An Investigation of the Determinants of Non-Tax Compliance among Small and Medium Enterprises: Case Study of Green Market, Mutare

- Liberty D Mudzengerere

- Kudzai Munyawarara

- Kudakwashe Munyepwa

- Memory Matsikure Cheure

- Allen Mutumwa

- Denny Chakauya

- Tafadzwa Mudadi

- Tinashe Mudzengerere

- 771-806

- Mar 17, 2025

- Education

An Investigation of the Determinants of Non-Tax Compliance among Small and Medium Enterprises: Case Study of Green Market, Mutare

Liberty D Mudzengerere, Kudzai Munyawarara, Kudakwashe Munyepwa, Memory Matsikure Cheure, Allen Mutumwa, Denny Chakauya, Tafadzwa Mudadi, Tinashe Mudzengerere

Manicaland State University, Mutare, Manicaland, Zimbabwe

DOI: https://doi.org/10.51244/IJRSI.2025.12020062

Received: 10 February 2025; Accepted: 15 February 2025; Published: 17 March 2025

ABSTRACT

Tax compliance is crucial for both individuals and businesses to fulfill their financial obligations accurately. Small and Medium Enterprises (SMEs) are vital to economic growth but ensuring their tax compliance is a global challenge. This study sought to assess, identify and analyze the key determinants of non-tax compliance with specific reference to SMEs at Green Market, Mutare. The sample comprised of 90 participants who were selected through the use of stratified random sampling procedure. The descriptive survey design and the mixed method approach were adopted for this study. Data collection was done using a semi-structured questionnaire and personal interviews for triangulation purposes. Qualitative data was analyzed according to emerging themes, while quantitative data was presented and analyzed using IBM SPSS (version 21.0). Integration of rational choice theory, deterrence and the social capital theory formed the foundations for this study. The study was guided by both positivism and interpretivism paradigm. The study revealed that institutional, social and economic factors affect tax compliance for SMEs at Green Market. The correlation between level of information access and provision of support services by business development organisations and improved tax compliance was also revealed via the use of Pearson’s coefficient correlation. The Kaiser Meyer-Olkin and Bartlett’s test were used to reveal significant factors where social and economic factors were noted. The study highlighted some strategies that could be adopted by ZIMRA which includes extended payment deadlines, public awareness campaign and provision of online chat-bot and support services. From the findings it can be concluded that there is need for all SMEs to appreciate the role of tax compliance since tax contribute to the nation’s development. Level of access to information and provision of support services from BDOs should be consistent and ZIMRA should prioritize the implementation of an online tax chat-bot to provide immediate assistance to taxpayers. This study suggests that scholars could expand the current research by expanding the sample frame to all SMEs in Zimbabwe. Further studies should incorporate the impact of digitalization on tax compliance investigating on how the digital divide may impact SME tax compliance, particularly in rural areas or among businesses with limited technological resources.

Keywords: SME, tax compliance, business development organisation

INTRODUCTION AND BACKGROUND

The importance of tax compliance has grown significantly for both individuals and businesses in developed and developing countries alike. It ensures taxpayers fulfil their responsibility of reporting income accurately, which in turn determines their fair share of taxes owed. Small and Medium Enterprises (SMEs) play a critical role in economic development, particularly in emerging economies like Zimbabwe (Dlamini and Schutte, 2020). Gherghina et al., (2020) pointed out that SMEs contribute significantly to job creation, innovation, and national output. However, ensuring tax compliance among SMEs remains a persistent challenge for governments worldwide, including Zimbabwe (Mpofu, 2023).

Alm (2019) defined tax compliance as the fulfillment of all legal tax obligations by individuals or businesses. This encompasses paying the correct amount of tax, based on taxable income or activity, as defined by the relevant tax laws and regulations. It also includes filing tax returns accurately and on time, thus providing all necessary information to the tax authorities and maintaining proper records of income, expenses, and other relevant financial data for verification purposes. Taxes are the lifeblood of any government, providing the resources needed to fund essential public services, infrastructure development, social programs and infrastructure development (Bihabwa, 2017; Taddesse, 2023; Oyedokun et al., 2024). When SMEs comply with tax regulations, they contribute their fair share to supporting critical functions. It also fosters a sense of fairness and accountability within a society and promotes a level playing field for businesses, promoting fair competition and economic growth.

In Zimbabwe, the definition of an SME (Small and Medium Enterprise) is based on annual turnover and is categorized by the Zimbabwe Revenue Authority (ZIMRA) (Jachi & Muchongwe, 2019; Dlamini et al., 2020). SMEs are contributing between 40% and 60% of the GDP in Sub-Saharan African countries (Dlamini and Schutte, 2020). The Small and medium enterprise act of Zimbabwe (24:12) defines an SME as a business that employees 6-75 permanent employees with an asset base of USD$250000 to USD$ 2 million and an annual turnover of USD $500 000 to USD $3 million (Finance Act, 2018; RBZ, 2013; ZIMRA, 2016). A 2021 survey carried out by the Zimbabwe National Chamber of Commerce (ZNCC) revealed that a significant portion of SMEs perceive the tax system as unfair and lacking transparency. This perception stems from concerns about corruption within the tax administration and the uneven distribution of collected revenue. This effected into negative perception leading to a decrease in trust towards the tax system, discouraging voluntary compliance and potentially increasing instances of tax evasion. Transparency International Zimbabwe’s 2022 Corruption Perception Index ranked the country 157th out of 180 countries, indicating a high perception of corruption (Transparency International Zimbabwe, 2022). This perception, even if not directly linked to tax administration, can erode trust in the system and discourage voluntary compliance among SMEs.

It has also been noted that in Zimbabwe 52% of surveyed SMEs lacked a clear understanding of their tax filing deadlines and obligations (Nyamwanza et al., 2014). This knowledge gap directly impacts compliance, as many businesses unintentionally miss deadlines or fail to report income accurately. Mutanga et al., (2021) also concur with the observation, they corroborate that the complex and bureaucratic nature of the Zimbabwean tax system, particularly for SMEs, demotivated compliance (IMF, 2018; CZI, 2020). The study cited instances where business owners expressed difficulty navigating the tax code and filing procedures, leading to unintentional errors and missed deadlines however this complexity translates to lower tax compliance as evidenced by the high number of unfiled tax returns and discrepancies in reported income.

Ussif et al., (2020) postulated that SMEs are the backbone of Zimbabwe’s economy, contributing significantly to the Gross Domestic Product (GDP). Estimates suggest SMEs represent over 90% of registered businesses and contribute approximately 60% of total employment in the country (Gherghinaet al., 2020). Their vitality is crucial for driving economic growth and reducing poverty. Mwamba et al., (2022) vowed that SMEs are considered the crucial link between Zimbabwe’s current economic state and achieving the goal of becoming an upper-middle income economy by 2030. SMEs as engines of growth (Gherghinaet al., 2020), as they are a major source of employment. SMEs enable innovation and diversification (Bodlaj et al., 2020), which enables them to enter foreign markets. It also fosters a culture of entrepreneurship attracting investment (Gherghinaet al., 2020), and encouraging individuals to start and grow their own businesses. This injects dynamism and growth potential into the economy.

While limited specifically to Zimbabwe, research on tax compliance among SMEs across various contexts offers valuable insights. Studies have examined factors like cost-benefit calculations of compliance, perceived risk of penalties, and perceptions of fairness and government effectiveness. Achieving tax compliance among SMEs in Zimbabwe is critical for sustainable economic growth and national development. The researcher is assured that there remains a gap which must be covered in the area adjoining tax compliance among SMEs in Zimbabwe, and it is against this background that this research undertakes a comprehensive evaluation of factors influencing tax compliance among SMEs in Zimbabwe. Thus, the study aims to provide valuable insights for policymakers, tax authorities, and business development organizations (BDOs) in their efforts to foster a culture of tax compliance within the SME sector.

