Unveiling the Motivations Behind Malaysian Taxpayer Participation in Voluntary Disclosure Programme

- Noraza Mat-Udin

- Balamurugan Sinapayan

- 870-881

- Jan 4, 2024

- Peace and Conflict Studies

Unveiling the Motivations Behind Malaysian Taxpayer Participation in Voluntary Disclosure Programme

Balamurugan Sinapayan1, Noraza Mat-Udin2*

1Inland Revenue Board of Malaysia, Johor Bahru

2Tunku Putri Intan Safinaz School of Accountancy, Universiti Utara Malaysia

*Corresponding Author

DOI: https://dx.doi.org/10.47772/IJRISS.2023.7012065

Received: 16 December 2023; Accepted: 19 December 2023; Published: 03 January 2024

ABSTRACT

In the pursuit of enhanced tax compliance, voluntary disclosure programmes (VDP) serve as valuable tools when executed effectively. This study delves into tax professionals’ perspectives on factors influencing taxpayer participation in Malaysia’s VDP when first introduced in 2015 to boost revenue and compliance. This survey of 135 tax practitioners from prominent firms in Johor Bahru and Kuala Lumpur sheds light on critical VDP participation drivers. The findings indicate that the VDP’s success hinges on several factors. Foremost among these is the size of penalty reduction, which holds the greatest sway in motivating participation. Following closely is the apprehension of further audits, while fear of detection and punishment ranks third. The efforts made by the Inland Revenue Board of Malaysia in promoting the VDP emerge as the fourth significant driver. This study, among the first to explore VDP implementation in Malaysia, anticipates inspiring future research and policy refinements in the realm of tax compliance.

Keywords: voluntary disclosure programme, tax amnesty, participation, tax professional, tax compliance

INTRODUCTION

As tax administrators continually seek to enhance tax compliance through more efficient enforcement activities, the implementation of voluntary disclosure programmes (VDP) emerges as a promising tax policy strategy to effectively expand the tax base. This paper delves into the multifaceted realm of VDPs, offering insights into their potential efficacy when meticulously executed. Furthermore, it emphasizes the pivotal role of public participation in ensuring the successful implementation of such programmes. A voluntary disclosure programme (VDP), also known as a tax amnesty, extends an opportunity to taxpayers to rectify errors or omissions in their previous tax returns while granting partial or full waivers of financial penalties and criminal prosecutions. It is regarded as an integral component of tax administrators’ compliance strategies, enabling previously non-compliant taxpayers to regularize their tax affairs, subject to the terms outlined in the programme (OECD, 2015).

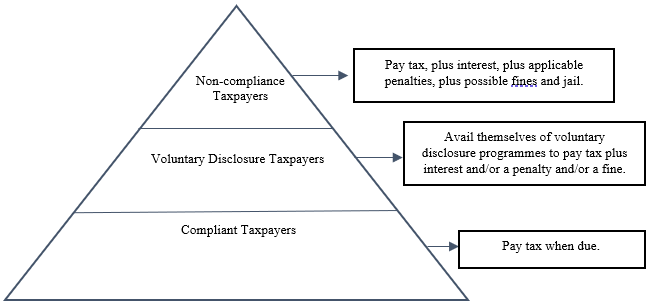

Presently, about 50 countries around the world offer VDPs. While the scope of these programmes may vary from one country to another in terms of coverage and incentives, their widespread existence underscores their importance as a low-cost tax compliance initiative for tax administrators. Beyond swiftly boosting revenue in the short term, a well-structured VDP can significantly expand the tax base by identifying taxpayers situated in the middle stratum of the compliance pyramid, as depicted in Figure 1.

Fig. 1. The Compliance Pyramid & Voluntary Disclosure (Source: OECD, 2015)

In Malaysia, the Inland Revenue Board of Malaysia (IRBM) has consistently rewarded taxpayers who proactively rectify their tax affairs before the commencement of audit or investigation activities, offering reduced penalty rates ranging from 10% to 35% as compared to the 45% to 300% penalty rates applied during audits or investigations. In addition to the permanent voluntary disclosures outlined in the tax audit framework, IRBM introduced special VDPs in 2015/2016 and 2018/2019. These programmes encompassed various direct taxes administered by the IRBM, including corporate tax, petroleum tax, individual tax, stamp duty, and real property gains tax. The key elements of these programmes are summarized in Table 1 and Table 2.

