The Bridge To Acceptance: Investigating Consumer Perceptions of Virtual Bankers

- Ekwunife Gabriel Okafor

- Njelita, Chukwudi I.

- 982-995

- Jun 19, 2024

- Marketing

The Bridge To Acceptance: Investigating Consumer Perceptions of Virtual Bankers

Ekwunife Gabriel Okafor1, Njelita, Chukwudi I.2

1Department of Marketing, Nnamdi Azikiwe University, Awka, Nigeria.

2Department of Entrepreneurship, Nnamdi Azikiwe University, Awka, Nigeria.

DOI: https://doi.org/10.51244/IJRSI.2024.1105064

Received: 25 April 2024; Revised: 12 May 2024; Accepted: 19 May 2024; Published: 19 June 2024

ABSTRACT

Electronic banking technology advancements have resulted in new methods to process banking transactions, particularly through online banking channels. Virtual bankers are still in their early stages in Nigeria and are not being used as a significant cost-cutting tool for banks or to improve customer relationships. Using the technology acceptance model (TAM), this study will investigate the adoption of virtual bankers by customers of selected banks in Anambra State. The model was tested with a survey sample of 323 people, employing the survey research method as the research design, and simple linear regression to analyze the data. The study findings show that perceived usefulness and perceived ease of use have a positive and significant impact on virtual banker adoption. The study suggests that financial institutions adopt and deploy virtual banker platforms to enable seamless transactions and quick responses to task completion, as well as to improve job performance and overall output within the organization. Additionally, the study recommends that, for effective deployment and adoption of a virtual banker, financial institutions provide learning platforms that will ease the process and ensure that actual and prospective customers become proficient with the use and working processes of the virtual banker. The provision of learning platforms will encourage more consumers to get on board and adopt virtual bankers. Finally, the study suggests that virtual banker platforms and software should be continuously improved. This improvement aims to make them easier to use, faster in responding to consumer needs, and more innovative in addressing the anticipated and ever-growing needs of existing and future customers.

Keywords

Adoption, electronic banking, virtual banker, financial institution, Anambra state

BACKGROUND

Organizations invest in information systems for a variety of reasons, to improve efficiency, effectiveness, and productivity. According to Ayaz, and Yanartas (2020), research has shown that user’s attitude toward the acceptance of a new information system determines how efficient and effective the new information system is, and this also determines how much the system will benefit the organization. If users are unwilling to accept the information system, the organization will not reap the full benefits. The more users accept a new information system, the more willing they are to change their practices and use their time and effort to use the new information system (Sulci and Walter, 1999).

The technology acceptance model (TAM) is one of the models used to study information system acceptance (Davis, 1989; Davis and Venkatesh, 1996). The technology acceptance model is a theory of information systems that describes how users come to accept technology. It is a model in which perceived usefulness (PU) and perceived ease of use determine system use (actual behaviour) (PEOU). Therefore, the goal of this study is to investigate the technology acceptance model and consumer adoption of virtual bankers among customers of selected banks in Anambra State

Statement of The Problem

The evolution of information systems has had a profound impact on the banking industry, allowing for more adaptable payment methods and more user-friendly banking services. It has improved banking services all over the world and fundamentally altered the way banks function. Consumers welcomed some of these innovations while rejecting others.

Virtual banking continues to evolve the financial landscape, therefore understanding consumer perceptions of virtual bankers becomes imperative for financial institutions aiming to enhance customer experience and trust in digital platforms. Although there is remarkable positive change in the proliferation of virtual banking services, there remains a gap in comprehending how consumers perceive and interact with virtual bankers compared to traditional banking services.

This study therefore seeks to investigate the following key questions: how consumers’ perceived usefulness toward virtual banker actual adoption and also how consumers’ perceived ease of use toward virtual banker actual adoption.

By addressing these questions, this research aims to contribute valuable insights into the evolving dynamics of virtual banking and provide practical recommendations for financial institutions to effectively navigate and leverage consumer perceptions in their digital banking initiatives.

Objective of The Study

The main objective of this research is to examine the technology acceptance model and consumer adoption of virtual bankers through a study of customers of selected banks in unizik Awka

However, the specific objectives are;

To determine consumers’ perceived usefulness toward virtual banker actual adoption.

To determine consumers’ perceived ease of use toward virtual banker actual adoption.

Research questions

- Does perceived usefulness have influence on virtual banker adoption?

- Does ease of use have influence on virtual banker adoption?

Research hypotheses

H1: Perceived usefulness will have a positive and significant influence on virtual banker adoption.

