Analysing Factors that Enhance the Growth and Survival of Small and Medium Enterprises in Ghana

- Seth Amoako (PhD)

- Elvis Boateng (PhD)

- Edward Domina Attafuah (PhD)

- 335-351

- Mar 14, 2024

- Education

Analysing Factors that Enhance the Growth and Survival of Small and Medium Enterprises in Ghana

Seth Amoako (PhD)1, Elvis Boateng (PhD)2, Edward Domina Attafuah (PhD)3

CEO- S AMOAKO VENTURES, Post Office Box 8984, Ahinsan, Kumasi1

Manager Ghana Water Company Limited, Kumasi- Ashanti2

School of Finance and Financial Management, Universidad Empresarial De Costa Rica3

DOI: https://doi.org/10.51244/IJRSI.2024.1102026

Received: 15 January 2024 ; Revised: 04 February 2024; Accepted: 09 February 2024; Published: 14 March 2024

ABSTRACT

The economy of Ghana has been growing consistently during the recent years, and this growth has increased poverty and increased the number of middle-income countries in the region. Meanwhile, the current regional and global economic slowdown requires a new growth model for Ghana, with strengthened fluctuation for Small and Medium-sized enterprises (SMEs) to raise national productivity.

Small and Medium Enterprises (SME’s) in Ghana play a dynamic role in the development of this nation, and this cannot be over- emphasized. It also serves as a means of employment in the country thus releasing the pressure on the civil and public sector in the case of employment. The study seeks to solve a problem of technology by Small and Medium Enterprises (SME’s) surveyed in Ghana by using PESTEL theory. It that painful process that Small and Medium Enterprise face to access the loan.

Examine the various causes that hinder the growth and survival of small businesses in Ghana. To examine the variables that leads to the growth and survival of small businesses. To enumerate various sources of funds available to SMEs in Ghana and to ascertain the impact of hindrances by SME‟s to the growth of Ghana economy. Finally, the study also revealed that most of the entrepreneurs do not have much knowledge in using technology and it has affected the growth and the survival of SME. It is believed that if all the recommendations are taken into consideration, that entrepreneurs must regard the legal aspect of their day-to-day activities and process the necessary documents to avoid legal actions taken against them.

Key words; Entrepreneur, Entrepreneurship, survival, growth, finance, pestle, sme’s, debt finance, equity finance, micro business, large business

INTRODUCTION

BACKGROUND TO THE STUDY

There is increasing identification of the significant role that Small and Medium Enterprises (SME‟s) play in economic development in Ghana. They are often described as efficient job creators in certain cases and the seeds of businesses and the fuel of national economic engines in Ghana (Amoah S K & Amoah, A K 2018). Even in the developed industrial economies, SME‟s Sector is the largest employer of workers. Interest in the role of SME‟s in the development process continues to be at the forefront of policy debates in most countries. Governments at all levels have undertaken initiatives to promote the growth of SME‟s (Feeney and Riding, 2020: Carsamer, 2019).

Micro, Small and Medium Enterprises in Ghana are said to be a characteristic feature of the production landscape and have been noted to provide about 85% of manufacturing employment of Ghana (Aryeetey, 2021). SME‟s are also believed to contribute about 70% to Ghana’s Gross Domestic Product (GDP) and account for about 92% of businesses in Ghana. SME’s therefore have a key role to play in facilitating growth, generating employment and contributing to poverty alleviation, given their economic weight in African countries Amoah, S. K., & Amoah, A. K. (2018). SME‟s development can encourage the process of both inter and intra-regional decentralization; and, reckoning force in catching up with economic superpowers of larger economies in the developed world. More generally, the development of SME‟s is seen as accelerating the achievement of wider socioeconomic objectives, including poverty alleviation (Cook and Nixson, 2020).

A lot has been said and written about SME‟s the world over. It has also formed the subject of discussions in so many seminars and workshops both locally and internationally. In the same token, governments at various levels (local, state and regional levels) have in one way or the other focused on the Micro and Small Enterprises. Governments almost all over the world had formulated policies aimed at aiding and empowering the growth, development and performance of the SME‟s. Some of the governments‟ efforts relate to focus on assisting the SME‟s to grow through soft loans, managerial training and other fiscal incentives through support from international agencies and organizations Adjei, D. S. 2019).

It has been notified that most of the Small and Medium enterprises in Ghana to be precise Kumasi of Ashanti Region collapse after some few years of establishment recognize poor growth and lack survival (Saani, S. M. 2018). Also, it is believed that, a lot of Small and Medium Enterprises do not grow due to poor planning and it has been one of the biggest challenges that most of the Small Scale Enterprises are facing intensively in Kumasi (Kusi et al 2015). In an effort to expand its economy, Ghana has implemented a number of policy initiatives (Mmieh and Owusu-Frimpong, 2019). As a component of the revitalization initiatives aimed at stimulating the Ghanaian economy, the financial system received additional support to reach a noteworthy degree of development.

In order to supplement the efforts of the main 23 banks in providing financial help to SMEs, the distressed banks experienced a resurgence. The number of large banks expanded from 5 to 23. Additionally, over 125 community banks were involved (Mmieh and Owusu-Frimpong, 2019). The study indicates that despite attempts to strengthen the financial system to support the SME sector, the domestic economy still depends heavily on the small company sector for funding, and that the sector still lacks the financial lubricant to promote expansion and growth. about activities related to subsistence (Mmieh et al., 2019). According to data from the African Commission’s 2009 report, entrepreneurship has been viewed as a competitive option to formal employment in Africa from the standpoint of development. As a result, a large portion of development assistance is concentrated on measures to help African youth realize their full potential through entrepreneurship, with the hope that this will boost the continent’s countries’ competitiveness and spur growth driven by the private sector.

