The Influence of Islamic Financial Literacy and Product Knowledge on The Decision to Use Islamic Banking Products on Students of Muhammadiyah Colleges in South Sulawesi, Indonesia

- Rabiatul Adawiah

- Agusdiwana Suarni

- Sri Wahyuni

- 960-971

- Jul 4, 2024

- Finance

The Influence of Islamic Financial Literacy and Product Knowledge on The Decision to Use Islamic Banking Products on Students of Muhammadiyah Colleges in South Sulawesi, Indonesia

Rabiatul Adawiah, Agusdiwana Suarni, Sri Wahyuni

Departmen in Islamic Economics, Faculty of Economics and Business, University of Muhammadiyah Makassar, Indonesia

DOI : https://dx.doi.org/10.47772/IJRISS.2024.806073

Received: 14 May 2024; Revised: 29 May 2024; Accepted: 01 June 2024; Published: 04 July 2024

ABSTRACT

This research investigates the effect of Islamic financial literacy and product knowledge on the decision to use Islamic banking products among students of Muhammadiyah Universities in South Sulawesi. Islamic financial literacy refers to an individual’s understanding of the principles of Islamic finance, while product knowledge relates to their knowledge of the various Islamic banking products available. This study used a quantitative approach by distributing questionnaires to 348 sample student respondents scattered and randomly selected from several Muhammadiyah universities in South Sulawesi. The collected data were analyzed using SPSS version 25 with multiple linear regression analysis techniques to identify the influence of the two independent variables on the dependent variable. The results showed that both interpretations were accepted, with the coefficient of determination showing 86.8% variation in the decision to use Islamic banking products, explained by Islamic financial literacy and knowledge of Islamic banking products, and a constant coefficient value of 0.005. Islamic financial literacy (X1) has a regression coefficient of 0.755, and product knowledge (X2) is 0.275. X1. The propensity value is <.001 <0.05. with a count value of 11.914 and a table of 1.652. (tcount>ftable). X2 is <001 <0.05, the count value is 9.236, and the table is 1.652 (tcount> table) with the results of the data normality test (X1), product knowledge (X2), and usage decisions (Y) The analysis shows a positive relationship between Islamic financial literacy and the use of Islamic banking products and a positive influence between product knowledge and the use of Islamic banking products.

Keywords: Financial Literacy, Sharia, Islamic Banking, Students, Muhammadiyah.

INTRODUCTION

Indonesia’s Islamic banking industry has emerged as a leading economic pillar during globalization. This phenomenon cannot be separated from the great public interest, especially students, who have great potential as prospective customers for Islamic banking products. The student demographic has the potential to play an important role in driving the growth of the Islamic economy. The development of Islamic banking financing can be traced since the enactment of Law No. 21 of 2008 which specifically discusses Islamic banking. The law, which was issued on July 16, 2008, highlights the significant contribution of Islamic banks in encouraging national economic growth by facilitating the distribution of financing.

The problem of sharia financial literacy among students is still an urgent concern that requires serious attention because sharia financial literacy includes an in-depth understanding of sharia principles in financial transactions which is the main basis for determining financial choices. Insufficient sharia financial literacy can have a negative impact on students’ decision-making processes in choosing and using sharia banking products.

Based on data from the Research and Development Council of PP Muhammadiyah, there were 162 Muhammadiyah and ‘Aisyiyah Universities (PTMA) until August 2020. Among them are 60 universities, 82 colleges, 6 academies, 9 institutes and 5 polytechnics. South Sulawesi Province as a center of education and economic growth makes it an ideal place to test the effect of Islamic financial literacy on individual choices in using Islamic banking products.

This study aims to increase our understanding of the determinants that influence students’ choices in using Islamic banking products, as well as the importance of Islamic financial literacy in the decision-making process because the amount of Islamic financial literacy and awareness of Islamic banking products are significant determinants in individual choices to utilize Islamic banking products. Many recent studies show that there is no substantial impact of the level of Islamic financial literacy in influencing consumers’ choice or desire to use Islamic banking products (Dikriansyah, 2018; Hakim, 2020).

The primary responsibility of humans, who are considered as khalifahs (representatives of Allah SWT) in this world, is to actively improve the welfare conditions of mankind and carry out submissive devotion to the Almighty Creator. Humans have a very important role in economic activities to achieve the welfare of humanity on this planet. From the Islamic perspective, it is advisable to engage in business operations or commercial activities as well as make investments in the financial sector as part of an economic endeavor. This view has been explained in QS. Lukman verse 20:

Translation:

“Have you not noticed that Allah has subjected for you what is in the heavens and what is on the earth? He has perfected for you His favors, outward and inward. However, there are those among the people who dispute the Oneness of Allah without knowledge, guidance, or an illuminating scripture.

Financial literacy includes a series of activities aimed at increasing individuals’ understanding, ability, and confidence in managing their own money effectively. Sharia financial literacy is one of the areas of financial literacy in Indonesia. Sharia financial literacy is a type of financial literacy that is currently developing. The aim of increasing Sharia financial literacy is to expand understanding and knowledge about Sharia financial concepts, as well as to increase the adoption of Sharia financial goods and services among consumers and with increasing Sharia financial literacy, it is hoped that there will be an increase in customers in the sharia financial sector thereby contributing to the expansion of the industry Islamic finance. This anticipated increase is undoubtedly related to the large Muslim population in Indonesia.

