A Substantive Theory Explaining Namibian Employers’ Tax Compliance Behaviour towards Employee Taxes

- Zelda van der Walt

- Marina Bornman

- Grietjie Verhoef

- 151-166

- Mar 27, 2025

- IJRSI

A Substantive Theory Explaining Namibian Employers’ Tax Compliance Behaviour towards Employee Taxes

Zelda van der Walt1, Marina Bornman2, Grietjie Verhoef3

1Faculty of Commerce, Human Sciences and Education, Namibia University of Science and Technology, Namibia

2,3College of Business and Economics, University of Johannesburg, South Africa

DOI: https://doi.org/10.51244/IJRSI.2025.12030011

Received: 12 February 2025; Accepted: 21 February 2025; Published: 27 March 2025

ABSTRACT

Studies on tax compliance behaviour seek to identify the key determinants and frameworks for the compliance decision. These studies primarily explain the compliance decisions of tax-liable persons regarding their own taxes. However, compliance behaviour relating to employers’ withholding and remitting employees’ taxes may be more complex than the conduct of individuals regarding their own taxes. Few studies have investigated the compliance decisions of employers regarding withholding and remitting taxes on behalf of employees.

In this study, using a grounded theory (GT) approach, a systematic analysis of Namibian employers in micro, small and medium enterprises (MSMEs) attitude towards employee taxes forms the basis for developing a substantive theory explaining employers’ compliance behaviour regarding their statutory obligation towards employee taxes. The results show that employers’ compassion towards employees, moral values, upbringing and religion, lack of tax knowledge, and the power of the tax authority are the core variables influencing their compliance decisions. These results advance the understanding of employers’ compliance behaviour and may assist tax authorities’ efforts in encouraging compliance behaviour towards employee taxes.

Keywords: Micro, small and medium enterprises, employee taxes, compliance, employers, compassion, moral values, upbringing and religion, the power of the tax authority, lack of tax knowledge, grounded theory.

INTRODUCTION

Taxes are essential for income and wealth redistribution, public goods and services provision, stabilising and harmonising the economy, and regulating and promoting socio-economic welfare. The tax compliance literature suggests that taxpayers in countries that are not fully democratic may even be less compliant than those in fully democratic countries (Braithwaite, 2003; Kirchler, Hoelzl & Wahl, 2008; Gangl, Torgler, & Kirchler, 2016). This observation has an essential bearing on tax compliance in Namibia, as the democracy index of 2020 categorises Namibia’s democracy status as Deficient (Universität Würzburg, 2020).

Contrary to the common belief that taxation solely pertains to economics and fiscal policy, it represents a complex socio-economic phenomenon. Research analysing and explaining tax compliance behaviour draws on perspectives that range from traditional economic approaches to more contemporary views that incorporate sociological and psychological explanations of compliance behaviour (see Allingham & Sandmo, 1972; Feld & Frey, 2007; Kirchler, 2007; Braithwaite, Murphy, and Reinhart, 2007).

In an effort to identify the key determinants and frameworks for compliance decisions, studies on tax compliance behaviour predominantly elucidate the choices of tax-liable individuals regarding their taxes. Many of these studies conclude with strategies to encourage voluntary compliance (Allingham & Sandmo, 1972; Jackson & Milliron, 1986; Chau & Leung, 2009; Kołodziej, 2021). However, few studies have explored individuals’ compliance decisions concerning the withholding and remittance of taxes on behalf of others. One such study, focusing on a third-party reporting context, examined the compliance behaviour of firms acting as third parties that report income on behalf of individuals (Klevin, Kreiner, and Saez, 2009). The study found that a combination of verifiable accounting records and a substantial workforce is vital for the success of third-party tax enforcement. Nevertheless, their research has been primarily theoretical and did not address the attitudes and perceptions of employers concerning their compliance decisions regarding employee taxes.

The commissioner of the Namibia Revenue Agency (NamRA), Mr Sam Shivute, notes that tax compliance in Namibia is notably low, as not everyone declares the amounts they are obligated to pay (Amukeshe, 2021). Given the low compliance observed by NamRA, Namibia’s fiscal capacity may be considered inadequate.

Employers are ultimately responsible for deducting and remitting PAYE in countries such as Zambia and Kenya (Section 71 (1) of the ITA, Zambia; Section 37 of the Income Tax Act 8 of 1991, Kenya). However, the current practice of the Namibian tax authority places the burden of unpaid employee taxes on the employee. Paragraph 5(2) of Schedule 2 of the Namibian Income Tax Act No. 24 of 1981 allows an employer to transfer the liability for unpaid employee taxes to the employee (Income Tax Act 24 of 1981). Consequently, the effect of unpaid employee taxes is ultimately greater for the employee than for the employer.

Furthermore, employees in countries such as the UK and USA are encouraged to ensure the proper deduction and remittance of PAYE, as this influences their eligibility for certain public benefits (IRS, 2021; HMRC, 2022). Namibian employees do not experience this motivation. The primary question in this regard is: What factors affect Namibian employers’ compliance decisions concerning employee taxes?

Aim of the Study

The study aims to develop a substantive theory that explains the compliance behaviour of MSME employers in withholding and remitting employees’ taxes from their remuneration.

Significance of the Study

Compliance behaviour concerning employers’ withholding and remitting of employees’ taxes may be more complex than that of individuals regarding their own taxes. Further research is necessary to elucidate employers’ behaviour towards employee taxes. Identifying the key determinants affecting employees’ tax compliance decision-making requires thorough analysis. In this study, a systematic examination of employers’ compliance behaviour towards employee taxes serves as the foundation for developing a substantive theory that explains the compliance behaviour of Namibian employers in MSMEs regarding their statutory obligations towards employee taxes. Consequently, the theory may offer a new understanding of the factors driving employers’ compliance decision-making concerning employee taxes.

