Developing derivative-based hedging strategies to manage volatility in energy market prices

- Oluwole Oluwadamilola Agbede

- Experience Efeosa Akhigbe

- Ajibola Joshua Ajayi

- Nnaemeka Stanley Egbuhuzor

- 1651-1672

- Mar 6, 2025

- Business

Developing Derivative-Based Hedging Strategies to Manage Volatility in Energy Market Prices

1Oluwole Oluwadamilola Agbede, 1Experience Efeosa Akhigbe, 2Ajibola Joshua Ajayi, 3Nnaemeka Stanley Egbuhuzor

1Booth School of Business, University of Chicago, IL, USA

2The Wharton School of Business, University of Pennsylvania, PA, USA

3Columbia Business School, Columbia University, NY, USA

DOI: https://dx.doi.org/10.47772/IJRISS.2025.9020135

Received: 31 January 2025; Accepted: 05 February 2025; Published: 07 March 2025

ABSTRACT

The energy market is inherently volatile, driven by factors such as geopolitical events, supply-demand imbalances, and macroeconomic uncertainties. This volatility poses significant financial risks for market participants, including energy producers, consumers, and investors. Developing effective hedging strategies is critical to mitigating these risks and ensuring financial stability. Derivative-based hedging, using instruments such as futures, options, and swaps, offers a structured approach to manage price fluctuations in the energy market. This study explores the development and optimization of derivative-based hedging strategies tailored to address the complexities and dynamics of energy market volatility. The research begins by analyzing the fundamental drivers of price volatility in energy markets, including the impact of seasonal variations, geopolitical tensions, and technological advancements in renewable energy. It highlights the role of derivatives in providing price stability and enabling long-term planning for stakeholders. The study develops a framework that combines financial theory with quantitative modeling techniques to design hedging strategies aligned with varying risk appetites and market conditions. The framework incorporates tools such as Value at Risk (VaR), stress testing, and scenario analysis to assess the effectiveness of hedging instruments in diverse market scenarios. In addition, the research evaluates the performance of key derivative instruments, focusing on their suitability for managing specific types of energy risks, such as crude oil, natural gas, and electricity prices. The study leverages historical data and machine learning algorithms to predict price trends, enabling more informed decision-making in derivative transactions. Case studies from global energy markets are utilized to illustrate the practical application of these strategies and their potential to safeguard financial outcomes in turbulent conditions. The findings of this study underscore the importance of derivative-based hedging as a cornerstone of risk management in energy markets. It provides actionable insights for market participants, policymakers, and financial institutions to enhance market stability and resilience. By integrating advanced analytical techniques with robust hedging frameworks, this research contributes to the broader goal of achieving sustainable and efficient energy market operations amidst ongoing volatility.

Keywords: Energy Market Volatility, Derivatives, Hedging Strategies, Futures, Options, Swaps, Risk Management, Econometrics, Price Stability, Financial Instruments, Market Liquidity

INTRODUCTION

Energy markets are indeed characterized by significant price volatility, influenced by a myriad of factors including geopolitical tensions, supply and demand imbalances, technological advancements, and unpredictable weather patterns. The interplay of these elements creates a complex environment where price fluctuations can be abrupt and severe, posing substantial risks to various market participants such as energy producers, utilities, investors, and end-users (Alabi, et al., 2024, Toromade, et al., 2024, Udeh, et al., 2024). For instance, the volatility in oil prices has been shown to affect industrial production and economic stability, highlighting the broader implications of energy price dynamics on market participants’ revenue streams and operational costs (Elder, 2017; Arouri et al., 2012). Furthermore, the rapid transition towards renewable energy sources, while beneficial for sustainability, introduces additional uncertainties that can exacerbate market volatility (Safarzynska & Bergh, 2017).

The financial implications of this volatility are profound, as sudden price changes can disrupt financial stability and complicate budgeting processes for energy-related businesses. This is particularly critical for energy producers who must navigate the uncertainties to ensure the viability of long-term investments, such as renewable energy projects and infrastructure expansion (Londoño & Velásquez, 2023). Effective risk management strategies are essential for mitigating these financial impacts. By stabilizing cash flows and improving planning, these strategies help protect against adverse price movements, thereby enhancing the financial stability of both producers and consumers (Wing, 2015).

Derivative-based hedging has emerged as a vital tool in managing the risks associated with price volatility in energy markets. Instruments such as futures, options, swaps, and forward contracts allow market participants to lock in prices and cap their exposure to unfavorable price movements (Guo & Luo, 2017). This hedging capability not only secures predictable revenues for energy producers but also aids consumers in stabilizing their input costs, which is crucial for industries heavily reliant on energy (Arouri et al., 2011). Moreover, the role of derivatives extends to financial institutions and investors, enabling them to manage risks associated with energy-linked assets and portfolios effectively (Liu, 2021).

In conclusion, the development of derivative-based hedging strategies tailored to the unique dynamics of energy markets is critical for managing price volatility. By analyzing market conditions, evaluating hedging instruments, and applying quantitative methods, stakeholders can derive actionable insights to navigate the inherent risks of this volatile environment. Such robust risk management practices not only enhance individual financial stability but also contribute to the overall efficiency and resilience of energy markets, fostering confidence and facilitating sustainable growth across the sector (Jiang et al., 2018).

METHODOLOGY

A systematic approach was adopted to develop derivative-based hedging strategies for managing volatility in energy market prices. The Preferred Reporting Items for Systematic Reviews and Meta-Analyses (PRISMA) methodology was utilized to ensure a structured and transparent research process. The process began with defining the research objective, followed by a systematic literature search, selection, data extraction, and analysis.

A comprehensive literature search was conducted using electronic databases such as Scopus, Web of Science, and Google Scholar. The search included peer-reviewed journal articles, conference proceedings, and industry reports published between 2010 and 2024. The search terms included “energy market volatility,” “hedging strategies,” “financial derivatives,” “risk management,” and “commodity futures.” The Boolean operators AND and OR were used to refine the search results.

The screening process involved title and abstract screening, followed by a full-text review. The inclusion criteria were studies that focused on derivative-based hedging techniques such as futures contracts, options, and swaps applied to energy markets. Exclusion criteria included studies that did not discuss practical applications, those with insufficient methodological details, and papers unrelated to risk management in energy trading. Data extraction involved identifying key variables such as hedging instruments, risk measurement techniques, statistical models used, and market conditions under which hedging strategies were implemented. The extracted data were synthesized using a thematic analysis approach, categorizing findings based on their relevance to energy price volatility and risk mitigation.

The synthesized data were analyzed to determine the effectiveness of different hedging strategies. The analysis focused on comparing hedging performance across different energy commodities, evaluating the risk reduction potential of various derivative instruments, and identifying emerging trends in hedging practices. Statistical tools such as Value at Risk (VaR), Conditional Value at Risk (CVaR), and Monte Carlo simulations were used to assess the robustness of hedging techniques.

Findings from the systematic review informed the development of optimized hedging strategies. The proposed strategies were designed to mitigate price fluctuations by incorporating dynamic hedging models, AI-driven predictive analytics, and hybrid hedging approaches. The recommendations were based on empirical evidence and best practices identified in the literature.

A PRISMA flowchart was developed to illustrate the study selection process, detailing the number of records identified, screened, excluded, and included in the final analysis. The flowchart is structured in four main phases: identification, screening, eligibility, and inclusion, ensuring transparency and reproducibility of the systematic review. Figure 1 shows the PRISMA flowchart illustrating the study selection process for the systematic review on derivative-based hedging strategies in energy markets.

Figure 1: PRISMA Flow chart of the study methodology

Energy Market Volatility: Causes and Impacts

Energy market volatility refers to the fluctuations in the prices of energy commodities, such as oil, natural gas, coal, and electricity, which are subject to significant and often unpredictable changes. These fluctuations are driven by a variety of factors, both internal and external, that create uncertainty and risk for stakeholders in the energy sector. Understanding the causes and impacts of energy market volatility is crucial for developing effective risk management strategies, including derivative-based hedging, to mitigate the financial risks associated with price movements (Avwioroko, et al., 2024, Bristol-Alagbariya, Ayanponle & Ogedengbe, 2024).