Product knowledge, as defined by Nurlaeli (2017), refers to the comprehensive understanding that customers have about various goods and services. This includes knowledge of different types of products and their functions, which is used to make informed purchasing choices. Islamic banking now provides a variety of products including Easy Savings, Mabrur Savings, Tabunganku, and Retirement Savings (webform.bsm.co.id, 2021). The variety of savings products offered by Islamic banks has its own benefits and has several characteristics that make it easier for customers (Hasibuan & Wahyuni, 2020). Despite the many variants and benefits of savings products offered by Islamic banks, there is still a lack of public awareness of these products. As a result, only a few Indonesians use Islamic banking products (Firdaus & Alawiyah, 2021).

The significant growth of Islamic banking in Indonesia can be seen with the introduction of the Islamic economic system. Recognition of the existence of Islamic banking became evident with the introduction of legislation. The text refers to banking legislation, namely Law Number 7 of 1992 which has changed. Law No. 8 of 1998 emphasized that the Islamic banking system was integrated into the national banking system. This integration is further elaborated in Law Number 10 of 1998 which regulates the legal framework and various forms of business conducted by Islamic Banks. The law contains provisions that encourage banks in Indonesia to establish Islamic branches or transform into Islamic banks. In addition, all operational details must be implemented through government regulations, Minister of Finance decrees, or directives issued by Bank Indonesia.

Islam contains many principles that regulate Sharia financial management and the importance of knowledge about products that are halal and following religious teachings. One of the relevant hadiths is the hadith narrated by Imam Ahmad and Abu Daud from Abdullah bin Amr, that the Prophet Sallallahu ‘alaihi wa sallam said:

“A strong believer is better and more loved by Allah than a weak believer, even though there is goodness in both. Be firm in seeking what is beneficial for you ask Allah for help and don’t feel weak. If something happens to you, don’t say anything, ‘if only I did this and that’ but say, ‘This is Allah’s destiny and Allah does what He wills’. Indeed, the words ‘if’ open the door to Satan.” (HR. Ahmad and Abu Daud)

Although it does not specifically mention financial literacy or product knowledge, this hadith emphasizes the importance of perseverance, strength, and courage in seeking what is useful. It provides a basis for Muslims to acquire the necessary knowledge in financial management and product selection by sharia principles. Muslims are also directed to look after their finances well. One of them is a hadith narrated by Imam Bukhari and Muslim from Abu Hurairah. This hadith emphasizes the importance of effort and hard work in seeking halal sustenance. With good effort, a person can obtain blessings from the results of his work. This also shows the importance of not depending on other people absolutely in economic matters, but rather making effort and hard work as an effort to achieve financial independence.

This issue is of great concern, especially in countries where the majority of the population adheres to Islam. Therefore, it is important to investigate the extent to which Islamic finance literature contributes to facilitating customer choice in Islamic banks. The importance of this linkage calls for further action from the government, the business world, businesses and academia to improve Islamic financial literacy. Having an adequate understanding of Islamic finance may motivate individuals to choose Shariah-compliant institutions over conventional banks.

Rooted in the description above, it is necessary to study the various aspects that influence a person’s choice to become an Islamic bank customer. By finding many factors that have the potential to have an impact. Examining the correlation between Islamic financial literacy and familiarity with Islamic banking products is very important to understand its impact on the decision-making process related to the use of Islamic banking products. Do people with high levels of Islamic financial literacy also have sufficient information about Islamic banking products to make informed financial decisions? The act of a consumer choosing to use a product involves choosing from two or more different options. By improving the understanding of Islamic financial literacy and fostering a deeper understanding of Islamic banking among university students, the aim is to facilitate the development of effective learning methodologies that can increase their awareness and understanding of Islamic banking products. Therefore, this study aims to facilitate by investigating and analyzing the growth of the Islamic banking sector in Indonesia and improving the understanding of Islamic finance among the younger generation.

This study seeks to test and assess the impact of two crucial aspects, namely Islamic financial literacy and understanding of Islamic banking products on the choices made by students of Muhammadiyah Universities in South Sulawesi Province in utilizing Islamic banking products. The purpose of this study is to offer a comprehensive understanding and practical guidance for implementing Islamic economic policies at the student level. The findings are expected to not only contribute to the academic world but also have a positive influence on the growth of Islamic economics in Indonesia.

Partial test findings, the hypothesis regarding the correlation between Islamic Financial Literacy and Using Islamic Banking Products is accepted. Good Sharia financial literacy skills can help an individual to understand the risks and potential benefits as well as the good according to Sharia law in Islamic banking products. With a high level of literacy or a good understanding of the Islamic financial system will tend to make financial decisions carefully, informed and logical. Then in turn can make their decisions in using Islamic banking products. Strong financial literacy can provide a better understanding of sharia principles in the financial context, understand the consequences, and keep away from possible violations of Islamic law in the financial management process. The higher the level of Islamic financial literacy that students have, the more likely they are to choose to use banking products based on Islamic principles.

