The Impact of Strategic leadership and Committee practices, Ethics Training, and Whistleblowing on Fraud Prevention in Churches

- Wasswa Asaph Senoga

- 2934-2956

- May 24, 2024

- Religious Studies

The Impact of Strategic leadership and Committee practices, Ethics Training, and Whistleblowing on Fraud Prevention in Churches

Wasswa Asaph Senoga

Bishop Tucker School of Theology and Divinity, Uganda Christian University, Mukono

DOI: https://dx.doi.org/10.47772/IJRISS.2024.804275

Received: 10 April 2024; Revised: 19 April 2024; Accepted: 24 April 2024; Published: 24 May 2024

ABSTRACT

Purpose – The purpose of this paper is to examine the impact of strategic leadership and committee practices, ethics training, whistleblowing, and their effects on the Fraud prevention of Churches.

Design/methodology/approach – Data were collected from 12 surveys conducted in the church of Uganda dioceses in central Uganda. Regression analysis was conducted to examine the relationships between the impact of Strategic leadership and Committee practices, ethics training, whistleblowing, and fraud prevention.

Findings – The findings revealed that strategic leadership and committee practices, ethics training, and whistleblowing significantly contribute to positive fraud prevention for Church finances.

Practical implications – In order for Churches to prevent fraud, serious emphasis on strategic leadership, ethics training, and whistleblowing is vital.

Originality/value – According to the author’s understanding, this is one of the first empirical studies to assess the impact of strategic leadership and committee practices, ethics training, and whistleblowing on fraud prevention in the Church of Uganda.

Keywords: Strategic leadership, Staff ethical training, Whistleblowing mechanism, Fraud Prevention.

INTRODUCTION

Over the last decade, the corporate Integrity concerns of non-profit organizations have been brought up in an effort to minimize fraud instances, with the Churches being aggressively encouraged to implement Strategic leadership and Committee practices, ethics training, and whistleblowing mechanisms to enhance Fraud Prevention (Alzola & Arkan, 2021; Bainbridge, 2021; Niemandt, 2019; Onyinah, 2020). In addition, a lack of fraud prevention strategies has ramifications and implications for churches as a result of donors’ loss of faith. Implementing Strategic leadership and Committee practices, ethics training, and whistleblowing is essential for churches to recover public confidence.

Fraud is an impediment to an institution’s development because it undermines good governance, distorts public policy, results in the misallocation of resources, and hinders economic progress (Asea, 2018; Balfour, Sullivan, Self & Byers, 2021; Pan, Blankley, Harris & Lai, 2022; Rockson, 2019). In Uganda, financial scandals, such as the embezzlement by church leaders, have damaged the credibility of the Churches.

Meanwhile, Extensive research has been conducted on the aspects of corporate integrity that contribute mitigation of financial fraud in ecclesiastical organizations, although these studies tend to concentrate on managerial efficiency (Decker et al., 2019; Ghanem & Castelli, 2019; Jachi, 2019; Njobvu et al., 2020). However, there is a severe dearth of empirical research examining the variables that influence fraud prevention results in the setting of churches. Consequently, the purpose of this research is to identify and investigate the three elements of the corporate integrity system that enhance fraud prevention in church organizations. This research examines the link between three components of the Corporate Integrity System (Strategic leadership and Committee practices, Staff ethical training, and whistleblowing mechanisms) on fraud mitigation in the church of Uganda dioceses in central Uganda.

Strong grounds exist for doing research in a country like Uganda. Uganda is a developing economy that aims to attain the vision of 2020 by 2030 and become a middle-income country. Therefore, the church of Uganda takes corporate integrity seriously by promoting strategic leadership, whistleblowing mechanisms, and ethical guidelines that offer organizations a framework for reducing fraud opportunities, and an overall indication of organizational integrity. It is a strategy adopted to assist establishments in assessing and measuring their progress toward a formal and transparent commitment to ethics and integrity in the workplace (Balfour et al., 2021; Fernandhytia & Muslichah, 2020; Mawanza, 2014).

LITERATURE REVIEW AND HYPOTHESES DEVELOPMENT

Strategic leadership and Committee practices and Fraud prevention

According to Shahid et al., (2022), committees should contain individuals with various experiences and skill sets. Committee members should keep each other accountable for providing board tasks with appropriate time to discuss critical problems and choices thoroughly. The committee should consistently endeavor to increase its members’ understanding of the field of corporate governance. The Non- Profit- organizations like churches should have a functional board with the necessary composition, size, and commitment to effectively carry out their tasks and duties (Zollo et al., 2019). Lee, (2020) added that committees should embrace independent directors.

Prior research indicated that strengthening committee practices could be beneficial in a variety of ways. According to Bryson, (2018), organizations can enhance their governance processes by clearly stating their beliefs and objectives and improving human resource development, leadership, and staff training. Moreover, through improved management procedures, financial management, accounting, and budget systems.

Balfour, (2020) posits that fraud opportunities can be thwarted in churches with a strong board of directors. Hoppmann, Naegele & Girod, (2019) established that to maintain a stable, powerful board, those involved must be competent and have corresponding inclinations, level of knowledge, and source of income. Defining an organization’s strategic direction results in its improvement. According to Deming (2022); Munyao (2021) when done well, strategic planning positively affects church performance by broadening the scope and quality of services and multiplying financial resources. According to McGahan (2021), the strategy creates a chance for stakeholders to come to an agreement. In such forums, long-term solutions are forged, provided the leadership pauses and reconsiders its mission to develop a long-term vision for the church. Aine (2022) states that strategy enables churches to be more focused and effective in their endeavors, benefitting teamwork. A well-developed church plan is a foundation for making key decisions such as resource allocation. This would result in greater performance as resources are allocated to essential departments. Indah et al., (2022) argue that motivated employees exploit the weaknesses of the committee of directors to commit fraud. Akotia (2019) posits that members of committees with limited capacity cannot participate effectively in procedural exercises and decision-making. According to Mojambo (2022), it is expected that the ability of the management committee would be enhanced by organizational performance. Nortey (2019), Miiro (2013), and Rockson (2019) conclude that the real power of churches is due to the poor capability of the finance committee to address error, misuse, fraud, and interference of top church officials. Consequently, this research investigates the following hypothesis:

H1. There is a positive relationship between Strategic leadership and Committee practices and Fraud prevention.

Staff ethical training and Fraud prevention

Employee fraud training is an essential measure to avoid fraudulent activities within an organization as a result of an employee’s behavior. Fraud can be common in the church, and employees must be well-taught and watchful in order to prevent fraudulent acts. Employees must understand their responsibilities within the context of internal control and how they are accountable for the work of others. According to Osiefuah & Gwekye (2013) and Davis & Harris (2020), one of the most effective ways to be proactive is to educate employees about internal control tasks. Employee training is vital as it increases employees’ knowledge and enables them to accomplish the organization’s vision and objective (Razak, 2021). To develop the essential and most successful training, an organization’s personnel must first understand the organization’s vulnerabilities.

According to the fraud triangle theory, if an organization has an opportunity for fraud, it will encourage personnel to commit fraud. If the organization is committed to fraud prevention, it will eliminate all opportunities for fraudulent activities. For instance, fraud in churches can take various forms; an employee must be aware of when they are in danger to protect the organization of which they are a member. Employees will benefit from training since they will know how they should conduct themselves inside an organization and what to look out for in fraudulent activities. A formal ethics training program delivers information on an organization’s ethical viewpoint. Seminars and other ethical training activities reinforce the organization’s behavioral standards and clarify the type of action the organization considers acceptable or unregulated. Suryandari et al., (2021) advised that training includes a discussion of fraud risk along with the types of fraud that can occur against the company, what actions can be implemented to deter fraudulent activity, and how fraud impacts the organization and its personnel.

Previous research has revealed that training personnel is critical for preventing fraud. Suryandari etal., (2022) contends that organizations require individuals with proper training, a strong ethical foundation, and an understanding of accountability. According to Priyanka et al., (2022), two efficacious strategies can be employed to prevent and detect instances of job-related fraud. These involve the implementation of internal controls, such as the provision of ethics and fraud training. Other scholars have argued that comprehensive training enables management and staff to prevent organizations from fraud (Herimamy, 2021; Tanui, Omare & Bitange, 2016). Verma, Mohapatra & Löwstedt (2016) believe that ethical training helps ensure that organizations make ethical decisions. According to Krishna & Garg (2022), the organization that recruits and trains devoted people has a chance to realize the vision and objective of the organization. According to Zietlow, Hankin, Seidner, and Timothy (2018), Jenssen (2018), and Maifizar, Marlina, Vonna, Damrus, and Abdullah (2020), ethical leadership is crucial for preventing fraud by educating, hiring, and retaining qualified and dedicated personnel. Kirby (2020) and Maduabuchi (2021) emphasized the importance of making clear what is expected of the employee through training. He continued by stating that organizations should provide training to ensure that staff is capable of meeting expectations. Inadequate training may make the prevention and detection of fraud more difficult. Said, Asry, Rafidi, Obaid, and Alam (2018) claim that insufficient fraud training or a deficiency of anti-fraud measures for staff increases the likelihood of fraud occurring in an organization. Nortey (2019) and Treadwell (2020) underlined the importance of training management and staff on fraud and how to prevent it by raising employee awareness. According to Kirby (2020), allowing inexperienced and unqualified church leaders, staff, and volunteers to conduct financial functions exposes the church to an elevated risk of fraud. Consequently, organizations may assist in restricting fraud chances by enhancing fraud awareness via training and cultivating an ethical organizational culture.