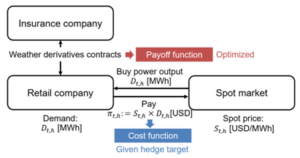

One of the primary drivers of energy market volatility is geopolitical tensions. Energy markets are deeply interconnected with global politics, and events such as armed conflicts, sanctions, and trade disputes can have significant effects on the supply and demand of energy commodities. For instance, conflicts in oil-producing regions like the Middle East often disrupt production and transportation, leading to sudden increases in oil prices due to fears of supply shortages. Similarly, political instability in countries that are major exporters of natural gas or coal can create uncertainty in global energy markets, leading to fluctuations in prices as traders react to potential disruptions. Geopolitical tensions can also result in changes in government policies that affect energy production, consumption, and trade, further contributing to price volatility (Onukwulu, Agho & Eyo-Udo, 2023, Tula, et al., 2023). Matsumoto & Yamada, 2021, presented Simple market model for a retail company as shown in figure 2.

Figure 2: Simple market model for a retail company (Matsumoto & Yamada, 2021).

Supply-demand imbalances are another critical driver of energy market volatility. Energy prices are largely determined by the relationship between supply and demand, and when this balance is disrupted, prices can experience sharp movements. For example, if a major energy producer experiences a decline in production due to weather-related events, technical failures, or operational disruptions, the reduced supply can drive up prices if demand remains steady or increases (Alabi, et al., 2024, Oyewole, et al., 2024, Shoetan, et al., 2024). Conversely, when energy producers ramp up production in response to higher prices, oversupply can lead to a price crash. Additionally, seasonal demand patterns, such as higher heating and cooling requirements during winter and summer months, can further exacerbate volatility as supply struggles to meet peak demand. These fluctuations often create challenges for energy stakeholders in forecasting prices and planning for future needs (Oyewole, et al., 2024, Patrick, Sule, et al., 2024, Uwumiro, et al., 2024).

Macroeconomic factors also play a significant role in energy market volatility. Global economic growth, inflation, and currency fluctuations all affect energy prices. For instance, during periods of robust economic expansion, demand for energy tends to increase as industries ramp up production and transportation needs rise. This heightened demand can push energy prices higher, particularly if supply cannot keep pace. On the other hand, economic recessions tend to dampen energy demand, leading to lower prices as consumption drops (Alex-Omiogbemi, et al., 2024, Soremekun, et al., 2024, Toromade & Chiekezie, 2024). Additionally, fluctuations in exchange rates can affect the cost of importing and exporting energy commodities, further contributing to price volatility. For example, a weakening of the U.S. dollar often leads to higher oil prices, as commodities priced in dollars become more expensive for foreign buyers. These macroeconomic influences add layers of complexity to the energy market, making price movements harder to predict and increasing the risks for stakeholders.

Technological advancements in renewables have introduced both opportunities and challenges that contribute to energy market volatility. As renewable energy sources, such as wind, solar, and hydroelectric power, become more integrated into the global energy mix, their impact on market prices has increased. While the growth of renewables is seen as a positive step toward reducing reliance on fossil fuels and mitigating climate change, the intermittent nature of renewable energy generation can introduce new uncertainties into the market. For example, solar and wind energy production is dependent on weather conditions and time of day, leading to fluctuations in supply that may not always align with consumer demand (Avwioroko, 2023, Onukwulu, Agho & Eyo-Udo, 2023, Popo-Olaniyan, et al., 2024). This intermittency creates challenges for grid operators and increases the volatility of energy prices, particularly in regions with a high penetration of renewables. In some cases, the integration of renewable energy into the grid requires backup power sources, often from fossil fuel-based plants, which can further complicate price dynamics. Moreover, technological innovations that reduce the cost of renewable energy technologies may alter market conditions by shifting the energy supply curve, potentially displacing traditional energy sources and creating price instability (Avwioroko & Ibegbulam, 2024, Sam-Bulya, et al., 2024, Uwumiro, et al., 2024).

The effects of energy market volatility are felt across a wide range of stakeholders, each of whom faces unique financial and operational risks. Producers, consumers, and investors are all directly impacted by the price fluctuations that characterize energy markets. For energy producers, volatility presents both opportunities and risks. On the one hand, rising energy prices can lead to higher revenues, especially for producers with large reserves of oil, natural gas, or coal (Attah, Ogunsola & Garba, 2022). On the other hand, sharp declines in prices can significantly reduce profits, particularly for companies with high production costs or those that are unable to quickly adjust to changing market conditions. Additionally, geopolitical instability and supply-demand imbalances can create uncertainties about the future viability of energy projects, leading to delays, cancellations, or changes in investment strategies.

For consumers, volatility can lead to unpredictable energy costs, particularly for industries that rely heavily on energy inputs, such as manufacturing, transportation, and utilities. Energy price spikes can increase operational costs, which may be passed on to consumers in the form of higher prices for goods and services. For households, fluctuations in electricity and fuel prices can strain budgets, especially for low-income families who spend a higher proportion of their income on energy. As a result, energy price volatility can have far-reaching economic consequences, affecting inflation rates, cost-of-living adjustments, and overall economic stability (Anjorin, et al., 2024, Oyewole, et al., 2024, Usman, et al., 2024).

Investors in the energy sector are also exposed to the risks of price volatility. Investment decisions in energy assets, such as oil and gas reserves, renewable energy projects, and energy infrastructure, are often based on the expectation of stable or predictable price movements. Volatile energy prices can disrupt these expectations, leading to financial losses or missed opportunities. Moreover, the growing importance of environmental, social, and governance (ESG) factors in investment decisions has added a layer of complexity to energy market investments (Onukwulu, Agho & Eyo-Udo, 2022, Oyegbade, et al., 2022). As stakeholders demand more sustainable and socially responsible energy practices, investments in traditional fossil fuel-based assets may become less attractive, further contributing to market uncertainty.

The financial and operational risks posed by energy market volatility can be effectively managed through the use of derivative-based hedging strategies. Derivatives such as futures, options, and swaps allow market participants to lock in prices or mitigate the impact of price fluctuations. For producers, hedging strategies provide a way to secure future revenues and protect against adverse price movements. For consumers, derivatives offer a mechanism to stabilize energy costs and reduce the risk of price shocks (Ajayi, Toromade & Olagoke, 2024, Udo, Toromade & Chiekezie, 2024). Investors can also use derivatives to manage their exposure to energy price volatility, diversifying their portfolios and minimizing financial risk. By utilizing these tools, stakeholders can navigate the uncertainties of energy markets with greater confidence, ensuring financial stability and facilitating long-term planning. Transaction model of electricity and derivatives presented by Yamada & Matsumoto, 2021, is shown in figure 3.

![]()

Figure 3: Transaction model of electricity and derivatives (Yamada & Matsumoto, 2021).

In conclusion, energy market volatility is driven by a range of factors, including geopolitical tensions, supply-demand imbalances, macroeconomic conditions, and technological advancements in renewables. These fluctuations have significant financial and operational impacts on energy producers, consumers, and investors, creating risks that require effective risk management strategies (Asogwa, Onyekwelu & Azubike, 2023, Onukwulu, Agho & Eyo-Udo, 2023, Uwaoma, et al., 2023). Developing derivative-based hedging strategies is a key approach to mitigating these risks, enabling stakeholders to protect against price volatility and enhance financial stability. As the energy market continues to evolve, understanding the causes and effects of price volatility will remain essential for ensuring a stable and sustainable energy future.

Overview of Derivative Instruments

Derivative instruments are essential financial tools used to manage and mitigate risk, especially in volatile markets like energy. These instruments allow market participants—such as energy producers, consumers, investors, and traders—to hedge against price fluctuations, ensure financial stability, and enhance decision-making capabilities. In the context of energy markets, which are inherently volatile due to factors such as geopolitical tensions, supply-demand imbalances, and macroeconomic shifts, derivative instruments provide valuable mechanisms for managing financial exposure to energy price movements (Al Hasan, Matthew & Toriola, 2024, Solanke, et al., 2024). Futures, options, swaps, and forward contracts are the primary derivative instruments used in energy markets. Each of these tools has unique characteristics and applications, depending on the specific needs of market participants.

