A Review on the Application & Influence of Big Data in the Financial Institutions

- Mirza Fahim Ahmed

- Ishter Mahal

- 208-229

- Feb 28, 2025

- Education

A Review on the Application & Influence of Big Data in the Financial Institutions

Mirza Fahim Ahmed1*, Ishter Mahal2

1Lecturer, Department of Humanities & Business, Khulna University of Engineering & Technology (KUET)

2Associate Professor, Department of Accounting & Information Systems, University of Dhaka

*Corresponding Author

DOI: https://doi.org/10.51244/IJRSI.2025.12020019

Received: 02 December 2024; Accepted: 15 February 2025; Published: 28 February 2025

ABSTRACT

The research explores & elaborates on the application & influence of Big Data on the main areas or functions of various financial institutions, mainly commercial banks. Big Data has become an integral part of modern finance & economy. This study aggregates the main factors associated with the application of Big Data over various financial activities. The research also explores the complexities & constraints of Big Data within the lens of financial activities. The research follows a secondary data collection technique by systematically locating & reviewing academic research focusing on Big Data and finance or banking activities. Ultimately, the study provides a comprehensive overview of the fundamental characteristics of Big Data, its applications in financial institutions, related complexities & potential strategies to minimize the complexities.

Keywords: Big Data, financial institutions, Risk management, Big Data management, predictive analysis.

INTRODUCTION

Research Background

The financial sector especially banks and other financial institutions are recognizing data analytics to gain competitiveness. The entities are continuously generating vast amounts of structured and unstructured data through various operations. The primary source for Big Data is multi-dimensional including transactions, market activities, customer interactions and regulatory reporting. Historically financial institutions were dependent on conventional data processing methods to analyze and manage information (Hajiheydari et al., 2021). However, due to technological advancements consumer interactions and market expansion has increased which led to exponential growth in data volume and variety. This has increased the complexity of the financial transactions and traditional methods have become inadequate to meet the demands of modern financial operations (Al-lozi et al., 2022). Big Data analytics offers transformative solutions for the financial market, enabling real-time interpretation of massive data sets. It provides deeper insights into market dynamics and client behavior, enabling informed decisions. It revolutionizes banking operations by offering automation, personalized services, and efficiency improvements. It aids in fraud detection and prevention and represents a paradigm shift in operational and decision-making processes (Zhu and Yang, 2021). It optimizes budgeting, forecasting, resource allocation, adaptability to market trends, and real-time insights into financial performance.

Problem Statement

The application of Big Data is much higher in the financial and banking sectors compared to other industries. However, as the concept of Big Data is new, the publications on Big Data and finance are very limited (Yu et al., 2021). Moreover, there are very limited studies that clearly define in which areas of the financial markets, Big Data is being used & analyzed mostly. Our study is to show the application of Big Data within the finance industry by analyzing & reviewing scholarly articles & journals. This research aims to provide a comprehensive overview of Big Data’s fundamentals and application in financial markets, analyzing various themes from studies and presenting the analysis in charts or tabular formats for better understanding (Bose, 2018).

Research Gap

The rapid growth of Big Data applications in the financial sector highlights a research gap in understanding its fundamental principles and their application in various financial institutions, including banks. Therefore, there is a need for research that provides a holistic overview regarding the fundamentals of Big Data & how Big Data Analytics can be applied across different types of financial markets. Big Data analytics comes with several complexities regarding security & data privacy-related concerns (Yang, 2022). This will also be critically examined in this report by providing various recommendations to minimize data management-related risks.

Research Questions

The purpose of this research is associated with the application & implications of Big Data analytics within financial markets. Three main research questions can be identified for this research.

- What are the fundamental characteristics of Big Data?

- What are the potential sources of Big Data in financial institutions?

- What are the uses of Big Data in financial institutions?

- How do financial institutions use Big Data in predictive analysis?

- How does Big Data aid the process of risk management and fraud detection?

- How does Big Data aid client analysis in financial institutions?

Research Aim

The study is aimed to provide a holistic overview of the fundamentals of Big Data & the application of Big Data Analytics in financial institutions. The research also aims to get insights regarding the challenges & ethical issues associated with Big Data.

Research Objectives

Tough studies have been done focusing on particular topics, but the extensive application & influence of Big Data in financial markets haven’t been done before with proper explanation. So, the objectives of this paper include:

- To understand the fundamental characteristics of Big Data (3Vs & 5Vs) (Hasan, Popp and Oláh, 2020).

- Identification of the potential sources of Big Data for banks & other financial institutions.

- To examine the use of Big Data in financial management.

- To explore predictive analysis in financial institutions with Big Data.

- To analyze the process of risk management & fraud detection in the finance industry with Big Data.

- To understand client analysis with Big Data in banks & other financial institutions.

LITERATURE REVIEW

Overview of Big Data

The financial sector is heavily influenced by data-driven activities and innovations, with Big Data analytics revolutionizing traditional practices. It enhances decision-making, risk analysis, and operational efficiency. The data-intensive sector generates vast structured and unstructured information, allowing financial institutions to extract actionable insights and achieve operational excellence. This influence includes various stakeholders (Balachandran and Prasad, 2017). Big Data Analytics can improve the financial management practices of financial institutions, regulators, investors, and society by optimizing risk analysis and enhancing banking operations. By gathering insights into market trends, customer behavior, and risk profiles, financial organizations can mitigate operational and financial risks. This research examines Big Data analytics in financial sectors, focusing on financial management, banking operations, and sources of Big Data. The research can significantly contribute to enhancing insights regarding data-driven innovation and Big Data management (Yu et al., 2021). Big Data is revolutionizing decision-making, involving stakeholders like employees, customers, and suppliers. Technology advances integrate banking operations, and top management invests in projects. Infrastructure and capacity building are needed for effective use.

Big Data is increasingly being utilized by large business organizations, particularly in the banking and financial sectors, despite its potential risks and complexity in managing data privacy and security. (Bayo Olushola Omoyiola, 2022). Big Data analytics enhances organizational information flow, decision-making, and competitive advantages in the financial sector. It generates trend analysis and predictive information, but management may feel disappointed if perceived benefits don’t offset marginal costs (Yang, 2022). Low-quality data can negatively impact companies and organizational viability. Financial institutions and governments face challenges in handling Big Data, despite unlimited resources. Definement of volume, variety, and velocity is crucial. (Khatib, Shehhi and Nuaimi, 2023). Numerous studies conducted to understand the challenges associated with Big Data in finance. However, a comprehensive understanding is lacking within the existing literature. The ultimate objective of this study is to propose certain actionable recommendations for financial institutions to effectively manage and execute big data-related operations (Begenau, Farboodi and Veldkamp, 2018).

Big Data Concepts & Technologies

Data is generated at a massive speed from a variety of sources. Studies indicate that the concept and technology associated with peak data analytics are multidimensional. In-depth, analysis of the structures and concepts associated with the data is essential for organizational survival and growth (Bose, 2018). Traditional data processing methods struggle to handle the massive volume of data generated from various sources, including transactions, social media interactions, sensor data, and client feedback, which presents both opportunities and challenges for financial organizations (Yang et al., 2017). Data can involve semi-structured as well as restructured or unstructured data. Research indicates that structured data includes transactional records and financial statements which are organized in organizational databases. Structured data is comparatively easier to process and analyze than other formats. However financial and other organizations deal with unstructured data including text documents and images or videos (Khatib, Shehhi and Nuaimi, 2023). Unstructured data cannot be found in a predefined structure and it requires specialized tools and techniques for further analysis. A week of structured and unstructured data sets is referred to as semi-structured data formats. Big Data analytics has also unique characteristics regarding data generation and collection processes. The modern business environment has increased data stream flows including social media interactions and through IOT devices (Broby, 2022). Financial and General Institutions need real-time data analytics for informed decisions. Traditional batch-processing methods face challenges due to data velocity and variability. Institutions must adapt their data processing and analytics methods to meet market demands and address frequent changes in business scenarios (Cerchiello and Giudici, 2016). Various technological solutions and tools have already been introduced to minimize the challenges associated with Big Data analytics and processing. Distributed computing framework networks including Apache Hadoop and Apache Spark can enable parallel processing of large datasets. Stream processing platforms such as Apache Kafka and Apache Flink, enable real-time processing and analysis of streaming data. NoSQL databases such as MongoDB and Cassandra can process unstructured or semi-structured data (Wassouf et al., 2020).