Opoku (2020) reiterates that employment and entrepreneurship are becoming more and more crucial to economic growth and development at different levels of SMEs. It is said that employment in the unorganized sector has increased significantly during the last 20 years everywhere in the world, but especially in Africa. It is estimated that 93% of newly created employment in Africa come from the unorganized sector (Opoku, 2020). However, there hasn’t been a clear-cut definition of SME that is accepted by everyone (Burns, 2021). The OECD (2018) defines a rapid growth firm as a high growth enterprise with average yearly growth in turnover and workers. Importantly, a nation’s economic development mostly depends on small enterprises that expand quickly to become middle-sized and ultimately major businesses. Above all, any country that is capable of supporting small firms’ expansion is, in theory, the most crucial component of company development (Storey and Greene, 2020). In emerging economies, such as those in Sub-Saharan Africa, like Ghana, the expansion of SMEs may offer a path for export development and economic expansion (Robson and Freel, 2018).

Despite this, Sub-Saharan African economies—aside from South Africa—have given relatively little attention to the role that SMEs play in exporting, and as a result, their share in world commerce is just 23% (World Economic Forum, 2017). For example, in Ghana, the share of SME exporters in overall exports is barely 25% (Owusu Frimpong and Mmieh, 2019; GEPC, 2016). It is widely acknowledged that developing nations’ GDPs are greatly boosted by the informal sector, and this tendency is seen to be improving (World Bank, 2017). According to estimates (DFID’s Commission for Africa, 2015), the private sector generates around 90% of all newly created jobs in Sub-Saharan Africa, excluding South Africa, and accounts for about 85% of all employment in the region.

About 90% of all workers in Ghana are employed in the private sector (GSS, 2020). It is unfortunate to say that, despite the private sector’s major influence, scholars have given the economic activity in Africa’s informal sector very little attention (Jackson et al., 2018). This study aims to close this information gap by examining the variables affecting the expansion of SMEs in Ghana’s unorganized sector. It is significant to highlight that the informal sector dominates Ghana’s economic activity (Owusu Frimpong and Mmieh, 2019).

Nevertheless, barriers include difficult access to capital, unfavorable exchange rates, inadequate infrastructure, and inadequate trade organizations hobble SMEs in Ghana (Buame, 2022; Storey and Greene, 2020; Ghauri, et al. 2023). Lack of information on business procedures and security concerns affect a larger proportion of SMEs involved in entrepreneurial activities in emerging economies (Storey and Greene, 2020; Buckley, 2017; Ghauri, et al., 2023). Fadahunsi (2022), however, notes that a number of the linked claims made in earlier research are unclear because the empirical data for them is occasionally contradictory.

Therefore Agyapong (2020) and OML Africa (2022) highlight that the Ghanaian experience of entrepreneurship has not been that good, and SMEs continue to suffer stagnation and their activities are largely unaccounted for. For this reason, there is a need to investigate the factors influencing the development and growth of SMEs in the Ghanaian context. In the context of small businesses, key decision-making is the sole responsibility of the owner/manager, and the ability to grow or expand the business depends on a number of variables which will influence the expansion and growth of the business. This generates insights into the question as to whether the performance of a business is influenced by the entrepreneur by way of undertaking actions that can significantly influence that growth (Storey and Greene, 2020). There are many factors that influence the development and growth of SMEs. Storey and Greene (2020) suggests three categories of seminal key factors that influence the performance and growth of small businesses.

Other factors influence the development and growth of SMEs as far as a developing country like Ghana is concerned (Dietz, et al., 2020). These factors unraveled through this study, however, not given attention, among other things include erratic energy supply, inflation, government policy on taxation, location, and terms of repayment on loans. These factors play a pivotal role in either enhancing or constraining the development and growth of SMEs in Ghana. These factors are particularly important since small businesses depend on the national grid for energy supply, operate in a competitive global environment, and are affected by government fiscal and monetary policies.

This suggests that context counts so much as far as the activities of SMEs are concerned regardless of the homogeneity of the sector. The range and impact of factors may vary from one economy to another (Dietz, et al., 2020). This notwithstanding, very little attention has

been paid by researchers, despite the call for more research work needed in order to identify factors that affect SMEs in a developing economy context (Agyapong, 2020; OML Africa, 2022). This lack of research on the activities of SMEs in developing economies and Ghana in particular is quite alarming since the recent discussion on economic performance in advanced economies indicates that the private-sector growth could potentially improve the competitiveness of the African economies (IMF, 2022; African Commission, 2019). However, entrepreneurship in developing economies like the Sub-Saharan Africa, and Ghana for example, still remains under-researched in stark contrast to developed economies (Kshetri, 2021: 10; Melvin and Boyes, 2013).

Besides, the indiscriminate application of theories of developed economies to management studies in developing economies like the Sub-Saharan African and Ghana in particular, calls into question the possible application of empirical evidence from existing studies on development and growth of SMEs conducted in developed economies to the context of Africa (Jackson, 2018). This premise precipitates the need for studies in a Sub-Saharan developing economy like Ghana on factors that influence the development and growth of SMEs, and this study aims to fill that gap.

LITERATURE REVIEW

This episode tends to note how various writers have endeavored to publish about Small and Medium Enterprise (SME’s) as well as factors that hinders the growth and survival of Small and Medium Enterprises, especially in Ghana. It deals with the various definitions, characteristics associated with Small Scale Enterprises. Their roles in developing the economy, sources of their financial operations and support service provided by the government of the day, and to explore the various barrier to accessing funds and managing Small and Medium Enterprises (SME’s) and their owners in Kumasi Metropolis (Opoku 2019).