According to (Fernandhytia & Muslichah, 2020; Ghanem & Castelli, 2019; Peltier-Rivest, 2018) ethical training will enhance employees’ desire to behave in a manner that demonstrates accountability, which should lead to higher Fraud Prevention. Consequently, the following theory is put forward:

H2. There is a positive relationship between Staff ethical training and Fraud prevention.

Whistleblowing and Fraud Prevention

Scaturro (2018) defines whistleblowing as members of an organization disclosing unlawful, unethical, or inappropriate acts under their supervision to individuals or groups against whom they can effect change. Whistleblowing is the act of disclosing or reporting wrongdoings or unlawful behavior within an organization to people in positions of control or the general public (Ceva & Bocchiola, 2020; Khan, Saeed., Zada, Ali, Contreras-Barraza, Salazar-Sepúlveda & Vega-Muñoz, 2022). According to Mohamed-Isa, Razman, Latiff, Noor, Osman and Hj (2020), whistleblowing entails notifying persons in authority about wrongdoing, including financial fraud. According to the ACFE (2018) report, certain kinds of fraud and malpractices are discovered as a result of input from stakeholders or anonymous sources. Something that bolsters the concept of anonymous hotlines for reporting abuse to authorities. This means the whistleblower is not directly harmed by unethical conduct or misconduct.

Numerous studies and case studies suggest that whistleblowing systems can be beneficial in a variety of ways. A whistleblowing policy establishes standards for disclosing misconduct inside an organization (Scheetz & Fogarty, 2019). It contributes to developing an ethical culture and encourages transparency and trust (Rustiarini & Merawati, 2020). According to the ACFE (2018), Hasan, Saifunnajar, Azlina, Al Mansur & Saifullah, 2022; Krambia-Kapardis, 2020; Meitasir et al., 2022; Priyadi, Hanifah & Muchlish, 2022), whistleblowing is an effective method of combating fraud. Similar sentiments are argued by Atmadja, Saputra and Manurung (2019), Transparency International (2016), and Maulida and Bayunitri (2021), all claiming that organizations that use effective whistleblower systems may be able to discover fraud more easily, take remedial action, and avoid fraud-related expenses.

Putra, Rasmini, Gayatri, and Ratnadi (2022) contend that the implementation of an efficient system for whistleblowing will lead to a heightened level of community engagement and a greater propensity among organizational personnel to take action in order to prevent fraudulent activities by promptly reporting them to the relevant governing bodies. Whistleblowing can help shift the culture from secrecy toward honesty and transparency. According to Handayani and Kawedar (2021), the success of the whistleblowing policy may be measured by the number of identified frauds and the time required to take action, which is significantly less than that required by other approaches.

Putra et al., (2022); Shaddiq, Zulkarnain & Anggraini, (2023) and Oelrich (2021) have demonstrated that the whistleblowing system influences fraud prevention. Atmadja, Saputra and Manurung’s (2019) finding in Handayani and Kawedar (2021), on the other hand, reveals that the whistleblowing mechanism does not influence fraud prevention. Whistleblowing ends misconduct, fraud, or illegal activity early on, minimizing harm and cost. According to ACFE (Thornton, 2022), whistleblowing proves to be an effective method of preventing and identifying occupational fraud. Accordingly, this study explores the following hypothesis:

H3. There is a positive relationship between whistleblowing and fraud prevention.

Strategic leadership theory is concerned with the capacity of the leaders within an organization to define their future, devise plans, and persuade subordinates to execute them. The primary goal of strategic leadership theory is to comprehend the degree of impact that organizational leaders have and how the leaders affect organizational performance (Nurlina, 2022; Paais & Pattiruhu, 2020). Strategic leadership theory directs its attention toward achieving organizational triumph by means of envisioning a desired future state and cultivating a conducive environment that fosters the attainment of desired outcomes (Samimi, Cortes, Anderson & Herrmann, 2022). The presupposition of strategic leadership theory is that leaders’ efforts are visible in an organization’s performance and values (Irene, Kiptoo., Christine, Jeptoo, Sawe, 2022; William, Wakhisi, 2021) These findings are backed by Oreg and Berson (2019), who notices that strategic decisions made by senior managers have a direct influence on an organization’s success.

The primary emphasis of strategic leadership theory is on how executives influence overall performance via the formulation and implementation of organizational strategies (Bryson & George, 2020; Samimi, Cortes, Anderson & Herrmann, 2022; Walter, 2021). This argument was backed by Alblooshi, Shamsuzzaman, and Haridy, (2021), who said that the leaders’ vision, their personalities, and interaction with their subordinates are crucial facets of strategic leadership theory. According to Luciano, Nahrgang & Shropshire, 2020; Fuertes, Alfaro, Vargas, Gutierrez, Ternero & Sabattin, 2020), strategic leadership theory concerns how management in organizations may influence workers by clearly communicating the direction that the company is moving in, which then explains the performance of such enterprises. Strategic Leadership Theory emphasizes organizational executives, including senior management teams, who have total accountability for the organization (Luciano, Nahrgang & Shropshire, 2020; Samimi, Cortes, Anderson & Herrmann, 2022). The function of developing and outlining broad organizational goals is assumed by the executive (Yoon & Suh, 2019). Strategic Leadership Theory discusses the strategic leaders’ capacity to lead in a variety of circumstances by using and implementing various leadership styles with the goal of influencing individuals from all organizational levels (Abolade, Damilare & Lawal, 2022). This means that strategic leaders are capable of thinking through any circumstance and charting a course of action.

This research was confined to committee practices of effectively managing the church’s financial resources, emphasizing ethical practices, and whistle-blowing as a way of emphasizing organizational controls. Each of these parts of Strategic Leadership Theory was significant in this research since church leaders intend to decide their organizations’ strategic orientation via the formation of vision, mission, and core values. The strategic leadership theory was appropriate for this research due to the abilities of church leaders to effectively emphasize ethical practices, develop human capital, and establish organizational controls.

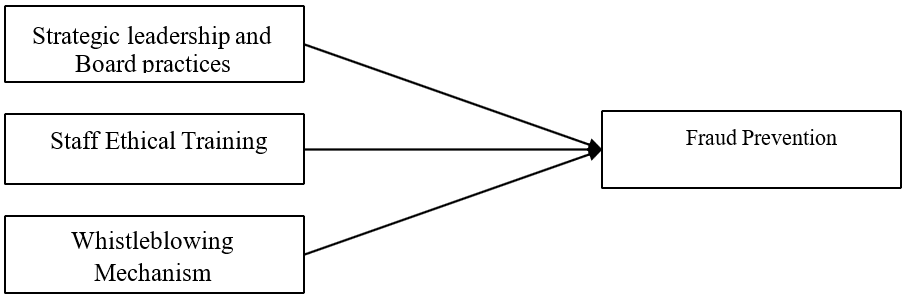

Conceptual Framework

This study is based on a framework concerning the impact of committee practices, staff ethical training, and whistleblowing on fraud prevention. The independent variable of the study is Strategic leadership and Committee practices, Staff ethical training, whistleblowing mechanisms, and fraud prevention as a dependent variable.

Figure 1. Conceptual Framework

Strategic Leadership: This encompasses the top-level decision-making and direction-setting within an organization. It includes aspects such as vision, goal-setting, resource allocation, and organizational culture.

Committee Practices: This refers to the practices and procedures followed by various committees within the organization, such as audit committees, compliance committees, or ethics committees. It includes aspects like meeting frequency, composition, independence, and effectiveness.

Staff Ethical Training: This involves training programs and initiatives aimed at instilling ethical values and promoting ethical behavior among the organization’s staff. It includes aspects like content, delivery methods, frequency, and effectiveness.