REVIEWING THE LITERATURE

In accordance with a grounded theory (GT) study, an extensive literature review was not conducted prior to data collection but rather throughout the research process. The literature review was conducted in two stages in this study. The researcher completed the initial review during the preparatory phase. This preliminary literature review encompassed literature on tax compliance, agency, and stakeholder theory to raise awareness of concepts that would be relevant and useful during the initial stages of interviewing.

The next stage of the literature review (the secondary review) took place during the extensive data collection process and, more specifically, after data analysis. This did not contradict the assumptions of Grounded Theory (GT), which maintains that the theory is generated from the actual data. On the contrary, the secondary literature review guided the researcher to relevant literature that would subsequently help explain the observed data. The emergent codes and categories, developed from the data through constant comparison and theoretical sampling, informed the secondary review. This secondary literature review explored in greater depth the tax compliance variables and agency theory. It assisted the researcher in refining and locating the emerging theory within various disciplines. Consequently, the theory is grounded both in literature and in actual data.

Defining Tax Compliance

Tax compliance can be understood as the degree to which a taxpayer follows tax rules and regulations (James & Alley, 2004). Youde and Lim (2019) define tax compliance as the taxpayer’s choice to adhere to tax laws and regulations pertaining to the timely and accurate payment of tax liabilities. Hassan, Naeem, and Gulzar (2021) describe tax compliance as the capability of taxpayers to follow tax laws, declare the correct income for each year, and make timely payments of the correct tax amounts.

Tax compliance means that taxpayers fulfil their legal obligations under tax laws, ensuring that all returns are submitted and tax liabilities are paid on time (South African Institute of Taxation, 2020; NamRA, 2021). Based on the definitions provided, compliance can be measured by four indicators: registration as a taxpayer, filing a tax return, declaring the correct PAYE, and paying PAYE within the stipulated period.

Tax Compliance Theories

The tax compliance frameworks encompass those developed by Allingham and Sandmo (1972), Chau and Leung (2009), Fischer et al. (1992), and Kirchler et al. (2008). Allingham and Sandmo (1972) contended that the factors affecting tax compliance decisions are primarily sanctions such as penalties, audits, and tax rates. Fischer et al. (1972), Chau and Leung (2009), and Kirchler et al. (2008) applied the classic economic model established by Allingham and Sandmo (1972). Fischer et al. (1992) integrated the influence of socio-economic and psychological processes, alongside demographic variables, on taxpayers’ compliance behaviour. Chau and Leung (2009) expanded on Fischer’s tax compliance model by incorporating culture and the interplay between non-compliance opportunities and tax systems. Conversely, Kirchler et al. (2008) proposed a framework for tax compliance where the power of tax authorities and trust in these authorities play a crucial role in elucidating enforced versus voluntary tax compliance; this framework, known as the Slippery Slope, combines economic and psychological perspectives. The theory posited by Kirchler et al. (2008) asserts that tax compliance can be enforced through the exercise of power or trust, contingent upon the supportive relationship between the state and the taxpayer.

However, the aforementioned tax compliance models and frameworks may not fully elucidate the employer’s decision in their capacity as an agent of the state, as well as the employee’s role in remitting taxes. This current study addresses this gap by examining employers’ tax compliance behaviour regarding employee taxes.

RESEARCH METHOD

The chosen methodology should allow for the consideration of the complex motivations behind the compliance decision. Since employers’ compliance behaviour regarding employee taxes is a relatively under-researched area, the methodology should remain open to various theories that may inform the study. As an exploratory approach, grounded theory is recommended for investigating areas where little research has been conducted (Charmaz, 2006, 2014).

Grounded theory (GT) is qualitative research that reflects the positivist worldview of US sociologist Barney Galland Glaser. It is primarily deductive and focuses on testing rather than developing a theory, with its roots in positivism and pragmatism (Glaser & Strauss, 1967; Edwina & McDonald, 2019). It systematically analyses various flexible strategies for constructing theory by integrating inductive, deductive, and abductive thinking (Glaser & Strauss, 1967).

Kathy Charmaz, a sociologist and student of Glaser and Strauss, is the first researcher to articulate a reformed constructivist approach to research. Her work is now recognised as constructivist grounded theory (CGT). In 2006, she published the seminal text “Constructing Grounded Theory: A Practical Guide through Qualitative Analysis,” which is grounded in pragmatist ontology and relativist epistemology (Charmaz, 2006). She endeavoured to ensure the participants’ presence throughout the research. In line with constructivist grounded theory, this study posits that both participants and the researcher co-construct reality (Charmaz, 2014).

Population and sampling

The target group consisted of MSME employers or an individual nominated by an employer who possessed relevant experience and authority within the organisation concerning the employee tax deduction from staff. The study conducted interviews with 25 respondents who were recruited through invitations made via radio broadcasts and letters sent to MSMEs, identified by a business consultant. The participants were spread across Namibia, ensuring representation from all the major regions. Table 1 below outlines the demographic and background information of the respondents.

Table 1: Demographic Information of Participants

| Parameter | Value | Number of Respondents |

| Gender | Male | 14 |

| Female | 11 | |

| Age | 25-34 | 4 |

| 35-44 | 5 | |

| 45-54 | 7 | |

| 55-64 | 8 | |

| 65 and above | 1 | |

| Education | Secondary school | 11 |

| Tertiary education | 14 | |

| Background | Financial | 5 |

| Non-financial | 20 | |

| Ownership | Family business | 12 |

| Non-family business | 13 | |

| Years of experience in current role | <5 years | 3 |

| 5-10 years | 6 | |

| >10 years | 16 | |

| Type of entity | Retail | 9 |

| Service | 16 | |

| Physical location | Central | 11 |

| North | 5 | |

| South | 4 | |

| West | 3 | |

| East | 2 | |

| Size of entity | Micro | 13 |

| Small | 5 | |

| Medium | 7 |

Source: Van der Walt (2024)

Ethical considerations

Ethical clearance was obtained from the Research Ethics Committee of the School of Accounting at the University of Johannesburg. Volunteers were informed that the study would focus on their actual perceptions and how these influence their behaviour towards employee taxes, thereby opening the possibility for tax reform based on employers’ honest opinions and actions. The researcher arranged access to and consent from key individuals before conducting the interviews, and participants’ consent was secured to make audio recordings of the interviews. Participants were assured that their personal information would remain confidential and that they could withdraw from the study at any time.