H2. Perceived ease of use will have a positive and significant influence on virtual banker adoption.

REVIEW OF RELATED LITERATURE

Financial Marketing And Banking

The American Marketing Association (AMA) defines marketing as “the process of planning and executing the conception, pricing, promotion, and distribution of ideas, goods, and services to create exchanges that satisfy individual and organizational objectives.” Banks survive by creating and selling products and services that attract and satisfy clients in exchange for their value. In the banking industry, this approach is only profitable if the bank can produce the essential products and services. Marketing is supposed to maximize bank product and service usage. However, consumer satisfaction should be prioritized over consumption.

Virtual Banker

When considering the history of the technologies that have revolutionized banking, we find that the internet and data connectivity are constant. Connectivity between clients and servers ensures the safe, rapid, and abundant exchange of data. This prompted the sharing of information, and we can now have instant conversations using the fantastic chat program found on modern smartphones. Throughout the world, people are using instant messaging programs like WhatsApp, AI software, WeChat, Facebook Messenger, and so on. Our age is being revolutionized by these tools, as mentioned by Ugoani & Ugoani (2017).

A virtual banker is an AI-powered chatbot that simulates human bank tellers while interacting with customers. With virtual bankers, customers may use their preferred messaging apps to conduct banking transactions. It serves as a personal banker in one’s stead. One may use this chatbot to do a variety of banking-related tasks, including checking balances, making transfers, paying bills, and many more (Mogaji, Balakrishnan, Nwoba, and Nguyen, 2021).

In order to save their customers time and effort, virtual bankers give comprehensive information in the most user-friendly style feasible and speed up the processing of financial transactions.

Since chatbot apps provide real-time, context-aware, and tailored communication, customers can reach out to agents or chatbots through a centralized interface where their conversations are archived for future reference. This eliminates the need for them to waste time searching through different resources or waiting on hold to get in touch with a human for information they’ve already gathered (Börstler et al., 2023).

Quah and Chua (2019) posit that some financial institutions have already deployed the new technology, but many still lack the authentication to send sensitive customer data over mobile banking apps. Therefore, technologies that let banks verify their chat contacts in the same way that PINs help banks authenticate mobile banking app users are the future of virtual bankers.

The convenience of a virtual banker, however, lies in the fact that they may serve their clients no matter where they happen to be located. This will aid in establishing the foundation of trust necessary for maintaining long-term client-bank partnerships (Quah and Chua, 2019).

Perceived Usefulness

Burgess & Worthington (2021) state that Perceived usefulness is defined as the degree to which an individual believes that using a particular technology would be beneficial. As an individual’s perceived usefulness of a given technology increases, their intentions to use the technology also increase. People tend to accept new technologies with the assumption that doing so will improve their performance. Additionally, a large body of research in the information systems field shows that perceived usefulness has a major impact on usage intention.

Perceived Ease of Use

Burgess & Worthington (2021) defined Perceived ease of use as the degree to which an individual believes that using a particular technology would be free from effort. As an individual’s perceived ease of use of using a given technology increases, their intentions to use the technology also increase. Similar to perceived usefulness, perceived ease of use has lately been shown by numerous researchers to have a major impact on people’s behavioural intention to embrace a new system.

For instance, Andavara, Sundaram, Bacha, Dadi, and Karthika, (2021) discovered that perceived ease of use was one of the key factors influencing people’s decision to use online mobile payment services, followed by security and privacy and information on online payment website. It is anticipated that perceived ease of use will be a factor in the adoption of a virtual banker. Perceived ease of use is a useful construct in understanding people’s desire to use newer technologies.

THEORETICAL FRAMEWORK

Technology Acceptance Model (TAM)

In the hopes that it will enhance their business processes and boost their overall efficiency, businesses continue to make significant investments in information technology. However, for technologies to increase productivity, they need to be embraced by the users to whom they are designed Venkatesh, Morris, Davis and Davis (2003),. According to Venkatesh et al. (2003), research aimed at comprehending user acceptance of new technology has led to the development of multiple theoretical models, the origins of which may be found in information systems, psychology, and sociology.