Futures contracts are one of the most widely used derivative instruments in the energy markets. These contracts represent an agreement to buy or sell an underlying asset, such as oil, natural gas, or electricity, at a predetermined price on a specified future date. Futures contracts are standardized and traded on exchanges, providing liquidity and transparency (Oyewole, et al., 2024, Paul, et al., 2024, Popo-Olaniyan, et al., 2024). Energy producers and consumers use futures contracts to lock in future prices for energy commodities, thereby mitigating the risk of price fluctuations. For example, an oil producer may use a futures contract to hedge against a potential decline in oil prices, while a utility company might use futures to secure a stable price for purchasing electricity in the future. Futures contracts are particularly advantageous because they are highly liquid and can be easily traded or offset before the contract’s expiration. However, futures require margin accounts and daily settlement, which can introduce risks related to funding requirements and margin calls. Feng, et al., 2024, presented the construction path of China’s electricity financial market system as shown in figure 4.

Figure 4: The construction path of China’s electricity financial market system (Feng, et al., 2024).

Options contracts, another popular derivative instrument, provide the right, but not the obligation, to buy or sell an underlying asset at a predetermined price before or on a specified date. Options are widely used in energy markets due to their flexibility and risk-limiting characteristics. A call option gives the buyer the right to purchase the underlying asset, while a put option gives the buyer the right to sell it (Alex-Omiogbemi, et al., 2024, Soremekun, et al., 2024, Toromade, et al., 2024). Energy market participants use options to hedge against unfavorable price movements while retaining the potential to benefit from favorable price changes. For instance, an oil refinery might purchase a call option on crude oil to protect against rising prices while still benefiting from a potential decline in oil prices. The main advantage of options is that they allow the buyer to limit their downside risk to the premium paid for the option, while offering the potential for substantial upside gains. However, options also come with their own risks, including the potential loss of the premium if the price does not move favorably by the expiration date.

Swaps are another key type of derivative used to manage risk in energy markets. A swap is a private agreement between two parties to exchange cash flows or other financial instruments based on the value of an underlying asset or index. In the context of energy markets, the most common type of swap is a commodity swap, in which one party agrees to pay a fixed price for an energy commodity, while the other party pays a floating price based on market conditions. Swaps are typically customized contracts negotiated between two parties, rather than standardized contracts traded on exchanges (Alabi, et al., 2024, Ukpohor, Adebayo & Dienagha, 2024). This makes them more flexible but also less liquid. Swaps are primarily used by energy producers and consumers to stabilize cash flows and protect against adverse price movements. For example, an energy company might enter into a swap agreement to receive a fixed price for natural gas while paying the market price, ensuring a predictable revenue stream even if market prices fluctuate. The main advantage of swaps is that they allow for more tailored risk management, as they can be customized to meet the specific needs of the parties involved. However, swaps also carry counterparty risk, as the performance of the contract depends on the financial stability of the counterparties.

Forward contracts are similar to futures contracts but are privately negotiated and not traded on exchanges. A forward contract is an agreement between two parties to buy or sell an asset, such as an energy commodity, at a predetermined price on a future date. Unlike futures, which are standardized, forward contracts are customizable and can be tailored to the specific needs of the participants (Avwioroko, 2023, Onukwulu, Agho & Eyo-Udo, 2023, Uwaoma, et al., 2023). These contracts are used by energy producers, consumers, and traders to hedge against price movements in energy markets. For instance, an electricity generator may enter into a forward contract to sell electricity at a fixed price in the future, providing financial stability even if market prices fluctuate. Forward contracts are commonly used by companies with specific delivery or purchasing requirements that need a customized solution. However, they also carry significant risks, particularly in terms of counterparty default risk, as these contracts are typically not subject to the oversight and regulations of an exchange.

When comparing these derivative instruments, it is important to recognize their respective strengths and weaknesses in the context of energy markets. Futures contracts offer high liquidity, transparency, and standardization, making them suitable for hedging large volumes of energy commodities. However, their standardized nature and daily margin requirements can make them less flexible compared to other instruments like forwards or swaps (Apeh, et al., 2024, Onyekwelu & Nnabugwu, 2024, Raji, et al., 2024). Options provide flexibility and limited downside risk, which makes them appealing for hedging against price fluctuations while retaining the opportunity to profit from favorable price movements. However, options come with upfront costs in the form of premiums, and the buyer may lose the premium if the market does not move as expected.

Swaps, on the other hand, are highly customizable, making them ideal for managing more complex risk exposures in energy markets. They allow participants to lock in fixed prices over longer time periods, providing predictability in cash flows. However, swaps are less liquid than futures and are subject to counterparty risk, as they are private agreements between two parties. Forward contracts share many of the same benefits and drawbacks as swaps, offering customization but also carrying the risk of default by the counterparty (Alao, et al., 2024, Onyekwelu & Nnabugwu, 2024, Paul, Ogugua & Eyo-Udo, 2024). Each derivative instrument can be more or less appropriate depending on the specific needs and circumstances of the market participants. For large energy producers and consumers who need to hedge substantial exposure to price fluctuations, futures contracts may provide the most efficient way to manage risk. For smaller entities or those with more specific risk management needs, options or swaps may offer more flexibility and tailored solutions. For market participants who have long-term, customized risk exposures, forward contracts and swaps are likely to be the most effective tools.

In conclusion, derivative-based hedging strategies are indispensable tools for managing volatility in energy market prices. Futures, options, swaps, and forward contracts each offer distinct advantages and trade-offs, with varying degrees of flexibility, liquidity, and risk. The choice of instrument depends on the specific needs of the market participant, including their risk appetite, the scale of their exposure, and the desired level of customization. By understanding the characteristics and applications of these derivative instruments, stakeholders in energy markets can better navigate price fluctuations, stabilize cash flows, and protect against the financial risks inherent in volatile energy markets (Onukwulu, et al., 2021, Onyekwelu, et al., 2018). These hedging strategies provide a robust framework for mitigating risk, promoting stability, and ensuring financial predictability in an otherwise uncertain energy landscape.

Framework for Developing Hedging Strategies

In managing the volatility of energy market prices, the development of effective derivative-based hedging strategies requires a clear understanding of risk profiles, financial objectives, and the specific market conditions in which a business or investor operates. Hedging is a critical risk management tool, used to protect against price fluctuations that can result from geopolitical instability, shifts in supply and demand, or macroeconomic factors (Onyekwelu & Oyeogubalu, 2020, Onyekwelu, et al., 2021). However, to maximize the effectiveness of hedging strategies, stakeholders must carefully design their approaches, taking into account the nature of the risks they face, the timing of their hedging needs, and the inherent costs and complexities of the financial instruments involved.

The first step in developing a hedging strategy is identifying the risk profiles and financial objectives of the market participants. There are two primary motives for using derivatives: speculation and hedging. Speculation involves taking positions in financial instruments with the aim of profiting from price movements. In contrast, hedging is a protective measure used to offset or minimize potential losses caused by unfavorable price fluctuations. Understanding the difference between these motives is crucial in determining the appropriate strategy for a given situation (Onyekwelu, 2020). Hedging is typically employed by companies and investors seeking to stabilize their cash flows or protect their balance sheets from unexpected price changes, while speculative strategies are often used by traders aiming to profit from market volatility.

For energy producers and consumers, such as oil companies, utilities, and large industrial players, the primary objective is often to mitigate risk and ensure stable pricing for future transactions. For example, an oil refinery may use hedging strategies to lock in a fixed price for crude oil, thus reducing the uncertainty around its input costs. The key here is to identify the specific risks that need to be managed—whether they relate to changes in energy prices, supply chain disruptions, or foreign exchange fluctuations—and design a hedging strategy that aligns with the company’s financial goals (Onyekwelu & Azubike, 2022). The objective is not necessarily to profit from market movements, but rather to reduce the potential for negative financial impacts.

Once the risk profile is established, the next step is to design a tailored hedging strategy that meets the specific needs of the participant. Hedging strategies can be broadly classified into short-term and long-term approaches, depending on the time horizon of the exposure and the nature of the risks being hedged. Short-term hedging strategies are typically used to manage price volatility in the near term and are often associated with contracts that have shorter maturities, such as futures or options (Onyekwelu & Ibeto, 2020, Onyekwelu, 2020). These strategies are particularly useful for companies or traders that face immediate price risk due to seasonal fluctuations, supply disruptions, or short-term market movements. For instance, an energy company with a large amount of short-term power sales can hedge the risk of fluctuating electricity prices by using short-term futures contracts.