Many positive characteristics of Small and Medium Enterprise have long been recognized at the first and second Industrial Development Decade for Africa (IDDA) as a potent engine for growth. After independence policies on economic development in Ghana are paying attention to the formation of contemporary industrial structures throughout Direct Public Investment in large-scale industries. Creditable as they were, policies on industrial development become unsuccessful because insufficient concentration was remunerated to the economic feasibility of the enterprise market prospect. As a result of a change in government policies not granting subsidies to and a move from direct state contribution through ownership of companies, the government now places stress on private sector initiatives instead of the large public enterprises. Since that time, micro businesses have played a meaningful role in the direction of industrialization many positive characteristics of Small and Medium Enterprise have long been recognized at the first and second Industrial Development Decade for Africa (IDDA) as a potent engine for growth.

After independence policies on economic development in Ghana are paying attention to the formation of contemporary industrial structures throughout Direct Public Investment in large-scale industries. Creditable as they were, policies on industrial development become unsuccessful because insufficient concentration was remunerated to the economic feasibility of the enterprise market prospect. As a result of a change in government policies not granting subsidies to and a move from direct state contribution through ownership of companies, the government now places stress on private sector initiatives instead of the large public enterprises. Since that time, micro businesses have played a meaningful role in the direction of industrialization (Jackson, 2018).

LACK OF CAPITAL

Lack of capital seems to be the primary reason for business failure and is considered to be the most significant problem facing small and micro business owners. Shafeek (2019) said; from a business viewpoint without adequate financing, the business will be unable to maintain and acquire facilities, attract and retain capable staff, produce and market a product, or do any of the other things necessary to run a successful operation.

HUMAN RESOURCE MANAGEMENT

The competence of the SME owner/manager is the ultimate determinant of survival or failure. The cause of either SME failure or poor performance is almost invariably a lack of management attention to strategic issues such as human resources management. Moreover, the early founder of the SME’s personal competence in selecting the right business and running it will be crucial, as the firm is likely to be indistinguishable from the owner Nikolić et al (2015). . Therefore, as the market develops, growth can be rapidly partial due to unwillingness or inability to draw others to help with the management of the agribusiness sme (pasanen, 2019).

MARKETING

According to Shafeek (2019) marketing is the only functional area that links the products or services of a business to its customers. He adds on to say; it is vitally important to ensure that this function. To have a good chance of survival, a small or micro agribusiness firm needs to answer the basic strategic questions: “what markets are we targeting, with what products?” A common weakness in the (agribusiness) SME owner/managers lies in their failure to understand key marketing issues (Stokes and Wilson, 2019). Stokes and Wilson (2019) are of the belief that product or service concepts and standards often reflect only the perceptions of the owner, which may not exist in the marketplace. He adds on to say, minor fluctuations in markets can topple a newly established small/micro firms, particularly where it is reliant on a small number of customers.

BUSINESS PLAN

According to Nieman and Nieuwenhuizen (2019), a business plan is a written document that carefully explains the business, its management team, its products/services and its goals together with strategies for reaching goals. It is a living document that forms part of the formal planning done by firms and serves as a tool for reducing the risk of venture failure, a benchmark for a firm’s internal performance as well as a tool for accessing funds (Nieman and Nieuwenhuizen 2019).

Small and micro firms by nature avoid formal planning, and as such do not have proper business plans. This, in turn, makes them not to be able to assess the firm’s internal performance, fail to access funds such as loans, and also be exposed to the higher risk of venture failure. A business plan as a living document needs to for it to increase the agribusiness SMEs’ chances of growing and surviving in the market Hove (P et al 2017).

ACCESS TO TRAINING

Education is one of the factors that impact positively on the growth of firms (King and McGrath, 2022). Those entrepreneurs with larger stocks of human capital, regarding education and (or) vocational training, are better placed to adapt their enterprises to continually changing business environments. SME‟s also lack business and marketing skills that may allow them to put together viable business proposals. They have less access to formal channels that provide comprehensive skills training because they are mostly unaware of the existence of such programmes and even when they are aware, their time constraints may limit their access.

MANAGERIAL COMPETENCIES

Managerial competencies have a positive influence on the performance of SMEs. Administrative experience, education, knowledge and start-up experience are used to measure managerial skills (Hisrich & Drnovsek, 2022). In a study where the importance of management competence in SMEs success a lack of managerial competency was found to be the leading cause of why SMEs fail (Martin & Staines, 2018). Abdel, Rowena & Robyn (2010) revealed that small business owner-managers have the fundamental understanding of financial and accounting information and have severe problems with financial planning literacy. On the same theme, it has been that small and micro enterprises owner-managers have little knowledge about financial matters, and found out that those with low or limited financial planning skills do not even value the information extracted from financial statements (Alattar, Kouhy & Innes, 2019).

SOURCES OF FINANCE TO BUSINESSES

Sources of finance are the means by which a firm obtains the funds or money needed to pay for fixed assets and support the business. According to Floyd (2021), sources of finance could be into external and internal sources. In other words, it could be as debt and equity depending on the purpose of the fund. External Source of Finance Debt is where an organization seeks capital outside the organization to undertake its day to day activities whiles Short-Term Debts

BANK OVERDRAFT

This type occurs when a customer of a banking financial institution is allowed to over withdraw his bank account. In other words, this is the amount by which the account holder is authorised to remove more than the amount of his credit. More often than not, a bank grants overdraft when the firm has enough savings with the bank and that the companies known as the customer of the bank. As per Schell (2018), the company pays interest on the amount over withdrawn.