The interpretation of these results is that a good understanding and knowledge of Islamic financial concepts can influence students’ preferences and financial decisions in choosing Islamic banking products. Students who have high Islamic financial literacy tend to be more confident and motivated to use Islamic banking products. In the context of Muhammadiyah University of South Sulawesi, the results of this study indicate the importance of improving Islamic financial literacy among students as an effort to expand the use of Islamic banking products in this community. Factors such as understanding of sharia principles in finance, understanding of the benefits and features of Islamic banking products, and awareness of Islamic financial values can be the main drivers in making decisions to use Islamic banking products.

Partial test findings, the hypothesis regarding the correlation between product knowledge and Using Islamic Banking Products is accepted. The role of product knowledge certainly also plays an important role because with in-depth knowledge of Islamic banking products, it will be able to increase customer understanding and trust so that it will contribute positively to their decisions. The higher the level of knowledge of students about Islamic banking products, the more likely they are to choose and use these products.

The interpretation of these results is that good knowledge of Islamic banking products, including an understanding of the features, benefits, and advantages of Islamic products, can influence students’ preferences and decisions in choosing banking services that comply with sharia principles. Students who have deeper product knowledge tend to be more trusting and motivated to use Islamic banking products. In the context of Muhammadiyah University of South Sulawesi, this finding highlights the importance of increasing students’ knowledge and understanding of Islamic banking products as an effort to promote the use of Islamic products among students. Education and counseling efforts on Islamic banking products can help increase students’ awareness and interest in sharia-based financial products, thus potentially increasing the penetration and adoption of Islamic banking products in the college environment.

LITERATURE REVIEW

Research conducted regarding the influence of sharia financial literacy and product knowledge on decisions to use sharia banking products contains several theoretical reviews that are relevant and can be a basis for understanding the context and concepts.

Research on Islamic financial literacy and product knowledge in the context of using Islamic banking products has become a major focus in an effort to understand people’s financial behavior has also been carried out by a number of previous researchers, such as Aisyah and Wicaksono in 2020, who have made significant contributions in this field, as seen in their research entitled “Analysis of the Effect of Islamic Financial Literacy and Product Knowledge on Decisions to Use Islamic Banking Products.” Case Study of Islamic Economics and Islamic Banking Students in Bantul Regency, Yogyakarta: Case Study of Sharia Economics and Sharia Banking Students in Bantul Regency, Yogyakarta.”

The results of Aisyah and Wicaksono’s research recorded interesting findings, namely that Islamic financial literacy has a positive and significant influence on the decision to use Islamic banking products. However, as an additional research that complements the previous contributions, my research aims to go further in-depth by considering two main variables, namely Islamic financial literacy and product knowledge.

Islamic financial literacy is defined as one’s ability to understand Islamic financial principles, while product knowledge refers to an in-depth understanding of available Islamic banking products. In this study, the hypothesis is proposed that Islamic financial literacy and product knowledge together play an important role in shaping the decision to use Islamic banking products.

The research method used involves surveys and statistical analysis to measure the level of Islamic financial literacy and product knowledge of respondents, as well as assessing the extent to which these two variables influence the decision to use Islamic banking products. Hopefully, this research can provide deeper insights into the factors that influence consumer decisions in choosing Islamic banking products by detailing aspects of Islamic financial literacy and product knowledge, this research is expected to contribute more deeply to our understanding of people’s financial behavior, especially in the context of using Islamic banking products.

METHODOLOGY

This research uses quantitative methodology to determine the influence between research variables on factors that influence the use of Islamic banking products, focusing on the role of Islamic financial literacy and product knowledge. The type of data used is obtained data directly from respondents who filled out the questionnaire. The research conducted in this study used quantitative survey research methodology to collect data on the extent of Islamic financial literacy and product knowledge as well as factors that influence individual decisions to use Islamic banking products. A questionnaire containing relevant questions was used to assess participants’ knowledge in this regard. The data obtained were then statistically analyzed using the Likert scale technique. The sampling method uses purposive sampling technique, where the sample is determined randomly referring to the criteria that are in accordance with the research objectives. The criteria for respondents in this study were active students at the sampled universities and then used multiple linear regression to analyze the data that had been obtained.

This study was conducted to determine the effect of Islamic financial literacy and product knowledge on the decision-making process of students at Muhammadiyah Universities in South Sulawesi in adopting Islamic banking products to determine the impact of Islamic financial literacy and product knowledge on customer preferences in using Islamic banking products, we will assess their understanding of Islamic financial concepts, measure their knowledge of Islamic financial products, and evaluate their level of Islamic financial literacy. This will help us understand how these factors affect decision-making in using Islamic banking products.