Data collection

Data collection occurred in two stages. In a grounded theory study, a researcher is usually confronted with unexpected themes and concepts, necessitating flexibility to accommodate these unforeseen ideas. Consequently, an unstructured or semi-structured conversational format is most appropriate for this methodology (Charmaz, 2006; Corbin & Strauss, 2008).

The first round of interviews sought to identify as many factors as possible that could explain employers’ PAYE compliance behaviour. The information gathered during this initial round informed the subsequent data collection in the second stage. The study continued to collect data until no new ideas emerged. After interviewing 25 respondents, data collection concluded.

The researcher also compiled a memorandum after each interview. The memorandum summarised the interview, included observations made during that interview, and provided guidance for theoretical sampling.

Data analysis

Data analysis commenced immediately after the first interview and involved initial, focused, and theoretical coding (Charmaz, 2014). The aim of initial coding is to generate as many codes as possible. Following open coding, the researcher elevates the most frequent and significant initial codes to higher-level categories through focused coding. This intermediate coding process further groups the data into variables and elucidates the relationship between the variables and the underlying categories (Strauss & Corbin, 1990; Charmaz, 2014; Tie, Birks & Francis, 2019). Theoretical coding represents the final stage towards theory development and the integration of the substantive theory from existing literature.

RESEARCH FINDINGS

During the first round of interviews, broad questions were posed to gain insights into employers’ compliance behaviour and identify as many indicators as possible to explain their attitudes toward their obligation to withhold and remit employee taxes. The transcription of each interview was coded line by line to uncover categories in the data relating to the reasons why respondents comply or do not comply with the provisions for employee taxes. These categories were grouped to reflect common themes, and several variables that warranted further investigation were identified in the second round of interviews. Based on the insights into respondents’ opinions and perspectives, the researcher could categorise the identified concepts into those that appear to influence the compliance decision and those that do not seem to influence the compliance decision strongly. Some of the most significant concepts after round one of the interviews, based on the frequency of occurrence in the interview data, were: compassion towards employees; employer/employee relationships; employers’ knowledge of remuneration; frustration regarding the duty to withhold and remit employee taxes; ethical values; fear of the tax authority; ultimate responsibility for employee taxes; and contributions to the common good.

The second round of interviews featured more specific questions and probed some concepts identified in the first round. The interview schedule was organised into six sections: in Section A, the researchers aimed to gather more information on respondents’ views of the government and the role their upbringing played in shaping this attitude. In Section B, further details were sought regarding employers’ perceptions of their employees as stakeholders and the extent of their compassion towards them. Section C examined respondents’ ethical behaviour by posing direct close-ended questions on several non-tax-related situations that required a yes or no answer. Section D assessed respondents’ understanding of what constitutes remuneration, while Section E aimed to explore the respondents’ frustrations with the tax authorities, specifically regarding their PAYE responsibilities. Section F endeavoured to deepen the researchers’ understanding of the relationship between employers’ views of the government and taxes in general, on one hand, and their PAYE compliance behaviour on the other.

In accordance with grounded theory guidelines, categories were identified to explain employers’ PAYE compliance decisions. A total of 59 categories were identified, which were subsequently grouped into six compliance decision variables, as illustrated in Table 2, before being organised into themes. The study achieved theoretical saturation as respondents elaborated on the categories extensively, and all theoretical ambiguities were clarified.

Table 2: Variables explaining employers’ PAYE compliance decision-making

| Categories | # | Total # for Variable | Variables Influencing Compliance Decision | Themes |

| Perceived power of the tax authorities | 22 | 124 | Power of the Tax Authority | Enforced Compliance Indicators |

| Fear of the tax authorities – based on reason | 84 | |||

| Effect on future generations | 6 | |||

| Disgruntled employees may act as whistleblowers | 7 | |||

| Reputational damage | 5 | |||

| Contribution to the common good | 32 | 109 | Moral Values, Religion and Upbringing | Voluntary Compliance Indicators |

| Patriotism towards the government | 4 | |||

| Religious beliefs mandate compliance | 9 | |||

| Moral Values | 47 | |||

| Upbringing demands compliance | 17 | |||

| Compassion towards employees in the lower income category | 99 | 101 | Compassion | Intentional Non-Compliance Indicators |

| Black Tax | 2 | |||

| Distribution fairness of the tax system | 16 | 78 | Perceived Fairness of the Tax System | Intentional Non-Compliance Indicators |

| Tax scales should be based on occupation and contribution towards youth development | 7 | |||

| Government’s inability to account for state funds | 24 | |||

| Lack of public services and goods | 31 | |||

| Seeking non-compliance opportunities or loopholes in the Act | 5 | 54 | Non-compliance opportunities | Intentional Non-Compliance Indicators |

| Non-compliance opportunity: Availability of cash | 15 | |||

| PAYE does not receive the same priority as other taxes | 4 | |||

| Non-compliance opportunity: information asymmetry | 2 | |||

| Seek non-compliance opportunities based on own low tax morale | 21 | |||

| Non-compliance opportunity – connected persons | 3 | |||

| Non-compliance opportunity – non-cash payments | 2 | |||

| Cashflow constraints of the entity | 2 | |||

| Knowledge – Non-cash payments are not taxed | 37 | 94 | Tax knowledge | Unintentional Non-Compliance Indicators |

| Insignificant amounts are not taxed | 2 | |||

| Ad-hoc benefits/payments not taxed – regarded as a gift | 17 | |||

| Knowledge: Rely on web-based information | 8 | |||

| Only amounts stipulated in the employment agreement are regarded as ‘remuneration” | 9 | |||

| Non-cash benefits are regarded as “gifts” | 2 | |||

| Tax knowledge: Strong reliance on payroll software | 12 | |||

| Employee taxes are generally complex | 5 | |||

| Knowledge: Do not know how to calculate tax on non-cash amounts | 2 | |||

| TOTALS | 560 | 560 |

Source: Van der Walt (2024)