Whistleblowing Mechanisms: These are the channels and processes through which employees can report unethical or fraudulent behavior within the organization, either internally or externally. It includes aspects like accessibility, anonymity, protection for whistleblowers, and responsiveness.

Dependent Variable:

Fraud Prevention: This represents the effectiveness of the organization’s measures and strategies in detecting, preventing, and mitigating fraudulent activities. It includes aspects like the incidence of fraud, financial losses due to fraud, detection mechanisms, and overall organizational resilience to fraud.

Conceptual Relationships:

Strategic Leadership: Strong strategic leadership is expected to influence committee practices, staff ethical training, and the establishment of effective whistleblowing mechanisms. Leaders who prioritize ethical conduct are likely to create a culture that values transparency, accountability, and fraud prevention.

Committee Practices: Effective committee practices are expected to facilitate fraud prevention by ensuring robust oversight, risk assessment, and internal controls within the organization.

Staff Ethical Training: Comprehensive and effective ethical training programs are expected to enhance employees’ awareness of ethical standards and encourage ethical decision-making, thereby reducing the likelihood of engaging in fraudulent activities.

Whistleblowing Mechanisms: Well-established and accessible whistleblowing mechanisms provide employees with avenues to report suspected fraud or misconduct, thereby enabling early detection and prevention of fraudulent activities within the organization.

RESEARCH METHODOLOGY

This section deals with the methodology of the research. We will examine the study’s variables, sampling, data sources, and data analysis techniques.

Research Philosophy

The selection of suitable methodologies for this research was influenced by the positivist philosophy.

Research Design

The investigation employed a research design utilizing surveys and a quantitative methodology to examine the association among variables and verify hypotheses.

Study and target population

The research population consisted of all twelve church leaders from the six dioceses of the Church of the Province of Uganda in central Uganda.

Population, Sampling, and data collection

The initial step in conducting research, as stated by MacMillan and Schumacher (2001), involves the identification and delineation of the population that will be examined, taking into account its geographic, demographic, and other parameters. This analysis is vital for determining whether the entire population or only a portion of it should be encompassed. Consequently, when referring to a research population or target population, one indicates the specific group from which the researcher intends to gather data and derive conclusions (Hennink, Hutter, & Bailey, 2020). The population of this research consisted of 12 church leaders from the six churches of the Province of Uganda dioceses in central Uganda who had the authority and expertise to manage the institutional resources, emphasizing ethical practices, and establishing organizational financial controls. There were six diocesan secretaries and six diocesan treasurers from the Church of Uganda’s six dioceses in central Uganda.

Sampling

This study undertook purposeful sampling in order to characterize the sample of the research being considered. The selection of individuals for the sample was predicated upon their expertise, connections, and research acumen, utilizing this technique (Frey, 2000). To facilitate the researcher’s selection of participants with a distinct association with the phenomenon under investigation, as well as substantial and pertinent professional background in financial management, and active engagement in church activities and ministry, this study implemented a non-probability purposive sampling strategy. The objective of this approach was to fulfill the goals of the analysis and address the research inquiries.

Sampling techniques, and sample size

The sample was obtained through the implementation of a purposive sampling technique that took into account specific factors. The respondents who participated in this study were selected depending on their positions as Church administrators, specifically, Diocesan secretaries and Diocesan treasurers. These individuals were directly engaged in the management of resources, financial planning, the promotion of ethical practices, and the establishment of controls within the dioceses.

Types of data, sources, and collection instruments

The data was obtained through the means of field research, whereby the subject of the study was visited in the dioceses and a questionnaire was distributed. Respondents contributed primary data by filling out a questionnaire that had a series of questions. The questionnaires were personally handed to the respondents during the period from April to August 2022. The questionnaire was divided into four sections: demographic information, Committee practices, strategic leadership, Staff ethical training, and whistleblowing policy.

The respondents were probed about Strategic leadership and Committee practices, which encompass the responsibility of the organization’s leadership in developing, directing, and supporting the organization’s integrity and ethical activities. It addresses the accountability of leaders and managers for fostering ethics and integrity. This category assesses the “Tone from the Top” of the organization at both the senior executive and governance levels.

In the case of Staff ethical training, respondents were questioned about, the availability of regular training on fraud prevention, leaders being encouraged to be honest, Training raising awareness of fraud, Training for employees involved in fraud control activities, Training helping management to raise ethical decisions, and Ethical training enhanced employees’ desire to behave in a way that demonstrates accountability, Church employees are familiar with the church standards regarding the proper use of the church’s resources.

Finally, the respondents were probed about the whistleblowing policy that investigates how the church encourages employees (both internal and external to the church) to speak out and report dubious behavior. This category examines the techniques and protections provided to anyone who seeks to alert an organization to suspected unethical behavior, misbehavior, or unlawful activities. It encompasses both anonymous and confidential reporting, as well as the methods utilized by churches to protect whistleblowers from reprisal.

Data analysis

The methodology employed in this study involved utilizing the IBM SPSS Statistics 20 software for data analysis. The analysis of questionnaire data encompassed descriptive statistics, assessments of data quality and assumptions, as well as hypothesis testing (Ghozali, 2013). Assessing data quality aimed at establishing the validity and reliability of the questionnaire. The software facilitated the generation of tables presenting the study results. Regarding data analysis, the research utilized percentages, correlation, and regression analysis to investigate the impact of Strategic leadership and Committee practices, ethics training, and whistleblowing on Fraud Prevention within the Church of Uganda context. The findings of this study’s testing of hypotheses by linear regression analysis are shown in Table 11.

RESULTS AND FINDINGS

Research results

This section of the research provides an assessment of the key findings made during the investigations into the influence of Strategic leadership and Committee practices, ethics training, and whistleblowing on Fraud Prevention in the instance of the Church of Uganda. The various analyses conducted were subjected to meticulous evaluation and conveyed with the assistance of accompanying tables. The responses obtained from the questionnaires, along with the subsequent analysis and discussion, are outlined below:

Reliability

Table 1: Reliability Test results

| Construct | Cronbach’s Alpha Values | Number of Items |

| Fraud Prevention | 0.726 | 4 |

| Strategic leadership and Committee practices | 0.743 | 7 |

| Staff Ethics Training | 0.720 | 7 |

| Whistleblowing Mechanisms | 0.781 | 10 |

The reliability test demonstrates that Cronbach’s alpha spans from 0.720 to 0.781. These results suggest values exceeding 0.7. These findings ascertain the reliability of the study questionnaire.

Typically, a Cronbach’s alpha value of 0.5 and above is considered acceptable, although the threshold for acceptability may vary depending on the context and the specific scale being assessed.

If Cronbach’s alpha is 0.5 or above, it suggests that the items in the scale are moderately to highly correlated with each other, indicating a relatively good level of internal consistency. This means that the items are measuring a similar construct or concept consistently across the scale. Researchers often aim for Cronbach’s alpha values of 0.7 or higher for scales used in research studies, as this indicates a higher degree of internal consistency and reliability.

Table 3 Participants’ Description

| Gender | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Male | 11 | 91.7 | 91.7 | 91.7 |

| Female | 1 | 8.3 | 8.3 | 100.0 | |

| Total | 12 | 100.0 | 100.0 | ||

Source: Field data 2022

Twelve persons in positions of leadership from the six churches of the Province of Uganda dioceses in central Uganda took part in this research endeavor. Out of the twelve respondents, eleven (92%) were of the male gender, with the remaining one (2%) being female.

Table 4 Participants’ age group

| Age group | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | 31-40 | 3 | 25.0 | 25.0 | 25.0 |

| 41-50 | 2 | 16.7 | 16.7 | 41.7 | |

| 51 – 60 | 5 | 41.7 | 41.7 | 83.3 | |

| 61 and above | 2 | 16.7 | 16.7 | 100 | |

| Total | 12 | 100 | 100 | ||

Source: Field data 2022

According to the data presented in the table, individuals between the ages of 31 and 40 account for 25% of the population, while those aged 41 to 50 make up 16% of the population. Additionally, individuals aged 51 to 60 represent 42% of the population, with those aged 61 and above comprising 17% of the population

Table 5 Educational Attainment

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | Diploma | 1 | 8.3 | 8.3 | 8.3 |

| Bachelor’s Degree | 5 | 41.7 | 41.7 | 50.0 | |

| Master’s Degree | 6 | 50.0 | 50.0 | 100 | |

| Total | 12 | 100.0 | 100 | ||

Source: Field data 2022

According to the table mentioned above, the educational background of the respondents spans from a diploma to a master’s degree. The data reveals that 8% of the respondents possess a diploma, while 42% hold a bachelor’s degree, and the remaining 50% hold a master’s degree.