Statement of the problem

SMEs are the engine of economic growth in Zimbabwe (Watambwa & Shilongo, 2021). They contribute significantly to job creation, innovation, and national output. However, despite their critical role, a persistent challenge plagues this vital sector – low tax compliance. Failing to collect taxes from SMEs has significant consequences on the Zimbabwean economy. Uncollected tax revenue translates into a lack of resources for essential public services like infrastructure development, education, and healthcare (Mathew, 2022). This impedes national development and creates a vicious cycle. Without adequate public services, the environment for business growth weakens, hindering the very sector that could drive economic prosperity. The issue extends beyond lost revenue. A culture of non-compliance creates an unfair playing field, disadvantaging businesses that adhere to regulations. Informal or non-compliant businesses may enjoy lower costs by avoiding taxes, allowing them to undercut prices and potentially stifle the growth of compliant competitors. This stifles a healthy business environment and discourages further investment in the formal sector. The issue of low tax compliance among SMEs in Zimbabwe is not singular; it’s a complex web of challenges which include resource constraints, perceptions of corruption and inefficiency, navigating complexity, and limited support systems. Therefore, a holistic approach is required to address it effectively. Understanding the interplay between resource limitations, informal practices, perceptions of inefficiency, and lack of support is crucial, hence, the need to evaluate the factors influencing tax compliance in Zimbabwean SMEs.

General Objective

The primary objective of this research was to identify and analyze the key determinants of non-tax compliance: Case study of SMEs at Green Market, Mutare.

Specific Objectives

- To establish the extent to which formal and informal institutional factors, alongside business owner characteristics and firm-specific attributes, contribute to non-tax compliance among SMEs at Green market downtown, Mutare.

- To determine if the level of access to information and support services provided by business development organizations (BDOs) correlate with improved tax compliance behavior among SMEs in the green market

- To craft ways in which ZIMRA can tailor its tax compliance strategies so as to effectively address the knowledge gaps, administrative burdens, and trust perceptions of SMEs in Zimbabwe, leading to increased tax compliance

Research questions

- To what extent do formal and informal institutional factors, alongside business owner characteristics and firm-specific attributes, contribute to non-tax compliance among SMEs at Green market downtown, Mutare?

- Does the level of access to information and support services provided by business development organizations (BDOs) correlate with improved tax compliance behavior among SMEs in the green market?

- How can ZIMRA tailor its tax compliance strategies to effectively address the knowledge gaps, administrative burdens, and trust perceptions of SMEs in Zimbabwe, leading to increased tax compliance?

Hypothesis

H0 There is no effect on the level of access to information and support services on improving tax compliance behavior among SMEs in the Green Market.

H1 There is a positive effect on the level of access to information and support services on improving tax compliance behavior among SMEs in the Green Market.

Definition of key terms

The following definitions were used contextually for this study.

Tax compliance: Upholding tax obligations by adhering to the laws and requirements established by the government and tax authorities, ensuring accurate and timely tax payments. (Abdu, E., & Adem, M. 2023).

Factors: A measurable variable that influences the outcome or result of a situation or process.

Influence: To cause someone or something to change or do something in a particular way, especially gradually or indirectly

Company: A company is an organization and legal entity set up by a group of people for the purpose of operating either a commercial or industrial business enterprise.

SME: Small and medium enterprises

BDOs: Business development organisations

LITERATURE REVIEW

Introduction

This research seeks to investigate the determinants of tax compliance among Small and Medium Enterprises: Case study of Green Market, Mutare. This chapter will focus on the identification of literature relevant to the study. The literature will be contextualised to make it relevant to the problem under study and the gap in knowledge will also be further established. This chapter is basically threefold, that is, the conceptual framework, theoretical framework and lastly empirical literature review. On conceptual framework, the key concepts of the research will be identified and explained. Theories relating to the study will be discussed under the theoretical framework and a justification will be given as to which theory underpins this study. The researcher will look at what other researchers have done in the same study area under empirical review. Discussion is done on how researches by previous researchers influence this research as well as establishing the research gap.

Literature Review

SME

SMEs play a dominant role in the national economy (Ahmed et al., 2022), but they have limited administrative capabilities. International experience shows that SMEs face disproportionate regulatory burdens (Mallett et al., 2019). In addition, Felmi. (2021) highlights that tax compliance is a major problem for many tax authorities and it is not an easy task to persuade taxpayers to comply, although “tax laws are not always precise”. The Small and medium enterprise act of Zimbabwe (24:12) defines an SME as a business that employees 6-75 permanent employees with an asset base of USD$250000 to USD$ 2 million and an annual turnover of USD $500 000 to USD $3 million (Finance Act, 2018; RBZ, 2013; ZIMRA, 2016). Business turnover is one of the most popular criteria in determining tax rules for SMEs (Inasius, 2019), as it has separate definitions for tax purposes. Estimates suggest there are over 60,000 registered SMEs in Zimbabwe. However, the actual number, including informal ones, is likely much higher. SMEs contribute significantly to Zimbabwe’s GDP, with estimates ranging from 50% to 60% (Dlamini et al., 2020; Watambwa et al., 2021; Musabayana et al., 2022). They are the largest employer, particularly for young people, providing crucial income opportunities (Walter, 2019).

Tax Compliance

Tax compliance refers to the act of adhering to tax laws and regulations set by a government or tax authority (Slemrod, 2019). The act of adhering to tax laws and regulations set by governments is a crucial element for any nation’s economic stability. However, navigating the intricacies of tax codes varies significantly across the globe (Sabry, 2024). This includes, filing tax returns accurately and on time, paying all taxes owed in full and keeping proper accounting records (Hendriks et al., 2020). Adherence to tax compliance is vital. Tax compliance is essential for governments to generate revenue for public services and infrastructure development Oyewumi et al., 2020). However, SMEs consistently exhibit higher non-compliance rates compared to larger corporations (Nartey, 2023). A stable tax system fosters economic growth and development. It increases fairness as everyone contributes their fair share to support the government. Some hurdles are associated with the issue of taxes. Tax laws can be intricate and difficult to understand, leading to errors or non-compliance (Nguyen et al., 2020). The process of filing tax returns and keeping records can be time-consuming and costly for businesses. Transactions within informal economies often go unreported.

Tax Compliance in Zimbabwe

Zimbabwe, like most countries, relies heavily on tax revenue to finance its government (Binha, 2021). However, Akaro, (2023) points out that tax compliance in Zimbabwe is a significant challenge, with estimates hovering around 30% according to official data. This section delves into the complexities of tax compliance in Zimbabwe, exploring the factors that hinder businesses, particularly Small and Medium Enterprises (SMEs), which are the backbone of the country’s GDP.

Factors contributing to non-tax compliance

Complexity of tax regulations

The Zimbabwean tax system imposes a multitude of taxes on businesses, including corporate income tax, Value Added Tax (VAT), withholding taxes, and various other levies (Sebele-Mpofu, et al., 2021; Murahwa, 2023). Keeping track of these different taxes, their rates, and filing requirements can be overwhelming, especially for smaller businesses without dedicated tax specialists. The Zimbabwean tax code is notorious for frequent amendments and changes (Sebele-Mpofu, et al., 2021). Staying updated on these changes requires constant vigilance and can be a significant burden for SMEs who may not have the resources to constantly monitor updates. Missing a crucial amendment can lead to errors in filing and potential penalties, further discouraging compliance. The wording of tax regulations can be ambiguous and open to interpretation (Demin, 2020). This ambiguity creates confusion and uncertainty for businesses unsure of how specific rules apply to their situation. The fear of misinterpreting the regulations and facing penalties can lead to non-compliance as a form of risk aversion. Tax regulations often lack clear and concise explanations, making it difficult for businesses to understand their obligations (Owens et al., 2021). Kagande et al., (2022) vows that the the absence of readily available guidance materials and the bureaucratic nature of ZIMRA (Zimbabwe Revenue Authority) can further hinder SMEs’ ability to navigate the system effectively (Dlamini, 2022; Mpofu, 2021).