LONG-TERM DEBT

These are liabilities which the businesses anticipate to pay off in a stipulated time give beyond one year. Long-term obligations are most often used to finance assets of the firm that is to be purchased for and used over an extended period and not employed in the course of the day to day business operations, such as the case with assets like inventory. Assets which are from long-term debts are fixed assets like equipment, plant and machinery land, and buildings, etc. Aryeetey et al.(2021). Just like short-term debts, long-term liabilities consist of the following:

LEASING

Leasing is a long-term means of getting hold of finance for a profession. This agreement is between two parties where one party the renter obtains the right to use an asset and makes period payment, known as rent, to the other party (lessor). Thus, instead of a firm acquiring an asset with cash, the business can obtain such an asset through hiring from another company. In leasing, the user of the property holds rights of the park, but the only, ownership rests with the lessor (Neuberger & Räthke-Döppner, S. (2019). Leasing contract could be operating (service), financed (capital). With the operating lease, according to Rose et al. (2020), managing lease is not fully amortised. That is, payments (rent) required are not enough to recover the full cost of the asset. Occurs due to the lifespan of the operating lease is usually lesser than the economic useful development cycle of the estate. T

EQUITY

Equity financing, unlike debt financing, creates a more uniform or stable correlation in which ownership interests to the person, a firm or entity providing funds. Equity in business reflects the owners’ investment in the market according to Floyd (2021), sources of finance could be into external and internal sources. In other words, it could be as debt and equity depending on the purpose of the fund. External Source of Finance Debt is where an organisation seeks capital outside the organisation to undertake its day to day activities whiles Short-Term Debts

PARTNERSHIP/ JOINT VENTURE

The partnership is one means through which individuals can contribute funds towards the operations of their business. Many people can come together as partners or joint ventures to form a firm. A partnership usually helps in risk management in periods of losses.” As Harper (2020) said, a member of the company contributes to meet the needs of the firm in times of financial obligations”.

PERSONAL SAVINGS

Storey &Green (2020) further indicated that personal savings must be brought to the barest minimum levels and may end up in a steady lack of local savings with regard to domestic investment or accounts for surplus demand for available domestic savings. The most common source of funds for micro businesses is through personal past accumulations of funds. With this source of finance, the individual personally starts the business with his /her past savings accumulated over a period. The merit associated with this source of funds is that there is no or low risk associated with it Nunoo, J. (2021).

This chapter focuses on the general research design. It comprises the area of study population sample and sampling procedures, the administration of the instrument, the limitation of the study and data analysis procedures.

METHODOLOGY

RESEARCH DESIGN

Technically disentangling the link between or among variables in a circumstance and analyzing the relationship free of outside effects is crucial to solving the study challenge (Nenty, 2019). Accordingly, Nenty (2019) believes that study design comprises the methods by which we may investigate and evaluate the link between the variables involved in our problem and, as a result, to argue for the superiority of certain processes over others.

A quantitative research design and a descriptive study are used to conduct this profound study. Adams et al., (2017); and Bryman (2022) point that the quantitative research design uses different types of statistical analysis and provides stronger forms of measurement, reliability and ability to generalize. Quantitative design refer to the research that is based on the methodology principles of positivism and neo-positivism and adheres to the standards of a stick research design developed prior to the actual research (Adam et al., 2017). Moreover, Berg (2020) argues that the quantitative method can deal with longer time periods with larger number of samples increasing the generalization capacity. The research study in the Ashanti Region of Ghana. Descriptive design on the other hand is Descriptive research design uses a range of both qualitative research and quantitative data (although quantitative research is the primary research method) to gather information to make accurate predictions about a particular problem or hypothesis Gunter, B. (2013).

In this research work, the Small and Medium Enterprise (SME’s) operators and managers were involve because the researcher believes it would help him to have the chance to work together with them. Entrepreneurs in this industry to get hold of how they carry on with a business about financing in Ghana.

Both Primary (questionnaire) and Secondary data were employed for the study. A practical data collection approach is use for the research work. This part of the study brings to the user how the data is collected for the study. The mode of data collection incorporated primary data and secondary data sources. This source provides the researcher with second-hand data relating to the research topic. In other words, data collected from this source are those who are already in existence and have for further use for the studies. They usually are from credible sources such as banks, educational institutions, governmental organizations.

It also brought to light the extent to which awareness is being to this study;

The primary sources of data make available direct and new data from the field. This source of data enabled the researcher to get hold of first-hand facts on the ground of study. This data after the researcher had sufficiently exhausted the secondary data. The researcher employed designed questionnaires techniques to collect data

RESEARCH METHODS

Researchers around the world have employed two main research approaches, namely the quantitative and the qualitative research methods (Adams et al., 2017). The qualitative method presents a descriptive and non-numerical approach to collect the information in order to present understanding of the phenomenon (Berg 2020). Adams et al , (2017) argue that qualitative method employs methods of data collection and analysis that are non-quantitative, aims towards the exploration of social relations, and describes reality as experienced by the respondents. Babbie (2020) points out that qualitative method is an active and flexible method that can study subtle nuances in the attitudes and behaviors for investigating the social processes over time.

On the other hand, Adams et al., (2017); and Bryman (2022) point that the quantitative approach uses different types of statistical analysis and provides stronger forms of measurement, reliability and ability to generalize. Quantitative approaches refer to the research that is based on the methodology principles of positivism and neo-positivism and adheres to the standards of a stick research design developed prior to the actual research (Adam et al., 2017). Moreover, Berg (2020) argues that the quantitative method can deal with longer time periods with larger number of samples increasing the generalization capacity.