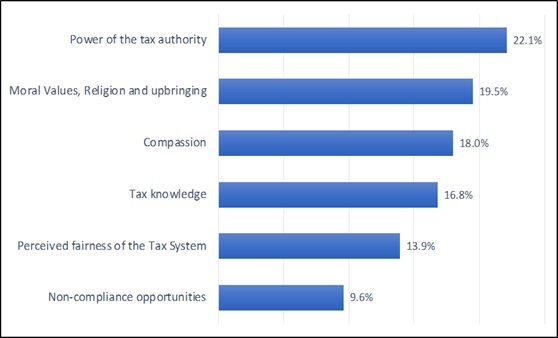

Figure 1 below illustrates, in descending order, the frequency of the variables that emerged during the interviews. While grounded theory aims to avoid becoming entangled in numbers, understanding the significance of certain variables compared to others is nevertheless valuable for evaluating the results and informing the subsequent substantive theory. Therefore, the data is presented as percentages of the total.

Figure 1: Compliance Decision Variables Expressed in Percentages

Source: van der Walt (2024)

Six variables explain employers’ decisions about compliance with employee taxes. These variables include compassion, moral values, upbringing and religion, the power of the tax authority, the employers’ lack of tax knowledge, opportunities for non-compliance, and the perceived fairness of the tax system. As discussed below, these variables lead to either Unintentional Non-Compliance, Intentional Non-Compliance, Voluntary Compliance, or Enforced Compliance.

Consequently, the variable compassion directly contributes to intentional non-compliance; moral values, upbringing, and religion promote voluntary compliance; the tax authority’s power enforces compliance; and a lack of tax knowledge results in unintentional non-compliance.

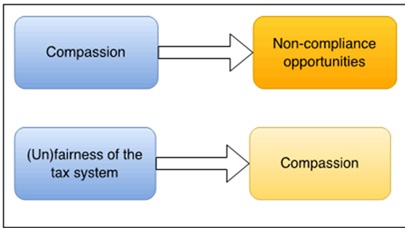

Non-compliance opportunities are identified as a significant variable; however, this variable, when considered in isolation, does not seem to lead to substantial non-compliance. Rather, it is the impact of other variables, particularly compassion, that drives the pursuit of non-compliance opportunities. Some employers contended that benefits are funded by private means and, therefore, are not associated with the employment agreement and, in their opinion, are not part of remuneration. Employers also perceive non-cash benefits as alternatives to a higher salary. These payments do not influence the accounting records. Respondents remarked, “there is no audit trail“, and no entries appear in the “accounting records.” A direct relationship between compassion and non-compliance opportunities is thus apparent.

An indication of the relationship between compassion, the perceived fairness or unfairness of the tax system, and the pursuit of non-compliance opportunities is the perception that employees 1) “struggle”, 2) “cannot make ends meet”, and 3) “they (employees) do not always have food at home”. Responses such as 1) “they (government wastes money”; 2) “the employees need the money more than the government”; 3) “saving on taxes can buy bread and milk”; 4) “Government only takes and takes, and does not give” reveal employers’ views that the government does not provide adequate public goods and services.

Thus, the perceived fairness of the tax system, along with the availability of non-compliance opportunities, influences the compliance decision through compassion and can be characterised as an intervening variable. The diagram below illustrates these relationships.

Figure 2: Relationships within variables

Source: Author’s own presentation

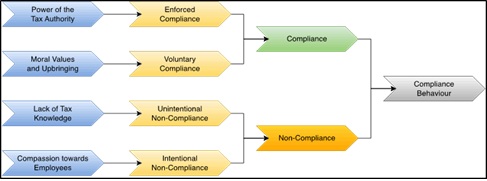

Only four variables were thus included in the substantive theory. The remaining two variables, the perceived fairness of the tax system and the availability of non-compliance opportunities are not necessarily disregarded. By including the four core variables, the remaining two are considered through their association with compassion and non-compliance opportunities. The primary drivers are, thus, compassion, moral values, upbringing and religion, the power of the tax authority and the employers’ lack of tax knowledge. These four variables were finally organised around four themes. Figure 3 shows the substantive theory explaining employers’ compliance behaviour towards employee taxes, and a discussion of the core variables with supporting evidence from interview responses and the literature follows thereafter.

Figure 3: Substantive theory explaining employers’ compliance behaviour towards employee taxes

Source: Author’s own presentation

Figure 3 illustrates the core variables that explain compliance behaviour. In this diagram, employers comply voluntarily with tax legislation based on their moral values and upbringing. Compliance may also be enforced through sanctions imposed by tax authorities. However, some employers choose to be non-compliant out of compassion for their employees. The final variable consists of employers who lack sufficient tax knowledge and are unintentionally non-compliant with employee tax legislation.

Core variable 1: The power of the tax authority

The responses indicate that the threat of sanctions for disobeying tax legislation significantly influences tax compliance. Various categories illustrate the power of the tax authority. These categories are: 1) fear of the authority, whether rooted in upbringing or actual encounters with it; 2) the impact of non-compliance on future generations; 3) the concern that disgruntled employees may report non-compliance; and 4) fear of reputational damage. The categories were organised under the broader concepts of “perceived power of the tax authority” and “fear of the tax authority – reason-based.”

The perceived power of the tax authority

The respondents frequently signalled their fear of the tax authorities, often attributing it to the values instilled during their upbringing. They suggested that their parents set an example for them to obey tax laws to shield them from legal sanctions. This group of taxpayers—employers—did not necessarily have prior encounters or negative experiences with the tax authorities. However, based on their parents’ teachings, they perceive the tax authorities as powerful.