While the majority hold master’s degrees, there’s a smaller representation of individuals with diplomas. This suggests a potentially higher level of expertise among respondents but may limit generalizability to individuals with lower levels of formal education or experience

Table 6 Number of Years in the Position or Department

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | 5-8 | 7 | 58.3 | 58.3 | 58.3 |

| 9-12 | 3 | 25.0 | 25.0 | 83.3 | |

| 13-16 | 1 | 8.3 | 8.3 | 91.7 | |

| 16 and above | 1 | 8.3 | 8.3 | 100 | |

| Total | 12 | 100.0 | 100 | ||

Source: Field data 2022

Additionally, the leaders’ work experience was taken into account. There were seven responses (58%) with 5-8 years of service. The proportion of responders with 9-12 years of service was 3 (25%). There were one or 8% of responders with 13-16 years of experience. Finally, one (8%) of the participants had more than 16 years of service.

Descriptive statistics for Fraud Prevention

The dependent variable in this study was fraud prevention, which was assessed using a five-point Likert scale. The constructs that measured the variable were whether the church lowered situational pressure, the church decreased perceived opportunities, the church reinforced employees’ personal integrity, and the church Enhanced internal controls.

Table 7 statistics show that the majority of respondents believed that the Church alleviated situational pressure, with a maximum mean score of 5 and a standard deviation of 1.348. This was followed by the church’s reduced perceived opportunities (mean score of 3.00, standard deviation of 1.279). The study also found that the Church improved employees’ personal integrity, with a mean score of 2.92 and a standard deviation of 1.165. The church’s strengthening of internal controls had a mean value of 2.75 and a standard deviation of 0.965.

The overall findings, with a mean score of 2.92 and a standard deviation of 0.888, show that the majority of participants believe that fraud is adequately reduced in the Church of the Province of Uganda dioceses in central Uganda.

Table 7: Mean and Standard Deviation for Fraud Prevention

| Mean | Std. Deviation | |

| The Church reduced situational pressure | 3.00 | 1.348 |

| The church reduced perceived opportunities | 3.00 | 1.279 |

| The Church strengthened employees’ personal integrity | 2.92 | 1.165 |

| The church strengthened internal controls | 2.75 | 0.965 |

| Overall | 2.92 | 0.888 |

Descriptive statistics for Strategic leadership and Committee practices

The constructs that measured the variable were, The committee contains individuals with various skills, The committee exhibits teamwork, committee members understand their fiduciary responsibility to churches, The committee endeavors to increase its members’ understanding of their role, committee members keep each other accountable, The church is committed to hiring competent and committed staff

Church leaders are familiar with the church’s standing regarding the proper use of the church’s resources.

Table 8 shows that most of the participants felt that the committee contained individuals will various skill sets and had the highest mean score of 3.75 and a mean score of 1.422. This was followed by the committee exhibiting teamwork with a mean value of 3.75 and a standard deviation of 1.288. Committee members keeping each other accountable showed a mean score of 3.67 and a standard deviation of 1.435. In this study, the church is committed to hiring competent and committed staff as revealed with a mean of 3.58, and the committee endeavoring to increase its member’s understanding of their role with a mean score of 3.50 and a standard deviation of 1.446 followed by a standard deviation of 1.443.This. Committee members’ understanding of their fiduciary responsibility to churches showed a mean value of 3.42 and a standard deviation of 1.379 which is categorized as effective. Concerning the Church leader’s familiarity with the church’s standing regarding the proper use of the church’s resources had the lowest mean score of 2.92 and a standard deviation of 1.165.

The general findings with a mean score of 3.51 and a standard deviation of 0.860 reveal that the greatest number of the participants agree that the Strategic leadership and Committee practices moderately influence Fraud prevention in the Church of the Province of Uganda dioceses in central Uganda.

Table 8: Mean and Standard Deviation for Strategic leadership and Committee practices

| Mean | Std. Deviation | |

| The committee contains individuals with various skill | 3.75 | 1.422 |

| The committee exhibits teamwork | 3.75 | 1.288 |

| committee members understand their fiduciary responsibility to churches | 3.42 | 1.379 |

| committee endeavors to increase its members’ understanding of their role | 3.50 | 1.446 |

| committee members keep each other accountable | 3.67 | 1.435 |

| The church is committed to hiring competent and committed staff | 3.58 | 1.443 |

| Church leaders are familiar with the church’s standing regarding the proper use of the church’s resources | 2.92 | 1.165 |

| Overall | 3.51 | 0.860 |

Descriptive statistics for Staff ethical training

The constructs which measured the variable were, the availability of regular training on fraud prevention, leaders being encouraged to be honest, Training raising awareness of fraud, Training for employees involved in fraud control activities, Training helping management to raise ethical decisions, and Ethical training enhanced employees’ desire to behave in a way that demonstrates accountability, Church employees are familiar with the church standards regarding the proper use of the church’s resources.

Table 9 statistics show that the greatest number of the participants felt that Training raised awareness of fraud and had the highest mean score of 3.75 and a standard deviation of 1.288. This was followed by Training help management to raise ethical decisions with a mean value of 3.58 and a standard deviation of 1.443. In this study, there is regular training on fraud prevention with a mean value of 3.42 and a standard deviation of 1.379. On whether Training employees were involved in fraud control activities the study revealed a mean score of 3.42 and a standard deviation of 1.311. According to this study, leaders were encouraged to be honest with a mean value of 3.08 and a standard deviation of 1.379. Concerning whether Church employees are familiar with the church standards regarding the proper use of the church’s resources the study reveals a mean value of 3.00 with a standard deviation of 1.348. Ethical training enhanced employees’ desire to behave in a way that demonstrates accountability indicating the lowest mean value of 2.92 and a standard deviation of 1.165.

The overall findings with a mean score of 3.31 and a standard deviation of 0.815 suggest that the greatest number of the participants believe that the application of staff ethical training prevents fraud in the Church of the Province of Uganda dioceses in central Uganda.

Table 9: Mean and Standard Deviation for Ethical Training

| Mean | Std. Deviation | |

| There is regular training on fraud prevention | 3.42 | 1.379 |

| Leaders were encouraged to be honest | 3.08 | 1.379 |

| Training raised awareness of fraud | 3.75 | 1.288 |

| Training to employees involved in fraud control activities | 3.42 | 1.311 |

| Training helps management to raise ethical decisions | 3.58 | 1.443 |

| Ethical training enhanced employees’ desire to behave in a way that demonstrates accountability | 2.92 | 1.165 |

| Church employees are familiar with the church standards regarding the proper use of the church’s resources | 3.00 | 1.348 |

| Overall | 3.31 | 0.815 |

Descriptive statistics for Whistleblowing Mechanisms

The constructs that measured the variable were, The church recognizes the need to implement a whistleblower mechanism to avoid fraud, Church leaders lead the whistleblower system implementation policy, Church leaders explain whistleblower protection to workers, Churches protect whistleblowers from administrative penalties, The whistleblower mechanism is frequently evaluated, The church management encourage communicating to employees about behaviors that are not acceptable and to report them, Treasury has installed suggestion boxes to collect sensitive and secret information for efficient administration., There is a procedure for responding to the whistleblower, The church’s audit committee oversees the church’s whistle-blowing mechanism, and employees may easily file violation complaints.

Table 10 statistics show that the greatest number of the participants felt that the whistleblower mechanism is frequently evaluated and had the highest mean score of 3.750 and a standard deviation of 1.422. A standard deviation of 1.422 indicates the average deviation of individual responses from the mean score of 3.750 for the evaluation frequency of the whistleblower mechanism. Essentially, it reflects the extent to which participants’ perceptions vary from the average perception of the group. In this study, it suggests that while the majority of participants perceive the evaluation frequency as relatively high, there is variability in individual opinions, with some participants perceiving it differently.

This was followed by whether the Treasury has installed suggestion boxes to collect sensitive and secret information for efficient administration with a mean value of 3.750 and a standard deviation of 1.288. The church’s audit committee overseeing the church’s whistle-blowing mechanism revealed a mean score of 3.667 with a standard deviation of 1.371. Church leaders leading the whistleblower system implementation policy with a mean value of 3.583 and a standard deviation of 1.443 followed this. In this study, employees finding it easy to file violation complaints indicated a mean value of 3.583 with a standard deviation of 1.443. Regarding whether the church recognizes the need to implement a whistleblower mechanism to avoid fraud, the study revealed a mean value of 3.500 and a standard deviation of 1.446. The Churches protecting whistleblowers from administrative penalties showed a mean value of 3.417 and a standard deviation of 1.311 followed this. The study participants agreed that there is a procedure for responding to a whistleblower with a mean score of 3.417 and a standard deviation of 1.379. Moreover, the church management encouraged communicating with employees about behaviors that are not acceptable and reporting them indicated a mean score of 3.250 and a standard deviation of 1.422. Regarding whether Church leaders explain, whistleblower protection to workers indicated a mean score of 2.917 and a standard deviation of 1.165. This shows that the church is able to protect its whistleblowers.