POPULATION 0F THE STUDY

The main populations targeted were the owners or managers of various small and medium scale enterprises in Ghana especially Ashanti Region, Bosomtwe district. The people of the study consist of all the Small and Medium Enterprise (SME’s) operators or owners who are in Ghana, especially Ashanti Region, Bosomtwe district and its environs such as retailers, food vendors, carpenter etc. Ashanti Region is well-known as an exceptional place where almost all kind of trade takes place since it is the central business capital in Ghana. Over the years, micro business operators in the Ashanti Region have been a critical opportunity for self-employment and stage for training most of the youth especially the ignorant ones.

The sample size of the population was five hundred and forty (540) operators or owners in Ghana, especially Ashanti Region, Bosomtwe district. Given the information needed for the study and the nature of the population, the researcher adopted quota, stratified and convenient sampling techniques. Quota sampling to specific managers and entrepreneurs to the Bosomtwe district in the Region. After allocating a required number to the community, convenient sampling was used to choose respondents who were available to the data needed.

RESULTS

DATA AND INFORMATION DESCRIPTION

In this episode, the research goes on to present the analysis of the data obtained from the respondents and interviews in the research study. This part of the research work comprises questionnaires to respondents such as managers, entrepreneurs and employees or workers. This chapter presents the information on data collected from the respondents on the topic exploring obstacles to managing and accessing funds among small and medium enterprises in Ghana using financial ratios as a tool of measurement. The chapter presented the findings base on the objectives set for the study. The study evaluates the demography and the gender of the respondents. Examine the costs associated with debt finance and causes of failure in managing and accessing funds among small and medium enterprises. Assess various sources of resources available to small and medium companies, evaluates the multiple barriers to access to funding and the causes of low productivity to the small and medium group and finally ascertain the effect of causes of failure to managing and obtaining funds on some owner-manager in Ghana. The data are in tables and other statistical tools. The survey on a total of 250 respondents out of which 200 responses were received representing 80% response rate.

The data collected and gathered from the different sources using the designed questionnaires in a way that was meant to aid the reader to make sense of the information contained in the researcher’s findings. There was an abundant method of data analysis that was open up to the researcher to employ. However, the researcher selected these methods which for this project would allow the user to interpret the information contained in the plan without any sense of ambiguity and also to make easy assimilation.

CAUSES THAT HINDER THE GROWTH AND SURVIVAL OF SME’S

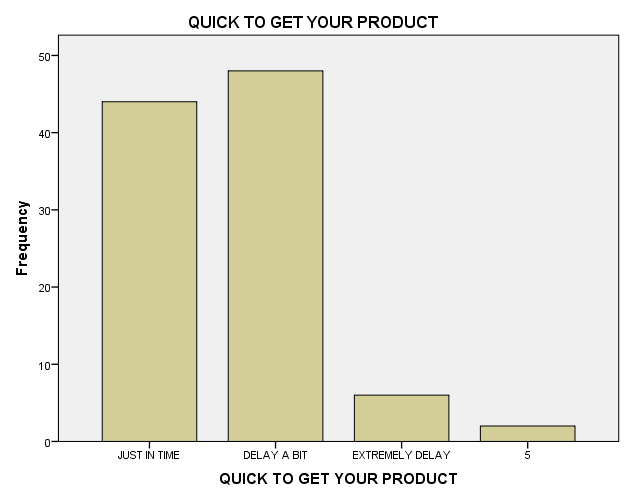

TABLE 4.2.2 QUICK TO GET YOUR PRODUCT

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | JUST IN TIME | 44 | 44.0 | 44.0 | 44.0 |

| DELAY A BIT | 48 | 48.0 | 48.0 | 92.0 | |

| EXTREMELY DELAY | 6 | 6.0 | 6.0 | 98.0 | |

| 5 | 2 | 2.0 | 2.0 | 100.0 | |

| Total | 100 | 100.0 | 100.0 | ||

Source: Researcher’s Fieldwork, 2018

Source: Researcher’s Fieldwork, 2022

FIGURE 4.2.1 QUICK TO GET YOUR PRODUCT

The above table shows that 44 % of the respondents believe that good and materials supply to the customer is just in time and does not hinder the growth and survival of a business. 48% of the respondents also believe that good and materials supply to the customer also delay a bit and this act hinders the growth and its survival of SME. Meanwhile, 6% of the respondents also believe that good and materials supply to the customer also delay extremely and this act hinder the growth and its survival of SME whiles 2% of the respondents are indifferent.

TABLE 4.2.3 PROBLEM DURING PRODUCT AVAILABILITY

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | PRODUCT SCARCITY | 35 | 35.0 | 35.0 | 35.0 |

| PROODUCT AVAILABILITY | 30 | 30.0 | 30.0 | 65.0 | |

| PARTIAL PRODUCT SCARCITY | 35 | 35.0 | 35.0 | 100.0 | |

| Total | 100 | 100.0 | 100.0 | ||

Source: Researcher’s Fieldwork, 2022

The above table shows that 35% of the respondents believe that scarcity of good hinders the growth and survival of a business. 30% of the respondents also believe that good are always available and does not hinder the growth and its survival of SME whiles 35% of the respondents also believe that goods are partially scarce and it hinders the growth and survival of SME. The implication is that majority of the respondent understand that scarcity and partial scarcity of goods hinder the growth and survival of businesses