Table 1. Penalty Rates Under Special Vdp Implemented In Year 2015 & 2016

| Penalty Regime | Reduced penalty rates (VDP) |

| Incorrect returns:

Voluntary Disclosure |

15% |

| Incorrect returns:

Discovery by IRBM during an audit/investigation |

25% – Full Payment

35% – Payment in 6 Instalments 45% – More than 6 Instalments |

| Tax in arrears | Waiver for increase in tax if full settlement |

Source: Operational Guidelines No. 1/2015 & No.1/2016 issued by IRBM on 05 March 2015 and 10 February 2016 respectively.

Table 2. Penalty Rates Under Special Vdp Announced In 2019 Budget

| Categories of Voluntary Disclosure | Period of SVDP and Penalty rate | |

| 03/11/2018-30/06/2019 | 01/07/2019-30/09/2019 | |

| Under-declared income and over-claimed expenses/ reliefs/deductions/rebates, under Income Tax Act 1967, Petroleum Income Tax Act 1967 and Real Property Gains Tax Act 1976. | 10% | 15% |

| Unstamped instruments | 10% or a minimum of RM50 | 15% or a minimum of RM100 |

Source: Operational Guidelines No. 1/2019 issued by IRB on 24 April 2019.

The tax amnesty programme in 2019, characterized by a comparatively reasonable penalty rate of 10% (in contrast to previous rates of 25%), garnered substantial attention. However, it fell short of its initial target of collecting RM10 billion from one million taxpayers (“IRB Collects RM10.1mil”, 2019). The IRBM’s chief reported that the 2019 SVDP collected RM7.88 billion from 286,428 contributors, including 11,176 new taxpayers (Hamdan, 2020). This discrepancy between the target and the actual collection persisted despite the extension of the programme for an additional three months to encourage taxpayer participation.

One of the primary objectives of tax amnesty programmes is to bring tax evaders back into the formal tax system, thereby reducing the shadow (underground) economy. However, in Malaysia, despite intensive government promotion of the amnesty, there is no discernible reduction in the shadow economy. Shortly after the amnesty programme, data released by the Ministry of Finance in January 2020 indicated that the shadow economy in Malaysia accounted for 21% of GDP, approximately RM300 billion. This suggests that there has been limited engagement with the Malaysian amnesty programmes. Nonetheless, the persistent demand for such programmes, as exemplified by proposals from renown tax experts underscores the potential of VDPs as effective compliance strategies to narrow the reported tax gap in Malaysia. Successful implementation, especially among taxpayers within the middle segment of the compliance triangle (as illustrated in Figure 1), is pivotal for the future of VDPs.

While VDPs are applicable to all taxpayer groups, they may be especially relevant to business taxpayers (self-employed and companies), as they possess greater opportunities to underreport income and submit incorrect returns. This aligns with the focus of many Malaysian tax compliance studies that have predominantly examined business taxpayers due to their significant non-compliance tendencies. Remarkably, there is currently limited published research on VDPs in Malaysia. Overseas studies on VDPs or tax amnesties have primarily concentrated on their effects on government revenue and future compliance levels. However, there is a dearth of information regarding the motivations or impediments to taxpayer participation in VDPs. Thus, investigating the reasons for participation among taxpayers, particularly from the perspective of tax professionals in Malaysia, is paramount.

This study not only aims to highlight valuable insights for tax administrators regarding the potential reduction of the tax gap without incurring additional administrative costs but also addresses the deficiencies in existing VDPs and offers recommendations from respondents to enhance their effectiveness. Such feedback will prove invaluable for the tax authority in evaluating past VDPs and incorporating tax professionals’ perspectives into future iterations of the programme. Furthermore, as this study was conducted after the first introduction of VDP in Malaysia, it contributes to the literature on VDPs and tax amnesty by shedding light on their uncharted territory in Malaysia. It serves as an initial effort to deepen understanding of Malaysian VDPs, particularly the motivations driving taxpayer participation. This enhanced comprehension holds the potential to stimulate further research in the field of VDPs in Malaysia, as well as contribute to the broader discourse on tax compliance by identifying the reasons behind taxpayers’ decisions to rectify their tax affairs.