On the other hand, long-term hedging strategies are used to address risks that span a more extended period, such as changes in global energy supply and demand trends, geopolitical risks, or regulatory shifts that may influence energy prices over several years. Long-term hedging can involve more customized instruments, such as swaps or forward contracts, which allow participants to lock in prices or cash flows for longer periods. For example, a natural gas producer might enter into a multi-year forward contract to ensure stable pricing over the life of a project or a large energy infrastructure investment (Ajayi, Toromade & Olagoke, 2024, Onyekwelu, et al., 2024, Toromade, et al., 2024). These strategies provide certainty regarding future revenues, but they also carry the risk of being locked into less favorable prices if market conditions improve.

When designing a hedging strategy, it is essential to consider several key factors that can influence the effectiveness of the hedging approach. Market conditions are one of the most critical considerations. The state of the energy markets—whether they are experiencing a bull or bear market, periods of high volatility, or relative price stability—can significantly impact the choice of hedging instruments (Anekwe, Onyekwelu & Akaegbobi, 2021, , Onyekwelu & Chinwe, 2020). During periods of high volatility, participants may seek to hedge more aggressively to protect against sharp price movements. In contrast, in more stable periods, participants may adopt a more relaxed hedging strategy, possibly using options to maintain flexibility while reducing hedging costs.

Transaction costs are another important consideration when developing a hedging strategy. These costs include the fees associated with executing the hedge, such as brokerage fees, spread costs, margin requirements, and the premiums paid for options contracts. Transaction costs can erode the financial benefits of hedging, especially in low-margin industries such as energy production (Attah, Ogunsola & Garba, 2023). Econometric models and market analysis are often used to quantify the potential impact of transaction costs on the overall effectiveness of hedging strategies. For instance, if transaction costs are high relative to the volatility of the underlying commodity, a company may decide to hedge less aggressively or seek alternative hedging instruments with lower costs.

Liquidity and counterparty risk also play a crucial role in the design of hedging strategies. Liquidity refers to the ability to buy and sell contracts in the market without causing significant price changes, and it is particularly important in futures and options markets. High liquidity ensures that participants can enter and exit positions quickly and efficiently, which is essential for minimizing the impact of price fluctuations. In contrast, illiquid markets can lead to wider bid-ask spreads, slippage, and difficulties in unwinding positions, all of which add costs to the hedging strategy.

Counterparty risk, on the other hand, refers to the risk that the other party involved in a derivative contract may default on its obligations. In over-the-counter (OTC) markets, where instruments such as swaps and forward contracts are negotiated privately, counterparty risk is particularly high (Akinmoju, et al., 2024, Raji, et al., 2024, Udeh, et al., 2024). To mitigate this risk, companies often require collateral or engage in credit assessments before entering into contracts. Clearinghouses and centralized exchanges help reduce counterparty risk in standardized contracts like futures and options by acting as intermediaries between buyers and sellers, but this added layer of protection comes with additional costs, such as margin requirements. Companies must carefully evaluate their risk tolerance and choose derivatives that align with their counterparty risk preferences.

When determining the specific instruments to use for hedging, market participants must weigh the advantages and disadvantages of various derivative products. Futures contracts, for example, offer a high level of liquidity and standardization, making them suitable for hedging short-term price risk in liquid markets (Alex-Omiogbemi, et al., 2024, Popo-Olaniyan, et al., 2024). They are widely used in energy markets, particularly for crude oil, natural gas, and electricity, and are ideal for hedging standardized exposures. However, futures contracts require margin accounts and daily settlement, which can lead to liquidity challenges in times of market stress.

Options contracts provide greater flexibility than futures by offering the right, but not the obligation, to execute a transaction at a predetermined price. This flexibility is especially valuable in volatile markets, as it allows hedgers to benefit from favorable price movements while limiting losses in the event of adverse price changes. However, options come with premiums, and their effectiveness is influenced by factors such as time decay and volatility.

Swaps and forward contracts are often more suitable for managing longer-term exposures and customized risks. Swaps allow participants to exchange cash flows based on an underlying asset’s price, providing a tailored solution for hedging price fluctuations over extended periods (Anjorin, et al., 2024, Sam-Bulya, et al., 2024, Toromade & Chiekezie, 2024). Similarly, forward contracts are privately negotiated and offer the ability to lock in prices for specific future dates. These instruments are particularly useful for businesses with long-term energy procurement or production needs, but they also carry counterparty risk and may require more sophisticated management.

In conclusion, developing effective derivative-based hedging strategies to manage volatility in energy market prices requires a comprehensive approach that takes into account risk profiles, financial objectives, market conditions, and transaction costs. The choice of hedging instruments—whether futures, options, swaps, or forward contracts—depends on the time horizon, liquidity preferences, and specific risks faced by market participants. A well-designed hedging strategy can protect businesses and investors from adverse price movements, stabilize cash flows, and support long-term financial stability (Oyewole, et al., 2024, Patrick, Toromade, Chiekezie & Udo, 2024). By carefully considering the relevant factors and tailoring their strategies to meet specific needs, stakeholders can effectively navigate the uncertainties of energy markets and capitalize on the benefits of hedging.

Quantitative Models for Hedging Strategy Development

The development of derivative-based hedging strategies to manage volatility in energy markets requires a strong quantitative framework that can accurately measure, predict, and mitigate the risks associated with price fluctuations. As energy markets are subject to high levels of volatility, driven by a variety of factors such as geopolitical events, weather patterns, technological advancements, and macroeconomic trends, quantifying the risk exposure and evaluating the effectiveness of hedging strategies becomes essential for stakeholders (Paul, Ogugua & Eyo-Udo, 2024, Soremekun, et al., 2024, Ugochukwu, et al., 2024). Various quantitative models, including Value at Risk (VaR), Conditional VaR, stress testing, scenario analysis, and predictive modeling, provide the tools needed to design, implement, and assess hedging strategies in these volatile markets.

One of the primary tools used for quantifying risk in derivative-based hedging strategies is Value at Risk (VaR). VaR is a statistical method used to measure the potential loss in the value of a portfolio over a specified time horizon, given a certain confidence level. It quantifies the maximum expected loss that a portfolio could experience, providing a clear and concise metric for risk. In energy markets, VaR is widely used to assess the potential losses that might arise from fluctuations in energy prices (Onyekwelu & Uchenna, 2020, Onyekwelu, 2017). For example, energy companies that hold large portfolios of futures and options contracts can use VaR to determine the maximum loss they could incur due to price movements in oil, gas, or electricity markets. The main advantage of VaR is its simplicity and ease of interpretation, as it provides a single, quantifiable measure of risk.

However, VaR has limitations, particularly in capturing extreme events or tail risks. To address this, Conditional VaR (CVaR) or Expected Shortfall (ES) is often used. CVaR measures the expected loss given that the loss has exceeded the VaR threshold, focusing on the tail end of the distribution. This is particularly important in energy markets, where extreme events such as geopolitical crises, natural disasters, or sudden market shocks can cause significant price fluctuations (Onyekwelu & Uchenna, 2020, Onyekwelu, 2017). By considering the risk of extreme losses, CVaR provides a more comprehensive measure of potential downside risk and helps market participants design more robust hedging strategies that can withstand rare but highly impactful events.

Stress testing and scenario analysis are also crucial quantitative techniques used to evaluate the potential impact of extreme price movements or changes in market conditions. Stress testing involves simulating hypothetical scenarios in which energy prices experience significant shocks, such as a sharp increase in oil prices due to geopolitical tensions or a dramatic fall in natural gas prices due to oversupply (Onukwulu, Agho & Eyo-Udo, 2023, Onyekwelu, et al., 2023). By applying these scenarios to a hedging portfolio, market participants can assess how their hedging strategies would perform under extreme conditions and identify potential vulnerabilities. Stress testing is essential for understanding the potential risks associated with extreme market conditions that might not be captured by regular market volatility.

Scenario analysis, on the other hand, involves the evaluation of different possible future outcomes based on changes in key market variables. This method allows stakeholders to explore a range of possibilities and understand how various scenarios—such as changes in demand, supply disruptions, or shifts in regulatory policy—could impact energy prices and the effectiveness of hedging strategies. Scenario analysis is often used in combination with other models, such as VaR and CVaR, to provide a more comprehensive view of risk and to test the resilience of hedging strategies across multiple possible futures (Chike & Onyekwelu, 2022, Onyekwelu, Chike & Anene, 2022).