Lack of awareness and knowledge

Many SMEs lack the financial resources to hire qualified accountants or tax advisors who can ensure proper bookkeeping and navigate the complexities of tax compliance (Buthelezi, 2023). This often results in errors in record-keeping and tax return filing, leading to potential penalties and hindering growth. Research by Mwangi (2018) emphasizes the knowledge gap among SME owners regarding tax obligations. Limited understanding of tax deductions, filing deadlines, and even basic tax concepts can lead to unintentional non-compliance (Ndlovu et al., 2022 Sithebe, 2022). Limited financial literacy, particularly among business owners in rural areas, can hinder their understanding of tax obligations and filing procedures (Maritim, 2020; Tadesse, 2023). Investment in financial literacy programs is essential to empower businesses to comply effectively.

Limited Access to Finance

SMEs often operate with limited cash flow and prioritise immediate financial needs for survival (Thorgren et al., 2020). Tax payments, perceived as a long-term obligation, can be deferred or neglected when day-to-day operations are at stake. This short-term focus can lead to tax arrears and potential penalties. Limited access to formal financing can also push SMEs towards informal sources of funding, such as loans from friends, family, or money lenders (Nguyen et al., 2021). These transactions are often cash-based and unrecorded, making it difficult to track income and expenses for tax purposes. The lack of a clear financial trail can hinder accurate tax filing and compliance (Mpofu et al., 2022). Non-compliance with tax obligations can further restrict access to formal finance. Banks and other financial institutions may be hesitant to lend to businesses with a history of tax delinquency (Franquesa et al., 2021). This lack of access to formal financing perpetuates the cycle of limited cash flow and discourages investment in proper accounting practices, making tax compliance even more challenging (Netshisaulu et al., 2022). Without proper financial records and a history of tax compliance, businesses may struggle to qualify for loans, hindering their formalization and growth (Peprah et al., 2020; Zylfijaj et l., 2020).

Economic Uncertainty

Economic uncertainty, characterised by factors like inflation, currency fluctuations, and political instability, casts a long shadow on tax compliance in Zimbabwe (Muchinguri, 2023; Raftopoulos et al., 2020). This instability creates a challenging environment for businesses, particularly Small and Medium Enterprises (SMEs), hindering their ability and willingness to comply with tax regulations. In an uncertain economic climate, businesses prioritize short-term survival over long-term planning. Tax compliance, perceived as a future obligation, may be sacrificed to meet immediate needs like payroll or operational costs. This short-term focus can lead to delayed tax payments and potential penalties. Economic uncertainty discourages investment and expansion plans for SMEs (Adomako et al., 2020). With limited visibility on future economic conditions, businesses are hesitant to invest in resources like proper accounting systems or tax advisors, making tax compliance more difficult (Prichard et al., 2019). Uncertainty can incentivize businesses to operate within the informal sector. The perception that the formal tax system is burdensome and complex, coupled with the lack of long-term stability, may lead SMEs to operate “off the grid” (Greenham, 2019).

High inflation and currency fluctuations can raise questions about the effectiveness of government spending financed by tax revenue. When citizens don’t see a clear link between their tax contributions and tangible improvements in public services or infrastructure, trust in the system erodes, leading to lower tax morale and reduced compliance (Taddesse, 2023). Frequent changes in tax regulations or policies in response to economic instability can create confusion and distrust among businesses. This unpredictability discourages compliance as businesses become hesitant to invest in formalization or long-term tax planning (Agbleze, 2022).

Tax administration hurdles

Mpofu (2023) points out that perceptions of inefficiency and bureaucracy within the Zimbabwe Revenue Authority (ZIMRA) can act as a major deterrent. He further highlights that long waiting times, unclear procedures, and a lack of readily available information contribute to frustration and a sense that tax compliance is an arduous task. Long processing times for tax refunds, cumbersome filing procedures, and limited access to support services can discourage timely filing and payment of taxes (Moore, 2020). The perception of corruption within the tax administration system can also be a major deterrent to compliance (Isaiah, 2022). Businesses may be hesitant to pay taxes if they believe a portion will be misappropriated. This undermines trust in the system and incentivizes non-compliance.

Access to information and support on tax compliance for SMEs by BDOs in Zimbabwe Business Development Organizations (BDOs) play a crucial role in supporting Small and Medium Enterprises (SMEs) in Zimbabwe with tax compliance. Andrean et al (2022) defined business development organisations as a form of business development services that improves the tax compliance of SMEs taxpayers. The Director General of Taxes uses this program to encourage tax compliance by integrating it with tax socialization. This program then provides various event platforms that increase tax knowledge and perceptions of tax justice. However, the level of access to information and support services can vary depending on several factors. Zimbabwe has a network of BDOs, some national and others regional. The range of services offered by these organizations can differ. Not all BDOs may prioritize or specialize in tax compliance support. The effectiveness of BDOs is often dependent on their financial resources. Some BDOs may offer limited free services or require membership fees, which can be a barrier for resource-constrained SMEs. Andrean et al (2022) further highlighted that many BDOs offer basic workshops or seminars on tax compliance. These sessions can provide general information on tax obligations, filing procedures, and deadlines. BDOs may not have the resources to offer in-depth tax advice or personalized assistance with complex tax situations. SMEs requiring specific guidance on tax calculations, deductions, or audits may need to seek help from qualified tax accountants. The core focus of many BDOs might be broader business development areas like marketing, finance management, or access to funding. Tax compliance may be a secondary service offered as part of a larger package. ZIMRA provides information and resources on its website and through its offices. However, navigating these resources can be challenging for SMEs with limited knowledge of tax terminology. Hiring qualified tax accountants is an option for SMEs requiring in-depth tax advice and support. However, this option can be expensive and out of reach for many SMEs.

ZIMRA tax compliance strategies for SMEs in Zimbabwe

The Zimbabwe Revenue Authority (ZIMRA) can implement various strategies to address the knowledge gaps, administrative burdens, and trust perceptions hindering tax compliance among SMEs.

Addressing Knowledge Gaps

Recognizing the knowledge gap faced by SMEs, ZIMRA can create a multi-pronged approach to information provision (Mwamba et al., 2022). This would include developing clear and concise tax guides and brochures specifically designed for SMEs, translated into local languages for wider accessibility. Trilar et al. (2021) mentioned that an online tax education portal would be established, offering interactive modules, FAQs, and explainer videos accessible on mobile devices. Estifanos, (2022) further elaborated that in collaboration with BDOs, regular capacity building workshops would provide practical guidance on filing procedures, record-keeping, and understanding tax obligations. Additionally, a dedicated tax hotline and online chat support system staffed by knowledgeable personnel would be available to answer basic tax questions and offer further assistance to SMEs. This comprehensive approach would empower SMEs with the knowledge and resources they need to navigate the tax system effectively.

Reducing Administrative Burdens

To streamline the administrative burden for SMEs, ZIMRA can implement a simplified tax regime with flat tax rates, fewer filing requirements, and a more streamlined process which would significantly reduce the complexity for SMEs (Musyoka et al., 2021). Secondly, investing in a user-friendly online tax filing system would allow for electronic filing and payments, eliminating the need for frequent visits to ZIMRA offices. To further ease the process, ZIMRA could consider pre-filling tax forms with basic information already available, such as income from registered businesses (Kinuu, 2023). . This would save SMEs valuable time and effort. Finally, offering extended payment deadlines, especially during economic hardships, would alleviate cash flow constraints and incentivize timely compliance among SMEs. These combined measures would make tax administration less burdensome and encourage SMEs to participate more effectively in the tax system (Kinuu, 2023;

Building Trust and Transparency

To build trust and encourage a culture of compliance, ZIMRA can improve communication with SMEs by providing clear and consistent information on tax policies, regulation changes, and available support services (Mpofu, 2023). It can also launch public awareness campaigns which would highlight the importance of tax compliance and how this revenue translates into tangible benefits for society through funding public services and infrastructure development. There is need for enhancing transparency in tax administration which involves establishing clear and fair grievance redressal mechanisms for SMEs (De, 2023). This allows them to address any concerns regarding tax assessments or audits (Mpofu, (2023), further points out that Zimra can also implement recognition programs that acknowledge and rewards SMEs with a consistent record of compliance. This positive reinforcement incentivizes good tax practices and fosters a culture of responsible tax citizenship among SMEs.