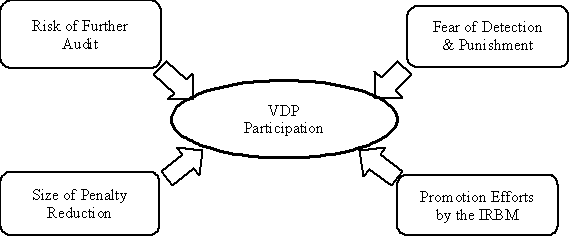

To gather insights into the reasons for taxpayer participation in the VDP introduced by the IRBM, this study seeks the perspectives of tax professionals employed at prominent firms. Questionnaires were employed to solicit their opinions on four factors that motivate VDP participation: the size of penalty reduction, fear of detection and punishment, risk of further audit, and promotional efforts by tax authority. This study is marking the initial attempt to examine the reasons for VDP participation in Malaysia. This paper is arranged in sequence subtopics which cover literature review, research methodology, results and findings, discussion of findings and it ends with a conclusion.

LITERATURE REVIEW

Tax amnesties have been recognized as moderately effective strategies for tax revenue collection (Fisher et al., 1989; Alm and Beck, 1993). However, the success of these programmes largely depends on taxpayer participation. Notably, despite the substantial body of research on tax amnesties, there is a notable gap in understanding the factors that motivate taxpayers to participate in such programmes. A study by Alm (1991) suggests that one primary reason for individuals to comply with the tax law is the fear of detection and subsequent punishment. Thus, in terms of participation in the tax amnesty programme, this factor relates to the view that an efficient tax audit and investigation system creates a deterrent effect thus, encouraging taxpayers to take advantage of amnesty opportunities (Alm et. al., 1990). Earlier, Fisher et al., (1989) categorized amnesty participants as those who perceive a significant increase in the likelihood of detection or penalties being imposed. However, some studies challenge this notion. Wang and Hsieh (2015) and Bayer, Oberhofer, and Winner (2014) argue that detection probability and post-amnesty enforcement levels do not necessarily correlate with amnesty participation. These studies suggest that taxpayers may opt for amnesty despite low exogenous variables, such as the penalty rate or the probability of tax evasion activities being discovered.

Besides fear of detection and punishment, Ross and Buckwalter (2013) identified strategic delinquency as another motivator for participating in tax amnesties. Some taxpayers delay their tax payments in anticipation of an amnesty programme, hoping to benefit from interest gains. This behavior is driven by the discrepancy between the penalty rate faced individually and the rate offered during a tax amnesty. The size of penalty reduction or incentives provided during an amnesty programme is another aspect that is believed to be driving taxpayers to participate in VDP. When the total tax liability, including penalties, exceeds the value of the taxpayer’s assets, participation becomes less appealing (OECD, 2015). Farrar and Hausserman (2016) also found that the size of the penalty reduction plays a crucial role in taxpayers’ decision-making regarding amnesty participation. Similarly, Mahestyanti, Juanda, and Anggraeni (2018) concluded that amnesty participation in Indonesia was highest during the initial three months when the tariff rates were at their lowest.

The fear of additional audits may discourage taxpayers from voluntary disclosures. OECD (2015) reported that many taxpayers are concerned that disclosure during an amnesty programme may lead to further audits either immediately or in the future. To address this concern, tax administrators must assure taxpayers that disclosures made during amnesty programmes will not trigger future compliance activity. Marchese (2014) suggested limiting or excluding auditing powers to boost participation in tax amnesties.

Guilted cognitions also play a role in the decision to participate in tax amnesty programmes. Farrar et al. (2016) examined the impact of guilt on tax amnesty disclosure decisions. They found that individuals are more likely to make amnesty disclosures when they take personal responsibility for their transgressions, can justify them, and foresee the negative consequences arising from those offences. Personal responsibility appears to be a significant factor in motivating taxpayers to come forward and admit their mistakes.