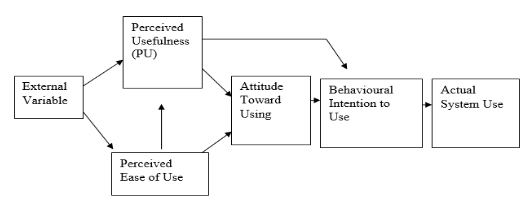

The purpose of this study is to investigate whether or not customers are willing to use virtual bankers, and it suggests using the technology acceptance model (TAM) to do so. TAM is one of the models that is applied the most when looking at the acceptability of information systems (Venkatesh and Davis,1996; Davis et al., 1989). The technology adoption model (TAM) utilizes two basic predictors for the potential adopter: the perceived usefulness (PU) of the technology and the perceived ease of use (PEOU) of the technology. These are the primary factors that determine an individual’s attitudes toward a new technology.

Perceived usefulness. This determinant demonstrates how people utilize or do not use an application according to the extent to which they find it useful for higher performance. PU is the degree to which a person believes that using a certain system will boost his or her job performance. However, this alone is not sufficient to decide whether or not a user will embrace the technology.

PU improves the user’s performance, but it does not guarantee a simple user experience; therefore, perceived ease of use is a vital factor to consider for simplicity of operation. PEOU is the degree to which an individual believes that making use of a specific system would require no effort at all (Davis, 1989). It is essential to strike a balance between the two factors to eliminate the risk of the benefits of utilization being outweighed by the difficulties associated with utilization. This suggests that the simplicity of the operation influences its usefulness.

Technology Acceptance Model, Tam (Davis, 1989).

Studies that employ the TAM often make use of one of these four distinct dependent variables. They are as follows: (a) the behavioural intention to use, (b) actual use, (c) acceptance, and (d) the intention to continue using.

According to Pikkarainen et al. (2004), the TAM has been subjected to numerous tests, and it has been discovered that its capacity to explain attitudes toward the use of information technology is superior to that of other models. According to Sharp (2007), the success of the TAM and its widespread utilization by researchers in the field of information systems can be attributed to the following three factors: (1) the TAM places a particular emphasis on information technology; (2) it is valid and reliable; and (3) the TAM has built up a research tradition.

According to Sumak, Polancic, and Hericko, (2010), one reason for the TAM’s widespread application in the field of information technology research is that it can be applied to the study of both pre- and post-adoption behavior.

Overview of Empirical Literature

Eren (2020) worked on determinants of customer satisfaction in chatbot use: evidence from a banking application in Turkey. The researcher investigated customer satisfaction from the use of bank chatbots and the effect of perceived trust in chatbots and banks’ reputation on customer satisfaction. A survey was conducted in Turkey involving 240 customers who experienced banking transactions using a chatbot. Partial least squares structural equation modelling (PLSSEM) was used to investigate the relationships between the variables. The data were analyzed using SPSS 21 and SmartPLS programs. The findings showed that perceived performance, perceived trust and corporate reputation significantly affect customer satisfaction with chatbot use. Customer expectations and confirmation of customer expectations have no direct impact on customer satisfaction, but customer expectations positively affect perceived performance. Customer expectations exert an indirect influence on customer satisfaction through perceived performance. Perceived performance has a positive impact on the confirmation of customer expectations, but customer expectations do not significantly impact the confirmation of customer expectations.

In Pakistani, Afshan, Sharif, Waseem & Frooghi (2018) investigated the framework of Internet banking with an expanded TAM model and the integration of extra risk variables. Through an online survey, 339 consumers’ information was gathered. The suggested framework was assessed using a technique called structural equation modelling. The study’s key influencing variables include structural assurance, individual trust inclination, and bank familiarity; these variables have an impact on consumers’ early trust in Pakistani Internet banking adoption. According to the authors, financial institutions should consider the research when developing their strategy for promoting Internet banking.

Chawla and Joshi (2018) used TAM and the Diffusion of Innovation (D.O.I.) Theory to empirically study the adoption of mobile banking and assess the moderating effects of demographic variables on consumer attitudes about this new form of banking in India. Age, gender, education, occupation, earnings, experience, and marital status are among the moderator factors. The information was gathered through a survey of 367 graduate and post-graduate students and focus groups with eight senior managers from the public sector. Multiple linear regression models and Fisher Z transformation were employed to examine the effects of moderating variables. The study’s findings demonstrate that educational background has no moderating influence on user attitude. All other variables are still significant, though.

Mogaji, Balakrishnan, Nwoba, Nguyen’s (2021) study in Nigeria was to position chatbots as a digital transformation tool to radically change business models, improve customer experience and enhance financial inclusion in emerging markets. The Search-Access-Test (S-A-T) model was adopted to understand how Nigerian banks are adopting chatbots. A majority of Nigerian banks now have chatbots that enhance customer engagement and financial inclusion. The findings show that Chatbots were often branded and presented with female gender identification. The chatbots were less responsive beyond their predefined path. While Nigeria is a multilingual country with English being the original language, none of the chatbots used any of the Nigerian’s local languages. There are also possibilities for branding the chatbot and developing content creation strategies for proper engagement.