Evolution of Big Data in Finance & Banking

The evolution of Big Data in finance and banking systems can be marked by significant milestones. The process is driven by advancements in technology and changes in consumer behaviours within the industry. Studies illustrate the evolution of Big Data in financial sectors and provide insights regarding how these organizations have adopted the challenges and opportunities of Big Data Analytics. The earliest stages of Big Data adoption in this industry can be identified back to the 1980s and 1990s (Cerchiello and Giudici, 2016). A common term was popular back at that time as data warehousing technologies. Financial institutions began to recognize the value of consolidating and centralizing data and converting them into potential assets. The process facilitated batch performing and historical analysis of transactional data and consumer information to maintain competitiveness within the industry. Data warehousing laid the foundation for more advanced data analytics and ultimately resulted in Big Data. The emergence of the Internet and digital technologies in the late 20th century has revolutionized the banking industry (Sun, Shi and Zhang, 2019). The process introduced digital banking platforms and online financial services to meet evolving consumer demands. Scholarly articles indicate a shift toward digital channels by financial institutions to gain access to a wider client base. Financial institutions have gained access to vast amounts of consumers by shifting towards digital channels (Song, Li and Yu, 2021). The financial system is constantly accumulating vast amounts of data through online transactions, mobile banking, and digital interactions. Advanced data analytics enable banks to analyze consumer behavior, retain client satisfaction, and manage risk (Chang et al., 2020). Machine learning algorithms are being used in credit scoring and fraud detection, enhancing accuracy and detecting anomalies quickly. Predictive analysis anticipates consumer needs and forecasts market trends, leading to increased investment in real-time data processing and analytics in banks and financial institutions. Streamlined analytics platforms are fostering decision-making and fraud detection, with Amazon Web Services, Google Cloud Platform, and Microsoft Azure being modern Big Data ecosystems (Dehbi et al., 2022). In recent years financial institutions have increasingly embraced the broader Big Data ecosystem to gain scalability and agility. The emergence of open-source Big Data platforms can make Big Data integration less costly. It can allow all sizes of organizations to harness the power of Big Data for innovation at a minimum initial investment (Song, Li and Yu, 2021).

Relevance of Big Data in Financial Markets

Big Data analytics provide huge opportunities for financial market participants including investors and traders as well as fund managers. Potential sources of Big Data analysis include market fees and social media as well as client interaction in a real-time manner. Market participants can gain critical insights regarding market trends and sentiment shifts to minimize the threats and capitalize on the available opportunities (Dicuonzo et al., 2019). Risk management is crucial for banks, involving market, credit, and liquidity analysis. Dictate Analytics helps minimize risks, with Big Data analysis correlated with understanding market indicators and macroeconomic trends (Soltani Delgosha, Hajiheydari and Fahimi, 2020). Big Data analytics is also essential for algorithmic trading and quantitative analysis in banks and investment funds. Automated trading strategies can be developed based on mathematical models and statistical analysis of large data sets. Articles on quantitative analysis illustrate that high-frequency trading firms often utilize Big Data to identify market inefficiencies and explore opportunities (Fan, Han and Liu, 2014). Data analytics execute trades at lightning-fast speed to gain a competitive edge in the financial industry. Transactional data and social media insights illustrate demographic information for financial institutions. Research indicates that organizations can identify cross-selling opportunities and provide tailored services to individual needs by utilizing data analytics (Sharma, 2023). Regulatory compliance and fraud detection are one of the top priorities for financial institutions to operate in a highly deregulated market. Big Data analytics facilitate financial institutions to comply with regulatory requirements by monitoring transactions and suspicious activities. Previous studies indicate that Big Data analytics can be available in real-time for detection and establishing preventive mechanisms over transactional patterns and anomalies (Saidali et al., 2019). The broader term used for this context is market surveillance (Gao, 2023). This can monitor market manipulation by insider trading and other illegal activities. Organizations maintain the integrity and stability of financial markets by leveraging the opportunities of Big Data and algorithm analysis.

Financial Management & Big Data Analytics

The financial decision-making process and strategic integration in the modern business environment are directly linked with Big Data analytics. Articles indicate that Big Data can assist financial managers to improve forecasting accuracy and conduct strategic planning accordingly (Bayo Olushola Omoyiola, 2022). Large data sets include various sources of transactions such as sales and expenses as well as other economic activities. Statistical models and machine learning programs can assist financial managers in conducting trend analysis (Hajiheydari et al., 2021). Traditional financial reporting often relied on static reports generated only from structured data sources. Studies indicate that structured data sources cannot provide timely insights during changing business conditions. Dictate Analytics facilitate real-time financial reporting by integrating data from multiple sources. Industry reports indicate that by analyzing this data in real time financial managers can gain immediate visibility into the key performance indicators (Rawat and Yadav, 2021). Thus, organizations promptly respond to emerging opportunities and risks. There is an interrelation between cost optimization and Big Data application. It is also identified that Big Data integration requires excessive initial investments. However, it also facilitates managers to identify cost optimization opportunities and improve operational efficiency. Researchers found that by leveraging data mining and optimization algorithms financial managers can effectively identify inefficiencies and streamline overall operations (Hariri, Fredericks and Bowers, 2019). Optimized resource allocation ultimately leads to reduced costs and improved productivity. Data Analytics also assist organizations to identify non-value-added activities and eliminate waste accordingly.

Innovation & Sustainability in Banks by Big Data Analytics

Big Data Analytics is crucial for banks to innovate and maintain sustainability in the evolving financial industry, enhancing service quality and competitiveness (Poornima and Pushpalatha, 2018). Tailored product offerings to serve specific client demands can be conducted with the help of data analytics. Targeted marketing campaigns are also dependent on advanced data analytics software (Ravi and Kamaruddin, 2017). There is also an interrelationship between societal impacts and the integration of Big Data within the financial industry. Big Data can analyze data regarding energy consumption and carbon emissions as well as resource utilizations of the banks. Organizations that operate with the help of bank credits Can be highlighted if their operations hamper ecological well-being (Hasan, Popp and Oláh, 2020). By integrating strict debt covenants banks can participate in the reduction of environmental footprints and adopt sustainable practices. Social risks are associated with supply chain and investment decisions. Environmental social and governance considerations must be integrated into the decision-making process of financial institutions. Ultimately Big Data analytics can attract socially responsible investors and contribute to bringing positive change in the environment and society. Studies suggest that Big Data analysis plays a critical role in driving innovation and sustainability in banks (Publication Sachin and Kumar, 2020). It facilitates product and service innovation and enhances risk management activities. Optimized operational activities can reduce costs and enhance customer experience while promoting environmentally friendly practices. Banks create long-term value for their stakeholder by focusing on sustainable growth and market competitiveness (He, Hung and Liu, 2022).