The population studied refers to students in Muhammadiyah universities in South Sulawesi Province who use or do not use Islamic banking products. This population includes all students who meet the criteria at Muhammadiyah universities in South Sulawesi including several Muhammadiyah universities including 5 PTM namely Muhammadiyah University of Makassar (UNISMUH MAKASSAR) with a total of 20,000 students, Muhammadiyah University of Bone (UM BONE) with a total of 878 students, Muhammadiyah University of Parepare (UMPAR) with a total of 4,123 students, Muhammadiyah University of Sinjai (UMSI) with a total of 3,864 students, Muhammadiyah University of Palopo (UM PALOPO) with a total of 3,981 students. The total number of students from these 5 universities amounted to 32,842 students. The number of samples selected must reflect the diversity in the population to be able to provide results.

This study uses Non-Probability Sampling Technique which is a sampling technique that does not provide equal opportunities for all members of the population to be sampled but only to samples that match the criteria and objectives of the study with certain considerations. The type of technique for determining the sample uses a method developed by Isaac and Michael with an error level (significance level) of 5%. With a population scale of 35,000, the determination of the number of samples and known population is 348 questionnaire samples.

Based on the table determination, there were 348 respondents and then determining the sample using purposive sampling technique, namely randomly referring to the criteria as active students at the sample universities outlined in the following table:

Table 1. 3 Total Population and Sample of Respondents

| No. | University Name | Population | Sample |

| 1. | University of Muhammadiyah Makassar | 20.000 | 140 |

| 2. | University of Muhammadiyah Bone | 878 | 28 |

| 3. | Muhammadiyah University of Sinjai | 3.864 | 50 |

| 4. | Muhammadiyah University of Pare-pare | 4.123 | 80 |

| 5. | University of Muhammadiyah Palopo | 3.981 | 50 |

| AMOUNT | 32.842 | 348 | |

Based on the list of tables, the number of respondents in each university is described with a total of 348 respondents. Then the interval data was researched by assessing using a Likert scale with a Convenience Sample strategy by distributing Google Form links to sample respondents and assessing with the scoring method then the instrument was measured on a Likert scale, ranging from positive to negative, using a quantitative approach. Respondents’ replies were then given a numerical score.

In the data analysis process, there are many analytical techniques used in this study, including descriptive statistical analysis, multiple linear regression analysis, and classical assumption testing. This research also uses standard assumption tests which include normality test, multicollinearity test, autocorrelation test, and heteroscedasticity test. This study also conducted hypothesis testing, including the f test (simultaneous test), t test (partial test), and the coefficient of determination (R2).

Based on the list of tables, the number of respondents in each university is described with a total of 348 respondents. Then the interval data was researched by assessing using a Likert scale with a Convenience Sample strategy by distributing Google Form links to sample respondents and assessing with the scoring method then the instrument was measured on a Likert scale, ranging from positive to negative, using a quantitative approach. Respondents’ replies were then given a numerical score.

In the data analysis process, there are many analytical techniques used in this study, including descriptive statistical analysis, multiple linear regression analysis, and classical assumption testing. This research also uses standard assumption tests which include normality test, multicollinearity test, autocorrelation test, and heteroscedasticity test. This study also conducted hypothesis testing, including the f test (simultaneous test), t test (partial test), and the coefficient of determination (R2).

RESULTS AND DISCUSSION

This research was conducted in South Sulawesi Province so that the respondents in this study were students at Muhammadiyah Universities which had a population of 32,842 students. The characteristics used in this study are related to the campus origin of each respondent student.

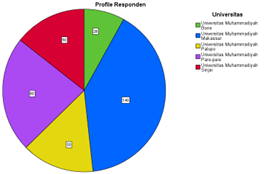

Figure 1. 1 Profile Chart of Research Respondents

Source: Data Processed (SPSS 25) 2024

Based on this figure, the respondent profile shows that the majority of respondents come from Muhammadiyah Makassar University. With a total comparison of 140 respondents from Universitas Muhammadiyah, 80 respondents from Universitas Muhammadiyah Parepare, 50 respondents from Universitas Muhammadiyah Sinjai, 50 respondents from Universitas Muhammadiyah Palopo, and 28 respondents from Universitas Muhammadiyah Bone.

Table 1.5: Descriptive Statistical Analysis Results

| Descriptive Statistics | |||||

| N | Min. | Max. | Mean | Std. Deviation | |

| Usage Decision | 348 | 09.00 | 45.00 | 36.34 | 9.227 |

| Literacy Skills | 348 | 10.00 | 45.00 | 35.80 | 8.116 |

| Product Knowledge | 348 | 09.00 | 45.00 | 35.63 | 8.715 |

| Valid N (listwise) | 348 | ||||

Source: Data Processed (SPSS 25) 2024

Table 1.5 is the output of descriptive statistics for all research variables with a sample size of 348 respondents. Based on the descriptive statistics table, it can be briefly explained, among other things, the literacy skill level variable has a minimum value of 10 and a maximum literacy level value of 45 and the average literacy skill level value is 36 with a standard deviation of 8.715. The Islamic bank product knowledge variable (product knowledge) has a minimum value of 9 and a maximum value of product knowledge of 45 and an average literacy level of 36 with a standard deviation of 8.116. The usage decision variable has a minimum value of 9 and a maximum usage decision level value of 45 and an average value of 36 with a standard deviation of 9.227.