Another study by Kumar, Lall, and Mane (2017) in India used the key TAM model components PEOU and PU, along with trust and social influence, to examine user intention and discovered that these variables had a positive, significant influence on mobile banking services. In Pakistan, Arif, Afshan and Sharif (2016) examined customer views and intentions about the acceptance and use of mobile banking. When risk concerns including security, privacy, time, and financial risk are present, modified TAM is utilized. The findings of the study demonstrated that PEOU and PU had a significant, favourable impact on the user’s perception of mobile banking. Furthermore, sentiments toward using the mobile banking service were negatively impacted by privacy and financial hazards.

RESEARCH METHOD

The study opted for a descriptive survey approach. The study employed a survey technique to collect data via questionnaire, explain, and make inferences from financial institution customer acceptance of new technologies and the rise of online banking in the Awka metropolis.

The population for this study consists of customers of specific banks in Awka City. The population number was unknown (infinite) because it is impossible to obtain the records of bank customers of these banks in this location; therefore, the questionnaire was delivered to the available individuals during the study period, and their responses were collected for the research.

Since the population of the study is infinite, the sample size was estimated using Topman’s formula for the unknown population. Its format is as follows:

![]()

Where n = Sample size

Z = Standard normal deviation at the confidence level of 95%, the degree of confidence selected for the study. For this research, it is 95% and the confidence level is 1.96

P = Proportion of the respondents assumed to respond positively to the questionnaire or the assumed percentage of success. In this research, it is 70%.

Q = Proportion of the respondents assumed to have a negative response to the questionnaire or the percentage failure rate. It is denoted by q = (1-p). This means that the q-value is 30%.

E = percentage of the level of significance (0.5%) or margin of error.

Applying the provisions above to the formula,

![]()

![]()

![]()

![]()

= 322.69

= 323.

= 323.

The sample size for the study is 323, and the respondents were chosen using a basic random selection procedure. This strategy gives each element or unit in the population the same chance of being chosen for the sample. It is seen to be appropriate, especially when the sample has a homogeneous feature.

The study concentrated on primary data gathered through the use of a standardized questionnaire. A structured questionnaire was used as the study instrument and utilized in collecting the necessary data from the respondents. It was divided into two sections: Section A collected demographic information from respondents, such as gender, marital status, and academic qualification. Section B provides some of the technological acceptance model’s factors, such as perceived utility, perceived ease of use, and actual adoption. The questionnaire was built using five-point Likert scale responses of Strongly Agreed (SA), Agree (A), Undecided (U), Disagreed (D), and Strongly Disagreed (SD) (SD). The following values were assigned to the five-point Likert scales: Strongly Agreed (5), Agree (4), Undecided (3), Disagreed (2), and Strongly Disagreed (2). (1). This study’s factors include perceived utility (Davis, 1989), perceived ease of use (Davis, 1989), and actual adoption (Ho and Ko 2008). Each variable has four items, however actual adoption has three variables. The questionnaire was pilot-tested on a sample of 20 respondents in Awka, Anambra State, at various critical locations. The respondents were chosen based on their familiarity with the research objectives, and they did not take part in the final study (Frazer & Lawley, 2000). After receiving feedback, revisions were made to the questionnaire’s wording, layout, sequencing techniques, and validity before the final copy was administered.

RESULTS AND DISCUSSION

Analysis of Research Questions

The retrieved questionnaires distributed were Three hundred and fifteen (315); representing approximately eighty (90) per cent success rate. The demographic information of the respondents is shown in the table below.

Table 1: Demographic profile of the respondents

| Characteristic | Frequency | Percentage | |

| Gender | Male | 135 | 42.9% |

| Female | 180 | 57.1% | |

| Age | Under 30 | 100 | 31.7% |

| 31-45 | 92 | 29.2% | |

| 45-55 | 65 | 20.6% | |

| 56-above | 58 | 18.4% | |

| Marital Status | Single | 130 | 41.3% |

| Married | 160 | 50.8% | |

| Divorced | 15 | 4.8% | |

| Others | 10 | 3.2% | |

| Highest Academic Qualification | WAEC/NECO/NABTEB | 30 | 9.5% |

| OND | 45 | 14.3% | |

| HND/B.Sc | 190 | 60.3% | |

| M.Sc | 35 | 11.1% | |

| P.hD | 15 | 4.8% | |

Source: Field Survey (2023)

