Effect of Audit Quality on Financial Performance of Quoted Conglomerates in Nigeria

- Chibunna Onyebuchi Onwubiko

- Henry Arinze Nwankwo

- 316-336

- May 10, 2024

- Accounting & Finance

Effect of Audit Quality on Financial Performance of Quoted Conglomerates in Nigeria

Chibunna Onyebuchi Onwubiko, Henry Arinze Nwankwo

Department of Accounting, Faculty of Economics and Management Sciences, Abia State University, Uturu, Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2024.803021S

Received: 26 March 2024; Revised: 05 April 2024; Accepted: 09 April 2024; Published: 10 May 2024

ABSTRACT

This study was embarked on to ascertain the effect of audit quality on financial performance of quoted conglomerates in Nigeria. The study specifically investigates the effect of audit size, fee and tenure on return on asset of selected conglomerates in Nigeria. Purposive sampling technique was used to select the conglomerates in the study. The study involves a time series data between 2011-2021 involving 12 years. Data was excerpted from their financial summaries. The study adopted Ordinary least square regression technique, and also applied econometric estimations such as Augmented Dickey Fuller (ADF) and Johanson Cointegration tests. The study therefore concludes that audit tenure affects a propensity to disclose key audit matters. However, audit size and fee are not strong drivers of financial performance. The Study recommends that organisations should ensure credibility and transparency in audit; this will enhance the quality of audit report. There must be willingness of management to communicate with the auditor while also enlarging the audit size to improve audit reports and minimize the adverse impact on the company, the management should make the auditor more aware of the intended disclosure and the company’s position and communicate with the auditor more actively.

INTRODUCTION

Background to the study

Audit quality is defined as the market-estimated joint likelihood that a specific auditor would both detect and disclose a violation in the client’s accounting system (Kaoje and Mohammed, 2022). From the foregoing, there are numerous criteria and elements that have been found to influence audit quality. Audit fees, audit firm rotation, audit committee oversight, audit firm size, and the Auditor’s personal attributes, such as competence, independence, qualification, and experience, are all revealed (Kaoje, Babangida, and Kaoje, 2022). These criteria appear to be linked, as the larger the audit company, the higher the audit fees, competence, audit plan, independence, qualification, and experience, all of which contribute to the quality of the audit and the likelihood of a truthful and fair assessment of the financial statements being audited (Ugwunta, Ugwuanyi and Ngwa, 2018).

The credibility and value derived from assurance services by auditors are grounded in the foundation of auditors’ independence, both mind and in appearance. In recent years, the issues associated with the internal auditors’ independence and objectivity began to become of great interest to researchers (Adeleke, 2021). Audit quality has been viewed as being very fundamental to the auditor’s job and profession because, without it, audited financial statements would not have value in the perception of the end-users (Gana, Mohd and Peter, 2020). The quality of an audit is also expected to contribute to the improvement of efficiency and effectiveness of the management in financial management thereby contributing to the growth of organizational performance and maximization of shareholders wealth.

Audit is a critical component of financial stability and the re-establishment of trust and market confidence (Egiyi, 2022). When there are concerns regarding the accuracy of a company’s financial statement, we may look to the auditor’s report for answers. As a result, the financial reports’ credibility is predicated on the notion that the certified auditor is not influenced by their customers or other entities. The auditors’ independence is one of the issues that always surface in the audit quality debate. Audit fees, which mirror the billing rates of the entire audit team and are charged by an audit firm or eventually paid by the client for audit services, have become an area of concern in auditing. This is largely due to the possible counterintuitive effects of audit fees on audit quality, wherein the magnitude of the audit fee may enhance auditors’ capacity to discern misstatements or damage auditors’ independence (Oladipupo & Monye-Emina, 2016).

Audit quality has been shown in several studies to increase a company’s financial performance. According to Afza and Nasir (2014), independent audit quality increased a company’s operational performance in the eyes of investors. They discovered that some companies that are audited by large audit firms will release financial statements that are reliable, appropriate, and legitimate, with the goal of reinforcing investor trust in those companies. However, Bouaziz (2012), excellent audit quality can lower agent costs when an auditor provides a reliable and sufficient index for financial statements, lowering monitor costs and enabling improved efficiency in a company’s commercial activities. Kaoje and Mohammed (2022) on the other hand, found a link between audit quality and firm performance. As a result, audit quality is projected to have a favorable impact on financial performance.