Marketing campaigns and public awareness efforts are essential components of successful tax amnesty programmes. Studies by Mikesell (1984, 1986), Parle and Hirlinger (1986), Ross and Buckwalter (2013), and Ross (2012) emphasize the importance of effectively communicating the goals and benefits of an amnesty programme to the targeted participants. Publicity should convey a positive image of the programme and provide a clear appeal to potential participants.Tax amnesty programmes can also be motivated by international opportunities. Firms seeking to benefit from economic growth, liberalization policies, and international trade openings are incentivized to participate in amnesties. A clean tax record is often a prerequisite for accessing credit and international markets. Thus, tax amnesty programmes attract tax evaders looking to expand their businesses globally (Marchese, 2014). Additionally, if globalization significantly impacts taxpayer income, tax amnesty can serve as an opportunity for legalizing business activities (Bose and Jetter, 2012).

It is important to note that not all amnesty participants are tax evaders. Honest taxpayers may also seek amnesty to rectify unintentional errors or omissions in their previous returns and avoid potential audits (Marchese, 2014).

METHODOLOGY

A conceptual framework based on the factors that believed to be contributing to VDP participation in Malaysia is suggested as depicted in Figure 2.

Fig. 2. Proposed Conceptual Framework for Reasons Contribute to VDP Participation

Questionnaire Development, Pretesting and Pilot Test

The questionnaire used in this study has been meticulously developed to facilitate accurate and straightforward responses. It was developed to include factors relevant to the Malaysian tax system and environment through discussions with tax experts, including senior tax officers and practitioners. The chosen factors for in-depth study include the size of penalty reduction, fear of detection and punishment, risk of further audit, and promotional efforts by tax authority. As recommended by Chen, Paulraj, and Lado (2004), questionnaires require pretesting before the data collection process to validate their content. Consequently, the questionnaire was distributed to tax experts, including professionals and academics, to ensure that the statements were understandable and relevant to the research questions. The suggestions and amendments regarding wording have been incorporated into the final draft of the questionnare. In addition to pretesting, a pilot test was conducted to enhance reliability of the questionnaire before the actual data collection. Positive feedback was received from the pilot test respondents. Reliability tests were conducted yielding Cronbach’s Alpha coefficients within the range of acceptable values.

Population and Sampling Method

The study’s population comprised tax professionals in Malaysia, including registered tax agents, tax preparers, tax accountants, in-house tax accountants, and self-employed individuals. This definition of tax professionals was adapted from previous studies (Roth, Scholz & Witte, 1989; Marshall, Smith & Armstrong, 1997). Eligibility criteria were defined to specify the characteristics required for individuals to be considered participants in the study. In this study, participants must have worked in the field of Malaysian taxation, specifically in preparing tax returns and providing tax-related advice to their clients (taxpayers).

This study employed a purposive sampling method which allows for using judgment to identify suitable samples. This method is particularly valuable for evaluating newly incorporated questionnaires, especially when the researcher seeks a sample of experts. Tax professionals from the Big Four tax firms in Klang Valley and Johor Bahru were identified. These professionals handle the highest number of clients and possess extensive knowledge of tax policies and programmes implemented by the IRBM. For example, Ernst and Young Malaysia published an article titled “Tax Amnesty: Reduction and Waiver of Tax Penalties” (Ernst & Young, 2016), demonstrating the pivotal role tax practitioners play in helping businesses understand the functions and benefits of VDP.

RESULTS AND FINDINGS

Response Rate and Respondents’ Profile

Out of the 160 questionnaires distributed, 135 were successfully completed and returned, resulting in a response rate of 84.4%. This response rate is considered very good for analysis and reporting (Babbie, 2007). Most of the respondents, certified tax professionals, held a first degree as their highest qualification, with only three having diploma qualifications. Specifically, 85 respondents held degrees, 45 had professional qualifications, and two held master’s degrees. Additionally, 53.3% of the respondents were from Johor Bahru, while 46.7% were from Kuala Lumpur. Concerning work experience, 51% had 1 to 5 years of experience, 17% had 5 to 10 years, and 31% had more than 10 years of experience in taxation. Thirty-six percent i.e., 48 of the respondents had experience in handling VDP cases, while 87, equivalent to 64%, had never handled VDP cases before.

Reliability and Validity Analysis

To assess the internal consistency of the items in each variable, Cronbach’s alpha was used, and the results are presented in Table 1. The minimum reliability scores in this study exceeded 0.7, indicating satisfactory reliability for all instrument variables (factors).