Challenges in Big Data Management

Big Data analytics presents significant challenges for organizations due to exponential data volume growth, particularly in the storage and processing capabilities of banks and other financial institutions. (Poornima and Pushpalatha, 2018). The entities can struggle to scale their infrastructure and systems to accommodate the growing data sources. Statistical analysis illustrates that the volume of data is continuously expanding at an unprecedented rate. Big Data can be characterized by diverse sources and formats including structured or unstructured manners. Advanced data analytics present challenges for the organization in terms of data integration and interoperability of the organizations (Indriasari et al., 2019). Traditional data management methods struggle with unstructured or semi-structured data, requiring significant investments and quality and governance challenges, especially in financial and banking institutions. (Bayo Olushola Omoyiola, 2022). Studies show that data quality and governance involve several complexities including inconsistency in data formats and accuracy-related issues. The distributed and decentralized nature of the Big Data environment also creates difficulties in enforcing data governance in banking institutions (Pejić Bach et al., 2019). Robust data quality assurance and governance are essential for Big Data analysis, but security and privacy challenges persist in financial institutions. Implementing comprehensive data security measures and encryption techniques is recommended (Khatib, Shehhi and Nuaimi, 2023). Studies highlight the importance of a data-driven culture to foster collaboration between IT teams and other hierarchies of financial institutions (Khade, 2016). Adequate investment in training and development initiatives can attract and retain top talents within financial markets. Cost and return on investments should be well balanced regarding Big Data Analytics applications. This process is costly and requires significant investments in infrastructure and software as well as personnel (Nobanee et al., 2021). Thorough cost-benefit analysis can reduce the complexity and uncertainty associated with Big Data projects in the financial markets (Ohlhorst, 2021). Articles prioritize quantification of return on investments to evaluate the cost and benefits of Big Data initiatives. Key performance indicators and cloud-based solutions can minimize risks and upfront costs for banks and other financial institutions (Khatib, Shehhi and Nuaimi, 2023).

RESEARCH METHODOLOGY

Overview of Research Methodology

The systematic review and analysis of secondary data sources will provide comprehensive knowledge on the use of Big Data in finance, enhancing understanding of Big Data analytics and its application in financial markets. (Ohlhorst, 2021). For this reason, the literature review process will have a long period from 2010 to 2024. A structured and systematic data collection process will be followed to gather relevant information from published articles and journals regarding Big Data and financial markets.

Research Philosophy

The research philosophy for this study aligns with positivism. Positivism emphasizes the use of secondary data sources to collect relevant data. Positivist research philosophy aims to generate reliable and generalizable knowledge (Nobanee et al., 2021). Positivism emphasizes the objective and systematic analysis of empirical data to uncover underlying patterns and concepts.

This study uses a positivist research philosophy to objectively explore Big Data and finance, systematically reviewing academic research to uncover empirical evidence and generalizable knowledge.

Conceptual Framework

A robust conceptual framework is vital to reinforce the research on Big Data claims in financial institutions. The subsequent theoretic standpoints proposed a substance for understanding how Big Data influences fiscal decision-making and risk management:

Theoretical Underpinnings

- Resource-Based View (RBV): Financial organizations employ Big Data as a strategic or tactical resource to advance a competitive benefit by augmenting operations, improving customer insights, and mitigating risks.

- Diffusion of Innovation (DOI) Theory: Big Data implementation is prejudiced by institutional features such as regulatory necessities, market rivalry, and high-tech willingness.

- Technology Acceptance Model (TAM): This philosophy enlightens how financial organizations implement Big Data analytics founded by apparent efficacy and ease of use.

- Financial Risk Management Theory: Big Data analytics chains uncovering risk, fraud detection, predictive modeling, refining financial steadiness and regulatory compliance.

Conceptual Model

A conceptual model is proposed to demonstrate the association between Big Data applications and financial outcomes:

- Big Data Sources: Customer dealings, market trends, regulatory reports, and social media communications.

- Big Data Applications:

- Predictive Analytics → Prediction of financial movements

- Risk Management → Uncovering fraud and credit scoring

- Client Analysis → Client segmentation and customized services

- Regulatory Compliance → Guaranteeing adherence to fiscal laws

- Financial Outcomes: Advancement decision-making, condensed operational risks, greater customer satisfaction, and amplified profitability.

Data Collection Approach

The purpose of this study is to systematically locate & review academic research focusing on Big Data and Finance or Banks. This will facilitate the research objective to get a comprehensive overview regarding the fundamentals of Big Data, Big Data application in finance & associated challenges. In this regard, secondary data sources will be used to collect relevant data.

Prominent secondary data collection sources include Research Gate, Science Direct, Google Scholar, Springer and Sage (Song, Li and Yu, 2021). The study will explore Big Data analytics, its characteristics and challenges, and its application in financial markets from various researchers’ perspectives, primarily focusing on academic and peer-reviewed journals.

Literature Review Framework

A systematic literature review & data collection process is followed in this research. Initial search conditions to locate & finalize relevant secondary papers are illustrated below in tabular format:

Table 1: Literature Review Framework & Initial Search Conditions

| Activities | Actions |

| Databases to be used | Research Gate, Science Direct, Google Scholar, Springer and Sage |

| Key concepts | Fundamentals of Big Data & application in finance & banking |

| Keywords to be used | Big Data, Financial Services, Banks, Baking Operations, Financial Industry, Risk Management, Big Data Finance, Finance, Big Data Management, Stock market, Predictive Analysis, Big Data in Banking, FinTech, Online Banking, Cybersecurity, Challenges |

| Boolean operators to combine keywords | § “And”

§ “Or” |

| Search span | From 2010 to 2024 |

| Primary language | English |

| Number of literature reviewed | 45 |

| Type of literature reviewed | Scholarly articles, peer-reviewed journals, academic papers & working paper projects. |

| Source: Primary (authors) |

Literature Screening Process

Figure 1: Literature Screening Process (Source: Authors)

Data Analysis & Reporting

Fundamentals of Big Data

Primary Characteristics of Big Data

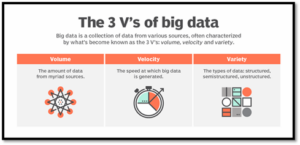

Researchers mostly identified the fundamental characteristics of Big Data as 3Vs (Ongsulee et al., 2018). These are identified as Volume, Velocity and Variety. There is no stead-fast definition for Big Data. Thus, certain conditions are applied to identify Big Data sources.

Volume refers to the scale of data generated collected and stored in various business environments. Big Data involves a huge amount of interrelated or unrelated data sets. This includes structured, unstructured or semi-structured data from a variety of sources. Dynamic business environments and multiple transactions often increase the volume of Big Data (Khatib, Shehhi and Nuaimi, 2023).

Velocity is the speed at which data is generated and processed in real time. Big Data environments deal with high-velocity data streams from multiple sources (Indriasari et al., 2019). Velocity is essential for applications such as real-time analytics, fraud detection, and dynamic pricing. Traditional data processing systems were focused on gathering data in a certain period or scheduled intervals. Due to advancements in data analytics information is generated continuously in large volume.

Figure 2: The 3Vs of Big Data (Indriasari et al., 2019)

Variety in Big Data analytics can be identified as diverse types and formats of data. Structured data can be obtained in a well-defined and organized format. This type of data is highly organized and easily searchable. Traditional database management systems (RDBM) to analyze structured data. Examples include numerical values and texts. Semi-structured data involves the characteristics of both structured and unstructured data sets. It does not conform to the rigid structure of traditional databases but contains some organized elements (Ohlhorst, 2021). The same structured data have irregular and flexible formats. A common example of semi-structured data involves XML and HTML. The third category of data involves unstructured data which is more challenging to process and analyze. It often includes free-form text, multimedia content, images, audio recordings or videos (Lehrer et al., 2018).

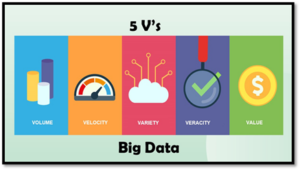

Veracity is related to justifying the reliability and accuracy of data. Big Data Analytics frequently deals with data variations in quality and completeness as well as consistency. Big Data may include errors and inaccuracies (Liu, 2019). This term is also related to implementing data quality assurance techniques. Organizations must validate data sources and contents to identify and correct errors in the data. Veracity ensures reliable insights to make informed decisions with confidence.