The overall findings with a mean score of 3.48 and a standard deviation of 0.796 suggest that the greatest number of the participants believe that the application of the whistleblowing systems satisfactorily affects fraud prevention in the Church of the Province of Uganda dioceses in central Uganda.

Table 10: Mean and Standard Deviation for Whistleblowing Mechanism

| Mean | Std. Deviation | |

| The church recognizes the need to implement a whistleblower mechanism to avoid fraud. | 3.500 | 1.446 |

| Church leaders lead the whistleblower system implementation policy. | 3.583 | 1.443 |

| Church leaders explain whistleblower protection to workers. | 2.917 | 1.165 |

| Churches protect whistleblowers from administrative penalties. | 3.417 | 1.311 |

| The whistleblower mechanism is frequently evaluated. | 3.750 | 1.422 |

| The church management encourages communicating with employees about behaviors that are not acceptable and reporting them | 3.250 | 1.422 |

| Treasury has installed suggestion boxes to collect sensitive and secret information for efficient administration. | 3.750 | 1.288 |

| There is a procedure for responding to whistleblower | 3.417 | 1.379 |

| The church’s audit committee oversees the church’s whistle-blowing mechanism | 3.667 | 1.371 |

| Employees may easily file violation complaints. | 3.583 | 1.443 |

| Overall | 3.48 | 0.796 |

Correlation investigates the linear link between two variables (Coakes et al., 2008). This technique allows us to determine if two variables are connected. Before evaluating the approach, a correlation study is conducted to determine the link between Committee practices, strategic leadership, Staff ethical training, as well as whistleblowing mechanisms in the church of Ugandan. A Pearson correlation test is performed to determine if there are multicollinearity issues among the variables in this research. The two variables are strongly correlated and explain the dependent variable, which will generate a multicollinearity issue if the coefficient values are 0.80 or 0.90, or higher (Field, 2000). The findings of a bivariate analysis undertaken to determine the correlation between two variables are summarized in Table 11.

Table 11: Correlation Analysis

| Fraud Prevention | Strategic leadership and Committee practices | Staff ethical training | Whistleblowing Mechanism | |

| Fraud Prevention | 1 | |||

| Strategic leadership and Committee practices | .656* | 1 | ||

| Staff ethical training | .748** | .728** | 1 | |

| Whistleblowing Mechanisms | .679* | .916** | .857** | 1 |

*. Correlation is significant at the 0.05 level (2-tailed).

**. Correlation is significant at the 0.01 level (2-tailed).

According to the statistical findings, the correlation values between the variables vary between 0.685 and 0.857. Since the correlation exceeds 0.80, this suggests that there is a multicollinearity issue among the variables. Fraud Prevention is crucial in Strategic leadership, Staff ethical training, and the Whistleblowing system.

In the meanwhile, Leadership is essential to, Staff ethical training, and whistleblowing. However, Staff ethical training and whistleblowing have mutual significance. In terms of the association between Strategic leadership and Committee practices, ethics training, and whistleblowing dimension and Fraud Prevention, the findings reveal that there is a substantial relationship between strategic leadership, ethical training, and whistleblowing.

However, this research showed a statistically significant correlation between church leadership and Fraud Prevention, indicating that church leadership in Uganda has an effect on church Fraud Prevention. This conclusion aligns with prior research by Wang, Yu & Gao, (2022), which revealed that leadership might have a good relationship with the Fraud Prevention system. Consequently, H1 is supported.

In addition, this research discovered a substantial correlation between Staff ethical training and the Fraud Prevention results of Ugandan churches. Therefore, H2 is supported since there is a good correlation between the ethical training offered to church personnel and their Fraud Prevention. This is consistent with (Atmadja, Saputra & Manurung, 2019; Fish, Self, Sargsyan & McCullough, 2021; Suryandari et al., (2021) findings, which they all agreed that ethical teaching and enforcement might lead to an increase in fraud prevention.

The research indicated a substantial favorable correlation between whistleblowing policy and the Fraud Prevention of Ugandan churches. This is also similar to the findings of (Maulida & Bayunitri, 2021), who argued that whistleblowing might alter an organization’s Fraud Prevention. Therefore, the premise that there is a positive association between whistleblowing and Fraud prevention is validated, and the presence of reporting rules such as whistleblowing may influence the view.

Regression analysis

The hypotheses in this study were examined using regression analysis, and the results are presented in the tables 12 -14 below.

Model Summary

Table 12 presented in the subsequent section provides a concise overview of the regression model analysis pertaining to the correlation between Fraud Prevention and the predictor variables, namely Strategic Leadership and Committee Practices, Staff Ethics Training, and Whistleblowing Mechanisms. In line with the results, it can be observed that the R-coefficient stands at 0.774, signifying a substantial positive relationship between the predictor variable and Fraud Prevention within the central diocese of the Church of the Province of Uganda.

The R-value denotes a robust and statistically significant correlation between the variables. The R-Square value of 0.598 signifies that the independent variables explain 59.8% of the variation in the dependent variable, with the remaining 40.2% accounted for by the error term. This indicates a well-fitting model. Consequently, it is apparent from this discovery that, all else being equal, Strategic leadership and Committee practices, ethics training, and whistleblowing contribute to 77.4% of the church’s Fraud Prevention.

Table 12: Model Summary

| Model | R | R Square | Adjusted R Square | Std. Error of the Estimate |

| 1 | .774a | .598 | .448 | .65953 |

| a. Predictors: (Constant), Whistleblowing Mechanisms, Strategic leadership and Committee practices, Staff Ethics Training | ||||

The Anova

The Anova findings demonstrate that the regression model as a whole possesses significance for the data, which is evident from the Anova (F-statistic) value of 3.975 and the corresponding value of .053. Both values were determined to be significant at the 5% level. The results, therefore, highlight that the model is statistically significant hence; the Strategic leadership and Committee practices, ethics training, and whistleblowing strongly contribute to positive Fraud prevention for Churches.

Table 13: ANOVA

| ANOVAa | ||||||

| Model | Sum of Squares | df | Mean Square | F | Sig. | |

| 1 | Regression | 5.187 | 3 | 1.729 | 3.975 | .053b |

| Residual | 3.480 | 8 | .435 | |||

| Total | 8.667 | 11 | ||||

- Dependent Variable: Fraud Prevention

- Predictors: (Constant), Whistleblowing Mechanisms, Strategic leadership and Committee practices, Staff Ethics Training

Multiple regression analysis

The researcher performed a multiple regression analysis to determine the impact of the independent variables (the Strategic leadership and Committee practices, ethics training, and whistleblowing Mechanisms) on Fraud prevention in Churches. The results are presented in the table below.

Table 14: Coefficients

| Coefficients | ||||||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | .045 | .902 | .050 | .962 | |

| Strategic leadership and Committee practices | .486 | .600 | .471 | .811 | .441 | |

| Staff ethical training | .794 | .494 | .729 | 1.608 | .147 | |

| Whistleblowing Mechanisms | -.421 | .864 | -.377 | -.487 | .639 | |

| a. Dependent Variable: Fraud Prevention | ||||||

Multiple regression analysis and Coefficient

The model

Y = B0+ B1X1+ B2X2+ B3X3+ E is used. Whereby:

Y = dependent variable (Fraud Prevention)

Bo = Regression’s constant

Bi = (i= 0, 1, 2, 3…n) = regression coefficients for each dependent variable

X1= Strategic leadership and Committee practices

X2= Staff ethical training

X3 = Whistleblowing Mechanisms

E= the model error variable

Assumption:

The multiple regression model assumes that the dependent variable has a normal distribution for each given value of the independent variable and that the dependent variable’s variances are consistent across all independent variables. The results, therefore, suggested that the model is statistically significant; hence, strategic leadership and committee practices, ethical training, and whistleblowing greatly contribute to beneficial fraud prevention for churches.

Substituting in the equation

Y= 0.45 + 0.486 x1 + 0.794 x2 + 0.421 x3

Based on the results of the multiple regression equation, each of the variables explains that:

- The regression equation shows that the constant value is 0.45, and the positive signs indicate the use of Strategic leadership and Committee practices (X1), Staff ethical training (X2), and Whistleblowing Mechanisms (X3) as constant factors in managing church finances for Fraud Prevention.