This research is in the Multiple Linear Regression Analysis Test which is an approach method to see the relationship between the independent variable and the dependent variable. Multiple Linear Regression Analysis is used to find the effect between the independent variable (X) and the dependent variable (Y) which includes at least two independent variables explaining that the constant coefficient value is 1.305, while the regression coefficient value for Islamic financial literacy (X1) is 0.612 and the regression coefficient value for product knowledge (X2) is 0.442. The classical assumptions tested in statistical calculations have also been tested as in the description of the histogram diagram, P-P Plot, as well as scatterplot.

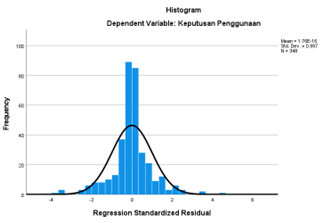

Figure 1. 2: Histogram Graph

Source: Data Processed (SPSS 25) 2024

The image on the histogram provides a visual depiction of how the normality of data looks like because a lot of data accumulates resting on the midpoint by forming a bell that can be an illustration of the normal distribution of data.

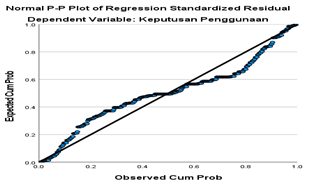

Figure 1. 2: P-P Plot Graph

Source: Data Processed (SPSS 25) 2024

The image in the P-P Plot version where it can be seen in the image subjectively how close it is if it is visually depicted how the normal form of a data is due to the amount of data that rests on a straight cut line or the distribution of residues in a straight and regular manner which can be an illustration of the normal distribution of a data. In addition, the normality test aims to be able to test whether in the regression model the dependent variable and the independent variable both have a normal distribution or not. To find out about the normality of the data in this study, it was carried out by looking at the Kolmogorov-Smirnov value. The data acceptance limit is declared normally distributed if the significant Kolmogorov-Smirnov> 0.05. The results of the data normality test on the variables Islamic financial literacy (X1), product knowledge (X2) and usage decisions (Y) show that the Asymp.Sig (2-tailed) significance value is 0.001, which is smaller than 0.05. So according to the basis for decision making, it can be concluded that the data is normally distributed. In this way, the assumptions or requirements for data normality have been met.

Multicollinearity in a regression model can be determined by calculating the Variance Inflation Factor (VIF) value. Based on the results and rules of the multicollinearity test, it can be concluded that the Collinearity Tolerance value is 0.187 and the Variance Inflation Factor (VIF) is 5.344 and the Unstandardized Constant is <0.05 so it is significant and multicollinearity does not occur. Other interpretations can then be made if all assumptions have been met.

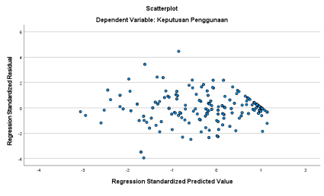

The heteroscedasticity test is carried out to test whether in the regression model there is an inequality or there is a disparity in the residual variance between one observation to another. The picture in the scatterplot version can be seen in the subjective image where if it is visually depicted the form of normality of a data if the residual distribution does not form a certain pattern or random distribution, there is no heteroscedasticity, and the points spread above and below the number 0 on the Y axis, then there is no heteroscedasticity.

Figure 1. 3: Heteroscedasticity Test Results

Source: Data Processed (SPSS 25) 2024

Based on the picture that there is no certain pattern either above or below the number 0. So it can be concluded that the regression model does not occur symptoms of heteroscedasticity and it is known that the significant value of variable X1 (Sharia Financial Literacy) is <.001>0.05 which means that there are no symptoms of heteroscedasticity while variable X2 (Product Knowledge) is .001>0.05 which indicates the absence of symptoms of heteroscedasticity. It can be concluded that the classical assumptions tested in the statistical calculation of the residual assumption test can visually show normal data results after testing as can be seen in the diagram image with all assumptions met.

The F (simultaneous) test is carried out to test a hypothesis, testing simultaneously or simultaneously, especially to assess the combined effect of independent variables on the dependent variable. It is also used to determine the relationship between variables X and Y, where variable X consists of variables X1 and X2 which together affect variable Y. In the simultaneous test X1 and X2 are tested simultaneously so how X1 and X2 affect Y. The significance value is 0.0, so the ability of Sharia Financial Literacy and Product Knowledge (both variables) has an effect on usage decisions.