Value is the actionable insights that organizations derive from Big Data Analytics. This is the ultimate stage of Big Data. The ultimate goal of Big Data analytics is to extract meaningful insights and drive the decision-making process. By utilizing diverse data sources organizations create value for internal and external stakeholders. Value is linked with operational efficiencies and better risk management processes as well as enhanced client experiences. Big Data analytics can prioritize initiatives that deliver the greatest value for a particular institution (Nie and Nie, 2022).

Figure 3: 5Vs of Big Data (Liu, 2019)

Potential Sources of Big Data for Banks

Banks have access to a wide array of data sources. This involves both internal and external sources. Data sources are leveraged for various purposes such as risk management, customer analytics, fraud detection, and operational efficiency improvements (Marr, 2015).

Table 2: Main Sources of Big Data for Banks

| Data Types | Sources | Usages |

| Transactional Data | ATMs, online banking platforms, mobile apps, and point-of-sale (POS) terminals | Understand customer behaviour, spending patterns, and preferences. |

| Customer Interaction Data | Communication channels including call centre logs, email exchanges, chat transcripts, and social media interactions | Improve customer service, and resolve issues promptly. |

| Demographic Data | Account opening forms and customer interactions | Customer segmentation, assess credit risk & determine loan eligibility. |

| Market & Economic Data | Government reports, central banks, financial exchanges, and legal authorities | Assess market conditions & adjust business strategies accordingly. |

Source: Primary (Authors)

Transactional Data: Transactional data, captured in real-time or near-real-time, includes customer transactions like deposits, withdrawals, transfers, payments, and loans, generating Big Data through various banking channels. (Mohanty, Jagadeesh and Srivatsa, 2013). Transactional data provides insights into customer behavior, spending patterns, and preferences. Banks can use transactional data for customer segmentation, personalized marketing, and product recommendations.

Customer Interaction Data: Communication channels between banks and customers involve call center logs, email exchanges, chat transcripts, and social media interactions. These are defined as customer interaction data. This data can provide valuable insights into customer inquiries, complaints, feedback, and sentiment. Customer interaction data allows banks to improve customer service, and resolve issues promptly to enhance customer satisfaction (Sharma, 2023).

Demographic and Socioeconomic Data: Banks use demographic data to understand their customer base, segment them effectively, and initiate targeted marketing campaigns based on their income levels, employment status, education, and geographic location. (Murugan, T and Marappan, 2023). Additionally, socioeconomic data can assist banks to assess credit risk & determine loan eligibility. Ultimately, banks offer relevant financial products and services to a particular demographic segment.

Market and Economic Data: Market and economic data comprise information about macroeconomic indicators, financial markets, interest rates, inflation rates, and industry trends. Banks gather market and economic data from various sources, including government reports, central banks, financial exchanges, and legal authorities (Wassouf et al., 2020). Market and economic data help banks assess market conditions, forecast trends, and adjust strategies, crucial for risk management, investment decision-making, and portfolio optimization in banking and financial services. (Pejić Bach et al., 2019).

The Application of Big Data in Financial Institutions

Overview of Big Data Application

This section highlights the main areas where Big Data analytics is primarily applied in the context of financial institutions. The areas of application were identified in various studies conducted at different times.

Table 3: Utilization of Big Data in Finance

| Application Area | Studies |

| Financial Management | (Ke and Shi, 2014), (Gao, 2023), (Sun, Shi and Zhang, 2019), (Yang, 2022), (Sharma, 2023), (Hajiheydari et al., 2021), (Dehbi et al., 2022), (Zhu and Yang, 2021) |

| Predictive Analysis | (Poornima and Pushpalatha, 2018), (Ongsulee et al., 2018), (Indriasari et al., 2019), (Broby, 2022), (Sachin and Kumar, 2020), (He, Hung and Liu, 2022) |

| Risk Management & Fraud Detection | (Cerchiello and Giudici, 2016), (Dicuonzo et al., 2019), (Khatib, Shehhi and Nuaimi, 2023), (Nie and Nie, 2022), (Murugan, T and Marappan, 2023), (Liu, 2019) |

| Client Analysis | (Ravi and Kamaruddin, 2017), (Pejić Bach et al., 2019), (Lehrer et al., 2018), (Saidali et al., 2019), (Khade, 2016), (Wassouf et al., 2020), (Soltani Delgosha, Hajiheydari and Fahimi, 2020) |

Source: Primary

Big Data & Financial Management

The process of financial management by Big Data in financial institutions involves several interrelated stages. Each stage utilizes Big Data analytics to optimize decision-making, mitigate risks, and enhance overall performance (Pejić Bach et al., 2019). Here’s a detailed description of the typical process:

Data Collection and Aggregation: Financial institutions including banks & others collect vast amounts of data from various sources. Prominent sources include transaction records, market data & customer information (Khatib, Shehhi and Nuaimi, 2023). External data sources also include social media and governmental or legal documents. Big Data technologies are employed to aggregate, integrate, and store these diverse data sets efficiently. This involves using distributed computing systems, data warehouses, and data lakes to handle large volumes of structured and unstructured data (Ke and Shi, 2014).

Data Cleaning and Preparation: The collected data goes through the cleaning and preparation process before conducting analysis. This process ensures accuracy, consistency, and completeness. One of the fundamental characteristics of Big Data, “Veracity” is involved in this process. This process removes duplicates & irrelevant data and corrects errors. Thus, the synthesized data is stored in standardized formats. This step is crucial to ensure the quality and reliability of the data used for financial management decisions (Gao, 2023). Data preprocessing techniques such as normalization, transformation, and imputation are applied to make the data suitable for analysis.

Table 4: Basic Data Processing Techniques

| Data Processing Techniques | Definitions |

| Normalization | Normalization is the process of scaling numerical data to a standard range. The range typically ranges between 0 and 1 or -1 and 1 (Sun, Shi and Zhang, 2019). |

| Transformation | Transformation involves modifying the distribution of data to make it more suitable for analysis or modelling. Common transformation techniques include log transformation & square root transformation. |

| Imputation | Imputation is the process of replacing missing or corrupted data with substituted values. Missing data is a common issue in Big Data. This can adversely affect the performance of machine learning models if not handled properly. |

Source: Zhu and Yang, 2021

Data Analysis and Modeling: Big Data analytics techniques can be applied to analyze the prepared data and extract actionable insights. This involves statistical analysis, machine learning algorithms, and predictive modelling techniques (Yang, 2022). The analysis can uncover patterns, trends, and relationships within the data of the concerned financial institutions. Studies indicate that financial institutions employ descriptive analysis to understand past performance & diagnostic analysis to identify the root causes of a particular issue. Moreover, predictive analysis can forecast future trends. Ultimately, prescriptive analysis recommends optimal courses of action (Khatib, Shehhi and Nuaimi, 2023).

Table 5: Common Data Analysis Techniques Regarding Big Data

| Data Analysis Modes | Application |

| Descriptive Analysis | To understand past performance |

| Diagnostic Analysis | For the identification of the root causes of a particular issue |

| Predictive Analysis | Forecast future trends |

| Prescriptive Analysis | Recommending the best solution to overcome the issue. |

Source: Yang, 2022

Financial Planning and Forecasting: Big Data analysis aids financial institutions in strategic planning and forecasting, ensuring accurate forecasting by incorporating historical data, market trends, and external factors. (Sharma, 2023). Financial planners of banks & other financial institutions can use scenario analysis and sensitivity analysis through Big Data utilization.