To further empower SMEs and encourage tax compliance, ZIMRA can strengthen its collaboration with BDOs. By leveraging the BDOs’ expertise and established reach, ZIMRA can disseminate tax information and support services more effectively to SMEs. Additionally, exploring the possibility of offering tax incentives, such as tax breaks or credits, to SMEs with a consistent track record of compliance, would provide a further nudge towards good tax practices. This collaborative approach, coupled with targeted incentives, can significantly improve tax compliance among SMEs.

Conceptual Framework

This framework outlines the key factors that influence tax compliance behavior among Small and Medium Enterprises (SMEs). It integrates elements from the Rational Choice Theory, Deterrence Theory, and Social Capital Theory to provide a holistic understanding. See Figure 2.2 below:

Figure 2.1 Conceptual Framework

Source: Researcher’s design (2024)

Dependent Variable: Tax compliance level (The willingness and ability of SMEs to fulfill their tax obligations accurately and on time.

Independent Variables:

- Economic Factors:

- Cost of Compliance: Complexity of tax regulations, filing procedures, and professional fees associated with tax preparation.

- Tax Burden: Perceived fairness and level of taxes levied on SMEs compared to potential benefits.

- Economic Conditions: Inflation, currency fluctuations, and overall economic stability can impact cash flow and willingness to comply.

- Institutional Factors:

- Tax Administration Efficiency: Transparency, ease of filing, and responsiveness of tax authorities (ZIMRA)

- Enforcement Mechanisms: Effectiveness of detection and penalty systems for non-compliance.

- Government Legitimacy: Perceived fairness and trustworthiness of the government in using tax revenue.

- Social Factors:

- Social Norms & Attitudes: Community perception of tax compliance and prevalence of the informal economy.

- Social Networks & Trust: Availability of information and support from BDOs, peers, and other trusted sources.

- Collective Action: Strength of SME associations and their ability to advocate for a fairer tax system.

Moderating Variables:

- Firm Characteristics: Size, industry, age, and ownership structure of the SME can influence its capacity and willingness to comply.

- Managerial Characteristics: Financial literacy, risk tolerance, and ethical values of SME owners/managers can impact compliance decisions.

Dependent Variable:

- Tax Compliance Level: The degree to which SMEs fulfill their tax obligations accurately and on time. This can be measured by factors such as timely filing of tax returns, accurate reporting of income, and payment of taxes due.

Relationships:

- Economic Factors: High costs of compliance, a perceived high tax burden, and economic instability can all discourage tax compliance among SMEs.

- Institutional Factors: A complex tax system, inefficient administration, weak enforcement, and a lack of government legitimacy can reduce SME trust in the system and lead to non-compliance.

- Social Factors: Strong social norms of tax compliance, access to reliable information and support networks, and the ability for collective action can encourage SMEs to comply with their tax obligations.

- Moderating Variables: Firm and managerial characteristics can influence how SMEs respond to the independent variables. For example, a larger, more established SME may be better equipped to handle complex tax regulations than a smaller, newer business.

The framework in Figure 2.1 above emphasizes the interconnectedness of these factors. Economic factors can influence social norms, while institutional factors can shape the effectiveness of social capital. Understanding these relationships is crucial for developing effective strategies to promote tax compliance among SMEs in Zimbabwe.

Theoretical Framework

Understanding the factors influencing tax compliance among SMEs at Green Market requires examining the issue through the lens of three theoretical frameworks. These are the rational choice theory, the deterrence theory and the social capital theory.

From a rational choice perspective, SMEs will comply with tax obligations if the perceived benefits outweigh the perceived costs (Barus et al., 2022). Highlighting the benefits can be crucial. For example, information campaigns could emphasize how tax compliance allows access to government contracts, loans, and reduces the risk of audits and penalties. Simplifying tax regulations, streamlining the filing process, and providing affordable tax preparation services can significantly reduce the costs associated with compliance for SMEs (Dlamini & Dube, 2020). This improves the overall cost-benefit equation and incentivizes compliance. The deterrence theory emphasizes the role of penalties in discouraging non-compliance (Koranteng et al., 2020). ZIMRA strengthening its detection and penalty enforcement mechanisms can increase the perceived costs of non-compliance for SMEs (ZIMRA, 2023). This, coupled with clear communication of penalties, strengthens the deterrent effect. Implementing a system of graduated penalties, with stricter measures for repeat offenders, can further deter non-compliance (EY, 2023). However, these penalties should be seen as a last resort, with a focus on education and support for first-time offenders. Building a network of support for SMEs through BDOs and fostering a sense of community among compliant businesses can be beneficial (Sebele-Mpofu, 2021). Social capital theory underscores the role of trust in encouraging tax compliance. ZIMRA needs to build trust with SMEs by promoting transparency in tax administration, addressing corruption concerns, and demonstrating how tax revenue is used for public services (Cox, 2024). This fosters a sense of shared responsibility. BDOs and other stakeholders can create networks for SMEs to share experiences, access information, and learn best practices regarding tax compliance. This nurture a sense of community and provides role models for compliant behavior. Social capital can also be leveraged to encourage collective action among SMEs to advocate for a fairer and more efficient tax system (OECD, 2023). This can increase their confidence in the system and incentivize compliance.

Integration of these three theories would aid in understanding tax compliance among SMEs at Green Market. Thus, effective enforcement (deterrence) can enhance the perceived benefits of compliance (rational choice) (Kim, 2023). Building trust (social capital) can lead to more efficient enforcement (deterrence). By integrating these frameworks, clients can gain a deeper understanding of the factors influencing SME tax compliance decisions. This knowledge can then be used to create targeted interventions that address both the economic and social drivers of non-compliance. Ultimately, a combination of rational incentives, effective deterrence, and a strong sense of social responsibility can lead to a more compliant and prosperous SME sector in Zimbabwe.

Empirical Framework

Abdu, & Adem (2023) carried out a review-based research tax compliance behaviour of taxpayers in Ethiopia in order to identify determinants and challenges of tax compliance behaviour of taxpayers. The review revealed that the major challenges are the complexity of the tax system, inefficiency of tax authorities, lack of tax knowledge and awareness, negative perception of taxpayers, a negative act of tax assessors, absence of tax training, lack of transparency of tax system, arbitrary estimation of taxes, personal financial constraints, political instability and lack of timely tax audit. The present study is necessary in the sense that the previous research was a desktop research and there was no triangulation. The research to be carried out will use a mixed method approach for the triangulation of the results which would result in the generalizability of the findings.

A research carried out by Fauziati,et al. (2020) in Kota Padang, Indonesia is also worth mentioning in relation to the present study. The aim of the paper was to examine the impact of tax knowledge on tax compliance. The survey research design was used in conducting the investigation. The primary source of data used were 300 self- administered questionnaire which were distributed. The simple linier regression models were used to estimate the relationship between tax knowledge and tax compliance. The t-statistics was used to test the significance of the study variables. It was revealed that; tax knowledge has no impact on tax compliance. The previous study determined the relationship between tax knowledge and tax compliance and the current study is going to establish further the extent which tax compliance vary with a number of variables, thus, economic factors, institutional factors and social factors in line with SMEs at Green Market. Furthermore, the present study used questionnaires with a Likert-type scale just like the previous study. However, the previous study did not consider other variables and the sample size of the previous study is double the sample size of the current study. Indonesia is developed country while Zimbabwe is a developing country hence, it not easy for transferability of findings because the two studies are carried in different environment with different participants. Therefore, the present study is necessary for the generalisability and transferability of findings to the phenomena under study.