Statement of the problem

In most public organizations, especially in Nigeria, the Directors of enterprises are empowered to appoint, reappoint, and remove their auditors and to also fix the Auditor‘s fees using the guidelines of the organization. The problem so created is that the Directors are officers of the organization, who also have the responsibility of managing the funds, budgeting, spending including awarding of contracts and the preparation of financial statements. The same people who are therefore placed in a position to render stewardship accounts are now given the power to ‘hire and fire’ auditors who would audit the accounts of their own activities. This runs counter to the ideal principles of accountability. In the private sector, the stakeholders appoints external auditors subsequently approved by the CEO; the development therefore appears to put the auditor‘s investigative and reporting independence in jeopardy and this may defeat the purpose of audit and erode the independence and hence, the objectivity of report of the auditors. The foregoing therefore has raised doubts about the true independence of the auditors. And with recent high rate of corruption and collapse of organizations in the public and private sectors, the question of whether auditors are truly independent to carry out their task and whether the true independence of auditors would actually enhance organizational financial performance has thus necessitated this study.

Objectives of the study

The main objective of this study is to examine the effect of audit quality on financial performance of quoted conglomerates in Nigeria. The specific objectives of the study are:

- to find out the relationship between audit size and return on assets of quoted conglomerates in Nigeria.

- to assess the impact of audit fee on return on assets of quoted conglomerates in Nigeria.

- to determine the impact of audit tenure on return on assets of quoted conglomerates in Nigeria.

Research questions

The following questions have been raised to guide the study:

- What is the relationship between audit size and return on assets of quoted conglomerates in Nigeria?

- To what extent does audit fee impact on return on assets of quoted conglomerates in Nigeria?

- What impact does audit tenure have on return on assets of quoted conglomerates in Nigeria?

Research hypotheses

The following research hypotheses have been constructed and are presented in their null form.

- Ho: There is no significant relationship between audit size and return on assets of quoted conglomerates in Nigeria.

- Ho: Audit fee does not significantly impact on return on assets of quoted conglomerates in Nigeria

- Ho: Audit tenure has no significant impact on return on assets of quoted conglomerates in Nigeria.

REVIEW OF RELATED LITERATURE

Conceptual framework

The conceptual framework of this work is discussed below:

Audit quality

Yeboah (2020) sees auditing as obtaining and reasonable assurance that misstatement arising from Fraud and error that are material to the financial statements are detected. Generally, internal and external auditors may conduct audit into the operation of a company. The internal auditors are the employees of a company who are appointed by the management to carry out audit of the day-to-day affair of the company as part of the internal control system. The external auditor is highly regarded in the corporate governance framework because unlike the internal auditor, is appointed by the shareholders. The external auditor is an independent person or firm of auditors appointed according to statutory requirement to investigate the financial statements of an entity and express his opinion in form of report on the true and fair view of such financial statements (Alabede, 2012). Badara and Saidin (2014) state that audit effectiveness and audit independence have become a fruitful topic over the decade.

The financial statements that are audited are presented to shareholders to account for the stewardship of the management. However, such financial statements may lack credibility and shareholders may hardly believe the information contain therein. In order to overcome the problem of credibility of financial statements, an external auditor who is independent of the management is appointed to investigate the information in the financial statements and report his findings to the shareholders (Al-Thuneibal, Issa and Baker, 2011). For the shareholders and other stakeholders to believe in the financial statements, it is imperative to appoint independent expert to audit the financial statements, thus studies by Endaya and Hanefah (2016) have shown that there is direct relationship between auditors’ independence, characteristics and organizational performance.

Financial performance

The financial performance of publicly traded corporations on the capital market is important; it is also seen as a platform for attracting capital and lowering a company’s cost of capital (Kaoje and Mohammed, 2022). A corporation with a very high-pitched financial performance will, in reality, gain a favorable reputation among investors. At the same time, the capital market, managers, and investors rely on audited financial reports to make decisions about a company’s business efficiency (Thu et al., 2020). As a result, better financial reporting will have a favorable impact on the company’s financial performance. The term “financial performance” is described as “multifaceted” (Santos & Brito, 2012). Many scholars have used a variety of ways to quantify financial performance. The financial performance of the organization will be examined in this study based on its profitability. Profitability is always calculated as the ratio of pre-tax income to shareholder equity (Chen & Chen, 2011). Profitability is quantified in a variety of ways, including Return on Assets (ROA), Price Earnings Ratio (PER), and Return on Equity (ROE).