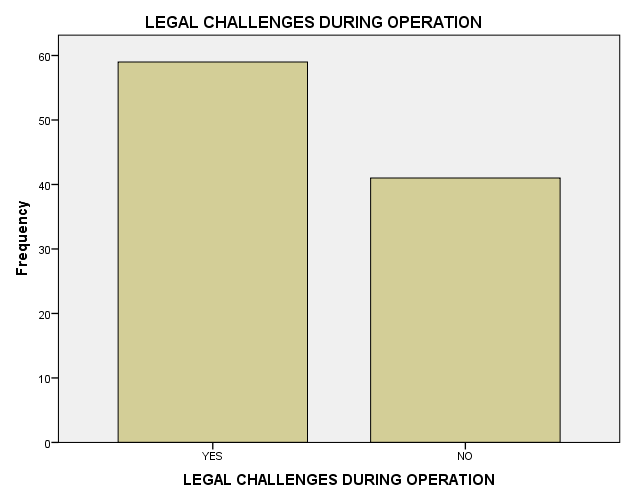

TABLE 4.2.4 LEGAL CHALLENGES DURING OPERATION

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | YES | 59 | 59.0 | 59.0 | 59.0 |

| NO | 41 | 41.0 | 41.0 | 100.0 | |

| Total | 100 | 100.0 | 100.0 | ||

Source: Researcher’s Fieldwork, 2022

Source: Researcher’s Fieldwork, 2022

FIGURE 4.2.2 LEGAL CHALLENGES DURING OPERATION

The above table shows that 59% of the respondents believe that there are a lot of legal challenges confronting SME during operations and it hinders the growth and survival of business while 41% of the respondents also believe that there are no legal challenges hinder the and its survival of SME.

FACTORS THAT ENHANCE THE GROWTH AND SURVIVAL OF SME’S

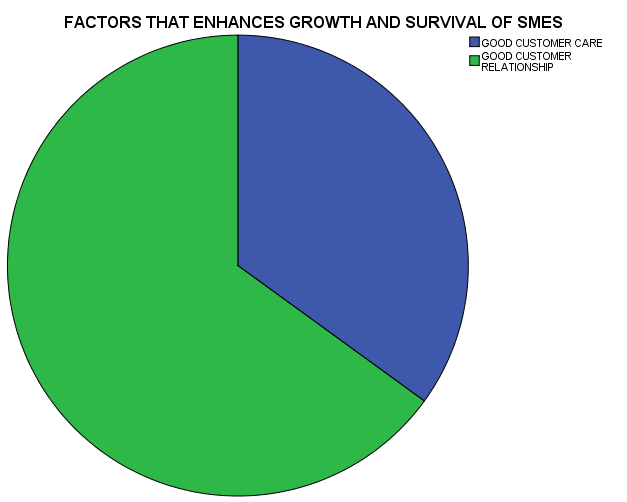

TABLE 4.28 FACTORS THAT ENHANCES GROWTH AND SURVIVAL OF SMES

TABLE 4.2.5 FACTORS THAT ENHANCES GROWTH AND SURVIVAL OF SMES

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | GOOD CUSTOMER CARE | 35 | 35.0 | 35.0 | 35.0 |

| GOOD CUSTOMER RELATIONSHIP | 65 | 65.0 | 65.0 | 100.0 | |

| Total | 100 | 100.0 | 100.0 | ||

Source: Researcher’s Fieldwork, 2022

Source: Researcher’s Fieldwork, 2022

FIGURE 4.2.3 FACTORS THAT ENHANCES GROWTH AND SURVIVAL OF SMES

The above table shows that 35 % of the respondents believe that good customer care enhances the growth and survival of business while 65% of the respondents also believe that good customer relationship improves the business growth and its durability. The implication is that majority of the respondent understand the customer relationship.

TABLE 4.2.6 CUSTOMERS HAVING PURCHASING POWER

| Frequency | Percent | Valid Percent | Cumulative Percent | ||

| Valid | GOOD PURCHASING POWER | 87 | 87.0 | 87.0 | 87.0 |

| AVERAGE PURCHASING POWER | 9 | 9.0 | 9.0 | 96.0 | |

| POOR PURCHASING POWER | 4 | 4.0 | 4.0 | 100.0 | |

| Total | 100 | 100.0 | 100.0 | ||

Source: Researcher’s Fieldwork, 2022

The above table shows that 67 % of the respondents have a good purchasing power, and 9% of them have an average purchasing power, whiles, 4% of the respondents also have poor purchasing power. The implication is that majority of the respondent can buy products at ease.

EVALUATION OF THE RESEARCH

This section is the final part of the research work that was. Most of the problems discovered through the questionnaires and interviews. Summary and findings of the research work, whiles recommendations and conclusions drawn from the research work are under this chapter. A lot of suggestions are for further research.

FINDINGS AND DISCOVERIES

CAUSES THAT HINDER THE GROWTH AND SURVIVAL OF SME’S

The respondents were whether goods and materials supply to the customer are supplied just in time or delay. 48% of the respondents believe that good and materials satisfy to customer delay a bit, and this act hinders the growth and its survival of SME. However, a few of them admitted that supply delays extremely. The implication is that majority of the respondent understand that delay of goods and materials to customer hinder the survival of SME,

Again, respondents were whether goods are always scarce in the market or not. A few of the respondents believe that excellent is still available, but the majority of the respondent understand that scarcity and partial scarcity of goods hinder the growth and survival of businesses.

The researcher wanted to know if SME faces legal challenges in their daily operations. It was that there are a lot of legal problems confronting SME during operations and it hinders the growth and survival of a business. Whiles 41% of the respondents also believe that there are no legal challenges hinder the and its survival of SME.