Table 1. Reliability Analysis of Variables (N=135)

| Variables | No. of items | Cronbach’s Alpha |

| Size of Penalty Reduction | 3 | 0.734 |

| Fear of Detection & Punishment | 3 | 0.872 |

| Risk of Further Audit | 3 | 0.812 |

| Promotion efforts by the IRBM | 3 | 0.841 |

The KMO values for all variables exceeded 0.650 (Table 2), surpassing the suggested minimum value of 0.60. Additionally, Bartlett’s sphericity test values for all variables were statistically significant (P=.000). The total variance explained for all factors ranged from 63.18% to 69.71%, which is considered good (Stevens, 2002).

Table 2. Factor Analysis (N=135)

| Variables | No. of

Items |

No. of

Factors |

KMO

|

Variance Explained (%) |

| Size of Penalty Reduction | 3 | 1 | 0.676 | 69.71 |

| Fear of detection and Punishment | 3 | 1 | 0.688 | 67.59 |

| Risk of Further Audit | 3 | 1 | 0.651 | 63.18 |

| Promotion Efforts by the IRBM | 3 | 1 | 0.642 | 63.71 |

The rotated component matrix (Table 3) was used to interpret categories or reasons for all items measured in this study. The results confirmed construct validity for all four reasons and validated the items used to measure each reason.

Table 3. Rotated Components Matrix (N=135)

| Items | Components | |||

| 1 | 2 | 3 | 4 | |

| Penalty Reduction Important | .782 | |||

| Penalty Structure Attractive | .826 | |||

| VDP Effective If Size Reduction Higher | .827 | |||

| Detect Mistakes Low | .789 | |||

| Greater Fear Participate | .849 | |||

| IRBM Enforcement Enhanced | .808 | |||

| Further Audit In VDP | .813 | |||

| Further Audit Discourage | .855 | |||

| If NO Further Audit More Taxpayers Will Participate | .647 | |||

| VDP Promoted Intensively to Taxpayers | .763 | |||

| Taxpayers Well Aware | .866 | |||

| The IRBM Should Increase Promotion | .743 | |||

Table 4 shows that the mean scores for all items were above 4.00, indicating a strong agreement with the statements. Respondents perceived that the size of penalty reduction is significant in VDP implementation, as the current penalty structure offered by IRBM was not attractive to taxpayers. Ideally, they believe that VDP in Malaysia would be more successful with higher penalty reduction. The small standard deviations for all the statements indicate that the results closely align with the mean.

Table 4. Size Of Penalty Reduction (N=135)

| No. | Size of Penalty Reduction | Mean | Std. Deviation |

| 1 | The Size of Penalty Reduction is Important in VDP Implementation. | 4.36 | 0.674 |

| 2 | Current Penalty Structure offered by IRBM for VDP failed to Influence more Taxpayers to Participate. | 4.07 | 0.745 |

| 3 | VDP in Malaysia will be more Effective if the size of Penalty Reduction is Higher. | 4.35 | 0.795 |

Fear of Detection and Punishment

Based on the results presented in Table 5, the mean value of 3.01 suggests that tax professionals maintain a neutral perspective regarding the probability of omission/error detection by IRBM. However, mean values above 3.5 for items two and three indicate their agreement with these statements. In other words, although tax professionals are unsure about IRBM’s detection probability, they believe that enhancing IRBM’s enforcement activities will encourage more taxpayers to participate in VDP due to the fear of detection and punishment. The small standard deviations for all the items indicate that the data is clustered around the mean.

Table 5. Fear Of Detection and Punishment (N=135)

| No. | Fear of Detection and Punishment | Mean | Std. Deviation |

| 1 | The Probability to Detect Mistakes/Omissions by the IRBM is Low.. | 3.01 | 0.617 |

| 2 | Taxpayers who have Greater Fear of Detection will likely Participate in VDP. | 3.82 | 0.818 |

| 3 | Taxpayers will Participate in VDP if IRBM Enforcement Activities are Enhanced. | 3.79 | 0.793 |

Risk of Further Audit

Table 6 shows mean values of 4.00 and above for all items, indicating that the risk of further audit is an important factor. Tax professionals foresee that IRBM will further audit the voluntary disclosures made by taxpayers, which discourages them from participating in VDP. Therefore, they agree that VDP participation would increase if IRBM accepts voluntary disclosures of past omissions without further checking. The low standard deviation shows that tax professionals’ responses are concentrated around the mean score.