Portfolio Optimization: Financial institutions utilize Big Data analytics to optimize investment portfolios and asset allocations. This involves balancing risk and return objectives to maximize portfolio performance (Broby, 2022). Portfolio optimization models incorporate Big Data analytics to analyze historical performance data, market trends, and correlation matrices. These models can assist financial managers not only in constructing well-diversified portfolios but also in investment goals.

Regulatory Compliance: Compliance with regulatory requirements is a critical aspect of financial management for banks & other financial institutions. Big Data analytics ensure regulatory compliance by monitoring transactions and ensuring adherence to anti-money laundering (AML) and Know Your Customer (KYC) regulations. Big Data analytics analyzes large volumes of transaction data in real-time to identify potential compliance issues (Hajiheydari et al., 2021).

Decision-Making and Strategy Execution: Big Data analytics aids financial institutions in making data-driven decisions on investment strategies, risk management, and operational efficiencies through simulating various scenarios. (Zhu and Yang, 2021). The execution of strategic initiatives and operational plans monitoring based on real-time data. Financial institutions can adapt quickly to changing market conditions through Big Data analytics. Ultimately, Effective utilization of Big Data maximizes value for stakeholders (Hajiheydari et al., 2021).

Predictive Analysis with Big Data

Predictive analysis plays a crucial role in financial institutions by forecasting future trends & identifying risks. The integration of Big Data analytics with predictive modelling can facilitate data-driven decisions in financial institutions.

Exploratory Data Analysis (EDA): Predictive analysis begins with exploratory data analysis. This involves examination of the data to understand characteristics, structure & potential usages. Big Data technologies allow financial institutions to handle large volumes of data efficiently (Poornima and Pushpalatha, 2018). This brings a comprehensive exploration of datasets with millions or even billions of records. Then descriptive statistics, data visualization techniques, and exploratory data mining are used to explore the relationships between variables and detect anomalies or outliers.

Model Selection and Training: Financial institutions employ diverse predictive modelling techniques in Big Data analytics. This involves regression analysis, time series forecasting, machine learning algorithms, and artificial intelligence (AI) models (Begenau, Farboodi and Veldkamp, 2018). The models can learn patterns and relationships within the data to make predictions about future outcomes.

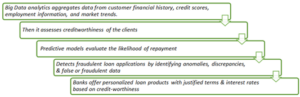

Loan Approval: Predictive analysis in banks streamlines loan approval processes by using big data models to evaluate loan applications based on predefined criteria and risk models. These models identify patterns and trends, allowing faster and more accurate loan approval decisions while minimizing credit risks. This helps financial institutions make informed lending decisions (Indriasari et al., 2019). The summarized process is:

Figure 4: Loan Approval Process of Banks Using Big Data Analytics (Broby, 2022)

Market Trend Forecasting: Big Data technologies collect diverse data sets, including historical market data, news articles, social media sentiment, economic indicators, and geopolitical events. Then the collected data is processed and prepared by the financial institutions for further analysis. Data is transformed and standardized to make it suitable for analysis. Common Big Data sets which are used for market trend analysis include historical price data, trading volumes, economic indicators (e.g., GDP, inflation), sentiment analysis of news articles or social media, and technical indicators (e.g., moving averages, Relative Strength Index). Big Data analytics analyze historical market data to identify patterns and relationships, making predictions about future trends. These predictions are ongoing, requiring regular monitoring and adjustment of predictive models. They are used for stock price forecasting, customer behavior prediction, credit risk estimation, and fraud detection (Broby, 2022).

Table 6: Overview of Forecasting Activities with Big Data

| Activity | Sources | Application |

| Market Trend Forecasting | § Historical market data

§ News articles § Social media sentiment § Economic indicators § Geopolitical events |

§ Forecasting stock prices

§ Short-term intraday trading § Technical indicators (Moving averages, RSI etc.) § Long-term investment strategies § Predicting customer behavior § Credit risk assessment |

Source: Publication Sachin and Kumar, 2020

Risk Management & Fraud Detection with Big Data

Big Data analytics plays a crucial role in identifying, assessing, and mitigating various types of risks faced by financial institutions. This ranges from credit risk, market risk, operational risk, and compliance risk. Predictive modelling techniques can analyze historical data to identify risk factors (Cerchiello and Giudici, 2016). Predictive modelling techniques can also quantify and predict potential losses associated with different types of risks.

Credit Risk: Big Data analytics assesses the creditworthiness of borrowers by analyzing historical data on repayment behavior, credit scores, income levels, and other relevant factors. Predictive modelling techniques, such as logistic regression or machine learning algorithms can quantify the probability of default and potential losses associated with lending activities (Nie and Nie, 2022).

Table 7: Main Activity in Credit Risk Analysis

| Main Activity | Process |

| Predictive Modeling | Predictive modelling techniques are statistical and machine learning methods. Predictive Modeling is used to predict future outcomes based on historical data and known factors (Liu, 2019). These techniques analyze patterns and relationships within the data to make predictions about future events or behaviors. Financial institutions use predictive models to assess the creditworthiness of borrowers and determine the likelihood of default. |

Source: Liu, 2019

Market Risk: Big Data analytics can also evaluate market risk by analyzing historical market data, including stock prices, interest rates, exchange rates, and commodity prices. Statistical models, time series analysis, and scenario simulations quantify the potential impact of market fluctuations on investment portfolios, trading positions, and financial performance (Begenau, Farboodi and Veldkamp, 2018).

Table 8: Main Activity in Market Risk Analysis

| Main Activity | Process |

| Time Series Analysis | Time series analysis techniques model and forecast data points collected at regular intervals over time. Banks & financial institutions apply time series analysis for forecasting financial metrics deposit growth, interest rates, and stock prices (Khatib, Shehhi and Nuaimi, 2023). |

| Scenario Simulations | Scenario analysis evaluates the potential impact of different hypothetical scenarios on financial performance, balance sheet, and risk exposures of financial institutions. Banks conduct scenario analysis to assess the impact of a severe economic downturn, interest rate fluctuations, or geopolitical events on operations and profitability. This is one kind of what-if analysis. |

Source: Dicuonzo et al., 2019

Operational Risk: These risks arise from internal processes, systems, and human error within financial institutions. Data mining techniques analyze operational data, incident reports, and historical patterns to identify potential weaknesses, vulnerabilities, and areas of operational risk exposure.

Table 9: Main Activity in Operational Risk Analysis

| Main Activity | Process |

| Data Mining | Data mining is the process of discovering patterns, relationships, and insights from large volumes of financial data to support decision-making. Data mining collects data from various sources, including transaction records, customer information, market data, economic indicators, social media, and news feeds (Khatib, Shehhi and Nuaimi, 2023). |

Source: Khatib, Shehhi and Nuaimi, 2023

Fraud Detection: Big Data analytics detects anomalies or deviations from normal behavior in transactional data. Big Data analytics applies Pattern recognition techniques to identify unusual patterns, outliers, or discrepancies in transaction volumes, amounts, frequencies, and locations. These deviations may indicate fraudulent behavior (Nie and Nie, 2022). Moreover, Big Data analytics conducts a behavioral analysis of customers and transactions to identify suspicious activities or patterns. Behavioral analyses use historical transaction data to build profiles of normal behavior for individual customers (Dicuonzo et al., 2019). Then the process can detect deviations or anomalies from their typical behavior. Big Data analytics implements a text mining process to analyze unstructured data from sources such as emails, chat logs, and social media feeds. Text mining can uncover fraud-related information and sentiment.