According to Table 1, 42.9 per cent of those who participated in the study were males, whereas 57.1.1 per cent were females. 31.7 percent were under the age of 30, 42.9 percent were between the ages of 31 and 45, 20.6 percent were between the ages of 46 and 55, and 18.4 percent were beyond the age of 56. The marital status of the respondents revealed that 41.3 percent were single, 50.8 percent were married, 4.8 percent were divorced, and 3.2 percent were others. The respondents’ highest educational level revealed that the majority of them had a first degree, accounting for 60.3 percent. Master’s degree holders made up 11.1 percent of the total, while PhD holders made up 4.8 percent. OND holders made up 14.3 while those with Waec/Neco/Nabteb account for 9.5% percent of the population.

The reliability of the instrument was tested using Cronbach Alpha (α), which reveals how reliable the components of the questionnaire are.

Table 2: Reliability coefficient of instrument sub-scales

| N | Cronbach Alpha (α) | |

| Perceived usefulness | 4 | .761 |

| Perceived ease of use | 4 | .750 |

| Actual adoption | 3 | .744 |

The instrument is divided into sub-sections with each sub-section corresponding to a particular sub-scale. The Perceived usefulness subscale consisted of four items (α = .761), the Perceived ease of use subscale consisted of four items (α = .750), and the Actual adoption subscale consisted of three items (α = .744). Overall, the instrument was found to be highly reliable.

Descriptive Statistics

Table 3: Descriptive statistics Perceived usefulness

| Item | Scale | ||||||

| SA | A | UD | D | SD | Total | ||

| Perceived usefulness | Using a virtual banker in transactions enables me to accomplish more tasks quickly | 125(40%) | 131(41%) | 19(6%) | 30(10%) | 10(3%) | 315(100%) |

| Using a virtual banker will increase my experience and satisfaction | 135(43%) | 120(38%) | 10(3%) | 20(6%) | 30(10%) | 315(100%) | |

| A virtual banker will be useful to me as a bank customer | 150(48%) | 125(40%) | 10(3%) | 19(6%) | 10(3%) | 315(100%) | |

| Using a virtual banker will make it easy to attend to other dealings | 150(48%) | 115(36%) | 20(6%) | 10(3%) | 19(6%) | 315(100%) | |

According to the analysis above, 40% of respondents strongly agree that using virtual bankers enables them to complete their transaction tasks more quickly, 41% agree, 6% are undecided, 3% disagree, and 3% strongly disagree that using virtual bankers enables them to complete their tasks more quickly.

It was also revealed that 43% of respondents strongly believe that using virtual bankers will improve their banking experience and satisfaction, 38% agree, 3% are uncertain, 6% disagree, and 10% strongly disagree that using virtual bankers will improve their experience and satisfaction.

According to the findings, 48 percent of respondents highly believe that a Virtual banker will be valuable to them as a customer. 40% agree, 3% are undecided, 6% disagree, and 10% strongly disagree that Virtual banker will be valuable to me as a customer.

According to the results of the aforementioned analysis, 48% of respondents strongly agree that using a virtual banker will ease the stress associated with traditional banking. 36 percent agree, 6 percent are undecided, 3 percent disagree, and 6 percent strongly disagree that using a virtual banker will lessen the stress encountered in the banking hall.

Table 4: Descriptive statistics of Perceived ease of use

| Item | Scale | ||||||

| SA | A | UD | D | SD | Total | ||

| Perceived ease of use | Learning to operate a virtual banker will be easy for me | 139(44%) | 123(39%) | 10(3%) | 24(8%) | 19(6%) | 315(100%) |

| I would find it easy to get a virtual banker to do what I want it to do | 133(42%) | 129(41%) | 19(6%) | 10(3%) | 24(8%) | 315(100%) | |

| It would be easy for me to become skilful in using virtual banker | 131(41%) | 122(38%) | 20(6%) | 17(5%) | 25(8%) | 315(100%) | |

| I would find virtual banker easy to use | 125(40%) | 141(45%) | 10(3%) | 29(9%) | 10(3%) | 315(100%) | |

According to the results of the above analysis, 44% of respondents strongly agree that learning to operate a virtual banker will be simple for them, 39% agree, 3% are undecided, 8% disagree, and 6% strongly disagree that using a virtual banker will make my job easier.