Table 6. Risk Of Further Audit (N=135)

| No. | Risk of Further Audit | Mean | Std. Deviation |

| 1 | IRBM will Further Audit the Voluntary Disclosures submitted by Taxpayers in VDP. | 4.13 | 0.786 |

| 2 | The Fear of Further Audit Discourages Taxpayers from Participating in VDP. | 4.17 | 0.739 |

| 3 | If IRBM accepts the Disclosures made by Taxpayers without Further Audit, More Taxpayers will Participate in VDP. | 4.37 | 0.741 |

Promotion Efforts by the IRBM

As demonstrated in Table 7, in terms of promotion efforts on VDP, tax professionals disagreed that IRBM had promoted VDP sufficiently to taxpayers, indicating that taxpayers were not aware of VDP. Consequently, they agreed that IRBM should increase promotion of the VDP to attract and encourage more taxpayers to participate. Similar to other reasons, a low standard deviation for all the items indicates that the scores are close to the average (mean).

Table 7. Promotion Efforts by Irbm (N=135)

| No. | Promotion efforts by the IRBM | Mean | Std. Deviation |

| 1 | VDP has been Promoted Intensively to Taxpayers. | 2.82 | 0.863 |

| 2 | Taxpayers are well Aware of VDP Implemented the IRBM. | 2.70 | 0.829 |

| 3 | IRBM should Increase Promotion of the VDP in order to Attract and Encourage Taxpayers to Participate. | 3.89 | 0.789 |

Ranking of the Reasons Contributing to VDP Participation

Based on the mean values obtained from data analysis, the reasons for VDP participation were ranked as shown in Table 8. The size of penalty reduction had the highest ranking, followed by the risk of further audit, both with mean values above 4.00 for all the statements. Fear of detection and punishment was ranked as the third important reason contributing to VDP participation, and lastly, promotion efforts by IRBM with a total mean value of 9.41.

Table 8. Ranking Of Reasons

| Reasons Contributing to VDP Participation | Mean value | Ranking |

| Size of Penalty Reduction | 12.77 | 1 |

| Risk of Further Audit | 12.67 | 2 |

| Fear of Detection and Punishment | 10.62 | 3 |

| Promotion Efforts by IRBM | 9.41 | 4 |

DISCUSSIONS OF FINDINGS

The primary objective of this study was to determine tax professionals’ perceptions of the reasons contributing to taxpayer participation in VDP. Tax professionals generally agreed that all the listed reasons contribute to VDP participation, although the level of agreement for each factor differed. Size of Penalty Reduction recorded the highest mean value (12.77), indicating that monetary incentives provided under VDP, particularly a reduction in penalties, are the main attraction influencing taxpayers’ decisions to disclose past omissions. This result aligns with standard tax-evasion theory, predicting that rational taxpayers participate in VDP or amnesty disclosure programmes if enforcement, penalty, or tax parameters are adjusted in a way that provides extra incentives (Alm & Beck, 1991). Tax professionals have suggested as follows:

“VDP rate should be around 0-5% to attract taxpayers to disclose their omissions or error. If the IRB did not pick up the case, the tax will never be collected. However, if the VDP rate is zero, it will encourage the taxpayer to admit their mistakes and remit the additional tax to IRB.”

“There should be an “incentive” for companies to opt for VDP. The differential in penalty rate is not attractive as taxpayers are exposed to risk of audit of VDP cases in future.”

“To only penalise if the additional tax payable based on the voluntary disclosure exceed 10% of the initial assessment submitted by taxpayer.”

Risk of Further Audit had a high mean value (12.67) and was ranked second, suggesting that many taxpayers in Malaysia are concerned that their disclosures under VDP will lead to further audits by IRBM. This risk becomes a major deterrent to VDP participation. To mitigate this issue, OECD suggested issuing clear guidance on VDP to assure the public that disclosures during VDP are confidential and will not affect future compliance activities (OECD, 2015). Marchese (2014) also emphasized excluding or limiting auditing powers during VDP to encourage taxpayer participation. This argument is supported by tax professionals as they commented as follows:

“IRBM should not classify VDP participants as their focused group of tax defaulters. They should be treated as other compliant taxpayers for future audit activities.”

