 0.05, *** p < 0.01

When conducting empirical research at the provincial level in China, due to the natural conditions and political factors of the TAR, it is more different from other provinces in terms of economy, population, real estate market, etc., i.e., the quality and reliability of its data are lower, and in order to avoid the adverse effects on the empirical results, after excluding the data from TAR, the sample is usually regressed again, and from the regression results, it can be seen that the regression coefficient of lnepr on lnp still has a significant positive contribution, and the regression coefficient changes from 0.135 to 0.121, which is a reasonable change and significant at the 10% level, indicating that the benchmark regression results are robust.

Endogeneity test

Table7: Endogeneity test

| (1) | (2) | |

| lnepr | lnp | |

| L.lnepr | 0.3589*** | |

| (0.0630) | ||

| lnepr | 0.3068** | |

| (0.1282) | ||

| lnmhi | -0.0499 | -0.2046*** |

| (0.1170) | (0.0535) | |

| lnpcgdp | -0.2245** | 0.3494*** |

| (0.0882) | (0.0826) | |

| lnsr | -0.8572 | -2.3453** |

| (1.4033) | (0.9137) | |

| lnpi | -0.0606 | 0.1281*** |

| (0.0544) | (0.0436) | |

| lngcr | -0.0647 | -0.2295* |

| (0.1039) | (0.1331) | |

| lnupd | -0.0039 | 0.0464 |

| (0.0306) | (0.0311) | |

| Year fixed effect | YES | YES |

| Province fixed effect | YES | YES |

| F-values in the first stage | 14.31 | |

| _cons | 9.2262 | 16.7043*** |

| (6.2974) | (4.3348) | |

| N | 286.0000 | 286.0000 |

| r2_a | 0.9279 | 0.9009 |

Standard errors in parentheses

* p < 0.1, ** p < 0.05, *** p < 0.01

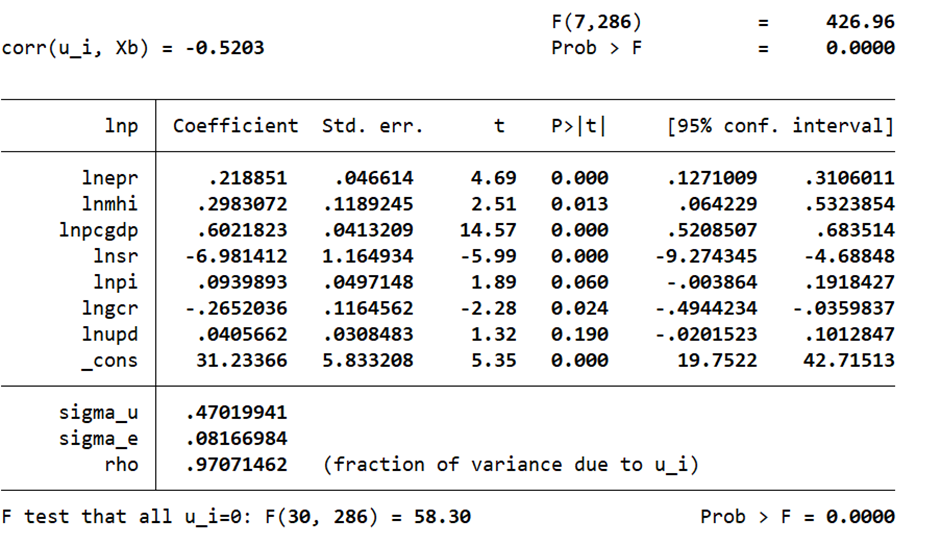

In this table7, the lag of the central explanatory variable lnepr, L.lnepr, was selected as an instrumental variable for endogeneity testing to fulfill the exogeneity and correlation requirements. As can be seen from the regression results, the first stage F-statistic in the table is 14.31, which is significantly larger than the empirical value of 10, indicating that there is no weak instrumental variable problem. The regression results in the first stage indicate that lnepr lag has a significant positive effect on current period lnepr. The regression results in the second stage show that after dealing with endogeneity, lnepr still has a significant promotional effect on lnp. This indicates that the choice of instrumental variables in this paper is reasonable and the results of the benchmark regression are robust and credible.

RESULTS AND DISCUSSION

From the empirical analysis, We can get the following result of the equation:

lnp = 9.132+0.135* lnepr+0.362*lnmhi+0.118*lnpcgdp-1.250*lnsr+0.046*lnpi-0.164*lngcr+0.01lnupd+ε

From the above equation it can be known that many factors have an impact on rising real property prices. A causal analysis of the specific effects of each variable follows:

Population ageing has a contributing effect on the rise of property prices, suggesting that China’s population ageing has a greater positive impact on the demand side of the property market. The first reason is that the aging population has contributed to a decrease in the number of working-age workers in the job market and a decrease in jobs supply, an increase in wage income, and an increase in the ability of young people to purchase homes, expanding housing demand. The second reason is that influenced by the traditional Chinese culture, most of the elderly people have to purchase houses for their children for marriage or inheritance of fixed assets. The third reason is that the demand for ageing housing has risen among the elderly population for their own considerations, and the wealth they have accumulated will be used to purchase apartments suitable for the elderly. All of these reasons contribute to the positive impact of older population on property prices.