Table 10: Main Activity in Fraud Detection

| Main Activity | Process |

| Pattern Recognition | Pattern recognition techniques involve the identification of regularities or patterns within data that may indicate fraudulent behavior. Pattern recognition analyzes the relationships and connections between customer accounts & transactions. This can uncover suspicious linkages and patterns within transaction data & potential fraudulent schemes. |

| Behavioral Analysis | Behavioral analysis focuses on understanding the behavior of individuals or entities based on their historical actions and interactions. Behavioral analysis creates profiles of individual customers based on their transaction history, spending patterns, geographic locations, and other behavioral attributes (Liu, 2019). Thus, behavioral analysis forecasts future behavior and identifies potential fraud risks |

| Text Mining | Text mining techniques extract actionable insights from textual data & identify keywords, phrases, or sentiments associated with fraudulent activities or intentions. |

Source: Murugan, T and Marappan, 2023

Client Analysis with Big Data

Big Data Analytics analyzes clients by leveraging large volumes of customer-related data. Financial institutions can gain insights into customer behavior, preferences, and needs. By analyzing these data, banks properly understand their customers & offer specific products and services.

Customer Segmentation and Targeting: Banks collect vast amounts of customer data from various sources, including transaction records, account information, demographic details, customer interactions, and feedback. Big Data technologies enable banks to aggregate, store, and manage this data efficiently. This captures both structured and unstructured data from disparate sources (Ravi and Kamaruddin, 2017). Big Data analytics is used to segment customers into groups based on common characteristics, behaviors, and needs. Once segments are identified, banks profile each segment to understand their unique characteristics, preferences, and needs (Saidali et al., 2019). Customer segmentation assists banks in delivering customized services according to each segment’s preferences. The process can be simplified as:

Table 11: Process of Customer Segmenting & Targeting with Big Data

Source: Pejić Bach et al., 2019

Behavioral Analysis: Big Data analytics conducts a behavioral analysis of customers to understand their preferences, habits, and interactions with the bank. Big Data analytics can identify behavioral patterns and trends within customer data (Saidali et al., 2019). Big Data and customer journey mapping techniques help banks understand customer interactions, anticipate future preferences, and identify service bottlenecks through predictive modelling and visualization (Wassouf et al., 2020). For example, if behavioral data indicates that customers are dissatisfied with a particular feature or service, financial institutions can rectify or enhance it to optimize customer experience.

Personalized Marketing and Offers: Based on behavioral insights, banks develop personalized marketing campaigns and targeted offers tailored to individual customer preferences and needs. Personalized messages, product recommendations, promotional offers & discounts can be delivered through email, mobile apps, websites, and social media. Big Data analytics identifies cross-selling and upselling opportunities within each segment based on customer behavior and preferences (Soltani Delgosha, Hajiheydari and Fahimi, 2020). Targeted recommendations and offers are provided to customers based on their transaction history & product usage.

Table 12: Personalized Product Recommendations Using Big Data (Khade, 2016)

| Main Activity | Process |

| Cross-Selling | Cross-selling is the practice of offering additional products or services that complement a customer’s existing relationship with the bank. These products or services are typically related to the customer’s current needs or interests. If a customer has a savings account the bank may cross-sell additional products including credit cards, personal loans, mortgages, investment accounts, or insurance policy. |

| Up-Selling | Upselling is the practice of encouraging customers to upgrade or purchase a higher-value version of a product or service they already have. Upselling typically involves offering a premium checking account with additional benefits such as higher interest rates, unlimited transactions, enhanced features & other premium options at a higher price point. |

Source: Khade, 2016

Challenges Associated with Big Data

Although Big Data analytics offers significant opportunities for the finance industry, it also comes with several challenges. Challenges are multidimensional as identified by the researchers. Some of the main factors include:

Data Quality & Accuracy: Financial data encompasses a wide range of information, including transaction records, market data, customer details, and regulatory filings. This data often comes from multiple sources in both structured and unstructured formats. Data sets with diverse sources face challenges in completeness and consistency, leading to inaccuracies and errors, including manual data entry, system glitches, and discrepancies in data integration processes (Bayo Olushola Omoyiola, 2022). Financial data with missing or incomplete information can impact analysis accuracy, reliability, and timeliness, which is crucial in finance for accurate interpretations (Rawat and Yadav, 2021). Decisions can be made based on real-time or near-real-time data. Delays in data processing, ingestion, or availability can impact the accuracy and relevance of analysis. This issue becomes more severe, especially in fast-paced trading environments (Investment companies, brokers, banks etc.) where split-second decisions are critical.

Table 13: Data Quality & Accuracy Related Issues

| Key Issues | Explanations |

| Data Variety | Involves structured, unstructured, incomplete and inconsistent data. Diverse data types can degrade data quality and accuracy. |

| Timeliness | Potential delays in Big Data processing & analysis reduce information relevance. |

Source: Primary (Authors)

Data Privacy & Security: Big Data in finance includes customer transactions, account details, and sensitive personal information. These are highly confidential and valuable. Unauthorized access or breaches of this data can lead to financial losses and reputational damage for financial institutions. Breaches of financial data can result in financial fraud, legal liabilities, regulatory fines, and loss of customer trust (Fan, Han and Liu, 2014). Banks face cyberattacks due to sensitive financial data, including phishing, malware, ransomware, and insider threats. Outsourcing services to third parties increases privacy risks, necessitating encryption of sensitive data to prevent unauthorized access (Hariri, Fredericks and Bowers, 2019). However, Encryption of Big Data is very challenging due to the volume, velocity, and variety of data involved. Another concept related is Insider threats. Negligent employees of financial institutions increase significant risks to data privacy and security. Multi-level employees often have access to sensitive financial data. Intentionally or unintentionally the involved insiders can misuse or disclose this information. This will lead to data breaches & compliance violations (Rawat and Yadav, 2021).

Table 14: Data Privacy & Security Related Risks (Rawat and Yadav, 2021)

| Key Issues | Explanations |

| Cybersecurity Threats | Involves unauthorized access, malware attacks & suspicious activities. |

| Third-Party Risks | Reliance on external parties reduces control over sensitive information. |

| Data Encryption | Due to the volume, variety & velocity of Big Data, complete data encryption is not possible. |

| Insider Threats | Negligent employees intentionally or unintentionally may misuse sensitive data. |

Source: Rawat and Yadav, 2021

Resource Intensive: Big Data in finance necessitates significant infrastructure investments and skilled professionals for real-time data analysis, requiring advanced computing power, storage capacity, and long-term investments in cloud-based infrastructure and distributed computing technologies (Fan, Han and Liu, 2014). There is a shortage of skilled professionals in the market to properly understand & analyze Big Data. Professionals include data scientists, analysts, and professionals with expertise in Big Data analytics, machine learning, and data visualization in the finance industry. Financial institutions need a diverse workforce with the necessary technical skills. Not only there are talent gaps in the market but also financial institutions need investments for recruiting, training, and developing technical personnel (Balachandran and Prasad, 2017).

Table 15: Key Issues Related to Resource Requirements

| Key Issues | Explanations |

| Infrastructural Investments | Require investments in advanced computing power and huge storage capacities. |

| HR Investments | Resources are required to attract, retain & develop relevant technical professionals from the market. |

Source: Primary (Authors)

Concluding Remarks

Recommendation

This segment addresses the challenges of Big Data analytics in financial institutions, emphasizing the need for a strategic and holistic approach to overcome these issues. Synthesized recommendations from previous scholars & secondary sources can be summarized as:

- Strengthen Data Governance and Quality Management

To implement robust data governance frameworks to ensure accuracy, consistency, and security is a necessity. To maintain high-quality datasets AI-driven data validation tools need to be utilized (Saidali et al., 2019).

- Enhance Cybersecurity Measures

The finance industry can deploy advanced encryption and multi-factor authentication to protect sensitive financial data. Cybersecurity measures are essential to protect sensitive financial data (Khatib, Shehhi and Nuaimi, 2023). Financial organizations must conduct regular security audits to identify vulnerabilities and strengthen cybersecurity protocols to identify loopholes and address security gaps.