- The regression coefficient for Strategic leadership and Committee practices is 0.486 and has a positive sign, indicating that an increase in the value of Strategic leadership and Committee practices will result in a corresponding increase in church Fraud Prevention by 0.486, assuming other variables remain constant. Therefore, there is a positive relationship between Strategic leadership and Committee practices and Fraud Prevention in church finances. Consequently, H1 is supported, and Strategic leadership and Committee practices are associated with church Fraud Prevention.

- The regression coefficient for Staff ethical training is 0.794 and has a positive sign, indicating that an increase in the value of Staff ethical training will result in a corresponding increase in church Fraud Prevention by 0.794, assuming other variables remain constant. Therefore, there is a positive relationship between Staff ethical training and Fraud Prevention in church finances. Consequently, H2 is supported, and Staff ethical training is associated with church Fraud Prevention.

- The regression coefficient for the whistleblowing mechanism is 0.421 and has a positive sign, indicating that an increase in the value of the whistleblowing mechanism will result in a corresponding increase in church Fraud Prevention by 0.421, assuming other free variables remain constant. Therefore, there is a positive relationship between the whistleblowing mechanism and Fraud Prevention in church finances. Consequently, H3 is supported, and the whistleblowing mechanism is associated with Fraud Prevention.

DISCUSSION

The effect of Strategic leadership and Committee practices on Fraud Prevention

The first hypothesis was that there is a positive relationship between Strategic leadership and Committee practices and Fraud prevention. Table 14 shows that the coefficient of Strategic leadership and Committee practices is 0.486 with a p-value of 0.000. Since the p-value is less than 0.005, the hypothesis is supported by the research findings. The finding of testing the hypothesis indicated that Strategic leadership and Committee practices influence fraud prevention.

This research confirms (Gianotti & Damião da Silva’s, 2021; Maulida & Bayunitri, 2021; Ocansey & Ganu, 2017) study showing that Strategic leadership influences fraud prevention. The outcome conflicted with the findings of Gakhar & Mulla, (2021), who discovered that ethical leaders have a significant impact on molding the morale and Fraud Prevention of workers, both favorably and adversely.

The Effect of Ethical Training on Fraud Prevention

The second hypothesis posited a positive relationship between staff ethical training and fraud prevention. Table 14 presents the coefficient of staff ethical training as 0.459, accompanied by a p-value of 0.000. Since the p-value is less than 0.005, the research findings support the hypothesis. The results of the hypothesis testing affirm that Staff ethical training significantly influences Fraud prevention. This finding aligns with previous research conducted by Herimamy (2021), Tanui, Omare, and Bitange (2016); Verma, Mohapatra, and Löwstedt (2016), all of whom have demonstrated the impact of Ethical Training on Fraud prevention.

The Effect of Whistleblowing Mechanism on Fraud Prevention

The third hypothesis posited that there exists a positive relationship between whistleblowing mechanisms and fraud prevention. Table 14 presents the coefficient of the whistleblowing mechanism as 0.718, with a p-value of 0.000. Since the p-value is less than 0.005, the research findings support the hypothesis. The results of hypothesis testing indicate that the whistleblowing mechanism has an influence on fraud prevention. This study corroborates previous findings by Meitasir, Bella Chenia, Agrianti Komalasari (2022) that demonstrate the influence of the Whistleblowing Mechanism on Fraud prevention.

The study’s findings are also congruent with those of Sharma, (2022), who stated that an organization would react successfully if it had reporting rules in place. This is due to the fact that churches are mission-driven and tightly tied to public image. Even if the employee does not blow the whistle, ethical difficulties may still occur. Because whistleblowing reflects a contradiction between the employee’s allegiance to the business and the employee’s legal duty to disclose potentially fraudulent acts to the appropriate authorities, some institutions may consider the whistleblower a traitor (Uys & Uys, 2022). On the other side, others may see the whistleblower as a valiant protector (Alam & Khalid, (2021; Barde, 2021). In the instance of the church, if an employee remains quiet while knowing that anything unethical is occurring inside the church, he or she is regarded as unethical by the faithful of the society. Churches should thus promote the whistleblowing practice.

CONCLUSIONS

Strategic leadership and Committee practices on Fraud Prevention

The study concluded that Strategic leadership and Committee practices influence Fraud prevention.

Staff ethical training on Fraud Prevention

The study concluded that Staff ethical training influences Fraud prevention in the church of Uganda dioceses in central Uganda.

Whistleblowing Mechanism on Fraud Prevention

The study concluded that the Whistleblowing Mechanism influences Fraud prevention in the church of Uganda dioceses in central Uganda.

RECOMMENDATION

In order for Churches to demonstrate increased levels of fraud prevention, it is necessary that they implement aspects of Strategic leadership and Committee practices, ethics training, and whistleblowing. Particularly Church of Uganda should train its staff in organization ethics to abate fraud propensities. Church leaders should also explain whistleblower protection to workers. Moreover, church leaders should familiarize themselves with the church’s standing regarding proper procedures for using church resources.

BIBLIOGRAPHY

- Abolade, A. P., Damilare, A. E., & Lawal, I. O. (2022). Thematic Exploration of Strategic Leadership and Organizational Performance in National Information Technology Development Agency. KIU Interdisciplinary Journal of Humanities and Social Sciences, 3(2), 472-498.

- Aine, Donovan. (2022). Strategic Leadership as a Tool for Growth, Mission Alignment and Long-term Stability in advance. Teaching Ethics, doi: 10.5840/tej2022330112

- Akotia, Y. A. (2019). Financial management of churches in Ghana: A case study of Legon Interdenominational Church.

- Alam, H. S. N., & Khalid, R. (2021). Whistleblowing for better environmental protection in Malaysian society. In The Role of Law in Governing Sustainability (pp. 237-248). Routledge.

- Alblooshi, M., Shamsuzzaman, M., & Haridy, S. (2021). The relationship between leadership styles and organizational innovation: A systematic literature review and narrative synthesis. European Journal of Innovation Management, 24(2), 338-370.

- Alzola, M. A., & Arkan, Ö. (2021). Whistleblowing in the Catholic Church: The Role of Wrongdoing Characteristics and Ethical Climate. In Academy of Management Proceedings (Vol. 2021, No. 1, p. 16259). Briarcliff Manor, NY 10510: Academy of Management.

- Asea, W. B. (2018). Combating political and bureaucratic corruption in Uganda: Colossal challenges for the church and the citizens. HTS Teologiese Studies/Theological Studies, 74(2).

- Atmadja, A. T., Adi Kurniawan Saputra, K., & Manurung, D. T. H. (2019). Proactive Fraud Audit, Whistleblowing, and Cultural Implementation of Tri Hita Karana for Fraud Prevention. European Research Studies Journal, XXII(3), 201–214.

- Bainbridge, S. M. (2021). Restoring Confidence in the Roman Catholic Church: Corporate Governance Analogies. Public Law Research Paper, (18-32).

- Bakri, H. H. M., Mohamed, N., & Said, J. (2017). Mitigating asset misappropriation through integrity and fraud risk elements: Evidence emerging economies. Journal of Financial Crime, 24(2), 242–255. https://doi.org/10.1108/JFC-04-2016-0024

- Balfour, W. T. (2020). The inability of Leaders of Religious Not-For-Profit Organizations in New Jersey to Identify and Implement Adequate Internal Accounting Controls to Detect and Deter Accounting Fraud.

- Balfour, W., Sullivan, G., Self, S., & Byers, R. (2021). Detecting and Deterring Not-for-Profit Organization Accounting Fraud. Journal of Accounting and Finance, 21(4), 50–74. https://doi.org/10.33423/jaf.v21i4.4525

- Barde, P. V. (2021). Whistleblowing Mechanism: A Positive Step towards Enhancing Corporate Governance. Issue 1 Int’l JL Mgmt. & Human., 4, 1613.

- Bayar, S. (2018). Examining the role of the internal control system, church leaders’ accountability, and transparency on donors’ trust. April.

- Bingi, H. (2022). Internal audit practices and quality of financial reporting in selected Catholic Church Organizations in Kampala, Uganda (Doctoral dissertation, Kampala International University, College of Economics and Management).

- Brown, L. V. (2018). Ministry and nonprofit finance: A guide to promote awareness, stewardship, and compliance. Liberty University.

- Bryson, J. M. (2018). Strategic planning for public and nonprofit organizations: A guide to strengthening and sustaining organizational achievement. John Wiley & Sons.

- Bryson, J., & George, B. (2020). Strategic management in public administration. In Oxford Research Encyclopedia of Politics.

- Bryson, J., & George, B. (2020). Strategic management in public administration. In Oxford Research Encyclopedia of Politics.

- Ceva, E., & Bocchiola, M. (2020). Theories of whistleblowing. Philosophy Compass, 15(1), e12642.