Respondents aged 50 years and older mentioned the perceived power of the tax authority. Despite their frequent references to their upbringing, the responses from older employers did not show any trust in, loyalty towards, or respect for the authorities, potentially indicating a lack of intrinsic motivation to comply. For this group, the study proposes that the perceived power of the tax authorities, which was instilled during their upbringing several decades ago, has significantly diminished over time, leading to a corresponding reduction in its potential impact on their compliance behaviour. In contrast, the responses from younger respondents indicated that their fear of the authorities is based on their observations of current practices and past encounters with the tax authorities, rather than their upbringing. This observation confirms that the influence of upbringing on the tax behaviour of the current generation is minimal and is likely to decline even further in the future.

Fear of the tax authority – reason-based

The fear of the authorities expressed by several respondents arises from the current practices of the tax authorities, which include imposing sanctions such as fines and even initiating legal action for non-compliance. Many of these respondents had previous encounters with the tax authorities or at least knew someone who had negative experiences with them. The threat of sanctions can change taxpayers’ behaviour due to the fear of the consequences linked to non-compliance. Various studies (Webley, Cole & Eidjar, 2001; Kogler, Muehlbacher, & Kirchler, 2015; Alm, Bruner, & McKee, 2016) have found that friends and family members can sometimes influence a taxpayer’s decision to comply or not comply. However, the extent of this influence remains unaddressed.

Tax sanctions aim to deter non-compliant taxpayers and serve as a tool to prevent violations of tax laws. Taxpayers are likely to comply with these laws if they understand the risks of facing sanctions, such as fines, interest, and criminal offences. The relationship between tax enforcement strategies and tax compliance has been the focus of numerous studies, most of which have concluded that tax sanctions positively influence tax compliance (Alm, 1991; Benk, Çakmak & Budak, 2011; Gangl, Hofmann & Kirchler, 2015; Gangl et al., 2016). The findings of the current study align with Doran (2009). It indicates that employers evaluate the potential sanctions against the possible financial gains from non-compliance, concluding that the risks of sanctions outweigh the potential benefits. This insight also applies to respondents who discussed the implications of non-compliance for future generations. The participants in the present study recognised that there is a chance employees might report non-compliance. The impact of whistleblowing on employers’ compliance behaviour has been explored previously. Yaniv in Schulz (2021) suggests that tax enforcement may diminish when employers and employees collude over tax non-compliance. Kleven et al. (2009) argue that employees might act as whistle-blowers and inform the tax authority about non-compliance. The authors propose that the likelihood of whistleblowing increases with the number of employees: organisations with more personnel may face more severe consequences due to the actions of dissatisfied employees. Interestingly, although it could be argued that larger entities are more likely to recognise the implications of whistleblowing, one respondent, who employed only four individuals, also expressed concern over the potential actions of disgruntled employees.

Core variable 2: Moral values and upbringing

Employers’ moral values appeared to be a guiding factor in their compliance behaviour and resulted in voluntary compliance. Moral values, upbringing, contributions to the common good, religious beliefs, patriotism, and national pride explain this variable. Simply put, morals refer to the distinction between right and wrong. Whiteley (1960, p. 141) suggests that the “morality of a community consists of those ways of behaviour which each member of the community is taught, bidden, and encouraged to adopt by the other members.” Moral behaviour, therefore, refers to adherence to these “ways of behaviour” or customs. While various definitions of morals and values exist, understanding the distinction between right and wrong remains the principal element. For this study, responses indicating the desire to do what is right were labelled “moral values.”

In layman’s terms, the treatment and guidance a child receives from its parents during childhood is referred to as its upbringing. It was observed that whenever respondents mentioned moral values, it generally triggered a reference to their upbringing. These responses align with the definition and explanation of upbringing provided earlier in this section.

Notably, the respondents who often cited upbringing and moral values were all aged 50 and over. These individuals also expressed the greatest frustration regarding the decline in public services and goods and thus appeared most susceptible to a decrease in trust in the government, potentially leading to non-compliance. Respondents seemed to experience a conflict of conscience between, on one hand, adhering to their moral principles and, on the other hand, harbouring resentment towards the reduced support from the government. This observation implies that compliance driven by moral values may become less common in the future.

Genuine moral values, or the desire to do what is right, are frequently mentioned in the responses and are linked to voluntary compliance. This study concurs with Troutman (1993), who verifies the connection between morals and tax compliance. Kirchler (2007) and Alm and Torgler (2011) further bolster this argument. While most previous research concentrated on taxpayers’ compliance behaviour concerning their own taxes, the current study aligns with their assertions.

The current study confirms that religion positively influences employers’ willingness to comply with tax legislation. It is important to note that all respondents in this study are of the Christian faith. Mohdali and Pope (2012) identified a correlation between voluntary tax compliance and religious beliefs among Malaysian taxpayers. In 2016, Benk, Budak, Yüzbaşı, and Mohdali validated these findings in their research conducted in Turkey. However, a study carried out in Ghana indicated that religion does not lead to voluntary compliance. The authors propose that tax evasion is viewed as ethical (Carsamer & Abbam, 2023).

Etzioni (2015) and Hussain (2018) describe the common good as that which is shared and beneficial for all or most members of society. For the purposes of this study, the common good denotes taxpayers’ intrinsic willingness to comply with tax legislation based on the perception that their taxes contribute to this shared benefit.

If individuals view their tax contributions as a benefit to society, their willingness to pay taxes honestly increases, regardless of whether the public benefits received match the taxes paid (Feld & Frey, 2007).

The respondents’ compliance attitude relates to their perception of the benefits a country should and can provide its citizens. This observation echoes the contention by Braithwaite and Ahmed (2005) that a relationship exists between a positive compliance attitude and the values individuals hold regarding the type of society they wish to inhabit. This study confirms that citizens who view their actions as contributing to the well-being of the community are inclined to voluntarily comply with employee taxes. One of the factors identified in the study as influencing the desire to contribute to the common good is a sense of patriotism and national pride. Patriotism can be described as the bond between an individual and their country, reflecting positive emotions such as trust, pride, loyalty, devotion, commitment, and concern (Alm, 2019; Hamada, Shimizu & Ebihara, 2021). It serves as an essential guide for citizens’ community behaviour (Huddy & Khatib, 2007). Consequently, citizens tend to emulate the behaviour of others whom they perceive as members of the same community or social group. Actions that diverge from the norms of other members of a social group may result in the transgressor facing rejection by the group. Ultimately, patriotism can enhance cooperation among citizens as they recognise a shared social identity. The evident impact of patriotism and national pride on the respondents’ compliance attitude reinforces the findings of a study conducted in Spain by Martinez-Vazquez and Torgler (2009), which indicated a strong correlation between national pride and a favourable compliance attitude. Similarly, Gangl et al. (2016) found that higher satisfaction with a country’s democratic institutions should lead to increased tax morale.