FACTORS THAT ENHANCE THE GROWTH AND SURVIVAL OF SME’S

Considering factors that enhance the growth and survival of SME, it observed that 35 % of the respondents believe that good customer care enhances the growth and survival of business while 65% of the respondents also think that good customer relationship improves the business growth and its durability. The implication is that majority of the respondent understand the customer relationship.

Again, the researcher wanted to whether customers have purchasing power or not, and it was that 67 % of the respondents have a good purchasing power, and 9% of them have implication is that majority of the respondent can buy products at ease.

Similarly, asking about the customer’s loyalty to the product at hand it was noted that, 97 % of the respondents have good loyalty to the product and it enhances the growth and survival of business while 3% of the respondents also have a weak commitment to the product in a market.

In terms of price sensitivity, 11 % of the respondents believe that price regulation of a product from the government enhances the growth and survival of a business, 14% of the respondents believe that also think that tax reduction improves the growth and survival of a business whiles, 75% of the respondents also believe that good policies from the government does it all.

17% of the respondents believe that product availability enhances SME growth and survival. 45% of the respondents also think that fair competition amongst SME improves the growth and survival of SME and 38% of the respondents also believes that good infrastructural enhance the growth and survival of SME.

Finally, 45% of the respondents agreed that quality product enhances the growth and survival of businesses, 53% strongly agreed to the same statement whiles 2% refrained from the same comment. The implicates is that most of the respondents were in favour that quality product enhance the growth and survival of businesses,

RECOMMENDATIONS

To deal with the topic analysing factors that impede the growth and survival of small and medium enterprises in Ghana using PESTEL as a tool of analysis. The researcher suggested that to minimise factors that interfere with the growth and endurance for the small and medium businesses in Ghana; entrepreneurs should maintain the pace at which materials supply to the customer so that they may not delay a

Again, the researcher recommended that it would be better if entrepreneurs could use their saving as start-up capital an also resort to debt finance from the banks to expand their businesses to employ more people. Furthermore, the researcher recommended that government should provide the enabling environment for entrepreneurs to be able to perform credibly.

Finally, the researcher suggested that entrepreneurs must regard the legal aspect of their day to day activities and process the necessary documents to avoid legal actions taken against them

It is highly recommended by the researcher that, small and medium enterprises in Ghana are promoted by the Government as well as individuals to help improve the sector.

The study consists of one hundred and ten (110) SME’s, meanwhile, all means of analysing factors that hinder the growth and survival of small and medium enterprises in Ghana had not covered. Meanwhile, some necessary variables within the SME industry can be subjected to more critical study so that one can decide the degree that one can compete with the use of the quantitative procedure. Given this other right variable such as political, economic, sociological, technological, environmental as well as legal (PESTEL) any of these variables could be considered to ascertain the impact of hindrances to Small and Medium Enterprise (SME’s) in Ghana. Further studies could be in this critical area.

CONCLUSION

On the whole, the study concludes that most of the Small and Medium Enterprises (SME’s) surveyed in Ghana PESTEL theory is highly applicable in Ghanaian economy as far as SME is concerned.

It that the problem that Small and Medium Enterprises (SME’s) in Ghana are facing is the painful process that they pass through before they can access the loan.

Finally, the study also revealed that most of the entrepreneurs do not have much knowledge in using technology and it has affected the growth and the survival of SME, but time did not permit that.

Most people who were contacted for responses were not ready to provide the most detailed information, all in the name of ensuring secrecy and confidentiality. However, the right work was done in spite of all these shortfalls or challenges. Cost of transportation, script typing and printing all in a way hindered the complete success of this research.

REFERENCES

- Alidu, M. Yakubu and Adae Korankye (2022) Morden Approach to Advance Level Economics.

- Altman, EI 2021, ‘Financial Ratios, Discriminant Analysis and the Prediction of Corporate

- Angela and Motsa Associates, (2020). SMME Finance Sector Background Paper: A Review of key documents on SMME Finance 1994-2004. Fin Mark Trust: Johannesburg.

- Anheier, H. K. and Seibel, H. D. (2017). “Small Scale Industries and Economic Development in Ghana”, Business Behaviour and Strategies in Informal Sector Economies, Verlag Breitenbech, Saarbruckh, Germany

- ASEAN (Association of Southeast Asian Nations) (2015), “SME Access to Financing: Addressing the Supply Side of SME Financing,” RAM Consulting, Final Report for the ASEAN Secretariat.

- Beal, D, Goyen, M &Shamsuddin, A 2018, Introducing Corporate Finance, 2 edn, John Wiley & Sons Australia, Ltd., Australia.

- Beaver, WH 2016, ‘Financial Ratios as Predictors of Failure’, Empirical Research in Accounting: Selected Studies, Supplement to Journal of Accounting Research, vol. 4,pp. 71-111.

- Blum, M 2020, ‘Failing Company Discriminant Analysis’, Journal of Accounting Research, vol. 12, no. 1, pp. 1-25.

- Brigham, E., & Houston, J. (2019).Fundamentals of Financial Management. Mason: Cengage Learning.

- Brigham, EF &Ehrhardt, MC 2018, Financial Management: Theory and Practice, 12 edn, South-Western, USA

- Churchill, C. and Frankiewicz, C. (2016). Making Microfinance Work: Managing for Improved Performance, International Labour Office. Geneva.

- Cressy, R. and Toivanen, (2021) Is there Adverse Selection in the Credit Market?, Venture Capital 3 (3) 215-238

- Drake, P. (2020). Financial ratio analysis.