Sebele-Mpofu et al., (2020) carried out a research on governance quality, tax morale and compliance in Zimbabwe’s informal sector. The study explored social networking technologies being used in higher education, their uses, extent of use, benefits and skills learners acquire from use of these technologies. The study adopted the interpretivism research philosophy and interviews and document reviews were used as the main research tools. Findings of the study suggested that tax morale was found in literature to shape tax compliance behaviour and to be significantly correlated with strategies of tax effort across countries. In addition views regarding the quality of institutions, the cost-benefit analysis on the use of tax revenues and the quality of governance influence tax morale thus in turn affecting tax compliance. The research by Sebele-Mpofu et al., (2020) employed a qualitative research design in that only interviews were used to collect data from participants while the current research will use both questionnaires and interviews to collect data enabling triangulation. Although both researches are carried in Zimbabwe, the findings cannot be easily generalised since the two researches are carried in different context and environment, hence a need to carry out the present study so authority can be stamped on the transferability and generalizability of the findings.

Summary

This chapter integrated various literature previously researched problems and considered the views and findings of early researchers from which the research gaps were recognised to justify why the researcher decided to research on similar matters. The chapter used objectives in the first chapter as a guideline to review early researches related to the study. The next chapter is set to specify the research methodology used by the study.

RESEARCH METHODOLOGY

Introduction

The previous chapter discussed about literature review. It focused mainly on other related literature for the study where conceptual, theoretical and empirical studies were discussed. However, this chapter is going to focus on research methodology which outlines on how the research will be conducted. In a nutshell, the research will be conducted using the research onion as developed by Saunders et al (2016). Issues discussed are research philosophy, research approach, research choice, research strategy, time horizon, research population, sample and sampling procedures, data collection sources, research instruments, data collection presentation and analysis, data reliability and validity, ethical considerations and the summary.

Research Design

A research design is a master plan specifying the methods and procedures for collecting and analysing the needed information (Zikmund, 1996). Higson (2015)) also defined research design as, “a process of creating an empirical test to support or refute a knowledge claim.” Therefore, the research design provides a blue print for reacting to the objectives of the research hence gives a framework for the research plan of action. (Smith, 1996).

Qualitative Approach

Qualitative approach is defined as research or study which generates results and conclusions with the help of qualitative analyses and, mainly, with qualitative data (Lundahl & Skärvad, 1999). The purpose of this method is to describe, analyse and understand the behaviour or impact of a certain phenomenon, often by using hermeneutic science (interpret and analyse) so a new theory or understanding may be outlined (Repstad, 1999; Lundahl & Skärvad, 1999). Mark’s (1996) definition has almost the same significance since he states that the qualitative approach studies phenomena using general descriptions to describe or explain them. Also, narrative descriptions of persons, events and relationships tend to be used by researchers who use the qualitative approach. The approach consists of descriptions, quotes, observations and excerpts from books and other documents (Quinn, 2002:308).

Quantitative Approach

The quantitative method involves some kind of measurement which should be reliable and valid (Lundahl & Skärvad, 1999). Mark (1996) defines the quantitative method as the approach which studies phenomena using numerical means. In this approach there is an emphasis on counting, describing and using standard statistics, such as means and standard deviations. A quantitative method is more suitable for highly structured research that may be statistically measured (Wigblad, 1997:31). According to Bryman and Burgess (1999), there is a tendency for quantitative researchers to reach generalised findings while contextual understanding outlines the basis for qualitative research. The quantitative approach to a research study involves the use of statistical data analyses to obtain information about the study simply because the approach is based on measuring quantity or amount (Harvey, 2006).

Barker, Pistrang & Elliot (2002) indicated that quantitative approaches use numbers that ensure precision in measurement resulting in data being objective and impartial. The collected data can easily be summarized, promoting effective communication of the findings as well as making comparisons where necessary. This approach enabled the researcher to collect data from a large sample. McMillan and Schumacher (1993, p.41) noted that quantitative approach is used with ‘experimental, descriptive and co-relational designs as a way to summarizes large number of observations.’

Mixed Research methods

Accordingly, mixed methods research is the class of research where the researcher mixes or combines quantitative and qualitative research techniques, methods, approaches, and concepts or language into a single study or set of related studies. Johnson and Onwuegbuzie (2004) stated that mixed methods research can be visualized on a continuum with qualitative research anchored at one pole and quantitative research anchored at the other, mixed methods research covers the large set of points in the middle area. Therefore, mixed methods research sits in a new third chair, with qualitative research sitting on the left side and quantitative research sitting on the right side (Imenda, 2014). Johnson, (2007) noted that the integration of both quantitative and qualitative research paradigms gives birth to a third research paradigm called mixed methods research. Johnson, Onwuegbuzie & Turner (2007) defined mixed methods research as an intellectual and practical synthesis based on qualitative and quantitative research. Mixed methods is now a dominant research paradigms having a much greater potential for explaining reality more fully than is possible when only one research paradigm is used (Imenda, 2014). It recognizes the importance of traditional quantitative and qualitative research but also offers a powerful third paradigm choice that often will provide the most informative, complete, balanced, and useful research results. In light of the above views by Johnson & Bartleson (2001) see it as reasonable to lay some emphasis on the “mixed methods” (blended) research paradigm which Johnson et al (2007) defined as an approach to knowledge (theory and practice) that attempts to consider multiple viewpoints, perspectives, positions, and standpoints (always including the standpoints of qualitative and quantitative research).

In this research, the mixed research approach is going to be used. A combination of quantitative and qualitative methods will be used for this study. This approach will enable the researcher to collect data from a large sample which comprises SMEs and BDOs. Thus, both quantitative and qualitative approach will give the researcher the opportunity to capture measurable evidence, which will assist in establishing factors affecting non-tax compliance in order to establish the possibility of generalising the findings to a large population. The benefit of such an approach lies in the fact that rarely can numbers alone provide full and authentic information, neither words on their own. Quantitative and qualitative approach will facilitate the integration of selected dataset (semi-structured questionnaire) and then the information obtained will be used to inform the subsequent data collection (personal interview) and it will enable comparison of the findings from different sources. Ultimately it will enable comparison of the findings from different sources and provided insight into a breadth of experiences.

During the study qualitative approach will be employed to bring about the respondents’ views on their attitude towards tax compliance. The quantitative approach will provide the researcher with the opportunity to capture measurable evidence, which will assist in analyzing the responses thereby establishing the possibility of generalising the findings to a population of the study. Metaphorically speaking, if the quantitative data is the skeleton, then the qualitative data provides the flesh. Therefore, for this study, mixed method approach will be considered in data collection, analysis and interpretation.

The study on the determinants of tax compliance among Small and Medium Enterprises is descriptive in nature. Therefore, the researcher sees it necessary and being prudent to adopt descriptive survey as a research strategy. According to Chiromo (2006), a descriptive survey can help the researcher to see over and beyond what a naked eye can see. Surveys usually relate to the present state of affairs and involve an attempt to provide a snapshot of how things are at the specific time at which data is collected. Neumann cited in Kriel (2007:14), highlighted the aim of descriptive survey as a phenomenon that “present a picture of the specific details of a situation, social setting, or relationship.” The descriptive survey method gathers information about the present existing condition. This will be done by asking “what,” “who” and “how’ questions.