The t test (partial) was conducted to test the hypothesis to determine the comparison between the two variables. The t test is carried out to compare tcount and ttable at a significant level of 5%, if tcount> ttable then the independent variable can be said to be significant. The effect of Islamic Financial Literacy on the Decision to Use Islamic Banking Products can be seen that the value of X1 based on the probability value on the Islamic financial literacy ability variable is <.001 <0.05. Then when viewed based on the tcount value is 11.914 and the ttable is 1.652. From this calculation, it can be stated that tcount>ftabel. This means that Islamic financial literacy has a positive and significant influence on the decision to use Islamic banking products. It can be concluded that H1 is accepted because this hypothesis suggests that the higher the level of Sharia financial literacy of customers, the more likely they are to make positive decisions in choosing Islamic banking products. Strong financial literacy is expected to provide a better understanding of sharia principles in a financial context. The effect of Product Knowledge on the Decision to Use Islamic Banking Products based on the explanation of Table 1.12 is known that the value of X2, namely product knowledge based on the probability value on the product knowledge variable is <.001> 0.05 Then when viewed based on the count value is 9.236 and the ttable is 1.652. From this calculation, it can be stated that tcount> ttable. This means that product knowledge also has a positive and significant influence on decisions to use Islamic banking products. The role of product knowledge is influential in making customer decisions. With in-depth knowledge of Islamic banking products can increase customer understanding and trust, it is hoped that this will contribute positively to their decisions.

The measure of the proportion of variation in the dependent variable that can be explained by the independent variable is known as the coefficient of determination (R2). This coefficient is used as a metric to assess how well the relationship between the independent variable and the dependent variable is in a regression equation. The coefficient of determination test, often called R2, measures how effective the regression model is in predicting the dependent variable. R2 determines the individual influence of each independent variable on the dependent variable, thereby allowing us to identify the variable that has the greatest impact. When calculating the coefficient of determination, the value ranges between 0 and 1. If R2 is equal to 0, it means there is no relationship between the independent and dependent variables. When R2 approaches 0, this indicates that the influence of the independent variable on the dependent variable is getting smaller. Conversely, when the R2 value approaches 1, the influence of the independent variable on the dependent variable becomes stronger (Ghozali, 2018).

Based on the calculation results which can be seen in table 1.13, the determinant coefficient (R2) value is 0.868, meaning the R2 value is close to 1 so that the influence of sharia financial literacy (X1) and product knowledge (X2) on the decision to use sharia banking products is very strong and is 86.8 percent of The independent variables (Sharia financial literacy and product knowledge) can explain the dependent variable (decision to use the product), while the rest is explained by other variables not explained in this research.

The results showed that Islamic financial literacy significantly influenced the decision to use Islamic banking products. The ability to understand the principles of Islamic finance can help individuals make financial decisions that are careful, informed, and following sharia principles. A high level of Islamic financial literacy increases the likelihood of a person to choose Islamic banking products, emphasizing the importance of increasing Islamic financial literacy among Muhammadiyah university students in South Sulawesi.

Knowledge of Islamic banking products also plays an important role in shaping the decision to use these products. In-depth knowledge of the features, benefits, and advantages of Islamic banking products can increase a person’s trust and motivation to use these products, so increasing knowledge of Islamic banking products is expected to expand the use of Islamic products among students. When compared to previous research conducted by Aisyah and Wicaksono in 2020, in their research entitled “Analysis of the Effect of Islamic Financial Literacy and Product Knowledge on Decisions to Use Islamic Banking Products: Case Study of Sharia Economics and Sharia Banking Students in Bantul Regency, Yogyakarta.” This research adds a deeper understanding of the factors that influence the decision to use Islamic banking products. Previous similar studies have highlighted the importance of Islamic financial literacy and product knowledge in the context of using Islamic banking products.

This study complements previous findings by thoroughly considering the influence of the two variables together. The more holistic analysis of this study provides a more complete understanding of financial behavior related to Islamic banking products. By examining Islamic financial literacy and product knowledge in detail, this study has the potential to go deeper in understanding consumer preferences and factors that influence financial decisions related to Islamic banking products. Thus, this study not only complements previous research, but also provides deeper insights into the relationship between Islamic financial literacy, product knowledge, and the decision to use Islamic banking products. The findings are expected to assist Islamic financial institutions in designing more effective educational and promotional programs to increase the acceptance of Islamic banking products in the community as well as in Muhammadiyah University students in South Sulawesi.

CONCLUSION

The conclusions to consider in this study are as follows:

- Islamic financial literacy and product knowledge are important in shaping students’ preferences for Islamic banking products at Muhammadiyah Universities in South Sulawesi. A high level of Islamic financial literacy increases the understanding of Islamic economic principles, strengthening students’ interest in using Islamic banking products.

- This study confirms that Islamic financial literacy significantly influences students’ decisions to use Islamic banking products, and product knowledge also plays an important role in influencing decisions, providing confidence and a better understanding of the benefits and features of Islamic banking products.

- The difference in the influence of Islamic financial literacy and product knowledge on the decision to use Islamic banking products on students at Muhammadiyah Universities in South Sulawesi shows that the two factors have a different but significant impact so that efforts to improve Islamic financial literacy and product knowledge need to be tailored to the characteristics and needs of students to have an optimal effect on increasing their interest and understanding of Islamic banking products.

REFERENCES

- Adiyanto, M. R., Purnomo, A. S. D., & Setyo, A. (2021). The Impact of Sharia Financial Literacy Levels on Interest in Using Sharia Financial Products. Journal of Office Administration, 9(1), 1-12.