Core variable 3: Lack of tax knowledge

A lack of knowledge about remuneration and tax laws, combined with minimal or no support from the tax authorities, may lead to unintentional non-compliance. Although respondents intend to comply and truly believe they are adhering to PAYE legislation, insufficient understanding of remuneration frequently results in non-compliance.

This variable is explained by: 1) knowledge of remuneration; 2) the employer’s reliance on payroll software to understand remuneration; 3) the reliance on web-based information; 4) the employer’s perception that only amounts stipulated in the employment agreement constitute remuneration; 5) the general perception that employee taxes are complex; 6) the view that ad-hoc payments are gifts; and 7) the belief that only cash amounts can be regarded as remuneration.

Participants’ responses indicated that employers heavily rely on payroll software to determine what qualifies as remuneration. While payroll software can offer some guidance, it typically considers only the most basic aspects. Likewise, the information on the tax authority’s website is rudimentary and occasionally outdated. The website generally outlines employee taxes, explains when an employer should deduct them, and indicates when the amounts are due to the authority. However, it does not address the concept of “remuneration” or the tax implications of fringe benefits.

The relatively widespread practice among participants of not taxing insignificant amounts suggests that employers view it as a lesser ‘sin’ than non-compliance, somewhat akin to a white lie in the biblical context of punishable sins. They also noted that they consider these insignificant amounts as “gifts.”

Respondents indicated that any amounts paid outside the employment contract and ad hoc payments were viewed as gifts or grants. Some respondents even suggested that employers made such payments in their personal capacity. Thus, the rationale used to exclude such payments from remuneration was twofold: first, they were classified as gifts or grants, and second, employers made them in their personal capacity. This study indicates that taxpayers generally believe that remuneration only includes cash amounts.

The value of the non-cash benefits under discussion was generally insignificant. However, larger organisations may offer non-cash fringe benefits of greater value, which, given the generally limited understanding of remuneration observed in this study, could significantly impact employee taxation and the government’s tax revenue. The Income Tax Act 24 of 1981 clearly defines remuneration as:

“… any amount of income which is paid or is payable to any person by way of any salary, leave pay, allowance, wage, overtime pay, bonus, gratuity, commission, fee, emolument, pension, superannuation allowance, retiring allowance or stipend, whether in cash or otherwise and whether or not in respect of services rendered…”

The literature supports the view that tax knowledge influences tax compliance. Studies conducted in Malaysia agree that tax knowledge is significant in determining taxpayers’ compliance behaviour under the Malaysian self-assessment system (Loo, 2006). Saad (2014), Timothy & Abbas (2021), and Naape (2023) further underscore the importance of tax knowledge in tax compliance.

The current study also observes that employers regard it as their responsibility to inform and educate employees about tax matters. The study recommends that the tax authority engage with employers to enhance their understanding of “remuneration” and fringe benefits tax liability. These sessions could be conducted face-to-face, broadcast via online media or television and radio services, or through outreach programmes.

Core variable 4: Compassion towards employees

The variable “compassion” is elucidated through the compassion shown towards employees in the lower income category and the concept of “black tax”. Definitions of compassion differ; it is at times characterised as an emotion, a multidimensional construct, or a motivational system (Kirby, Tellegen, & Steindl, 2017). As stated in the Oxford English Dictionary, the term “compassion” derives from the Latin “compati”, which translates to “to suffer with”. Scholars concur that compassion encompasses sympathetic feelings for someone who is suffering, as well as the drive to offer assistance (Goetz, Keltner & Simon-Thomas, 2010; Gilbert, 2014).

The responses in the current study clearly confirm the connection between compassion and the perception of declining government support for the less fortunate through public goods and services. This unfavourable perception is central to the high levels of compassion. This compassion is entirely understandable—taxpayers in the lower income bracket are more reliant on government support through public services and goods.

The plausible—but still undesirable—consequence of the current state of affairs is that employers are seeking opportunities for non-compliance to increase their employees’ disposable income. Compassionate employers aim to alleviate their employees’ financial distress and typically resort to opportunities to avoid paying employee taxes. An employer with sufficient tax knowledge usually identifies possible loopholes and straightforward non-compliance opportunities.

The fact that tax authorities lack sufficient knowledge about the entity’s payroll also significantly contributes to non-compliance. Information asymmetry is one of the key assumptions of agency theory. This theory postulates that agents act in their self-interest and may possess a higher risk appetite than their principals. If the principal lacks adequate insight into the tasks being performed, the agent may not consider the principal’s interests as one might expect (Eisenhardt, 1989).

However, what offsets the negative influence of employers’ compassion on compliance is their fear of the authorities and adherence to moral values. I observed that younger respondents did not exhibit the same sentiments regarding moral values as older respondents. This raises the possibility that the impact of moral values may diminish in the future.

DISCUSSION

The study aimed to develop a substantive theory, illustrated in Figure 3, that explains the compliance behaviour of MSME employers in withholding and remitting employees’ taxes from remuneration. Although extensive research has been conducted to identify the key drivers of taxpayer compliance decisions and document their results, the behaviour of employers regarding PAYE compliance has been overlooked by this research.

The study’s results were enlightening, revealing several factors that influence employers’ PAYE compliance decisions. A key revelation was that employers are more likely to be non-compliant than compliant. These findings are concerning, considering that the mission of the Namibian tax authorities, like their counterparts globally, is to promote voluntary compliance. Additionally, the results of this study provided new insights into various factors driving compliant and non-compliant behaviour.