The descriptive survey will then be appropriate for the research study as it allow the identification of similarities and differences of the respondents’ answers from different levels. For the study, two types of data will be gathered. These will include data derived from the answers given by the respondents in the self-administered questionnaire and the interviews. The descriptive survey method is advantageous for the researcher due to its flexibility; this method can use either qualitative or quantitative data or both, giving the researcher greater options in selecting the instruments for data gathering (Saunders, Lewis &Thornhill, 2003).

To ensure validity of the study, the researcher is directly involved in the data collection with questionnaires as well as the collection of information through face-to-face interviews with the selected respondents through interviews. It will give the study an in-depth view of the research problem. In this way, the study will be viewed at from both the qualitative and quantitative dimensions. The benefit of such an approach lies in the facts that rarely can numbers alone provide full and authentic information, neither words on their own. Therefore, the aim of the survey is to obtain information, which can be analysed, patterns extracted, and comparisons made.

According to Oppenheim (1986) the descriptive survey method describes and interprets activities, the relationships that exist and trends that are developed after gathering information from the sample. The suitability of this study is buttressed by Macmillan (1996) who adds that the descriptive survey approach is an effective method of collecting original data for determining attitudes, orientation and conditions prevalent in a given situation. The researcher will use this kind of research design to obtain first hand data from the respondents so as to formulate rational and sound conclusions and recommendations for the study. Therefore, the descriptive survey is deemed the best strategy in order to fulfil the research objectives. In this regard, the researcher therefore focused on Green Market Mutare using this design on intensive investigation into the impact and effectiveness of strategies to be implemented by ZIMRA so as to promote compliance.

Research Instruments

The researcher used questionnaires in collecting data for the research.

Questionnaires

The researcher used open closed ended questionnaires for this research. These were used to ensure that respondents chose between the options that were provided to them. The options on the questionnaire were filled in using a Likert scale. Likert scale was chosen because it is specific in that it provides respondents with a range of text-based answers that lie along a scale (Elliot 2021). Elliot further asserts that it provides more granular information on people’s attitudes towards a subject than a simple yes/no question type hence researchers can assess varying levels of agreement, importance, quality and other factors. The Likert scale was designed with different scales with numbers from number one to number five with the following options: Strongly agree, strongly disagree, Neutral, Agree and Disagree as reflected on the table below:

Table 3.1 Likert scale

| Strongly Agree | Disagree | Neutral | Agree | Strongly Agree |

| 1 | 2 | 3 | 4 | 5 |

Source: Elliot (2021)

The questionnaire was chosen because most respondents are familiar with it hence is not difficult to fill in the information required by the researcher. Debois (2019) supported the use of questionnaires in that apart from being inexpensive, questionnaires are also a practical way to gather data. Questionnaires are relatively low cost and practical for a large sample. The other benefit of questionnaire was that the data they gather can be processed and analysed relatively easily compared to spoken data which has to be recorded and transcribed before analysis. Also, the questionnaire does not need much time to analysed as the researcher did not have much time to use other research instruments which may require much time to analyse. It was also cheap to administer. The questionnaires were sent via email by the researcher to the research subjects who were given one day to fill them. The researcher did not employ a research assistant to help administer research instruments on data collection.

Interviews

The interview technique will be used to encourage SMEs to express a wide range of significant reactions, to facilitate better understanding of the topic under-study, to check and validate trends identified by the questionnaires and to enable comparisons.

Personal Interview

The assumption that the respondents also possess particular experience, on which elaboration will be sought, is based on background information. The situation will be analysed before the interview and the researcher sought additional information. The interview guide specifies the topics on which information is sought. The interviewer will be free to probe and ask to follow up questions.

Each one of the selected SME and BDO will be interviewed individually by the researcher for thirty to forty minutes. The answers will be open-ended, and there is more emphasis on the interviewee elaborating points of interest. With semi-structured interviews, the interviewer will have a clear list of issues to be addressed and questions to be answered. As well as in semi-structured interview the interviewer is prepared to be flexible in terms of the order in which the topics are considered, and, perhaps more significantly, to let the interviewee develop ideas and speak more widely on the issues that will be raised by the researcher. The strength of using the face-to-face interview when seeking in-depth information on the interviewee’s feeling, experiences, impressions and perceptions lies in its flexibility and adaptability (Babbie, 1992). In the study the discussion progressed at partnership level; the researcher will seek clarification through probing and non-verbal cues such as facial expressions, gestures and hesitation. This will give the researcher an opportunity of reconciling the words and non-verbal cues to get insights into the real feelings and attitudes of the respondents.

The interview will allow the interviewees to express themselves at some length, but the researcher will have sufficient structure to prevent aimless mumbling. In open-ended questions, the interviewer is able to probe further, giving the interviewees a chance to qualify their responses (Dhliwayo & Keogh, 2002). This will result in the discovery of information, which the researcher may not be aware of at the beginning of the study. Thus, it will allow the clearance of any misunderstandings, misconceptions of words or questions and to clarify the respondents’ responses.

The interview situation will allow the appraisal of validity of the responses as the interviewer had access to not only what respondents will say, but also how they will say it. The non-verbal behaviour within an interview is an important aspect to note. Since at times the respondents cannot simply and fluently write their responses to questions about complex and emotionally charged topics, an interview is the more appropriate technique for probing in such situations. Open-ended questions which, permitted free responses from an individual, will be employed. They are often used when an interviewer is interested in people’s views, opinions, perceptions, beliefs and motivation and in this study about the factors influencing non tax compliance of SMEs at Green Market. During the interview there will be note taking through careful and deliberate attention. Babbie (1992: 217) suggests that:

Do not trust your memory any more than you have to: It is untrustworthy. Even if you pride yourself on having a photographic memory, it is a good idea to take notes during the interview or as soon, afterwards, as possible.

The responses given during the interviews will be recorded by means of both field notes and tape recording. The interviews will then be transcribed, coded and analysed. Thus, the interviews will provide the researcher with the means of discovering factors influencing non-tax compliance of SMEs.

Research population and Sample

Population

Hair et al (2003), define population as an identified total group or elements. Churchill (1997) defines population as the totality of cases that conform to some designated specifications. The specifications define the elements of the target group and those that are to be excluded. An ideal population is all SMEs in Zimbabwe. Because of insufficient resources and time to conduct such a large-scale study, such a generalization may not be justifiable. One that might be justifiable and feasible would be a population of all SMEs at Mutare Green Market. However, it will not be possible to collect information from this whole population, because of huge costs involved, time constraints on the part of the researcher, who is fully employed and the impracticability of reaching out to every informant. To bring about valid results in a descriptive survey, the sample must be representative of all the characteristics, which make up the population. According to Babbie (1992) representativeness is, therefore, the quality of a sample of having the same distribution of characteristics as the population from which it is selected. Once a population is carefully defined, a representative sample can be drawn from it. In this study, a population of one thousand and one (1001) representing all SMEs at Green Market was used. This information was obtained from Mutare City Council as of June 2024. From this population the research targeted persons in the welding, timber production and shops as the target population. These departments had a total 450 employees and this is where the sample was drawn from.

Sample and Sampling Procedure

Fowler (1988) defines a sample as part of a population, which is actually observed and is selected in such a way that avoids presenting a biased view of the population. A sampling frame should ideally contain a complete, up-to-date list of all those that comprise the population for research. As far as surveys of participants are concerned, various registers are the most usual basis for the sampling frame. The researcher can select the required sample size purely at random, or do it more systematically.

In order to generalize from the findings of a survey, the sample must not only be carefully selected to be representative of the population: it also needs to include a sufficient number. Thus, the sample needs to be of an adequate size. Of the total population of four hundred and fifty SMES, 90 SMEs were selected to make up a sample that constituted twenty percent (20%) of the target student population. Chikoko and Mhloyi (1995) say, “In descriptive survey research a sample of 10 – 20 percent is often used.” Macmillan (1996) supports Chikoko, et al (1995) by asserting that in social science and educational research it is impractical and unnecessary to measure all elements in a population of interest. Some elements of the population cannot be studied directly because of lack of accessibility, limited time and prohibitive costs.