Predictive modeling plays a critical role in forecasting energy price movements and informing the design of hedging strategies. Machine learning and time-series analysis are two powerful approaches that can be used to predict future price trends, providing valuable insights for hedging decisions. Machine learning techniques, such as regression analysis, neural networks, and decision trees, can be applied to large datasets containing historical price movements, supply-demand patterns, geopolitical factors, and other relevant variables (Avwioroko, 2023, Osunbor, et al., 2023, Uwaoma, et al., 2023). These models can learn from past data to identify complex relationships and patterns in energy prices, enabling more accurate price forecasts. For example, machine learning algorithms can predict short-term fluctuations in crude oil prices based on macroeconomic indicators and geopolitical developments, allowing market participants to adjust their hedging strategies accordingly.

Time-series analysis is another valuable tool for predicting energy price movements. Time-series models, such as autoregressive integrated moving average (ARIMA) models, vector autoregression (VAR) models, and GARCH (Generalized Autoregressive Conditional Heteroskedasticity) models, are designed to analyze and forecast the behavior of price series over time. These models take into account historical price data and account for autocorrelation (the correlation of current values with past values) and volatility clustering (the tendency for high volatility periods to be followed by more volatility) (Alonge, Dudu & Alao, 2024, Osundare & Ige, 2024, Raji, et al., 2024). Time-series analysis is particularly useful for forecasting energy prices in the short to medium term, as it can capture trends, cycles, and seasonal patterns inherent in energy markets, such as the impact of weather patterns on natural gas demand or the seasonal fluctuations in electricity prices.

Once a hedging strategy has been developed using these quantitative models, it is essential to evaluate its performance to determine its effectiveness and value. Hedging effectiveness can be measured using several metrics, including the hedging effectiveness ratio and cost-benefit analysis. The hedging effectiveness ratio compares the changes in the value of a hedging portfolio to the changes in the underlying exposure, quantifying how well the hedge offsets the fluctuations in the underlying asset (Ajayi, Toromade & Olagoke, 2024, Toromade & Chiekezie, 2024). A higher ratio indicates a more effective hedge, meaning that the derivative instruments have successfully mitigated the risk of price movements. For example, if a company has used options contracts to hedge against fluctuations in oil prices, the hedging effectiveness ratio will measure how well the options have protected the company from adverse price changes in oil.

Cost-benefit analysis is another important metric for assessing the performance of hedging strategies. This analysis compares the costs associated with implementing a hedge—such as premiums paid for options or margin requirements for futures contracts—to the financial benefits gained from reducing price volatility and stabilizing cash flows. In energy markets, where transaction costs can be significant, cost-benefit analysis helps market participants determine whether the protection provided by hedging justifies the associated expenses (Onyekwelu, Monyei & Muogbo, 2022). For example, a utility company may evaluate whether the cost of hedging against fluctuations in electricity prices is worth the stability it provides in terms of more predictable financial outcomes.

Finally, examining case studies from global energy markets provides valuable real-world examples of how these quantitative models and metrics are applied in practice. In the crude oil market, companies such as ExxonMobil and Shell use derivatives to hedge against price fluctuations and secure stable cash flows (Alex-Omiogbemi, et al., 2024, Shittu, et al., 2024). These companies often employ a combination of futures, swaps, and options to protect their revenues from the volatility of oil prices, particularly in times of geopolitical instability or supply disruptions. For example, during the 2020 oil price crash due to the COVID-19 pandemic and OPEC production cuts, many oil producers used hedging strategies to mitigate the impact of falling prices and maintain financial stability.

In the natural gas market, utilities and traders use similar strategies to manage exposure to price volatility, particularly in markets where natural gas prices are highly sensitive to seasonal demand and supply conditions. For instance, U.S. natural gas producers have increasingly used swaps and options to hedge against price fluctuations caused by changes in weather patterns or production levels (Onyekwelu, et al., Peace, et al., 2022, Oyegbade, et al., 2022). During periods of extreme cold or hot weather, demand for natural gas can spike, driving prices higher. Hedge strategies allow these producers to lock in more favorable prices and reduce the financial risks associated with weather-related volatility.

In the electricity market, energy suppliers and large consumers such as manufacturing companies use derivatives to manage the volatility of electricity prices. Electricity prices are influenced by a range of factors, including fuel costs, demand fluctuations, and transmission constraints. By using forward contracts or options, these participants can lock in fixed prices or cap their exposure to price spikes. For example, in the European electricity market, utilities have used hedging strategies to mitigate the risks associated with fluctuating prices due to variable renewable energy output, which can cause grid imbalances and price volatility (Apeh, et al., 2024, Oyewole, et al., 2024).

In conclusion, quantitative models play an essential role in the development of derivative-based hedging strategies for managing volatility in energy markets. Techniques such as VaR, stress testing, scenario analysis, predictive modeling, and performance evaluation metrics help market participants understand their risk exposure and design more effective hedging strategies (Attah, Ogunsola & Garba, 2023, Uwumiro, et al., 2023). By applying these models and evaluating their performance, stakeholders can enhance their risk management practices and ensure greater financial stability in the face of price fluctuations. Real-world case studies from crude oil, natural gas, and electricity markets demonstrate the practical applications of these strategies, underscoring the importance of using quantitative tools to navigate the complexities of energy price volatility.

Challenges in Implementing Derivative-Based Hedging

Implementing derivative-based hedging strategies to manage volatility in energy markets is crucial for reducing financial risk and ensuring stability in a sector that is often subject to significant price fluctuations. However, despite the advantages these strategies offer, there are several challenges involved in their effective implementation. These challenges range from regulatory considerations and market liquidity constraints to the integration of renewable energy sources, counterparty risks, and the broader policy and institutional implications (Alabi, et al., 2024, Orieno, et al., 2024, Sule, et al., 2024). Understanding and addressing these challenges is vital for stakeholders who rely on hedging instruments to navigate the inherent uncertainties of the energy market.

Regulatory considerations are one of the most significant hurdles in implementing derivative-based hedging strategies in energy markets. Over the years, the energy sector has been subject to a variety of regulations, many of which have evolved in response to concerns about market manipulation, transparency, and financial stability. Hedging strategies often involve complex financial instruments, and the regulatory landscape governing their use can be intricate and, at times, restrictive. In some markets, particularly those involving futures and options, regulations require reporting of positions, margining, and compliance with trading rules set by exchanges or regulatory bodies (Anozie, et al., 2024, Orieno, et al., 2024, Popo-Olaniyan, et al., 2024). This can create significant challenges for businesses that want to implement hedging strategies without facing burdensome compliance costs or limitations.

For instance, regulations introduced after the 2008 global financial crisis, such as the Dodd-Frank Act in the United States, mandated stricter oversight of derivatives trading and required certain derivative contracts to be cleared through central counterparties. While these measures were designed to reduce systemic risk, they also increased operational complexity for participants in the energy markets (Bristol-Alagbariya, Ayanponle & Ogedengbe, 2024, Raji, et al., 2024, Udeh, et al., 2024). The need to comply with such regulations can limit the flexibility with which market participants can execute hedging strategies and potentially raise the cost of utilizing derivatives, as businesses may need to dedicate resources to ensure compliance with reporting and risk management requirements. Additionally, regulatory changes can lead to sudden shifts in market behavior, with new rules potentially altering the effectiveness of existing hedging strategies.

Another challenge in implementing derivative-based hedging strategies is market liquidity constraints. Liquidity is essential for the efficient functioning of any financial market, and it is particularly important in energy markets where price fluctuations can be sudden and large. In illiquid markets, participants may face difficulties in entering or exiting positions, leading to increased transaction costs and potentially wider bid-ask spreads. Energy markets can experience periods of low liquidity, especially for less frequently traded commodities or in smaller regional markets (Alabi, et al., 2024, Oriekhoe, et al., 2024, Oyewole, et al., 2024). This lack of liquidity can make it more difficult for market participants to hedge their exposures, as it may be harder to find counterparties willing to take the opposite side of a trade or to execute large hedging transactions without moving prices unfavorably.