- Davis, M. V, & Harris, D. (2020a). Strategies to Prevent and Detect Occupational Fraud in Small Retail Businesses. International Journal of Applied Management and Technology, 19(1), 40–61. https://doi.org/10.5590/ijamt.2020.19.1.04

- Decker, A., Oppong, M., Abedana, V. N., & Ibrahim, S. (2019). Curbing Fraudulent Practices through Accountability in Non-Profit Making Organizations Related papers Curbing Fraudulent Practices through Accountability in. Research Journal of Finance and Accounting, 10(14), 1–10. https://doi.org/10.7176/RJFA

- Deming, J. D. (2022). Exploring Strategy Planning and Execution Methods in Church Missions Programs.

- Fernandhytia, F., & Muslichah, M. (2020). The Effect of Internal Control, Individual Morality and Ethical Value on Accounting Fraud Tendency. Media Ekonomi Dan Manajemen, 35(1), 112. https://doi.org/10.24856/mem.v35i1.1343

- Fish, G. P., Self, S. W., Sargsyan, G., & McCullough, T. (2021). Preparation to prevent, detect, and manage fraud: A study of not-for-profits in south-central Pennsylvania. Journal of Leadership, Accountability, and Ethics, 18(2), 43-55.

- Fuertes, G., Alfaro, M., Vargas, M., Gutierrez, S., Ternero, R., & Sabattin, J. (2020). A conceptual framework for the strategic management: a literature review—descriptive. Journal of Engineering, 2020, 1-21.

- Gakhar, M., & Mulla, Z. R. (2021). Whistleblowing and the ‘Person-Situation’conundrum: what matters more? Journal of Human Values, 27(3), 247-260.

- Ghanem, K., & Castelli, P. (2019). Accountability and Moral Competence Promote Ethical Leadership. Journal of Values-Based Leadership, 12(1). https://doi.org/10.22543/0733.121.1247

- Glory, G. M., Lazaro, A. M., & Alexis, N. (2022). Effectiveness of fraud prevention and detection methods in the public sector in Tanzania. Journal of Accounting and Taxation, 14(1), 30–36. https://doi.org/10.5897/jat2021.0496

- Handayani, S., & Kawedar, W. (2021). Could the minimization of opportunity prevent fraud? An empirical study in the auditors’ perspective. Accounting, 7(5), 1157–1166. https://doi.org/10.5267/j.ac.2021.2.023

- Hasan, Z., Saifunnajar, S., Azlina, N., Al Mansur, M., & Saifullah, S. (2022). Implementation of Whistleblowing System to Prevent Sharia Banking Crime in Indonesia. Azka International Journal of Zakat & Social Finance, 32-52.

- Herimamy, R. (2021). Determinants of the Internal Control Effectiveness of Selected Seventh-day Adventist Church Entities in Madagascar. 2(2).

- Hoppmann, J., Naegele, F., & Girod, B. (2019). committees as a source of inertia: Examining the internal challenges and dynamics of committees of directors in times of environmental discontinuities. Academy of Management Journal, 62(2), 437-468.

- Irene, Kiptoo., Christine, Jeptoo, Sawe. (2022). Strategic Leadership Practices on Organizational Performance: A Case Study of Kenya Ports Authority. Asian Journal of economics, business, and accounting, doi: 10.9734/ajeba/2022/v22i730576

- Jachi, M. (2019). The Impact of Professional Competence & Staffing of Internal Audit Function on Transparency and Accountability Case of Zimbabwe Local Authorities. 10(8), 149–164. https://doi.org/10.7176/RJFA

- Jenssen, J. I. (2018). Leadership and church identity A discussion of how leadership in the local church can help to realize the true nature of the church. Norwegian School of Economics, University of Agder and Norwegian School of Leadership and Theology, 5, 1–24.

- Kabeyi, M. J. (2018). Ethical and unethical leadership issues, cases, and dilemmas with case studies. International Journal of Applied Research, 4(7), 373–379. https://doi.org/10.22271/allresearch.2018.v4.i7f.5153

- Khan, J., Saeed, I., Zada, M., Ali, A., Contreras-Barraza, N., Salazar-Sepúlveda, G., & Vega-Muñoz, A. (2022). Examining whistleblowing intention: The influence of rationalization on wrongdoing and threat of retaliation. International journal of environmental research and public health, 19(3), 1752.

- Kirby, M. (2020). A qualitative study on internal controls usage and financial accountability among Baptist churches in North Georgia. Liberty University, 21(2).

- Krambia-Kapardis, M. (2020). An exploratory empirical study of whistleblowing and whistleblowers. Journal of Financial Crime, 27(3), 755–770. https://doi.org/10.1108/JFC-03-2020-0042

- Krishna, C., & Garg, A. (2022). Employee Retention: An Important Factor for Strategies Development. ANWESH: International Journal of Management & Information Technology, 7(1).

- Lee, J., Oh, S.-H., & Park, S. (2022). Effects of Organizational Embeddedness on Unethical Pro-organizational Behavior: Roles of Perceived Status and Ethical Leadership. Journal of Business Ethics, 176(1), 111–125.

- Lee, W. M. (2020). The determinants and effects of board committees. Journal of Corporate Finance, 65, 101747.

- Luciano, M. M., Nahrgang, J. D., & Shropshire, C. (2020). Strategic leadership systems: Viewing top management teams and committees of directors from a multiteam systems perspective. Academy of Management Review, 45(3), 675-701.

- McGahan, A. M. (2021). Integrating insights from the resource-based view of the firm into the new stakeholder theory. Journal of management, 47(7), 1734-1756.

- Maduabuchi, E. S. (2021). An exploration of internal control deficiencies and their impact on fraud in local churches in Nigeria. Liberty University, School of Business, July.

- Maifizar, A., Marlina, L., Vonna, S. M., & Abdullah, I. (2020). the Religious Role of Leadership Morality in Preventing the Fraud of Gampong Funds in West Aceh District. Journal Of Archaeology Of Egypt/Egyptology, 17(5), 111–120.

- Maulida, W. Y., & Bayunitri, B. I. (2021). The influence of whistleblowing system toward fraud prevention. International Journal of Financial, Accounting, and Management, 2(4), 275-294.

- Maulida, W. Y., & Bayunitri, B. I. (2021). The influence of whistleblowing system toward fraud prevention. International Journal of Financial, Accounting, and Management, 2(4), 275-294.

- Mawanza, W. (2014). An Analysis of the Main Forces of Workplace Fraud in Zimbabwean Organisations: The Fraud Triangle Perspective. SSRN Electronic Journal, 2, 86–94. https://doi.org/10.2139/ssrn.2463235

- Meitasir, B. C., Komalasari, A., & Septiyanti, R. (2022). Whistleblowing System and Fraud Prevention: A Literature Review. Asian Journal of Economics, Business, and Accounting, 22(18), 23-29.

- Miiro, E. (2013). Internal controls and financial management in faith based organizations: A case study of Seventh-Day Adventists Church Central Uganda Conference (Doctoral dissertation, Uganda Management Institute).

- Mojambo, G., Tulung, J. E., & Saerang, R. T. (2020). The influence of Top Management Team (TMT) characteristics toward Indonesian Banks performance during the digital era (2014–2018). Available at SSRN 3541856.

- Mohamed-Isa, A., Razman, A., Latiff, A., Noor, M., Osman, H., & Hj, A. (2020). Determinants of Whistleblowing Intention in Organization. Journal of Environmental Treatment Techniques, 9(1), 54–58. https://doi.org/10.47277/jett/9(1)85

- Munyao, S. M. (2021). Effects of Strategic Leadership and External Environment on the Performance of Africa Inland Church Theological Training Institutions in Kenya (Doctoral dissertation).

- Niemandt, C. (2019). Missional leadership (p. 262). AOSIS.

- Nurlina, N. (2022). Examining Linkage Between Transactional Leadership, Organizational Culture, Commitment and Compensation on Work Satisfaction and Performance. Golden Ratio of Human Resource Management, 2(2), 108-122.

- Njobvu, E. N., Kaira, B., & Chowa, T. (2020). Financial Accountability and Internal Controls in Religious Organizations : A Case Study of Holy Spirit Catholic Parish. The International Journal of Business Management and Technology, 4(3).

- Nortey, R. E. G. I. N. A. (2019). Financial Management System of Churches: A Case Study of the Methodist Church Ghana, Tema Diocese. (Doctoral Dissertation, University of Ghana)., July, 1–87. file:///C:/Users/Harrison/AppData/Local/Mendeley Ltd./Mendeley Desktop/Downloaded/Doville NK – 2010 – University of Ghana httpugspace.ug.edu.gh University of Ghana httpugspace.ug.edu.gh.pdf

- Ocansey, E. O. N. D., & Ganu, J. (2017). The Role of Corporate Culture in Managing Occupational Fraud. Research Journal of Finance and Accounting, 8(24), 2222–2847.