The number of medical facilities contributes to the rise in property prices. More medical and healthcare facilities indicate that the region is rich in medical resources, which enhances the attractiveness of the region for settlement and drives up real estate prices.

GDP per capita has a positive influence on property prices. The rise in disposable income makes more people have the ability to purchase and pay for housing, and at the same time, the reserve capacity of residents has increased, more people choose real estate as an investment tool, which further pushes up the price of real estate.

Sex ratio has an inhibiting effect on the rise of property prices. An imbalance in the sex ratio will result in an increase in delayed marriages or even non-marriage, thus reducing the demand for marital housing and exerting downward pressure on housing prices.

Participants in basic urban pension insurance at year’s end promoted the growth of the price of property. An increase in the number of urban pension insurance participants is usually associated with an increase in the level of urbanization, and the growing population of the city also increases the needs for housing. At the same time, the extension of the cover of the old-age insurance system indicates an increase in the level of social security, which suggests that the increased ability of people to afford housing has promoted the rising of house prices.

The green coverage of built-up areas has a restraining influence on the rise of the prices of real estate. A well-balanced distribution of green space allows most residents to enjoy the convenience of greening, which will cause house prices to climb in the surrounding areas. However, if the distribution of green space construction is unreasonable, such as being too concentrated in the suburbs, it will not promote housing prices, and therefore China needs a more rationalized greening plan at this stage.

Urban population density contributes to the rise of real estate prices. High population density means high demand for housing, and due to the limited supply of land, the price of land rises significantly, increasing the cost of housing development. Meanwhile, high population density areas have better infrastructure development, which makes the region more attractive and drives up real estate prices.

POLICY IMPLICATION

Increase the supply of residential housing for the elderly

Encourage developers to build residences in accordance with ageing-friendly design standards, such as barrier-free access, low steps, non-slip floors and spacious corridors. In communities with a dense elderly population, promote the construction of community hospitals, rehabilitation centers, senior activity centers and other facilities for the elderly to create a more convenient living environment for the elderly. In response to the characteristics of the elderly in reducing the demand for living space, encourage the development of small and medium-sized, affordable properties.

Promoting the development of medical and nursing homes

In areas where the elderly population is concentrated, combine medical services, rehabilitation care, living services and other resources to build medical and nursing communities, so that the elderly can enjoy basic medical services where they live. At the same time, intelligent health monitoring systems are being promoted in retirement communities to facilitate the monitoring of daily health data by the elderly and docking with community medical centers through the platform to achieve health data sharing and timely warning.

Innovating the consumption pattern of home purchase

Accelerating the realization of the same rights for renting and purchasing, so that renters and purchasers enjoy the same rights to education, healthcare and other resources, easing the pressure of purchasing housing brought about by housing in school districts, increasing the willingness of residents to rent, and promoting the activation of the housing rental market. Implementing shared-ownership housing in areas with excess housing stock, where the government or enterprises hold part of the ownership rights and young and middle-aged people only need to purchase part of the ownership rights, reducing the pressure on down payments and loans. Provide residents who purchase shared-ownership housing with full use rights, including moving into the household registration and enrolling their children in school. After the purchaser’s financial situation improves, he or she can gradually buy back the property rights held by the government or enterprises, realizing full property rights ownership.

The implementation of regional differentiation policy

In cities or regions with a high degree of aging, set price ceilings for retirement properties with strong demand for senior citizens, to prevent developers from taking advantage of the immediate needs of the elderly to push up property prices. Adjust the down-payment ratio and loan policies for different types of properties, implement more flexible down-payment ratio and loan interest rate policies for properties that meet the needs of the elderly (e.g., medical and nursing homes, small-sized retirement homes, etc.), and provide tax incentives for the elderly to purchase aging-adapted residential properties, so as to lower the threshold for elderly people’s home purchases; and appropriately increase down-payment ratios for properties of a stronger nature for short-term investment, so as to reduce the number of investors entering the property market.

Optimizing urban layout

Optimize the construction of infrastructure and public services to enhance the attractiveness of small towns and villages, so that they can become livable choices for the elderly. Set up community medical centers in small towns and villages, and construct regional elderly care institutions to provide specialized care for the elderly. Build convenient transportation networks to closely connect small towns and surrounding big cities while creating a healthy and livable urban environment for the elderly through scientific planning and policy support, firstly, focusing on urban greening and increasing the area of urban green space, secondly, optimizing the distribution of medical resources and reducing the medical costs of the elderly, and thirdly, improving the convenience of transportation and planning a public transportation system suitable for the elderly, such as low-floor buses, subway elevators, barrier-free access, etc.