According to the results of the aforementioned investigation, 42% of respondents strongly agree that it would be simple to get a virtual banker to perform what they want it to do. 41% agree, 6% are undecided, 3% disagree, and 8% strongly disagree that it would be easy to get a virtual banker to perform what I want it to do.

According to the research above, 41% of respondents strongly agree that it would be easy for them to become skilled in using virtual bankers, 38% agree, 6% are undecided, 5% disagree, and 8% strongly disagree that it would be easy for them to become skilled in using virtual bankers.

According to the results of the above analysis, 40% of respondents strongly agree that they would find virtual banking easy to use, 45% agree, 3% were undecided, 9% disagree, and 3% strongly disagree that it would be easy for them to get skilled in using virtual banker.

Table 5: Descriptive statistics of actual adoption

| Item | Scale | ||||||

| SA | A | UD | D | SD | Total | ||

| Actual adoption | I will adopt virtual banker as soon as possible | 141(45%) | 129(41%) | 15(5%) | 15(5%) | 15(5%) | 315(100%) |

| I intend to use virtual bankers in the future | 140(44%) | 122(39%) | 10(3%) | 24(8%) | 19(6%) | 315(100%) | |

| I will regularly use virtual bankers in the future | 133(42%) | 129(41%) | 19(6%) | 10(3%) | 24(8%) | 315(100%) | |

According to the aforementioned study, 45 percent of respondents strongly agree that they will adopt virtual bankers as soon as possible, 41 percent agree, 5% are uncertain, 5% disagree, and 5% strongly disagree that they will use virtual bankers as soon as possible.

According to the findings, 44% of respondents highly agree that they plan to utilize virtual bankers in the future, 39% agree, 3% are undecided, 8% disagree, and 6% severely disagree.

According to the findings, 42% of respondents strongly believe that they will utilize virtual bankers frequently in the future, 41% agree, 6% are undecided, 3% disagree, and 8% strongly disagree.

Test of Hypotheses

Hypothesis One:

Perceived usefulness will not have a positive and significant influence on virtual banker adoption.

: Perceived usefulness will have a positive and significant influence on virtual banker adoption.

Decision rule: Accept the null hypothesis when the probability value is greater than the alpha value, otherwise we reject it.

| ANOVA | ||||||

| Model | Sum of Squares | Df | Mean Square | F | Sig. | |

| 1 | Regression | 70.100 | 1 | 70.100 | .439 | .002a |

| Residual | 478.700 | 3 | 159.567 | |||

| Total | 548.800 | 4 | ||||

a. Predictors: (Constant), perceived usefulness

b. Dependent Variable: virtual banker adoption

| Coefficients | ||||||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | 87.861 | 42.113 | 2.086 | .008 | |

| Perceived usefulness | .499 | .753 | .357 | .663 | .000 | |

a. Dependent Variable: virtual bank adoption

Virtual bank adoption = 87.861 + 0.499 perceived usefulness.

This demonstrates that for every unit increase in perceived utility, virtual adoption rises by 0.499 percent.

Because the probability value (0.0021) is less than the alpha value (0.05) in the study above, the researcher accepts the alternative hypothesis and believes that perceived usefulness have a positive and significant influence on virtual banker adoption.

Hypothesis Two:

perceived ease of use will not have a positive and significant influence on virtual banker adoption.

perceived ease of use will have a positive and significant influence on virtual banker adoption.

| ANOVAb | ||||||

| Model | Sum of Squares | Df | Mean Square | F | Sig. | |

| 1 | Regression | 70.100 | 1 | 70.100 | .439 | .0001 |

| Residual | 478.700 | 3 | 159.567 | |||

| Total | 548.800 | 4 | ||||

| a. Predictors: (Constant), perceived ease | ||||||

| b. Dependent Variable: visual bank adoption | ||||||

| Coefficients | ||||||

| Model | Unstandardized Coefficients | Standardized Coefficients | t | Sig. | ||

| B | Std. Error | Beta | ||||

| 1 | (Constant) | 89.67 | 42.113 | 2.086 | .001 | |

| perceived ease | .3289 | .753 | .357 | .663 | .002 | |

| a. Dependent Variable: virtual bank adoption | ||||||

From the analysis above the model is given below

Virtual bank adoption = 89.67 + 0.3289 perceived ease of use.

This shows that for every unit increase in perceived ease of use, virtual bank adoption increases by 0.3289.

From the analysis above, it shows that the probability value (0.0011) is less than the alpha value (0.05), the researcher accepts the alternative hypothesis and concludes that Perceived ease of use have a positive and significant influence on virtual banker adoption.