- Increase Investments in Advanced Analytics

Financial institutions should adopt machine learning and AI-driven analytics for real-time fraud detection and predictive modeling to effectively analyze Big Data. Investments can be made in scalable infrastructure, cloud computing, and distributed computing frameworks to handle large volumes of data and perform real-time analytics (Dicuonzo et al., 2019). Integration of cloud computing and scalable infrastructure may enhance efficiency to handle large data volumes.

- Develop a Data-Driven Organizational Culture

Financial analysts and decision-makers should be trained in Big Data analytics. Training is required for the employees on data privacy, security protocols, and regulatory compliance requirements (Yang, 2022). Financial organizations need to foster cross-departmental collaboration to enhance data utilization in strategic planning. Data literacy can effectively mitigate the risks of data breaches and insider threats.

- Align Big Data Strategies with Regulatory Compliance

Safeguarding financial institutions adhere to data protection laws and banking regulations. Immediate implementation of automated compliance monitoring systems is needed for preventing regulatory breaches.

- Optimize Customer Experience through Big Data Insights

Predictive analytics should be used for offering personalized financial products. Improving customer segmentation to enhance marketing strategies and customer engagement is a necessity.

- Conduct Cost-Benefit Analysis for Big Data Investments

Evaluation of ROI before implementing Big Data solutions is essential. It is better to balance technological advancements with cost efficiency for maximizing financial performance.

CONCLUSION

Big Data revolutionizes financial institutions by aligning decision-making, risk management, and customer engagement activities, enabling banks to uncover valuable insights from vast data volumes (Al-lozi et al., 2022). The insights gained from Big Data analytics are essential to drive innovation & maintain competitiveness. However, certain challenges are associated with Big Data which must be carefully addressed to harness the full potential of Big Data. The strategic adoption of Big Data technologies offers huge opportunities for financial institutions to thrive in an increasingly data-driven world & deliver superior value to the stakeholders.By integrating theoretical foundations and actionable insights, financial institutions can improve decision-making, augment risk management, and drive innovation successfully.

Research Limitations & Scopes for Further Studies

This study is based on a systematic literature review process about Big Data analytics within banks & other financial institutions. The study explored certain crucial applications of Big Data technologies in financial institutions. Moreover, various challenges associated with Big Data are also discussed with relevant risk mitigation strategies. One of the prime limitations of this research is the limited sample size. Reliable & relevant secondary data sources related to this topic were very limited. There are also time constraints to analyze the research objectives & findings in more detail. Further studies are required including longitudinal studies to examine the long-term impact and evolution of Big Data in financial institutions over time. A comparative analysis can also be done in this regard. By comparing the application of Big Data across different types of financial institutions (e.g., banks, insurance companies, and investment firms) future studies can identify variations, best practices, and areas for improvement.

REFERENCES

- Al-Lozi, E., Alfityani, A., Alsmadi, A. A., Al_Hazimeh, A. M., & Al-Gasawneh, J. A. (2022). The role of big data in financial sector: A review paper. International Journal of Data and Network Science, 6(4), 1319–1330. https://doi.org/10.5267/j.ijdns.2022.6.003

- Balachandran, B. M., & Prasad, S. (2017). Challenges and benefits of deploying big data analytics in the cloud for business intelligence. Procedia Computer Science, 112, 1112–1122. https://doi.org/10.1016/j.procs.2017.08.138

- Bayo Olushola Omoyiola (2022). The social implications, risks, challenges and opportunities of big data. Emerald open research, 1(4). https://doi.org/10.1108/eor-04-2023-0014

- Begenau, J., Farboodi, M. and Veldkamp, L. (2018). Big data in finance and the growth of large firms. Journal of Monetary Economics, [online] 97(56), pp.71–87. https://doi.org/10.1016/j.jmoneco.2018.05.013

- Bose, R. (2018). Understanding management data systems for enterprise performance management. Industrial Management & Data Systems, 106(1), pp.43–59. https://doi.org/10.1108/02635570610640988

- Broby, D. (2022). The use of predictive analytics in finance. The Journal of Finance and Data Science, [online] 8(3), pp.145–161. https://doi.org/10.1016/j.jfds.2022.05.003

- Cerchiello, P. and Giudici, P. (2016). Big data analysis for financial risk management. Journal of Big Data, 3(1). https://doi.org/10.1186/s40537-016-0053-4

- Chang, V., Xiao, L., Xu, Q. and Arami, M. (2020). A Review Paper on the Application of Big Data by Banking Institutions and Related Ethical Issues and Responses. Proceedings of the 2nd International Conference on Finance, Economics, Management and IT Business, [online] 5(978-989-758-422-0), pp.115–121. https://doi.org/10.5220/0009427701150121

- Dehbi, S., Lamrani, H.C., Belgnaoui, T. and Lafou, T. (2022). Big Data Analytics and Management Control. Procedia Computer Science, [online] 203(203), pp.438–443. https://doi.org/10.1016/j.procs.2022.07.058

- Dicuonzo, G., Galeone, G., Zappimbulso, E. and Dell’Atti, V. (2019). Risk Management 4.0: The Role of Big Data Analytics in the Bank Sector. International Journal of Economics and Financial Issues, 9(6), pp.40–47. https://doi.org/10.32479/ijefi.8556

- Fan, J., Han, F. and Liu, H. (2014). Challenges of Big Data analysis. National Science Review, [online] 1(2), pp.293–314. https://doi.org/10.1093/nsr/nwt032

- Gao, J. (2023). Importance of Introducing Big Data into Financial Management. International Journal of Science Technology and Society, 42(3). https://doi.org/10.57237/j.jsts.2023.01.002

- Hajiheydari, N., Delgosha, M.S., Wang, Y. and Olya, H. (2021). Exploring the paths to big data analytics implementation success in banking and financial service: an integrated approach. Industrial Management & Data Systems, 121(12), pp.2498–2529. https://doi.org/10.1108/imds-04-2021-0209

- Hariri, R.H., Fredericks, E.M. and Bowers, K.M. (2019). Uncertainty in Big Data analytics: survey, opportunities, and Challenges. Journal of Big Data, [online] 6(1), pp.1–16. https://journalofbigdata.springeropen.com/articles/10.1186/s40537-019-0206-3

- Hasan, Md. M., Popp, J. and Oláh, J. (2020). Current landscape and influence of big data on finance. Journal of Big Data, 7(1), pp.1–17. https://doi.org/10.1186/s40537-020-00291-z

- He, W., Hung, J.-L. and Liu, L. (2022). Impact of Big Data Analytics on banking: a Case Study. Journal of Enterprise Information Management, 36(2), pp.459–479. https://doi.org/10.1108/jeim-05-2020-0176

- Indriasari, E., Soeparno, H., Gaol, F.L. and Matsuo, T. (2019). Application of Predictive Analytics at Financial Institutions: A Systematic Literature Review. 2019 8th International Congress on Advanced Applied Informatics (IIAI-AAI), 42131(3). https://doi.org/10.1109/iiai-aai.2019.00178

- Ke, M. and Shi, Y. (2014). Big Data, Big Change: In the Financial Management. Open Journal of Accounting, 03(04), pp.77–82. https://doi.org/10.4236/ojacct.2014.34009

- Khade, A.A. (2016). Performing Customer Behavior Analysis using Big Data Analytics. Procedia Computer Science, [online] 79(1), pp.986–992. https://doi.org/10.1016/j.procs.2016.03.125

- Khatib, M.E., Shehhi, H.A. and Nuaimi, M.A. (2023). How Big Data and Big Data Analytics Mediate Organizational Risk Management? Journal of Financial Risk Management, 12(01), pp.1–14. https://doi.org/10.4236/jfrm.2023.121001

- Lehrer, C., Wieneke, A., vom Brocke, J., Jung, R. and Seidel, S. (2018). How Big Data Analytics Enables Service Innovation: Materiality, Affordance, and the Individualization of Service. Journal of Management Information Systems, 35(2), pp.424–460. https://doi.org/10.1080/07421222.2018.1451953

- Liu, Q. (2019). Research on Risk Management of Big Data and Machine Learning Insurance Based on Internet Finance. Journal of Physics: Conference Series, 1345(1), p.052076. https://doi.org/10.1088/1742-6596/1345/5/052076

- Marr, B. (2015). Big data: Using smart big data, analytics and metrics to make better decisions and improve performance. Chichester, West Sussex, United Kingdom; Hoboken, New Jersey: John Wiley and Sons, Inc.