In selecting the sample for the study, stratified random sampling procedure was employed. A stratified sample can be defined as one in which every member of the population has an equal chance of being selected in relation to their proportion within the total population (Explorable.com, 2009). In the first instance, then, stratified sampling continues to adhere to the underlying principle of randomness. However, it adds some boundaries to the process of selection and applies the principle of randomness within these boundaries. It is something of a mixture of random selection and selecting on the basis of specific identity or purpose. Random sampling is used when the population is split into distinguishable layers or strata that are quite different from each other and which together cover the whole population. Separate random samples will be taken from each stratum and put together to form the sample from the population. Fairfax County Department of Systems Management for Human Services (2003) noted that stratified sampling procedure can provide more precise estimates if the population being surveyed is more heterogeneous than the categorized groups, can enable the researcher to determine desired levels of sampling precision for each group and can provide administrative efficiency. Although this study is from a SMEs’ perspective, BDOs are not part of the study, but will also be included purposively to enable triangulation of the information solicited from SMEs through the use of different data collection instruments.

Data collection procedures

In collecting the required data the researcher will hand deliver questionnaires to SMEs at Green Market and to selected BDOs. Whilst distributing questionnaires, the researcher will also make an appointment for interviews. Not all SMEs and BDOs will be interviewed due to lack of adequate time. During the interview the researcher will put in writing what the respondent will say on the interview form designed by the researcher. After conducting a couple of interviews the researcher will move around the Green Market collecting completed questionnaires. The researcher will also download completed mailed questionnaires. Soon after collection of completed questionnaires the researcher will then submerge herself into the data, so that she understands it before analysis.

Primary data

According to Cateora (2002:68), primary data is, “data that is extracted from the field of study in its raw state.” He also states that, primary data is data obtained from the field by the researcher or primary methods are those that collect data for the first time, for a specific purpose. For the purpose of collecting primary data, the researcher will make use of a questionnaire and interview guide as data collection tools.

Secondary data

According to Bryman and Bell (2007), secondary data collection methods refer to the ability of the researcher to carry out an analysis of the data that has already been prepared by other researchers. Secondary data includes documents, data, and information from previous studies that a researcher might use in a new study (Oates, 2006). Secondary data in this study included documents, data and information from previous studies such as existing official reports and journals, other empirical researches in the area and any other relevant document from the libraries and internet. Data downloads and computer printouts available provided further information for authenticating the responses and providing collaborative information on the research problem. For triangulation purposes, this study will employ both primary and secondary data collection methods in order to make the analysis. Hence, questionnaire and interview guide will be used in the study to gather primary data while sources which included policy documents, data and information from previous studies such as existing official reports and journals, other empirical researches in the area and any other relevant document from the libraries and internet will be used to gather secondary data.

Plan for data analysis

Statistical Product and Service Solutions (SPSS) and Microsoft Excel will be used for data analysis in this study. Results will be presented first in their simplest form through tables and then through the use of simple narrative descriptions, simple counts of frequency, and descriptive statistics. SPSS 21.0, a statistical analysis software package will be used to conduct an analysis of the relationship between the level of access to information and support services provided by Business Development Organizations (BDOs) and the tax compliance behaviour of SMEs at Green Market through the use of closed-ended survey questions.

Ethical Considerations

The researcher will collect a supporting letter from the Department of Applied Accounting at Manicaland State University of Applied Sciences. As a way of securing the free and informed consent of the selected respondents, the researcher will relay to all the importance details of the study, including its aim and purpose. By explaining these important details, the respondents will be able to understand the importance of their role in the research study. The confidentiality and anonymity of the respondents is granted by not disclosing their names or personal information in the study. Only relevant details that help in answering the research questions will be included. The research subjects will not be coerced into participating in the study but should be done voluntary. Data collected will only be used for research purposes. The principle of anonymity will be strongly adhered to, to protect the identity of research subjects. Completed questionnaires by the respondents will be collected by the researcher and some respondents will mail their response where necessary as a way of ensuring a one hundred percent (100%) return of the questionnaires. Lastly, the researcher will make sure that when reporting the results, accuracy is a must to represent what has been read or what respondents have narrated. The researcher will make an effort not to take questionnaire responses out of context and not to discuss small parts of observations without putting them into the appropriate context.

DATA PRESENTATION, ANALYSIS AND DISCUSION

Introduction

The previous chapter discussed about the research methodology. It outlined the steps, procedures, processes and methods on how the research was conducted. This chapter is aimed to present and discuss the findings of the study, whose topic was to unleash “Determinants of non-tax compliance among Small and Medium Enterprises: Case study of Green Market, Mutare”. The research was guided by research objectives that enabled the researcher to unpack the topic under study. The research objectives are as follows:

Objectives of the study

- To establish the extent to which formal and informal institutional factors, alongside business owner characteristics and firm-specific attributes, contribute to non-tax compliance among SMEs at Green market downtown, Mutare.

- To determine if the level of access to information and support services provided by business development organizations (BDOs) correlate with improved tax compliance behavior among SMEs in the green market

- To craft ways in which ZIMRA can tailor its tax compliance strategies so as to effectively address the knowledge gaps, administrative burdens, and trust perceptions of SMEs in Zimbabwe, leading to increased tax compliance

Presentation of Findings

Quantitative data gathered was first presented either in a table form, graph or pie-chart and qualitative data was presented descriptively according to emerging themes.

Questionnaire response rate

The response rate was very high (100%). All the distributed questionnaires were completed and returned. This is obviously excellent by any standards. The 100% response rate could have been attributed to the artfulness of the researcher in collecting data. The follow-ups were effectively executed leading to all the target respondents filling up and returning all the questionnaires. The other reason of the high response rate could be attributed to the fact that the sample size was small but big enough to provide the required information.

Interview response rate

The interview attendance rate was very high (100%) though the researcher had to reschedule some of the interview dates and time to accommodate for some of the SMEs and BDOs officers since they operate under tight schedules. All the intended interviews were conducted as previously planned. The 100% interview response rate could have been attributed to the prowess of the researcher in organising and collecting data.

Demographic Data

Age of respondents

Table 4.1 Age of respondents

| Field | Frequency | Percentage |

| 16 to 25 years | 10 | 11 |

| 26 to 35 years | 18 | 20 |

| 36 to 45 years | 37 | 41 |

| 46 and above | 25 | 28 |

| Total | 90 | 100 |

Source: Primary data (2024)

From the responses given, 11% (10) of the respondents are between the age 16 to 25 years, 20% (18) are between the ages 26 to 35 years, 41% (37) are 36 to 45 years and 28% are above 46 years. From the above statistics it shows that the most of the entrepreneurs are mature and have developed deep-rooted connections within the business community (Imo, 2024), both locally and internationally and trusted relationships and have the ability to build trust and credibility among their peers and clients, which can enhance business opportunities and reputation. Sievinen et al., (2020) vows that basing on past experiences, mature entrepreneurs can make informed and strategic decisions, towards long-term success. Their experience allows them to create comprehensive financial plans, and deep understanding of their industry, including market trends, customer needs, and competitor dynamics (Cosenz and Noto, 2018). This would enhance SME’s competitiveness, resilience, and long-term sustainability.