- Oelrich, S. (2021). Intention without action? Differences between whistleblowing intention and behavior on corruption and fraud. Business Ethics, March 2020, 1–17. https://doi.org/10.1111/beer.12337

- Onyinah, O. (2020). Distinguished church leader essay: The Church of Pentecost and its role in Ghanaian society. In African Initiated Christianity and the Decolonisation of Development (pp. 183-194). Routledge.

- Oreg, S., & Berson, Y. (2019). Leaders’ impact on organizational change: Bridging theoretical and methodological chasms. Academy of Management Annals, 13(1), 272-307.

- Paais, M., & Pattiruhu, J. R. (2020). Effect of motivation, leadership, and organizational culture on satisfaction and employee performance. The Journal of Asian Finance, Economics, and Business, 7(8), 577-588.

- Pan, K., Blankley, A. I., Harris, R., & Lai, Z. (2022). Financial Fraud, Governance, and Survival in Congregations: An Empirical Assessment of Congregational Fraud in the United States Based on Cases Prosecuted by the US Department of Justice. Journal of Leadership, Accountability & Ethics, 19(2).

- Palepu, K. G., Healy, P. M., Wright, S., Bradbury, M., & Coulton, J. (2020). Business analysis and valuation: Using financial statements. Cengage AU.

- Peltier-Rivest, D. (2018). A model for preventing corruption. Journal of Financial Crime, 25(2), 545–561. https://doi.org/10.1108/JFC-11-2014-0048

- Priyadi, A., Hanifah, I. A., & Muchlish, M. (2022). The Effect of Whistleblowing System toward Fraud Detection with Forensic Audit and Investigative Audit as Mediating Variables. Devotion Journal of Community Service, 3(4), 336-346.

- Priyanka, Khandagale., Akshata, Utekar., Anushka, Dhonde., Prof., S., S., Karve. (2022). Fake Job Detection Using Machine Learning. International Journal For Science Technology And Engineering, doi: 10.22214/ijraset.2022.41641

- Putra, I. M. Y. D., Rasmini, N. K., Gayatri, G., & Ratnadi, N. M. D. (2022). Organizational culture as moderating the influence of internal control and community participation on fraud prevention in village fund management during the COVID-19 pandemic. Linguistics and Culture Review, 6(S1), 351-362.

- Putra, I., Sulistiyo, U., Diah, E., Rahayu, S., & Hidayat, S. (2022). The influence of internal audit, risk management, whistleblowing system and big data analytics on the financial crime behavior prevention. Cogent economics & finance, 10(1), 2148363.

- Rashid, A., Al-Mamun, A., Roudaki, H., & Yasser, Q. R. (2022). An Overview of Corporate Fraud and its Prevention Approach. AABFJ, 16(1), 101–119.

- Razak, N. (2021). The effect of training, competence and work motivation on employee performance. Jurnal Economic Resource, 4(2).

- Rockson, A. (2019). Strategies for preventing financial fraud in church organizations in Ghana (Doctoral dissertation, Walden University).

- Rustiarini, N. W., & Merawati, L. K. (2020). Fraud and Whistleblowing Intention: Organizational Justice Perspective. Riset Akuntansi Dan Keaungan Indonesia , 5(3), 210–222.

- Said, J., Asry, S., Rafidi, M., Obaid, R. R., & Alam, M. M. (2018). Integrating religiosity into fraud triangle theory: Empirical findings from enforcement officers. Global Journal Al-Thaqafah, 2018, 131–144. https://doi.org/10.7187/gjatsi2018-09

- Samimi, M., Cortes, A. F., Anderson, M. H., & Herrmann, P. (2022). What is strategic leadership? Developing a framework for future research. The Leadership Quarterly, 33(3), 101353.

- Scaturro, R. (2018). Defining Whistleblowing International Anti Corruption Academy Research & Science, 05, 1–21.

- Schaedler, L., Graf-Vlachy, L., & König, A. (2022). Strategic leadership in organizational crises: A review and research agenda. Long Range Planning, 55(2), 102156.

- Schroeder, R. G., Clark, M. W., & Cathey, J. M. (2022). Financial accounting theory and analysis: text and cases. John Wiley & Sons.

- Scheetz, A. M., & Fogarty, T. J. (2019). Walking the talk: Enacted ethical climates as psychological contract venues for potential whistleblowers. Journal of Accounting and Organizational Change, 15(4), 654–677. https://doi.org/10.1108/JAOC-06-2018-0047

- Shahid, Ali., Shoukat, Ali., Junfeng, Jiang., Martina, Hedvicakova., Ghulam, Murtaza. (2022). Does board diversity reduce the probability of financial distress? Evidence from Chinese firms. Frontiers in Psychology, doi: 10.3389/fpsyg.2022.976345

- Shaddiq, S., Zulkarnain, I., & Anggraini, N. (2023). The Influence of Human Resource and Marketing Competence, Morality, Whistleblowing, and Internal Control System on the Prevention of Fraud in Village Financial Management in Karimun Regency. Quality Festival.

- Sharma, N. (2022). Effects of Integrity and Controls on Financial Reporting Fraud. Retrieved December 8, 2022.

- Suryandari, N. N. A., Endiana, I. D. M., Susandya, A. A. B. A., & Apriada, K. (2021). The Role of Employee Ethical Behavior and Organizational Culture in Preventing Fraud at the LPD. PalArch’s Journal of Archaeology of Egypt/Egyptology, 18(08), 916-929.

- Tanui, P. J., Omare, D., & Bitange, J. B. (2016). Internal control system for financial management in the church: A case of protestant churches in Eldoret Municipality, Kenya. European Journal of Accounting, Auditing, and Finance Research. 4(6), 29–46.

- Tetteh, L. A., Muda, P., Yawson, I. K., Sunu, P., & Ayamga, T. A. (2021). Accountability and Internal Control Practices: a Study of Church Fund Management. Academy of Accounting and Financial Studies Journal, 25(6), 1–15.

- Treadwell, G. W. (2020). Preventing church embezzlement in US protestant and catholic churches. Journal of Business and Accounting, 13(1), 190–201.

- Uys, T., & Uys, T. (2022). Whistleblowing and the sociological imagination (pp. 1-23). Palgrave Macmillan US.

- Walter, A. T. (2021). Organizational agility: ill-defined and somewhat confusing? A systematic literature review and conceptualization. Management Review Quarterly, 71, 343-391.

- Verma, P., Mohapatra, S., & Löwstedt, J. (2016). Ethics training in the Indian IT sector: Formal, informal or both? Journal of Business Ethics, 133(1), 73–93. https://doi.org/10.1007/s10551-014-2331-4

- Wang, Y., Yu, M., & Gao, S. (2022). Gender diversity and financial statement fraud. Journal of accounting and public policy, 41(2), 106903.

- William, Wakhisi. (2021). Effect of strategic leadership on organization performance of state-owned Sugar manufacturing firms in Western Kenya. International journal for innovation education and research, doi: 10.31686/IJIER.VOL9.ISS9.3312

- Yulian Maulida, W., & Indah Bayunitri, B. (2021). The influence of whistleblowing system toward fraud prevention. International Journal of Financial, Accounting, and Management, 2(4), 275–294. https://doi.org/10.35912/ijfam.v2i4.177

- Yoon, J., & Suh, M. G. (2019). Determinants of organizational performance: some implications for top executive leadership in Korean firms. Asia Pacific Business Review, 25(2), 251-272.

- Yoon, S. (2020). A study on the transformation of accounting based on new technologies: Evidence from Korea. Sustainability, 12(20), 8669.

- Zaim, H., Muhammed, S., & Tarim, M. (2019). Relationship between knowledge management processes and performance: critical role of knowledge utilization in organizations. Knowledge Management Research & Practice, 17(1), 24-38.

- Zietlow, J., Hankin, J. A., Seidner, A., & Timothy, O. (2018). Strategies Church Financial Leaders Use for Financial Sustainability During Economic Crises. Critical Readings in Islamic Social Finance. Vol. 2, YTI Lecture Series, 7(2), 149–154. https://doi.org/10.1016/j.jbusres.2019.12.022

- Zietlow, J., Hankin, J. A., Seidner, A., & O’Brien, T. (2018). Financial management for nonprofit organizations: policies and practices. John Wiley & Sons.

- Zollo, L., Laudano, M. C., Boccardi, A., & Ciappei, C. (2019). From governance to organizational effectiveness: the role of organizational identity and volunteers’ commitment. Journal of Management and Governance, 23, 111-137.