For example, while futures contracts on widely traded commodities like crude oil or natural gas generally benefit from high liquidity, less liquid markets for electricity, carbon credits, or renewable energy certificates may present greater challenges. Participants in these markets may face difficulties in obtaining the desired level of hedging coverage or be forced to accept higher transaction costs, thus reducing the overall effectiveness of their hedging strategies. This challenge is compounded when market participants lack access to exchanges or platforms with sufficient depth to accommodate large positions (Paul, Ogugua & Eyo-Udo, 2024, Sule, et al., 2024, Uwumiro, et al., 2024). These liquidity constraints often force businesses to rely on over-the-counter (OTC) derivatives, which can carry additional risks related to counterparty exposure and less transparency.

The integration of renewable energy sources into traditional energy grids also presents significant challenges for derivative-based hedging. Renewable energy sources such as wind and solar are highly variable and dependent on weather conditions, making them more difficult to predict and manage from a financial perspective. As the share of renewables in global energy markets increases, the volatility in energy prices becomes more pronounced, adding complexity to the design of effective hedging strategies (Akinrinola, et al., 2024, Oriekhoe, et al., 2024, Raji, et al., 2024). Market participants who rely on traditional energy commodities, such as coal or natural gas, may find it more challenging to hedge against price fluctuations that are influenced by renewable energy generation. For instance, periods of high solar or wind generation can lead to lower electricity prices, while periods of low renewable output may drive prices up. This increased volatility can undermine the effectiveness of standard hedging tools, which are typically designed for more predictable supply conditions.

Moreover, renewable energy generation is often decentralized, with numerous small-scale producers contributing to the overall supply. This can further complicate the design and implementation of hedging strategies, as the underlying market dynamics become more fragmented and difficult to forecast. The challenge is not only about hedging energy prices but also about accommodating the new market structures that come with renewable energy integration (Avwioroko, 2023, Oriekhoe, et al., 2023). Hedging strategies in such a context require more sophisticated models that account for both the intermittency of renewable generation and the changing nature of energy consumption patterns.

Counterparty and credit risks are another significant concern when implementing derivative-based hedging strategies. In derivatives markets, especially those involving OTC instruments like swaps and forward contracts, participants face the risk that their counterparty may default on its obligations. While exchanges mitigate counterparty risk through clearinghouses, OTC derivatives do not have the same level of protection. The energy market is particularly exposed to these risks because of its complex and sometimes opaque nature, with participants often engaging in large, customized transactions (Alex-Omiogbemi, et al., 2024, Oriekhoe, et al., 2024, Ugwuoke, et al., 2024). During times of market stress, such as during financial crises or periods of extreme price volatility, the likelihood of counterparty defaults increases, which can undermine the effectiveness of hedging strategies.

Energy companies and traders must carefully assess the creditworthiness of their counterparties before entering into hedging agreements. This includes evaluating the financial stability of the counterparties and their ability to fulfill their obligations. However, even with such precautions, the risk of default remains a real concern, particularly in less regulated markets or in regions with weaker financial systems. To mitigate this risk, market participants often use collateral agreements or buy insurance, but these additional steps come at a cost and may not fully eliminate the possibility of counterparty default (Arinze, et al., 2024, Oriekhoe, et al., 2024, Oyewole, et al., 2024).

From a broader policy and institutional perspective, policymakers play a crucial role in supporting derivative-based hedging practices in energy markets. Governments and regulators must strike a balance between ensuring market transparency, stability, and fairness while providing participants with the flexibility to manage their risk exposures. This involves designing regulatory frameworks that support the use of derivatives for hedging purposes while preventing abuse or excessive speculation (Onyekwelu, Arinze & Chukwuma, 2015, Oyegbade, et al., 2021). Effective regulation can help increase market participation, build confidence, and facilitate the development of more sophisticated financial instruments for energy market participants.

Building market stability and resilience is another important objective for policymakers. Given the volatility of energy markets, particularly in light of shifting demand patterns, regulatory changes, and the growing integration of renewables, policymakers must promote stability in market conditions that will allow hedging strategies to be effective. This may include creating mechanisms for improving market liquidity, providing incentives for infrastructure development, and supporting the establishment of transparent and reliable pricing benchmarks (Onyekwelu, Ogechukwuand & Shallom, 2021, Oyeniyi, et al., 2021). Moreover, encouraging participation from diverse stakeholders—including producers, consumers, financial institutions, and governments—can help ensure that the benefits of hedging strategies are broadly distributed and that market risks are effectively shared across the economy.

Finally, the role of policymakers also includes fostering market innovation and ensuring that financial markets remain adaptable in the face of changing energy market dynamics. This could involve supporting the development of new hedging instruments tailored to the specific needs of renewable energy markets or facilitating the expansion of financial products that address the unique characteristics of energy price volatility (Chike & Onyekwelu, 2022, Onyekwelu, Patrick & Nwabuike, 2022). Governments can also encourage the use of renewable energy derivatives to provide participants with the tools they need to hedge against the price risks associated with renewable energy generation and consumption.

In conclusion, implementing derivative-based hedging strategies to manage volatility in energy markets presents several challenges, including regulatory considerations, market liquidity constraints, uncertainty in renewable energy integration, and counterparty risks. Despite these challenges, policymakers can play a critical role in supporting hedging practices by ensuring stable market conditions, encouraging diverse participation, and promoting market innovation (Alonge, Dudu & Alao, 2024, Schuver, et al., 2024, Toromade, et al., 2024). By addressing these challenges through targeted regulation and policy frameworks, energy markets can become more resilient, enabling businesses and investors to effectively manage price volatility and support long-term financial stability.

CONCLUSION

In conclusion, developing derivative-based hedging strategies to manage volatility in energy market prices is an essential component of effective risk management in a sector characterized by significant price fluctuations. The analysis of various hedging instruments, such as futures, options, swaps, and forward contracts, has shown that these tools offer valuable means for mitigating the financial risks associated with price movements. Hedging strategies allow market participants, including energy producers, consumers, and investors, to stabilize their cash flows, protect revenues, and reduce the uncertainty that accompanies volatile energy prices.

Derivative-based hedging is particularly crucial for maintaining market stability. By enabling participants to lock in prices or manage their exposure to price movements, these instruments help ensure smoother financial operations, reduce the likelihood of price shocks, and promote confidence in the market. Hedging strategies create a more predictable environment, which benefits not only individual businesses but also the broader energy market. This stability is essential for long-term planning, investment decisions, and the overall growth of the energy sector.

While significant strides have been made in the application of hedging strategies, there are still challenges to address. These include regulatory concerns, market liquidity, counterparty risks, and the complexities arising from the integration of renewable energy sources into traditional energy systems. Overcoming these challenges requires a collaborative effort between policymakers, financial institutions, and energy market participants to create a conducive environment for efficient hedging practices.

Looking to the future, research on derivative-based hedging strategies should focus on improving the design of instruments tailored to the evolving dynamics of energy markets, particularly with the increasing prominence of renewable energy. Further advancements in predictive modeling, stress testing, and scenario analysis will be crucial in enhancing the accuracy and robustness of hedging strategies. Additionally, the development of new financial products and regulatory frameworks that accommodate the unique challenges of energy markets will play a key role in facilitating broader participation and expanding the application of derivative-based risk management techniques.

In summary, derivative-based hedging remains a cornerstone for managing price volatility in energy markets. By continuously improving these strategies and addressing the challenges they face, stakeholders can ensure a more resilient and stable energy market that is better equipped to navigate the uncertainties of the future.

REFERENCES

- Ajayi, O. O., Toromade, A. S., & Olagoke, A. (2024). Data-Driven Agropreneurship (DDA): Empowering Farmers through Predictive Analytics.

- Ajayi, O. O., Toromade, A. S., & Olagoke, A. (2024): Circular agro-economies (CAE): reducing waste and increasing profitability in agriculture.

- Ajayi, O. O., Toromade, A. S., & Olagoke, A. (2024): Precision Agro-Economic Modeling (PAM): A New Approach to Optimizing Input-Output Ratios.

- Akinmoju, O. D., Olatunji, G., Kokori, E., Ogieuhi, I. J., Babalola, A. E., Obi, E. S., … & Aderinto, N. (2024). Comparative Efficacy of Continuous Positive Airway Pressure and Antihypertensive Medications in Obstructive Sleep Apnea-Related Hypertension: A Narrative Review. High Blood Pressure & Cardiovascular Prevention, 1-11.