“IRBM should not open back the assessment for the years which taxpayers opt to disclose under VDP.”

Fear of Detection and Punishment, ranked third with a cumulative mean value of 10.62, indicates that taxpayers who fear detection and punishment are more likely to participate in VDP, even if tax professionals are uncertain about IRBM’s future audit probability. This result supports previous studies highlighting the role of detection probability and fear of punishment in making VDP attractive to tax evaders (Alm, 1991; Fisher et al., 1989; Graetz and Wilde, 1993; Bayer et al., 2014).

Promotion Efforts by IRBM had a moderate level of agreement with a total mean value of 9.41. Tax professionals believed that many taxpayers were not aware of VDP, and therefore, they suggested increasing promotional efforts to attract and encourage participation. This aligns with overseas studies that emphasized the importance of promotion to reach targeted participants (Parle & Hirlinger, 1986; Mikesell, 1986; Ross & Buckwalter, 2013). In order to ensure the implementation and advantage of VDP reach the targeted taxpayers and tax defaulters, tax professionals have given the following suggestion.

“IRB should organize more campaigns and increase the range of publicity to let more people know about VDP through social media, IRB talk show and other main TV channels.”

CONCLUSION

This study examined the reasons contributing to taxpayer participation in Malaysian VDP from the perspective of tax professionals, shedding light on the significance of penalty reduction, fear of detection and punishment, risk of further audit, and promotion efforts. The findings of the study have been recommended to the IRBM for future decision-making process and policy making. The outcome of the study is seen to have been considered under the Special VDP 2.0 which had been launched recently starting from 1 June 2023 until 31 May 2024. The size of penalty has been reduced to 0% of which remarks a 100% waiver. In terms of the concern on risk of further audit, the Government has assured that there will be no further audit and investigation as the disclosure is treated as acceptance in good faith. However, taxpayers are reminded that they will be subjected to penalty after the Special VDP 2.0 as specified in the existing rulings. With regards to publicity effort, apart from issuing guidelines on the IRBM website i.e., Operational Guidelines No. 2/2023 issued on 22 August 2023 and announcement made during the Budget speech, a proper press release has been arranged which covered by all media so as to reach as many people as possible besides roadshows by the IRBM itself to boost taxpayers’ participation in the programme.

While this study has some limitations, including its focus on tax professionals’ perspectives, it contributes valuable insights into the Malaysian tax system context. Future studies should consider a broader range of stakeholders’ views such as taxpayers and IRBM staff and explore additional aspects contributing to VDP participation. In order to enrich and provide a broader or global perspective on motivations to participate in VDP or similar programmes, future studies could consider conducting cross-cultural comparative studies that may reveal commonalities and differences influenced by cultural and contextual factors in various countries. The questionnaire used was self-developed, while validity was tested, there is room for improvement to measure reasons more accurately in different research settings. Furthermore, as there is no published literature available on VDP in Malaysia during this study was conducted, comparisons with other studies were made using different VDP designs and tax laws. In conclusion, VDP is a promising tax policy in Malaysia that can enhance tax compliance and administration if executed carefully. This study examined the reasons for taxpayer participation in VDP from the perspective of tax professionals. The findings highlight the importance of penalty reduction, fear of detection and punishment, risk of further audit, and promotion efforts by the IRBM in influencing taxpayer decisions to participate in VDP. While this study has limitations, it provides valuable insights into the Malaysian tax system context, laying the foundation for future research in this area.

REFERENCES

- Alm, J. (1991). A perspective on the experimental analysis of taxpayer reporting. The Accounting Review. 66(3), 577-593.

- Alm, J., & Beck, W. (1993). Tax amnesties and compliance in the long run: A time series analysis. National Tax Journal, 46(1), 53-60.

- Alm, J., McKee, M. and Beck, W. (1990). Amazing grace: tax amnesties and compliance. National Tax Journal, 43(1), 23-37.

- Babbie, E. (2007). The practice of social research (11th Ed.). Belmont, CA: Thomson Wadsworth.