Voluntary compliance is influenced by the upbringing of employers, during which certain values are instilled. These values encompass an intrinsic motivation to act ethically and contribute to the common good. Older respondents frequently cited ethical motivation; this suggests that compliance rooted in ethical values is diminishing among younger employers and, more concerning, that future generations’ motivation for compliance may rely even less on ethical considerations. Conversely, younger respondents from a specific ethnic group exhibited greater patriotism and national pride, making them more driven to contribute to the common good than their counterparts. It could be argued that the patriotic fervour of these younger respondents may be politically motivated.

Fear of the tax authorities—stemming from either the perception of their power or from actual threats—correlates with enforced compliance. The fear perceived by taxpayers was ingrained during their upbringing but appears to diminish over time, as older taxpayers show a greater propensity for enforced compliance. Given that older respondents identified upbringing as a crucial factor in their compliance decisions, one could argue that the influence of values learned during upbringing is likely to wane over time in successive generations.

Perceptions of inadequate government support for the less fortunate, evidenced by the decline in public goods and services, lead to frustration with the authorities and heightened compassion for employees in lower income brackets. This provokes employers to deduct less PAYE than stipulated by the Act to assist the affected employees.

An uncomplicated opportunity for non-compliance arises due to the limited awareness tax authorities have regarding entities’ payrolls. The fact that MSMEs are not subjected to a thorough audit may also encourage creative accounting practices and the concealment of payroll transactions. Ultimately, this practice enables employees to benefit from a higher after-tax income.

Employers’ lack of knowledge regarding taxes results in unintentional non-compliance. While these employers believe they are compliant, they often are not. Furthermore, employers consider the education of employees about taxes to be their responsibility. Given the employers’ evident lack of tax knowledge, the information they provide to employees may be inadequate.

Non-compliance was also found to manifest in employers exploiting grey areas in the Act, such as its ambiguities regarding where the ultimate responsibility for unpaid or under-deducted PAYE lies. Employers arguably utilise these ambiguities to their advantage, contending that the Act stipulates that employees bear the final responsibility for unpaid taxes. Consequently, employers lack the motivation to comply.

Acknowledging Limitations

Similar to others employing the grounded theory approach, the study faced a limitation regarding the sample size, consisting of only 25 respondents. Additionally, the study population comprised solely Namibian MSMEs, which restricts generalisability.

Contributions

This study contributes to the scholarly literature on tax compliance and further enhances the understanding of employers’ compliance behaviour. The substantive theory developed should prove valuable to tax authorities in Namibia and others in similar contexts who aim to improve employers’ voluntary compliance behaviour regarding employee taxes.

Future research

This study revealed that employers are critical of a government perceived to be failing to provide disadvantaged employees with public goods and services. This, in turn, fosters employers’ compassion for affected employees and encourages non-compliant behaviour. The results of similar studies in countries where the general perception is that the government provides adequate support may be significantly different.

The role of compassion in employee tax compliance was found to be highly significant in this study. Therefore, it is recommended that the influence of compassion on employee tax compliance in both developing and developed countries be researched, as the findings could be valuable.

The substantive theory also provides opportunities for empirical verification in future studies across various tax contexts and economies.

ACKNOWLEDGEMENTS

My sincere gratitude goes to the respondents who took time out of their busy schedules to share their thoughts on the research topic. Your participation made this study possible.

REFERENCES

- Allingham, M. G., & Sandmo, A. (1972). Income tax evasion: A theoretical analysis. Journal of Public Economics, 1(3-4), 323–338.

- Alm, J. (1991). A perspective on the experimental analysis of taxpayer reporting. The Accounting Review, 66(3), 577-593.

- Alm, J. (2019). What motivates tax compliance? Journal of Economic Surveys, 33(2), 353-388.

- Alm, J., Bruner, D., & McKee, M. (2016). Honesty or dishonesty of taxpayer communications in an enforcement regime. Journal of Economic Psychology, 56(c), 85-96.

- Alm, J., & Torger, B. (2011). Do ethics matter? Tax compliance and morality. Journal of Business

- Amukeshe, L. (2021, 9 April). Low tax compliance leads to Nam’s spiking debt. The Namibian. https://allafrica.com/stories/202104090847.html

- Benk S., Budak T., Yüzbaşı, B., & Mohdali, R. (2016). The impact of religiosity on tax compliance among Turkish self-employed taxpayers. Religions. 7(4), 37.

- Braithwaite, V. (2003). A new approach to tax compliance. In V. Braithwaite (Ed.), Taxing democracy. Understanding tax avoidance and tax evasion (pp. 1–11). Ashgate.

- Braithwaite, V., & Ahmed, E. (2005). A threat to tax morale: The case of Australian higher education policy. Journal of Economic Psychology, 26(4), 523-540.

- Braithwaite, V., Murphy, K., & Reinhart, M. (2007). Taxation threat, motivational postures, and responsive regulation. Law and Policy, 29(1), 137-158.

- Benk, S., Çakmak, A. F., & Budak, T. (2011). An investigation of tax compliance intention: A theory of planned behavior approach. European Journal of Economics, Finance and Administrative Sciences, 28(28), 181-188.

- Carsamer, E. & Abbam, A. (2023). Religion and tax compliance among SMEs in Ghana. Journal of Financial Crime, 30(3), 759-775.

- Charmaz, K. (2006). Constructing grounded theory. Sage.

- Charmaz, K. (2014). Constructing grounded theory (2nd ed). Sage.

- Chau, G., & Leung, P. (2009). A critical review of Fischer tax compliance model: A research synthesis. Journal of Accounting and Taxation. 1(2), 34-40.

- Corbin, J., & Strauss, A. (2008). Basics of qualitative research: Techniques and procedures for developing grounded theory. (3rd ed.) Sage.

- Doran. M. (2009). Tax penalties and tax compliance. Georgetown Law Faculty Publications and Other Works, 111-161. https://scholarship.law.georgetown.edu/facpub/915

- Edwina, M. & Donald, S. (2019). Examining the use of Glaser and Strauss’s Version of the Grounded Theory in Research. International Journal of Engineering and Advanced Technology. 8.