CONCLUSION

In conclusion firstly, the result suggests that perceived usefulness has a positive influence on virtual banker adoption. This implies that when users perceive these systems as valuable tools that can enhance their banking experience, streamline their tasks, and provide meaningful assistance, they are more inclined to adopt them. Users are more likely to embrace virtual bankers when they see tangible benefits such as convenience, time-saving, improved access to information, and personalized recommendations. Therefore, a positive perception of the usefulness of virtual bankers significantly contributes to their adoption among users. It is evident that perceived usefulness plays a crucial role in driving the adoption of virtual bankers. Users’ perception of the value and practicality of virtual banking systems has a direct and positive impact on their willingness to adopt this technology.

Secondly, the result also suggests that perceived ease of use, have a positive and significant influence on virtual banker adoption. Perceive ease of use is a crucial factor in determining the adoption of virtual bankers. When users find these systems intuitive, simple to interact with, and understand their functions easily, they are more likely to embrace and use them. This positive perception of ease of use reduces the cognitive effort required for users to engage with virtual bankers, making the adoption process smoother and more appealing. As a result, it enhances the likelihood of users integrating virtual bankers into their daily financial activities.

The outcome of the results show that the Technology Acceptance Model is valid and fit to predict both consumer perception on the perceived usefulness on virtual banker adoption and perceived ease of use on virtual banker adoption, Marakarkandy, Yajnik, and Dasgupta, (2017)

This conclusion underscores the importance of designing and promoting virtual banking systems that prioritize user experience and functionality, as these elements are instrumental in gaining user acceptance and trust. As technology continues to advance, businesses and financial institutions must continue to recognize the significance of perceived usefulness and ease of use as pivotal factors in the successful implementation and widespread adoption of virtual bankers. It is imperative for future research and development efforts to focus on enhancing the perceived utility of such systems to encourage their continued growth and acceptance in the digital age .

RECOMMENDATION

Based on the findings of the hypotheses that accepts the alternative, indicating that perceived usefulness has a positive influence on virtual banker adoption and also perceived ease of use has a positive influence on virtual banker adoption. The following recommendations are proffered:

Financial institutions and businesses should invest in comprehensive user training and education programs to ensure that individuals fully understand the usefulness and benefits of virtual bankers. This can help improve perceived usefulness and increase adoption rates. Developers and providers of virtual banking systems should focus on continuously improving the features and functionalities of their virtual bankers. Regular updates and enhancements can make these systems more user-friendly and, thus, more useful to customers especially those not born in digital age. Financial institutions should transparently communicate the advantages of virtual bankers to these customers. Highlight how these systems can save time, offer convenience, and provide real value to users’ financial lives. It is of the essence for the institution to know that understanding changes in user expectations and preferences maintains high perceived usefulness and ease of use. These recommendations aim to help financial institutions and businesses leverage the positive influence of perceived usefulness on virtual banker adoption. By focusing on user-centric designs, continuous improvement, and clear communication of benefits, organizations can foster a more favourable environment for the adoption and utilization of virtual banking solutions.

Disclosure statement

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

REFERENCES

- Afshan, S., Sharif A., Waseem N. & Frooghi R. (2018) Internet banking in Pakistan: an extended technology acceptance perspective. International Journal of Business Information Systems, 27, 383-410.

- Andavara, V., Sundaram, B., Bacha, D., Dadi, T., & Karthika, P. (2021). The impact of perceived ease of use on intention to use mobile payment services for data security applications. Second International Conference on Electronics and Sustainable Communication Systems (ICESC) (pp. 1875-1880). IEEE.

- Arif, I., Afshan S. & Sharif A. (2016) Resistance to adopt mobile banking in a developing country: evidence from modified TAM model. Journal of Finance and Economics Research, 1, 23-38.

- Ayaz, A., Yanartaş, M. (2020): An analysis on the unified theory of acceptance and use of technology theory (UTAUT): Acceptance of electronic document management system (EDMS). Computers in Human Behavior Reports, Volume 2, 100032, ISSN 2451-9588.

- Bandura (1977). Self-efficacy: Toward a unifying theory of Behavioral Change. Psychological review. Vol.84, 2, 191-215

- Börstler J., Ali N., Svensson M., Petersen K., (2023). Investigating acceptance behavior in software engineering-Theoretical perspectives. Journal of Systems and Software, Vol. 198.

- Chawla, D. & H. Joshi (2018) The Moderating Effect of Demographic Variables on Mobile Banking Adoption: An Empirical Investigation. Global Business Review, 19, S90-S113.