Sex of respondents

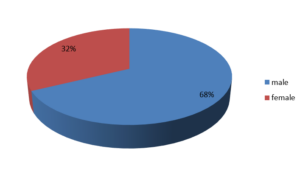

Figure 4.1 Sex of respondents

Source: Primary data (2024)

From the above figure 68% (61) of the employees are male while 32% (29) are female. Zimbabwean society has historically adhered to traditional gender roles, with men often associated with physical labour and women with domestic tasks. This cultural expectation has influenced career choices, with men more likely to pursue trades like timber production and welding. It has also been noted that the patriarchal nature of Zimbabwean society has often limited opportunities for women in traditionally male-dominated fields (Jeche, (2024). This has hindered their entry into entrepreneurship in these sectors. Issues like gender stereotyping discourage women from pursuing careers in traditionally male-dominated fields (Dunlap and Barth, 2019), leading to fewer women enrolling in relevant educational programs. Timber production, welding and shops are hostile work environments, which may expose women to sexual harassment, discrimination, and limited opportunities for advancement. This can deter women from entering or remaining in these fields. The explanation above can be further elaborated by cross tabulation on gender against area of specialisation below:

Table 4.2 Cross tabulation between gender and area of specialization

| Gender * Area of Specialization Cross tabulation | |||||

| Count | |||||

| Area of Specialization | Total | ||||

| Shops | Timber | Welding | |||

| Gender | male | 7 | 22 | 32 | 61 |

| female | 14 | 15 | 0 | 29 | |

| Total | 21 | 37 | 32 | 90 | |

SPSS output

Source: Primary data (2024)

Table 4.2 shows that we have more males in timber and welding trades, whereas more females are dominating in lighter and soft trades like running a shop and selling timber.

Educational Qualifications

Table 4.3 educational Qualifications

| Educational Qualifications | |||||

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | O Level | 27 | 30.0 | 30.0 | 30.0 |

| Diploma | 39 | 43.3 | 43.3 | 73.3 | |

| Degree | 20 | 22.2 | 22.2 | 95.6 | |

| None | 4 | 4.4 | 4.4 | 100.0 | |

| Total | 90 | 100.0 | 100.0 | ||

SPSS output

Source: Primary data (2024)

Table 4.3 above shows the response rate by educational qualifications. Thirty percent (30%) of the respondents are O level holders, while forty three percent (43.3%) holds a diploma, twenty-two percent holds a degree and four percent (4%) do not possess any qualification. Generally, SME owners at Green Market have above the minimal level of education. This would enable them to have eenhanced decision-making and problem-solving skills, improved financial management, enhanced marketing and sales strategies and improved operational efficiency. Education is a critical driver of SME growth and development (Lomatey et al., 2020; Marecha, 2020). This would enable entrepreneurs with the tools to analyse market trends, identify opportunities, and develop innovative solutions to challenges. The researcher however, further analysed their understanding of tax compliance in relation to their education. The results are shown on table 4.4 below:

Table 4.4 Cross tabulation between education and knowledge of tax compliance

| Qualifications * Knowledge of Tax Compliance Crosstabulation | |||||||

| Count | |||||||

| Knowledge of Tax Compliance | Total | ||||||

| strongly disagree | disagree | neutral | agree | strongly agree | |||

| Qualifications | O Level | 1 | 4 | 5 | 10 | 7 | 27 |

| Diploma | 3 | 2 | 9 | 14 | 11 | 39 | |

| Degree | 0 | 0 | 5 | 6 | 9 | 20 | |

| None | 2 | 0 | 2 | 0 | 0 | 4 | |

| Total | 6 | 6 | 21 | 30 | 27 | 90 | |

SPSS output

Source: Primary data (2024)

Cross tabulation was done to measure the link between level of education and knowledge of tax compliance by SMEs. One respondent with Ordinary level strongly disagreed to have knowledge of tax compliance, four disagreed, five were neutral, ten agreed to have knowledge about tax compliance while seven of the respondents strongly agreed to the notion. Five respondents with a diploma qualification did not have knowledge of tax compliance, nine were neutral, fourteen agreed and eleven strongly agreed to know tax compliance. Five respondents with degrees were neutral about knowledge of tax compliance, while six agreed and nine strongly agreed that they know the importance of tax compliance. This shows that the research subjects are generally educated and understand the issue of tax compliance. However, a substantial number of twenty one proved to be neutral on this matter. This could be due to ambivalence or fear of judgement on the subject matter. Although Lomatey et al., (2020) and Marecha, (2020) concurred that a person benefits from education in reading, arguing, being able to choose in a more informed way, this assertion in this case may not hold water since a good number of respondents opted to be neutral. More so, Basu (2020) added that education helps discover various facts and their inter relationships, help to discard distortions and contribute to an understanding of reality, make critical and logical analysis of problems, help in analysing perceptions, attitudes on different issues in local and global environment; this could only apply in areas of specialty by participants.

Reliability Scale

Cronbach’s Alpha test was done to assess the reliability, or internal consistency, of a set of scale or test items i.e. to check on the validity of the scale and the results are shown below:

Table 4.5 Reliability Statistics

| Reliability Statistics | ||

| Cronbach’s Alpha | Cronbach’s Alpha Based on Standardized Items | N of Items |

| .751 | .789 | 15 |

SPSS output

The reliability of the scale has a Cronbach’s Alpha value of 0.751 which is above 0.70, hence the scale reliability is considered good. There was no individual item that was higher than the total Alpha, hence all items were retained.

Factors that contribute to non-tax compliance

Objective 1: To what extent do formal and informal institutional factors, alongside business owner characteristics and firm-specific attributes, contribute to non-tax compliance among SMEs at Green market downtown, Mutare

Table 4.6 Factors that contribute to non-tax compliance

| Descriptive Statistics | |||||

| N | Minimum | Maximum | Mean | Std. Deviation | |

| Institutional factors | 90 | 1 | 5 | 3.48 | 1.400 |

| Economic Factors | 90 | 1 | 5 | 3.87 | .902 |

| Social Factors | 90 | 1 | 5 | 3.94 | 1.135 |

| Firm’s Characteristics | 90 | 1 | 5 | 3.84 | 1.170 |

| Managerial Characteristics | 90 | 1 | 5 | 3.79 | 1.156 |

| Average mean Valid N (listwise) | 90 | 3.79 | 1.153 | ||

SPSS Output

Source: Primary data (2024)

From table 4.6 above show the factors that contribute to non-tax compliance. A high mean of 3.94 shows strong agreement to the assertion that social factors contribute greatly to non-tax compliance, with a standard deviation of 1.170 which is above 1 showing a deviation from the mean achieved on the question. Overally the average mean and standard deviation respectively (M=3.79, SD=1.153). The SD=1.153 is relatively high compared to the mean which means the responses ranged from strongly agree to strongly disagree; hence the responses were not close to the mean.

Factor analysis using KMO and Bartlett’s Test

Table 4.7 KMO and Bartlett’s Test for determinants of non-tax compliance

| KMO and Bartlett’s Test | ||

| Kaiser-Meyer-Olkin Measure of Sampling Adequacy. | .574 | |

| Bartlett’s Test of Sphericity | Approx. Chi-Square | 16.290 |

| df | 10 | |

| Sig. | .092 | |

The Kaiser-Meyer-Olkin (KMO) measure of sampling adequacy indicated that the sample is adequate enough to extract factors using factor analysis with KMO of 0.574. If the KMO > 0.5, it means that it is acceptable.

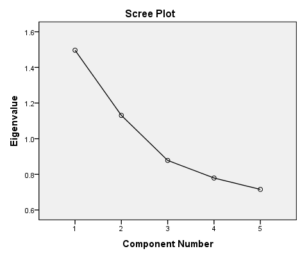

Table 4.8 Total Variance Explained for determinants

| Total Variance Explained | ||||||

| Component | Initial Eigenvalues | Extraction Sums of Squared Loadings | ||||

| Total | % of Variance | Cumulative % | Total | % of Variance | Cumulative % | |

| 1 | 1.497 | 29.931 | 29.931 | 1.497 | 29.931 | 29.931 |

| 2 | 1.131 | 22.614 | 52.545 | 1.131 | 22.614 | 52.545 |

| 3 | .878 | 17.562 | 70.106 | |||

| 4 | .779 | 15.586 | 85.692 | |||

| 5 | .715 | 14.308 | 100.000 | |||