- Eisenhardt, K. (1989). Agency theory: An assessment and review. The Academy of Management Review, 14(1), 57-74.

- Etzioni. A. (2015). The standing of the public interest. Barry Law Review, 20(2), 191-217.

- Feld, L. P., & Frey, B. S. (2007). Tax compliance as the result of a psychological tax contract: The role of incentives and responsive regulation. Law & Policy, 29(1), 102-120.

- Gangl, K., Hofmann, E., & Kirchler, E. (2015). Tax authorities’ interaction with taxpayers: A conception of compliance in social dilemmas by power and trust. New Ideas in Psychology. 37, 13–23.

- Gangl, K., Torgler, B., and Kirchler, E. (2016). Patriotism’s impact on cooperation with the state: An experimental study on tax compliance. Political Psychology, 37(6), 867–881.

- Gilbert, P. (2014). The origins and nature of compassion-focused therapy. British Journal of Clinical Psychology, 53(1), 6–41.

- Glaser, B. G., & Strauss, A. L. (1967). The discovery of grounded theory strategies for qualitative research. Sociology Press.

- Goetz, J. L., Keltner, D., & Simon-Thomas, E. (2010). Compassion: An evolutionary analysis and empirical review. Psychological Bulletin, Vol. 136(3), 351–374.

- Hamada, T., Shimizu, M. & Ebihara, T. (2021). Good patriotism, social consideration, environmental problem cognition, and pro-environmental attitudes and behaviors: a cross-sectional study of Chinese attitudes. SN Applied Sciences, 9(361), 3-16.

- HMRC. (2022). Employer further guide to PAYE and national insurance contributions. https://www.gov.uk/government/publications/cwg2-further-guide-to-paye-and-national-insurance-contributions

- Huddy, L., & Khatib, N. (2007). American patriotism, national identity, and political involvement. American Journal of Political Science, 51(1), 63–77.

- Hussain, W. (2018). The common good. In Edward N. Zalta (Ed.). The Stanford Encyclopedia of Philosophy. https://plato.stanford.edu/archives/spr2018/entries/common-good/

- Internal Revenue Services. (2021). Understanding employment taxes https://www.irs.gov/businesses/small-businesses-self-employed/understanding-employment-taxes

- Jackson, B., & Milliron, V. (1986). Tax compliance research: Findings, problems and prospects. Journal of Accounting Literature, 5, 125-165.

- Kirby, J.N, Tellegen, C.L., & Steindl, S. R. (2017). A meta-analysis of compassion-based interventions: Current state of knowledge and future directions. Behavior Therapy, 48(6), 778-792.

- Kirchler, E. (2007). The economic psychology of tax behaviour. Cambridge University Press.

- Kirchler, E., Hoelzl, E., & Wahl, I (2008). Enforced versus voluntary tax compliance: The “slippery slope” framework. Journal of Economic Psychology, 29, 210-225.

- Klevin, H.J., Kreiner, C. T., & Saez, E. (2009). Why can modern governments tax so much? An agency model of firms as fiscal intermediaries. Economica, 83, 219-246.

- Kogler, C., Muehlbacher, S., & Kirchler, E. (2015). Testing the “slippery slope framework” among self-employed taxpayers. Economics of Governance, 16(2), 125-142.

- Kołodziej, S. (2021). Validation of the Polish version of the Motivational Postures (Toward Taxes) Questionnaire. PLoS ONE. 16(6), 1-17.

- Loo, E.C. (2006). Tax knowledge, tax structure and compliance: A report on a quasi-experiment. New Zealand Journal of Taxation Law and Policy, 12(2), 117-140.

- Martinez-Vazquez, J., & Torgler, B. (2009). The evolution of tax morale in modern Spain. Journal of Economic Issues. 43(1), 1-28.

- Mohdali, R., & Pope, J. (2012). The effects of religiosity and external environment on voluntary tax compliance. New Zealand Journal of Taxation Law and Policy, Vol.18(2), 119-139.

- Naape, B. (2023). Tax knowledge, tax complexity and tax compliance in South Africa. Finance, Accounting and Business Analysis. 5(1), 14-27.

- Namibia Income Tax Act, Act 24 of 1981. https://www.lac.org.na/laws/annoSWA/INCOME%20TAX%20(1981)%20-%20Income%20 Tax%20 Act%2024%20of%201981%20(annotated).pdf

- Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia – Social and Behavioral Sciences, 109(1), 1069-1075.

- Schulz, B. (2021). The Cum-ex case: A look at Germany. Economic Studies & Analyses/Acta VSFS, 15(1), 49-62.

- Strauss, A., & Corbin, J. M. (1990). Basics of qualitative research: Grounded theory procedures and techniques. Sage.

- Tie, Y.L., Birks, M., & Francis, K. (2019). Grounded theory research: A design framework for novice researchers. SAGE Open Medicine, 7, 1–8.

- Timothy, J., & Abbas, Y. (2021). Tax morale, perception of justice, trust in public authorities, tax knowledge, and tax compliance: a study of Indonesian SMEs. eJournal of Tax Research, 19(1), 168-184.

- Troutman, C.S. (1993). Moral commitment to tax compliance as measured by the development of moral reasoning and attitudes toward the fairness of the tax laws. Unpublished PhD thesis. Oklahoma State University. https://shareok.org/bitstream/handle/11244/317024/Thesis-1993D-T861m.pdf? sequence=1

- Universität Wursburg. (2020). Ranking of Countries by Quality of Democracy. The democracy definition of the democracy matrix. Universität Wursburg. https://www.democracymatrix.com/ranking

- Webley, P., Cole, M., & Eidjar, O. (2001). The prediction of self-reported and hypothetical tax-evasion: Evidence from England, France and Norway. Journal of Economic Psychology. 22 (2), 141-155.

- Whiteley, C.H. (1960). On Defining Moral. Analysis, 20(6), 141–144.