- Bayer, R.C., Oberhofer, H., & Winner. H. (2014). The occurrence of tax amnesties: theory and evidence. Working Paper in Economic and Finance 06, Austria: University of Salzburg.

- Bose, P., &Jetter, M. (2012). Liberalization and Tax Amnesty in a Developing Economy. Economic Modelling, 29, 761-765.

- Chen, I.J., Paulraj, A. &Lado, A.A. (2004). Strategic purchasing, supply management and firm performance, Journal of Operations Management, 22(5), 505-523.

- Ernst and Young (2016). Tax Amnesty 2016: Reduction and waiver of tax penalties. Retrieved: https://www.ey.com/Publication/vwLUAssets/ey-take-5-tax-amnesty.

- Faith, O., Lu, S.G., & Kurlu, E.C.A.S. (2011). Tax amnesty with effects and effecting aspects: tax compliance, tax audits and enforcements around; The Turkish Case. International Journal of Business and Social Science, 2(7), 3-4.

- Farrar, J. & Hausserman, C. (2016). An exploratory investigation of extrinsic and intrinsic motivations in tax amnesty decision-making. Journal of Tax Administration, Vol. 2(2), 47-66.

- Farrar, J., Hausserman, C., & Dunn, P. (2016). The influence of guilt cognitions on taxpayers’ voluntary disclosures. Business Faculty Publications and Presentations, 39.

- Fisher, R. C., Goddeeris, J. H., & Young, J. C. (1989). Participation in tax amnesties: the individual income tax. National Tax Journal, 42(1), 15-27.

- Graetz, M.J. and L. Wilde (1993). The decisions by nonfilers to participate in income tax amnesties, International Review of Law and Economics 13, 271–283.

- Hamdan, M.A. (2020, February 18). IRB collected RM7.9b via voluntary disclosure programme, says CEO. The Edge Malaysia. https://theedgemalaysia.com/article/irb-collected-rm79b-voluntary-disclosure-programme-says-ceo

- IRB collects RM 10.1mil under voluntary declaration programme. (2019, January 4). The Star. https://www.thestar.com.my/business/business-news/2019/01/04/irb-collects-rm-10mil-under-voluntary-declaration-programme/

- Mahestyanti, P., Juanda, B., & Anggraeni, L. (2018). The determinants of tax compliance in tax amnesty programs: experimental approach. Etikonomi: Jurnal Vol. 17 (1): 93 – 110. doi: http//dx.doi.org/10.15408/etk.v17i1.6966.

- Marchese, C. (2014). Tax amnesties. Italy: IEL paper in Comparative Analysis of Institutions, Economics and Law No.17.

- Marshall, J. R., Smith, M., & Armstrong, R. W. (1997). Self-assessment and tax audit lottery: The Australian Experience. Managerial Auditing Journal, 12(1), 1-8.

- Mikesell, J.L. (1984).Tax Amnesties as a tool for revenue administration. State Government 57, 114–20.

- Mikesell, J.L. (1986). Amnesties for state tax evaders: the nature of and response to recent programs. National Tax Journal 39, 507–525.

- OECD (2015). Update on voluntary disclosure programs: A pathway to tax compliance. OECD, August 2015. Retrieved from http://www.oecd.org/ctp/exchange-of-taxinformation/Voluntary-Disclosure-Programmes-2015.pdf.

- Parle, W.M. and Hirlinger, M.W. (1986).Evaluating the use of tax amnesty by state governments. Public Administration Review, 46(3), 246-255.

- Ross, J.M. (2012). Local government property tax amnesty programs: structures and themes. Public Finance and Management, 12(2) 146-173.

- Ross, J.M., &Buckwalter, N.D. (2013). Strategic tax planning for state tax amnesties: evidence from eligibility period restrictions. United State: Indiana University Bloomington.

- Roth, J. A., Scholz, J. T., & Witte, A. D. (1989). Taxpayer compliance: An Agenda for research. In (Vol. 1): University of Pennsylvania Press.

- Stevens, J. P. (2002). Applied multivariate statistics for the social sciences (4th Ed.). Hillsdale, NS: Erlbaum.

- Wang, Y. K. and Hsieh, W. J. (2015). Is tax amnesty good for the tax evader? Taiwan: British Journal of Economics, Management & Trade, 6 (4), 308-322.