- Basori, A., Maslichah, M., & Mawardi, M. C. (2022). Analysis of the Influence of Sharia Financial Literacy on the Decision to Use Sharia Banking Products (Study on Students of the Sharia Banking Study Program Feb Unisma). El-Aswaq: Islamic Economics And Finance Journal, 3(1).

- Bintang, A., Haanurat, A. I., & Rustam, A. (2021). Implementation of PTM Financial Management in Supporting Good University Governance (GUG) at Muhammadiyah Universities in South Sulawesi. COMPETITIVENESS, 10(1), 18-33.

- Djlantik, A. A. M. A., & Anwar, S. (2023). Analysis of the Sharia Financial Literacy Model for the Millennial Generation in Jabodetabek. Scientific Journal of Islamic Economics, 9(2), 2013-2020.

- Dikriansyah, F. (2018). Intisab pui doctrine as a means of strengthening cadre militancy (study of the history of Islamic organizations in West Java) (Bachelor’s thesis, UIN Syarif Hidayatullah Jakarta: Faculty of Adab and Humanities, 2018).

- Fadhilah, L. L. P. (2023). The Influence Of Religiosity, Belief And Product Knowledge On Interest To Apply Sharia Kpr At Bank Syariah Indonesia (Bsi) Kc Madiun Agus Salim ).

- Firdaus, D. F., & Alawiyah, T. (2021). Analysis of Public Knowledge about Sharia Banking. Literate Syntax; Indonesian Scientific Journal, 6(2), 654-663.

- Ghozali, M. (2018). System analysis of sharia financial institutions and conventional financial institutions. IQTISHODUNA: Journal of Islamic Economics and Business, 14(1), 19-21.

- Hasibuan, F. U., & Wahyuni, R. (2020). The Influence of Community Knowledge and Interest in Applying Islamic Values on the Decision to Use Sharia Banking Savings (Case Study of the Langsa City Community). Scientific Journal of Islamic Economics, 6(1), 22-33.

- Hidayat, A., Abdullah, W., Zulfikar, A., & Darussalam, A. (2023, August). The Influence of Sharia Financial Literacy, Lifestyle, and Social Environment on Consumption Patterns with Religiosity as a Moderating Variable. In Proceedings of the Unars National Seminar (Vol. 2, No. 1, Pp. 224-239).

- Harahap, M. A., & Hafizh, M. (2020). The Influence of Sharia Bank Financing, Interest Rates and GDP on the Money Supply in Indonesia. Al-Sharf: Journal of Islamic Economics, 1(1), 64-86.

- Ida, Z. S. (2023). The Influence of Sharia Financial Literacy and Lifestyle on Consumptive Behavior (Study of Prof. Kh Saifuddin Zuhri Purwokerto State Islamic University Students) (Doctoral Dissertation, Uin Prof. Kh Saifuddin Zuhri).

- Indri, A. (2022). Analysis of Financial Literacy and Inclusion in Increasing Interest in Using Sharia Bank Products (Case Study in the Kejobong Village Community, Purbalingga Regency) (Doctoral Dissertation, Uin Prof. Kh Saifuddin Zuhri).

- Inayah, N. (2017). Analysis of Customer Decisions to Save in Sharia Banks (Case Study at Pt Bprs Puduarta Insani) (Doctoral Dissertation, Postgraduate Uin Sumatra Utara).

- Indonesia, S. (2021). Ministry of Religion of the Republic of Indonesia. Al-Qur’an Tajwid and Translation.

- Finance, O. J. (2017). Financial Services Authority. Copy of Financial Services Authority Regulation Number, 65.

- Kurniawati, R., Ahmad, G. N., & Buchdadi, A. D. (2023). Intention to Use Sharia Banks in Generation Z in Indonesia. Management Studies And Entrepreneurship Journal (Msej), 4(5), 7169-7178.

- Kotler, P., & Keller, K. L. (2008). Marketing strategy. In London: London Business Forum.

- Khofifah, S. (2023). The Influence of Financial Literacy and Lifestyle on Student Financial Management (Doctoral dissertation, UIN Sultan Maulana Hasanuddin Banten).

- Luky, T. O. (2022). The Influence of Sharia Financial Literacy, Product Knowledge, and Customer Perceptions on Saving Decisions at Bank Muamalat KCU Purwokerto (Doctoral Dissertation, Uin Prof. Kh Saifuddin Zuhri).

- Melisa, J. (2022). The Influence of Sharia Financial Literacy and Income on the Use of Sharia Banking Products with Religiosity as a Moderating Variable (Case Study at Bprs Bandar Lampung City) (Doctoral Dissertation, Uin Raden Intan Lampung).\

- Nurlaeli, I. (2017). The influence of cultural, psychological, service, promotion and product knowledge factors on customers’ decisions to choose BPRS in Banyumas. Islamadina: Journal of Islamic Thought, 18(2), 75-106.

- Nurlaksita, D. (2018). The Influence of Product Knowledge, Financial Literacy, and Perceptions about Sharia Banks on the Interest of Micro, Small and Medium Enterprises (Mumkm) in Carrying Out Financing in Sharia Banking (Case Study at the Indonesian Santri Entrepreneurs Association (Doctoral Dissertation, Uin Sunan Kalijaga Yogyakarta).