CONCLUSION

This paper adopts a two-way fixed effect model and uses panel data from 31 provinces and cities in China from 2009 to 2019 to empirically analyze the impact of China’s aging population on housing prices. Property prices are decided straight away by changes in both demand and supply in the real estate market and are indirectly affected by population aging. The findings of the research show that population aging has a positive effect on housing prices mainly by affecting housing demand. First, the aging of the population has resulted in a decline in the supply of employment for the market-age workforce, an increase in wage income, and an increase in the ability of young people to buy houses, which expands housing demand. Second, influenced by traditional Chinese culture, most elderly people have to buy houses for their children to get married or inherit fixed assets. Third, for their own considerations, the elderly group has an increased demand for aging-friendly housing, and the accumulated wealth will be used to purchase apartments suitable for retirement. All of the above reasons have promoted the active influence of the aging population on the price of real estate. To conclude, the article proposes recommendations for policies that are relevant to provide necessary reference and support for optimizing the population structure, the rational development of the real estate market, and the high-quality development of the economy.

ACKNOWLEDGEMENT

This paper results from an academic exercise for EPPE6908 funded by EP-2018-001 at the Faculty of Economics and Management, Universiti Kebangsaan Malaysia.

REFERENCE

- Zhang, X. Potential Impact of Land Policy Change and Population Ageing on House Price Volatility.DOI: 10.32629/memf.v5i2.1988

- Zeng, Z. (2022). Analysis of the impact of population structure change on housing Pricei China. Advances in Economics, Business and Management Research/Advances in Economics, Business and Management Research. https://doi.org/10.2991/aebmr.k.220307.257

- Bai, Y., & Tan, M. (2018). Empirical testing of influencing factors of China’s housing prices – evidence from provincial panel data. Research in World Economy, 9(1), 9. https://doi.org/10.5430/rwe.v9n1p9

- Dai, W., & Jin, J. (2021). The Impact of Population Aging o nReal-estate Price: An empirical application at the provincial level in China.

- Cao, X., Deng, M., Kong, Y., & Li, S. The Impacts of Population Aging on Urban House Prices: Evidence from Chinese Real Estate Market. Available at SSRN 4666796.

- Wang, X., Hui, E. C., & Sun, J. (2018). Population Aging, Mobility, and Real Estate Price: Evidence from Cities in China. Sustainability, 10(9), 3140. https://doi.org/10.3390/su10093140

- Zeng, S., Zhang, X., Wang, X., & Zeng, G. (2019). Population aging, Household savings and asset Prices: A study based on urban commercial housing prices. Sustainability, 11(11), 3194. https://doi.org/10.3390/su11113194

- Chai, K. C., Liu, R. Y., Zhu, J. W., Lan, H. R., Xi, W. T., & Chang, K. C. (2022). Research on the challenge of population structure brought by China’s ‘Wu Zi’culture-Impact of economic growth and housing prices on population ageing.

- Mao, Y., Zhang, Z., Chen, Q., & Hu, Y. (2023, March). Population Age Structure and Housing Price–An Analysis Based on Panel Data from 2007 to 2019 in Zhejiang Province. In ICICA 2022: Proceedings of the 2nd International Conference on Information, Control and Automation, ICICA 2022, December 2-4, 2022, Chongqing, China (p. 44). European Alliance for Innovation.

- Tan, M., & Bai, Y. (2018). Empirical Testing of the Impact of Gender and Marital Status on the Price and Trend of Urban Real Estate–Evidence from Provincial Panel Data of China. International Journal of Economics and Finance, 10(7), 1-38.

- Dong, Z., Liu, J., Sha, S., Li, X., & Dong, J. (2017). Regional disparity of real estate investment in china: Characteristics and empirical study in the context of population aging. Eurasia Journal of Mathematics, Science and Technology Education, 13(12), 7799-7811.

- Mou, X., Li, X., & Dong, J. (2021). The impact of population aging on housing demand in China based on system dynamics. Journal of Systems Science and Complexity, 34(1), 351-380.

- Zhang, H., Lu, T., & Sun, Y. (2019, May). Research on the development of real estate market based on population change in China. In IOP Conference Series: Earth and Environmental Science (Vol. 267, No. 6, p. 062031). IOP Publishing.

- Li, M., & Shen, K. (2013). Population aging and housing consumption: A nonlinear relationship in China. China & World Economy, 21(5), 60-77.

- Yao, M. (2023). The impact of aging population on housing prices in Shaanxi Province. Academic Journal of Business & Management, 5(2), 73-79.

- Ma, S. (2020). Family Planning Policy and Housing Price in China. European Journal of Economics and Business Studies Articles, 6.

- Lin, Y., Ma, Z., Zhao, K., Hu, W., & Wei, J. (2018). The impact of population migration on urban housing prices: Evidence from China’s major cities. Sustainability, 10(9), 3169.