- Dwomo-Fokuo, E. (2016) Entrepreneurship Theory and Practice. Pg 132 European Economic Review, 31(4), pp. 887-9.5

- Equity in Higher Education. Rotterdam: Sense Publishers. International Journal of Business and Social Science Vol. 3 No. 21; November 2012173

- Financial Management by I. M. Pandey

- Financial Management by M. Y. Khan and P. K. Jain

- Financial Management by Prasanna Chandra

- Fitzpatrick, P 1931, Symptoms of Industrial Failure, Catholic University of America Press., USA

- Foxcroft, M., E. Wood, J. Kew, M. Herrington and N. Segal, (2022). Global Entrepreneurship Monitor: South African Executive Report, Graduate School of Business University of Cape Town

- Frase, L., & Ormiston, A. (2019).Understanding Financial Statements. New Jersey: Pearson Prentice Hall.

- Frino, A, Amelia, H & Chen, Z 2019, Introduction to Corporate Finance, 4 edn, Pearson, Australia.

- Gibson, CH & Frishk off, PA 2016, Financial Statement Analysis: Using Financial Accounting Information, 3 edn, Kent Publishing Company, USA.

- Gockel, A. G. and Akoena, S. K. (2022).Finance international for the poor: Credit demand by micro, small and medium scale enterprises in Ghana. A further Assignment for Financial Sector Policy? IFLIP Research Paper 02-6, International Labour Organisation.

- Green, A. (2023). Credit Guarantee Schemes for Small Enterprises: An Effective Instrument to Promote Private Sector-Led Growth? SME Technical Working Paper No. 10. Vienna: UNIDO. Retrieved from: http://www .unido.org/file-storage/download/ ?file-id = 18223, (Accessed on: 23 February 2010).

- Hey-Cunningham, D. (2023).Financial Statements Demystified. New South Wales: Allen &Unwin.

- International Journal of Business and Social Science Vol. 3 No. 21; November 2012175

- Johnstone, D. B. (2019).Worldwide Trends in Financing Higher Education. In J. Knight, Financing Access and

- Kayanula, D. and Quartey, P. (2020).The Policy Environment for Promoting Small and Medium Enterprise in Ghana and Malawi. Finance and Development research Programme Working paper series no. 15.

- Merwin, CL 2022, Financing Small Corporations in Five Manufacturing Industries, 1926-36,

- OECD, (2018). The SMEs Financing Gap Volume 1:Theory and Evidence. Retrieved from: http://ec.europa.eu/enterprise/newsroom/cf/document.cfm? action = display & doc-id = 624 & user service-id = 1, (Accessed on: March 20, 2009).

- Osei, B., Baah-Nuakoh, Tutu, A. K. A. and Sowa, N. K. (2023). “Impact of Structural Adjustment on Small-Scale Enterprises in Ghana”, in Helmsing, A. H. J. and Kolstee, T. H. 228 International Research Journal of Finance and Economics – Issue 39 (2010) (eds.), Structural Adjustment, Financial Policy and Assistance Programmes in Africa, IT Publications, London.

- Oteng, G. (2023),”Financing SMEs the way forward. The Ghanaian Banker, financing the SMEs, 4th Quarter, October-December7.

- Parker, R. Riopelle, R. and Steel, W. (2020) Small Enterprises Adjusting to Liberalisation in Five African Countries, World Bank Discussion Paper, No. 271, African Technical Department.

- Retrieved August 2012, From http://www.accounting4management.com/accounting_ratios.htm#RGmZwPOdLeiTcCLR.9.

- Retrieved August 2012, from Commission on Higher Education: http://www.ched.gov.ph/hes/index.html.

- Retrieved August 2012, from Philippine Stock Exchange: http://www.pse.com.ph/stockMarket/home.html.

- Steel W.F. (1977), small scale employment and production in developing countries.

- Steel, W.F. and Webster, L.M. (2021), “Small Enterprises in Ghana: Responses to Adjustment”, Industry Series Paper, No. 33, The World Bank Industry and Energy Department, Washington

- Stiglitz, J and Weiss, (2021). “Credit Rationing in Markets with Imperfect Information”, American Economic Review 81, pp. 393-410

- Storey D &Green. (2020). “Understanding the Small Business Sector” London: Routledge,

- Thormi, W H and Yankson, P W K (2019) Small-scale industries decentralization in Ghana, preliminary report on small-scale enterprises in small and medium-sized towns in Ghana, Frankfurt/Accra

- Zavatta, R. (2018) Financing Technology Entrepreneur and SMEs in Developing countries.

- Gomer, Justin and Jackson Hille. “An Essential Guide to SWOT Analysis.” http://formswift.com/swot-analysis-guide

- Kansas University Work Group for Community Health and Development. “Swot Analysis: Strengths, Weaknesses, Opportunities and Threats.” Community Tool Box.http://ctb.ku.edu/en

- Manktelow, James. “SWOT Analysis: Discover new opportunities, manage and eliminate threats.” Mindtools. http://www.mindtools.com/pages/article/newTMC_05.htm

- Queensland (Australia) Government. “SWOT analysis”. https://www.business.qld.gov.au/business/starting/marketcustomer-research/swot-analysis

- Start, Daniel and Ingie Hovland. “SWOT Analysis”. Tools for Policy Impact. Overseas Development Institute, 2004.http://www.odi.org/publications/156-tools-policy-impacthandbook-researchers

- Watkins, Michael. “From SWOT to TOWS: Answering a Reader’s Strategy Question.” Harvard Business Review online. https://hbr.org/2007/03/from-swot-to-tows-answering-a-readersstrategy-quest