- Davis, F.D. (1993), “User acceptance of information technology: system characteristics, user perceptions and behavioral impacts”, International Journal of Man-Machine Studies, Vol. 38, pp. 475-87.

- Davis, F.D. (1989) “Perceived usefulness, perceived ease of use, and user acceptance of information technology” Management Information System Quarterly, Vol.13, No.3, pp. 319-340.

- Davis, F.D., Bagozzi, R.P. and Warshaw, P.R. (1989), “User acceptance of computer technology: a comparison of two theoretical models”, Management Science, Vol. 35 No. 8, pp. 982-1003.

- Davis, F.D. and Venkatesh, V. (1996), “A critical assessment of potential measurement biases in the technology acceptance model: three experiments”, International Journal of Human-Computer Studies, Vol. 45, pp. 19-45.

- Eren B.A. (2020). Determinants of customer satisfaction in chatbot use: evidence from a banking application in Turkey. International Journal of Bank Marketing. Vol. 39 pp. 294-311.

- Kumar, V. R., Lall A. & Mane T. (2017) Extending the TAM Model: Intention of Management Students to Use Mobile Banking: Evidence from India. Global Business Review, 18, 238-249.

- Marakarkandy, B., Yajnik, N. & Dasgupta, C. (2017). Enabling internet banking adoption: An empirical examination with an augmented technology acceptance model (TAM). Journal of Enterprise Information Management, 30, 263-294.

- Mogaji E., Balakrishnan J., Nwoba A. C., Nguyen P. N. (2021). Emerging-market consumers’ interactions with banking chatbots. Telematics and Informatics, Volume 65, 101711, ISSN 0736-5853.

- Pikkarainen, T., Pikkarainen, K., Karjaluoto, H. and Pahnila, Seppo. (2004) “Consumer acceptance of online banking: an extension of the technology acceptance model”, Internet Research Vol. 14, No.3, pp. 224-235.

- Polančič, G., Heričko, M. and Rozman, I. (2010). An empirical examination of application frameworks success based on technology acceptance model”, Journal of Systems and Software, Vol. 83, pp. 514-584

- Prastiawan D.I., Aisjah S., & Rofiaty R., (2021) The Effect of Perceived Usefulness, Perceived Ease of Use, and Social Influence on the Use of Mobile Banking through the Mediation of Attitude Toward Use. Asia-Pacific Management and Business Application 9 (3) 243-260.

- Quah, J.T.S., and Chua, Y.W. (2019). “Chatbot assisted marketing in financial service industry,” in services computing –SCC 2019. Lecture Notes in Computer Science, eds J. Ferreira, A. Musaev, and L.J. Zhang (Cham: Springer), 107-114.

- Salawu R.O., Salawu M.K. (2007). The Emergence of Internet Banking in Nigeria: An Appraisal. Information Technology Journal 6: 490-469.

- Sharp, J.H. (2006): “Development, extension, and application: a review of the technology acceptance model.” Information Systems Education Journal, Vol. 5,9.

- Succi, M.J. and Walter, Z.D. (1999), “Theory of user acceptance of information technologies: an examination of health care professionals”, Proceedings of the 32nd Hawaii International Conference on System Sciences(HICSS), pp. 1-7.

- Sumak, B., Polancic, G., & Hericko, M. (2010). An Empirical Study of Virtual Learning Environment Adoption Using UTAUT. Paper presented at the 2010 Second Interna-tional Conference on Mobile, Hybrid, and On-Line Learning.

- Venkatesh V., Morris M.G, Davis G.B. and Davis F.D. User Acceptance of Information Technology: Toward a Unified View Quarterly, (2003), Management Information Systems Research Center. Vol 27, 3. pp. 425-478

- Triandis, H.C. (1980) Values, Attitudes, and Interpersonal Behavior. Nebraska Symposium on Motivation, University of Nebraska Press, Lincoln.

- Tulien L.W (1997) “Application of Information Technology” Being a Keynote Address on the Application of Information Technology on Financial Administration in Nigeria. MPRA Paper No. 16783

- Tsai M, Chin M., Chen C. (2010). The effect of trust belief and salesperson’s expertise on consumer’s intention to purchase nutraceuticals: Applying the theory of reasoned action. Social Behavior and Personality an International Journal

- Ugoani J.N.N., & Ugoani A. (2017). Information and Communication Technologies Management and Nigerian Banking Sector Liquidity. Independent Journal of Management & Production, 8(3).