- Akinrinola, O., Okoye, C. C., Ofodile, O. C., & Ugochukwu, C. E. (2024). Navigating and reviewing ethical dilemmas in AI development: Strategies for transparency, fairness, and accountability. GSC Advanced Research and Reviews, 18(3), 050-058.

- Al Hasan, S. M., Matthew, K. A., & Toriola, A. T. (2024). Education and mammographic breast density. Breast Cancer Research and Treatment, 1-8.

- Alab, O. A., Ajayi, F. A., Udeh, C. A., & Efunniyi, C. P. (2024). Leveraging Data Analytics to Enhance Workforce Efficiency and Customer Service in HR-Driven Organizations. International Journal of Research and Scientific Innovation, 11(9), 92-101.

- Alabi, O. A., Ajayi, F. A., Udeh, C. A., & Efunniyi, C. P. (2024). Data-driven employee engagement: A pathway to superior customer service. World Journal of Advanced Research and Reviews, 23(3).

- Alabi, O. A., Ajayi, F. A., Udeh, C. A., & Efunniyi, C. P. (2024). Optimizing Customer Service through Workforce Analytics: The Role of HR in Data-Driven Decision-Making. International Journal of Research and Scientific Innovation, 11(8), 1628-1639.

- Alabi, O. A., Ajayi, F. A., Udeh, C. A., & Efunniyi, C. P. (2024). The impact of workforce analytics on HR strategies for customer service excellence. World Journal of Advanced Research and Reviews, 23(3).

- Alabi, O. A., Ajayi, F. A., Udeh, C. A., & Efunniyi, F. P. (2024). Predictive Analytics in Human Resources: Enhancing Workforce Planning and Customer Experience. International Journal of Research and Scientific Innovation, 11(9), 149-158.

- Alao, O. B., Dudu, O. F., Alonge, E. O., & Eze, C. E. (2024). Automation in financial reporting: A conceptual framework for efficiency and accuracy in US corporations. Global Journal of Advanced Research and Reviews, 2(02), 040-050.

- Alex-Omiogbemi, A. A., Sule, A. K., Michael, B., & Omowole, S. J. O. (2024): Advances in AI and FinTech Applications for Transforming Risk Management Frameworks in Banking.

- Alex-Omiogbemi, A. A., Sule, A. K., Omowole, B. M., & Owoade, S. J. (2024): Advances in cybersecurity strategies for financial institutions: A focus on combating E-Channel fraud in the Digital era.

- Alex-Omiogbemi, A. A., Sule, A. K., Omowole, B. M., & Owoade, S. J. (2024): Conceptual framework for optimizing client relationship management to enhance financial inclusion in developing economies.

- Alex-Omiogbemi, A. A., Sule, A. K., Omowole, B. M., & Owoade, S. J. (2024). Conceptual framework for advancing regulatory compliance and risk management in emerging markets through digital innovation.

- Alex-Omiogbemi, A. A., Sule, A. K., Omowole, B. M., & Owoade, S. J. (2024). Conceptual framework for women in compliance: Bridging gender gaps and driving innovation in financial risk management.

- Alonge, E. O., Dudu, O. F., & Alao, O. B. (2024). The impact of digital transformation on financial reporting and accountability in emerging markets. International Journal of Science and Technology Research Archive, 7(2), 025-049.

- Alonge, E. O., Dudu, O. F., & Alao, O. B. (2024). Utilizing advanced data analytics to boost revenue growth and operational efficiency in technology firms.

- Anekwe, E., Onyekwelu, O., & Akaegbobi, A. (2021). Digital transformation and business sustainability of telecommunication firms in Lagos State, Nigeria. IOSR Journal of Economics and Finance, 12(3), 10-15. International Organization of Scientific Research.

- Anjorin, K. F., Ijomah, T. I., Toromade, A. S., & Akinsulire, A. A. (2024). Framework for developing entrepreneurial business models: Theory and practical application. Global Journal of Research in Science and Technology, 2(1), 13-28.

- Anjorin, K., Ijomah, T., Toromade, A., Akinsulire, A., & Eyo-Udo, N. (2024). Evaluating business development services’ role in enhancing SME resilience to economic shocks. Global Journal of Research in Science and Technology, 2(01), 029-045.

- Anozie, U. C., Adewumi, G., Obafunsho, O. E., Toromade, A. S., & Olaluwoye, O. S. (2024). Leveraging advanced technologies in Supply Chain Risk Management (SCRM) to mitigate healthcare disruptions: A comprehensive review. World Journal of Advanced Research and Reviews, 23(1), 1039-1045.

- Apeh, C. E., Odionu, C. S., Bristol-Alagbariya, B., Okon, R., & Austin-Gabriel, B. (2024). Advancing workforce analytics and big data for decision-making: Insights from HR and pharmaceutical supply chain management. International Journal of Multidisciplinary Research and Growth Evaluation 5(1), 1217-1222. DOI: https://doi.org/10.54660/.IJMRGE.2024.5.1.1217-1222

- Apeh, C. E., Odionu, C. S., Bristol-Alagbariya, B., Okon, R., & Austin-Gabriel, B. (2024). Reviewing healthcare supply chain management: Strategies for enhancing efficiency and resilience. International Journal of Research and Scientific Innovation (IJRSI), 5(1), 1209-1216. DOI: https://doi.org/ 10.54660/.IJMRGE.2024.5.1.1209-1216

- Arinze, C. A., Ajala, O. A., Okoye, C. C., Ofodile, O. C., & Daraojimba, A. I. (2024). Evaluating the integration of advanced IT solutions for emission reduction in the oil and gas sector. Engineering Science & Technology Journal, 5(3), 639-652.

- Arouri, M., Jouini, J., & Nguyen, D. (2011). Volatility spillovers between oil prices and stock sector returns: implications for portfolio management. Journal of International Money and Finance, 30(7), 1387-1405. https://doi.org/10.1016/j.jimonfin.2011.07.008

- Arouri, M., Lahiani, A., Levy, A., & Nguyen, D. (2012). Forecasting the conditional volatility of oil spot and futures prices with structural breaks and long memory models. Energy Economics, 34(1), 283-293. https://doi.org/10.1016/j.eneco.2011.10.015

- Asogwa, O. S., Onyekwelu, N. P., & Azubike, N. U. (2023). Effects of security challenges on business sustainability of SMEs in Nigeria. International Journal Of Business And Management Research, 3(2).

- Attah, R.U., Ogunsola, O.Y, & Garba, B.M.P. (2022). The Future of Energy and Technology Management: Innovations, Data-Driven Insights, and Smart Solutions Development. International Journal of Science and Technology Research Archive, 2022, 03(02), 281-296.

- Attah, R.U., Ogunsola, O.Y, & Garba, B.M.P. (2023). Advances in Sustainable Business Strategies: Energy Efficiency, Digital Innovation, and Net-Zero Corporate Transformation. Iconic Research And Engineering Journals Volume 6 Issue 7 2023 Page 450-469.

- Attah, R.U., Ogunsola, O.Y, & Garba, B.M.P. (2023). Leadership in the Digital Age: Emerging Trends in Business Strategy, Innovation, and Technology Integration. Iconic Research And Engineering Journals Volume 6 Issue 9 2023 Page 389-411.

- Avwioroko, A. (2023). Biomass Gasification for Hydrogen Production. Engineering Science & Technology Journal, 4(2), 56-70.

- Avwioroko, A. (2023). The integration of smart grid technology with carbon credit trading systems: Benefits, challenges, and future directions. Engineering Science & Technology Journal, 4(2), 33–45.

- Avwioroko, A. (2023). The potential, barriers, and strategies to upscale renewable energy adoption in developing countries: Nigeria as a case study. Engineering Science & Technology Journal, 4(2), 46–55.

- Avwioroko, A., & Ibegbulam, C. (2024). Contribution of Consulting Firms to Renewable Energy Adoption. International Journal of Physical Sciences Research, 8(1), 17-27.

- Avwioroko, A., Ibegbulam, C., Afriyie, I., & Fesomade, A. T. (2024). Smart Grid Integration of Solar and Biomass Energy Sources. European Journal of Computer Science and Information Technology, 12(3), 1-14.