- Mohanty, S., Jagadeesh, M. and Srivatsa, H. (2013). Big data imperatives: enterprise big data warehouse, BI implementations and analytics. New York press.

- Murugan, M.S., T, S.K. and Marappan, R. (2023). Large-scale data-driven financial risk management & analysis using machine learning strategies. Measurement: Sensors, 6421(2), p.100756. https://doi.org/10.1016/j.measen.2023.100756

- Nie, Y. and Nie, Q. (2022). Application of Big Data Analysis Technology in Financial Investment Risk Management. Atlantis Highlights in Intelligent Systems, [online] 126312(2), pp.998–1003. https://doi.org/10.2991/978-94-6463-030-5_98

- Nobanee, H., Dilshad, M.N., Al Dhanhani, M., Al Neyadi, M., Al Qubaisi, S. and Al Shamsi, S. (2021). Big Data Applications the Banking Sector: A Bibliometric Analysis Approach. SAGE Open, 11(4). https://doi.org/10.1177/21582440211067234

- Ohlhorst, F. (2021). Big data analytics: turning big data into big money. 6th ed. Hoboken, N.J.: Wiley.

- Ongsulee, P., Chotchaung, V., Bamrungsi, E. and Rodcheewit, T. (2018). Big Data, Predictive Analytics and Machine Learning. [online] IEEE Xplore. https://doi.org/10.1109/ICTKE.2018.8612393

- Pejić Bach, M., Krstić, Ž., Seljan, S. and Turulja, L. (2019). Text Mining for Big Data Analysis in Financial Sector: A Literature Review. Sustainability, 11(5), p.1277. https://doi.org/10.3390/su11051277

- Poornima, S. and Pushpalatha, M. (2018). A survey of predictive analytics using big data with data mining. International Journal of Bioinformatics Research and Applications, 14(3), p.269. https://doi.org/10.1504/ijbra.2018.092697

- Publication Sachin, S. and Kumar (2020). Banking and Financial Analytics -An Emerging Big Opportunity Based on Online Big Data. Springer, [online] ISSN (2), pp.2581–6942. https://doi.org/10.5281/zenodo.4451571

- Ravi, V. and Kamaruddin, S. (2017). Big Data Analytics Enabled Smart Financial Services: Opportunities and Challenges. Big Data Analytics, 10721(2), pp.15–39. https://doi.org/10.1007/978-3-319-72413-3_2

- Rawat, R. and Yadav, R. (2021). Big Data: Big Data Analysis, Issues and Challenges and Technologies. IOP Conference Series: Materials Science and Engineering, [online] 1022(1), p.012014. https://doi.org/10.1088/1757-899x/1022/1/012014

- Saidali, J., Rahich, H., Tabaa, Y. and Medouri, A. (2019). The combination between Big Data and Marketing Strategies to gain valuable Business Insights for better Production Success. Procedia Manufacturing, [online] 32(3), pp.1017–1023. https://doi.org/10.1016/j.promfg.2019.02.316

- Sharma, S. (2023). Big data in finance: A systematic literature review. AIP Conference Proceedings, [online] 2909(1). https://doi.org/10.1063/5.0182378

- Soltani Delgosha, M., Hajiheydari, N. and Fahimi, S.M. (2020). Elucidation of big data analytics in banking: a four-stage Delphi study. Journal of Enterprise Information Management, [online] ahead-of-print(ahead-of-print). https://doi.org/10.1108/jeim-03-2019-0097

- Song, H., Li, M. and Yu, K. (2021). Big data analytics in digital platforms: how do financial service providers customize supply chain finance? International Journal of Operations & Production Management, 41(4), pp.410–435. https://doi.org/10.1108/ijopm-07-2020-0485

- Subrahmanyam, A. (2019). Big data in finance: Evidence and challenges. Borsa Istanbul Review, [online] 8(71641), pp.112–140. https://doi.org/10.1016/j.bir.2019.07.007

- Sun, Y., Shi, Y. and Zhang, Z. (2019). Finance Big Data: Management, Analysis, and Applications. International Journal of Electronic Commerce, 23(1), pp.9–11. https://doi.org/10.1080/10864415.2018.1512270

- Wassouf, W.N., Alkhatib, R., Salloum, K. and Balloul, S. (2020). Predictive analytics using big data for increased customer loyalty: Syriatel Telecom Company case study. Journal of Big Data, [online] 7(1). https://doi.org/10.1186/s40537-020-00290-0

- Yang, D., Chen, P., Shi, F. and Wen, C. (2017). Internet Finance: Its Uncertain Legal Foundations and the Role of Big Data in Its Development. Emerging Markets Finance and Trade, 54(4), pp.721–732. https://doi.org/10.1080/1540496x.2016.1278528

- Yang, Q. (2022). Application of Big Data Technology in the Construction of Intelligent Financial Management System. Proceedings of the 2022 2nd International Conference on Education, Information Management and Service Science (EIMSS 2022), 1231(2), pp.71–77. https://doi.org/10.2991/978-94-6463-024-4_9

- Yu, W., Wong, C.Y., Chavez, R. and Jacobs, M.A. (2021). Integrating big data analytics into supply chain finance: The roles of information processing and data-driven culture. International Journal of Production Economics, 236(1), p.108135. https://doi.org/10.1016/j.ijpe.2021.108135

- Zhu, X. and Yang, Y. (2021). Big Data Analytics for Improving Financial Performance and Sustainability. Journal of Systems Science and Information, 9(2), pp.175–191. https://doi.org/10.21078/jssi-2021-175-17

APPENDICES

List of Tables

| Table | Title |

| 1 | Literature Review Framework & Initial Search Conditions (Source: Authors) |

| 2 | Main Sources of Big Data for Banks (Source: Authors) |

| 3 | Utilization of Big Data in Finance (Source: Authors) |

| 4 | Basic Data Processing Techniques (Source: Zhu and Yang, 2021) |

| 5 | Common Data Analysis Techniques Regarding Big Data (Source: Yang, 2022) |

| 6 | Overview of Forecasting Activities with Big Data (Source: Publication Sachin and Kumar, 2020) |

| 7 | Main Activity in Credit Risk Analysis (Source: Liu, 2019) |

| 8 | Main Activity in Market Risk Analysis (Source: Dicuonzo et al., 2019) |

| 9 | Main Activity in Operational Risk Analysis (Source: Khatib, Shehhi and Nuaimi, 2023) |

| 10 | Main Activity in Fraud Detection (Source: Murugan, T and Marappan, 2023) |

| 11 | Process of Customer Segmenting & Targeting with Big Data (Source: Pejić Bach et al., 2019) |

| 12 | Personalized Product Recommendations Using Big Data (Source: Khade, 2016) |

| 13 | Data Quality & Accuracy Related Issues (Source: Authors) |

| 14 | Data Privacy & Security Related Risks (Source: Rawat and Yadav, 2021) |

| 15 | Key Issues Related to Resource Requirements (Source: Authors) |

List of Figures

| Figure | Title |

| 1 | Literature Screening Process (Source: Authors) |

| 2 | The 3Vs of Big Data (Source: Indriasari et al., 2019) |

| 3 | 5Vs of Big Data (Source: Liu, 2019) |

| 4 | Loan Approval Process of Banks Using Big Data Analytics (Source: Broby, 2022) |