- Nuraini, P., Alfani, M. H., Muyasaroh, N., & Adawiyah, R. (2023). The Influence of Sharia Financial Literacy and Perceptions on Interest in Using Sharia Bank Products. Tabarru’ Journal: Islamic Banking And Finance, 6(1), 291-304.

- Navalia, A. (2023). The Influence of Sharia Financial Literacy and Product Knowledge on the Decision to Save in Sharia Banks with Religiosity as a Moderating Variable (Study of Students at the Faculty of Economics and Islamic Business, Uin Raden Intan Lampung) (Doctoral Dissertation, Uin Raden Intan Lampung).

- Putri, P. H. (2022). The Influence of Sharia Financial Literacy, Trust, and Sharia Services on BSI Savings Preferences. Islamic Economics And Finance In Focus, 1(4), 345-359.

- Pebrianti, A. N. (2023). The Influence of Sharia Financial Literacy, Product Knowledge, and Islamic Branding on the Decision to Become a Customer at a Sharia Bank with Interest as an Intervening Variable (Case Study of the Ngawi Regency Community).

- Pratiwi, N. A. (2023). Analysis of variables that influence the decision to give cash waqf. Islamic Economics And Finance In Focus, 2(1), 13-22.

- Rachmatulloh, D. P. (2020). The influence of sharia financial literacy, religiosity and service quality on the decision to save at sharia banks: Study of the millennial generation in Indonesia (Doctoral dissertation, Maulana Malik Ibrahim State Islamic University).

- Rosdiana, R., & Haris, I. A. (2018). The influence of consumer trust on interest in buying clothing products online. International Journal of Social Science and Business, 2(3), 169-175.

- Rasyid, R. (2012). Analysis of the level of financial literacy of students in the management study program, Faculty of Economics, Padang State University. Journal of Business Management Studies, 1(2).

- Ruwaidah, S. H. (2020). The Influence of Sharia Financial Literacy and Sharia Governance on Students’ Decisions in Using Sharia Banking Services. Muhasabatuna: Journal of Sharia Accounting, 2(1), 79-106.

- Salim, F., Arif, S., & Devi, A. (2022). The Influence of Sharia Financial Literacy, Islamic Branding, and Religiosity on Students’ Decisions in Using Sharia Banking Services. El-Mal: Journal of Islamic Economics & Business Studies, 3(2), 226-244.

- Suarni, A., Jam’an, A., Muchran, M., & Sakti, M. R. P. (2023, December). Financial Literacy and Inclusion of Indonesian Migrant Workers in Tawau Sabah Malaysia. In Proceedings International Conference of Community Service (Vol. 1, No. 2).

- Suarni, A. (2023). Sharia Financial Literacy Level of Muhammadiyah Residents in Sidrap Regency. Indonesian Journal Of Science, Technology And Humanities, 1(2), 62-67.

- Setiawan, S. (2023). The Decision to Become a Sharia Bank Customer: The Role of Sharia Financial Literacy, Trust, and the Image of Sharia Banks. Journal of Applied Islamic Economics and Finance, 3(2), 240-251.

- Silvia, K. I. The Influence of Sharia Financial Literacy and Product Knowledge on the Decision to Save in Sharia Banks with Religiosity as a Moderation (Bachelor’s Thesis, Faculty of Economics and Business, Uin Syarif Hidayatullah).

- Syahputri, K. M., & Dalimunte, A. A. (2023). The Influence of Product Knowledge and Customer Perceptions on Saving Preferences in Sharia Banks with Disposable Income as a Moderating Variable. Economics, Finance, Investment and Sharia (Equity), 4(3), 901-909.

- Sugiyono. (2017). Quantitative Research Methods. Alphabet

- Setiawan, S. (2023). The Decision to Become a Sharia Bank Customer: The Role of Sharia Financial Literacy, Trust, and the Image of Sharia Banks. Journal of Applied Islamic Economics and Finance, 3(2), 240-251.

- Tesya, A. (2023). The Influence of Product Knowledge, Brand Image and Brand Trust on Customer Loyalty of Bank Syariah Indonesia in Tanggamus Regency (Doctoral Dissertation, Uin Raden Intan Lampung).

- Thohari, C., & Hakim, L. (2021). The Role of Religiosity as a Moderating Variable in Sharia Banking Learning, Sharia Financial Literacy, Product Knowledge on Saving Decisions in Sharia Banks. Journal of Accounting Education (Jpak), 9(1), 46-57.

- Yuda, P. (2021). Analysis of the Influence of Sharia Financial Literacy on Customer Decisions to Use Sharia Banking Products (Study at Bank Bsi in Kotabumi, North Lampung) (Doctoral Dissertation, Raden Intan State Islamic University, Lampung).

- Zuhirsyan, M., & Nurlinda, N. (2021). The Influence of Religiosity, Customer Perceptions and Motivation on the Decision to Choose Sharia Banking. JPS (Journal of Sharia Banking), 2(2), 114-1.