- Avwioroko, Afor. (2023). Biomass Gasification for Hydrogen Production. Engineering Science & Technology Journal. 4. 56-70. 10.51594/estj.v4i2.1289.

- Bristol-Alagbariya, B., Ayanponle, L. O., & Ogedengbe, D. E. (2024). Sustainable business expansion: HR strategies and frameworks for supporting growth and stability. International Journal of Management & Entrepreneurship Research, 6(12), 3871–3882. Fair East Publishers.

- Bristol-Alagbariya, B., Ayanponle, O. L., & Ogedengbe, D. E. (2022). Integrative HR approaches in mergers and acquisitions ensuring seamless organizational synergies. Magna Scientia Advanced Research and Reviews, 6(01), 078–085. Magna Scientia Advanced Research and Reviews.

- Elder, J. (2017). Oil price volatility: industrial production and special aggregates. Macroeconomic Dynamics, 22(3), 640-653. https://doi.org/ 10.1017/ s136510051600047x

- Feng, H., Zhang, Y., Lan, Z., Wang, K., Wang, Y., Chen, S., & Feng, C. (2024). Developing China’s Electricity Financial Market: Strategic Design of Financial Derivatives for Risk Management and Market Stability. Energies, 17(23), 5854.

- Guo, Z. and Luo, Y. (2017). Dynamic stochastic factors, risk management and the energy futures. International Business Research, 10(9), 50. https://doi.org/10.5539/ibr.v10n9p50

- Jiang, Y., Yang, X., & Ren, Y. (2018). Time-varying volatility feedback of energy prices: evidence from crude oil, petroleum products, and natural gas using a tvp-svm model. Sustainability, 10(12), 4705. https://doi.org/10.3390/su10124705

- Liu, Y. (2021). Global transmission of returns among financial, traditional energy, renewable energy and carbon markets: new evidence. Energies, 14(21), 7286. https://doi.org/10.3390/en14217286

- Londoño, A. and Velásquez, J. (2023). Risk management in electricity markets: dominant topics and research trends. Risks, 11(7), 116. https://doi.org/ 10.3390/risks11070116

- Matsumoto, T., & Yamada, Y. (2021). Simultaneous hedging strategy for price and volume risks in electricity businesses using energy and weather derivatives. Energy Economics, 95, 105101.

- Onukwulu, E. C., Agho, M. O., & Eyo-Udo, N. L. (2022). Circular economy models for sustainable resource management in energy supply chains. World Journal of Advanced Science and Technology, 2(2), 034-057. https://doi.org/10.53346/wjast.2022.2.2.0048

- Onukwulu, E. C., Agho, M. O., & Eyo-Udo, N. L. (2023). Decentralized energy supply chain networks using blockchain and IoT. International Journal of Scholarly Research in Multidisciplinary Studies, 2(2), 066 085. https://doi.org/10.56781/ijsrms.2023.2.2.0055

- Onukwulu, E. C., Agho, M. O., & Eyo-Udo, N. L. (2023). Developing a Framework for AI-Driven Optimization of Supply Chains in Energy Sector. Global Journal of Advanced Research and Reviews, 1(2), 82-101. https://doi.org/10.58175/gjarr.2023.1.2.0064

- Onukwulu, E. C., Agho, M. O., & Eyo-Udo, N. L. (2023). Developing a Framework for Supply Chain Resilience in Renewable Energy Operations. Global Journal of Research in Science and Technology, 1(2), 1-18. https://doi.org/10.58175/gjrst.2023.1.2.0048

- Onukwulu, E. C., Agho, M. O., & Eyo-Udo, N. L. (2023). Developing a framework for predictive analytics in mitigating energy supply chain risks. International Journal of Scholarly Research and Reviews, 2(2), 135-155. https://doi.org/10.56781/ijsrr.2023.2.2.0042

- Onukwulu, E. C., Agho, M. O., & Eyo-Udo, N. L. (2023). Sustainable Supply Chain Practices to Reduce Carbon Footprint in Oil and Gas. Global Journal of Research in Multidisciplinary Studies, 1(2), 24-43. https://doi.org/10.58175/gjrms.2023.1.2.0044

- Onukwulu, N. E. C., Agho, N. M. O., & Eyo-Udo, N. N. L. (2021). Advances in smart warehousing solutions for optimizing energy sector supply chains. Open Access Research Journal of Multidisciplinary Studies, 2(1), 139-157. https://doi.org/10.53022/oarjms.2021.2.1.0045

- Onyekwelu, C. A. (2017). Effect of reward and performance management on employee productivity: A study of selected large organizations in South East of Nigeria. International Journal of Business & Management Sciences, 3(8), 39–57. International Journal of Business & Management Sciences.

- Onyekwelu, N. P. (2019). Effect of organization culture on employee performance in selected manufacturing firms in Anambra State. International Journal of Research Development, 11(1). International Journal of Research Development.

- Onyekwelu, N. P. (2020). External environmental factor and organizational productivity in selected firms in Port Harcourt. International Journal of Trend in Scientific Research and Development, 4(3), 564–570. International Journal of Trend in Scientific Research and Development.

- Onyekwelu, N. P., & Ibeto, M. U. (2020). Extra-marital behaviours and family instability among married people in education zones in Anambra State.

- Onyekwelu, N. P., & Nnabugwu, O. C. (2024). Organisational Dexterity and Effectiveness of Commercial Banks in Awka, Anambra State, Nigeria. International Journal of Business and Management Research, 5(1), 54-79.

- Onyekwelu, N. P., & Nnabugwu, O. C. (2024). Workplace Spirituality And Employee Productivity Of Manufacturing Firms In Anambra State. Crowther Journal Of Arts And Humanities, 1(2).

- Onyekwelu, N. P., & Oyeogubalu, O. N. (2020). Entrepreneurship Development and Employment Generation: A Micro, Small and Medium Enterprises Perspective in Nigeria. International Journal of Contemporary Applied Researches, 7(5), 26-40.

- Onyekwelu, N. P., & Uchenna, I. M. (2020). Teachers’ Perception of Teaching Family Life Education in Public Secondary Schools in Anambra State.

- Onyekwelu, N. P., Arinze, A. S., Chidi, O. F., & Chukwuma, E. D. (2018). The effect of teamwork on employee performance: A study of medium scale industries in Anambra State. International Journal of Contemporary Applied Researches, 5(2), 174-194.

- Onyekwelu, N. P., Chike, N. K., & Anene, O. P. (2022). Perceived Organizational Prestige and Employee Retention in Microfinance Banks in Anambra State.

- Onyekwelu, N. P., Ezeafulukwe, C., Owolabi, O. R., Asuzu, O. F., Bello, B. G., & Onyekwelu, S. C. (2024). Ethics and corporate social responsibility in HR: A comprehensive review of policies and practices. International Journal of Science and Research Archive, 11(1), 1294-1303.

- Onyekwelu, N. P., Monyei, E. F., & Muogbo, U. S. (2022). Flexible work arrangements and workplace productivity: Examining the nexus. International Journal of Financial, Accounting, and Management, 4(3), 303-314.

- Onyekwelu, N. P., Nnabugwu, O. C., Monyei, E. F., & Nwalia, N. J. (2021). Social media: a requisite for the attainment of business sustainability. IOSR Journal of Business and Management, 23(07), 47-52.

- Onyekwelu, N. P., Okoro, O. A., Nwaise, N. D., & Monyei, E. F. (2022). Waste management and public health: An analysis of Nigerias healthcare sector. Journal of Public Health and Epidemiology, 14(2), 116-121.

- Onyekwelu, N., & Chinwe, N. O. (2020). Effect of cashless economy on the performance of micro, small and medium scale enterprises in Anambra State, Nigeria. International Journal of Science and Research, 9(5), 375-385.

- Onyekwelu, O. S. A. N. P., & Azubike, N. U. (2022). Effects Of Security Challenges On Business Sustainability Of Smes In Nigeria.

- Onyekwelu, P. N. (2020). Effects of strategic management on organizational performance in manufacturing firms in south-east Nigeria. Asian Journal of Economics, Business and Accounting, 15(2), 24-31.

- Onyekwelu, P. N., Arinze, A. S., & Chukwuma, E. D. (2015). Effect of reward and performance management on employee productivity: A study of selected large organizations in the South-East, of Nigeria. EPH-International Journal of Business & Management Science, 1(2), 23-34.