Audit quality and organizational financial performance

Evidence from literature confirms that certain areas of risk stemming from various situations and relationships in which an auditor‘s independence, and therefore, objectivity can be threatened. Wood and Small (2019) among others identify some of these risks or threats to include undue dependence on a client; overdue fees; actions or threatened litigations; family or other personal relationships; beneficial interesting shares and other investments; beneficial interests in trusts, loans, voting on audit appointments; acceptance of goods and services as gifts or hospitality; and provision of other services to audit clients. External auditors, through their interactions with audit committees are able to influence the company’s internal control strength as well as reporting quality (Velte and Loy, 2018). Basically, the statutory role of the external auditors is to issue audit report of his opinion on financial statements.

The Code of Corporate Governance states that the majority of audit committee members must be independent, and the Chairman should be an independent non-executive director. It enhances the effectiveness of monitoring functions. It serves as a reinforcing agent to the independence of internal and external auditors. It is posited that the more independent the audit committee, the higher the degree of oversight and the more likely that members act objectively in evaluating the propensity of the company accounting, internal control and reporting practices. This indicates that an independent audit committee is able to help companies sustain the continuity of business although when they are faced with financial difficulties, they are expected to propose certain action plans to mitigate the problem (Adeyemi, Okpala, and Dabor, 2012).

The key issue in the field of auditing and assurance is to recognise that auditing can be of even greater value if it looks beyond traditional financial issues and focuses on areas that matter to a wide range of stakeholders and the public (Abubakar and Obansa, 2020). Auditor’s independence has been threatened by factors such as deriving significant financial interest from a client, provision of non-audit services to a client, having close relationship with a client and intimidation (IFAC, 2010). In recent times, it was reported that the greatest threat to the auditor’s independence in Nigeria is the provision of non- audit services to clients (Bhatti and Akram, 2020).

Auditors may compromise quality because they derived substantially part of their income from non-audit services. Evidence has shown that the large firms derived great part of their income from non-audit services. The problem with provision of non-audit services is that it divides the focus of the auditor and creates unnecessary compromise. Another area of independence, which no much is talk about, is appointment of external auditor, which in theory is done by the shareholders from recommendation of the directors. In reality, the management does the appointment and auditor may do anything to favour his employer (Solomon, 2012). Despite being challenged for its reputation and audit quality, independence in performing audits remains a key feature that affects the audit quality and the institution’s performance in terms of finances, returns and efficiency.

Audit tenure and organizational financial performance

Audit tenure is the agreed period of engagement between the auditor and client (Hartadi, 2009). The issue of audit tenure is usually linked to auditor independence. Research conducted by Ghosh and Moon (2003) shows that audit quality increases as audit tenure increases. This result is however contrary to the results of a research conducted by Indah (2010) which reveals that as the length of auditor-client relationship increases; there could be decrease in the level of audit quality, because too long auditor-client relationship impairs auditor’s independence. Furthermore, the audit quality decreases as the auditor-client relationship lengthen. Corroborating this finding, Carey and Simnett (2006) also find that, in Australia, long audit partner tenure is associated with lower propensity to issue a going-concern report. However, the study involving going-concern report in the US suggest that audit reporting failures are significantly higher in the first few years of auditor-client relationship (Geiger and Raghunandan, 2002). According to Onaolapo, Ajulo and Onifade (2017), audit firm tenure as well as audit partner tenure, affects financial reporting quality.

Audit fee and organizational financial performance

Audit fee can be explained to be the amount charged by the auditor for an audit assignment carried out. That is, the amount charged by the auditor for any work done in order to express opinion on the true and fair state of affairs or position of the client’s enterprise. Suharli and Nurlaelah (2008) described audit fee as the fee charged by a public accountant to the client for the financial audit services. This is in accordance with the opinion of The Securities and Exchange Commission, Final Rule (in Yuniarti, 2011) that the audit fee is the fees paid for annual audits and reviews of financial statements for the most recent fiscal year. The amount of audit fee can vary depending on the complexity of services, assignment risk, the cost structure of Public Accountants Firm, the required level of expertise, and other professional considerations. Moreover, Hoitash, Markelevich and Barragato (2005) opined that the aggregate of audit fees are the amount of all costs covered for auditor. There is variation in the amount of the fee, depending on audit size and how complex the auditing process is (Lyon and Maher, 2005). This is further corroborated by Turley et al. (2008) who states that there are three composite factors which contribute to the establishment of audit fees, which include complexity, Client size and associated risk. Audit fees are the fees paid to the auditors that reflect the cost of the effort conducted by the public editors and litigation risks (Choi, 2009). According to Ettredge et al. (2007), if a client (auditee) pays lower audit fees than other firms in the same sector, the firm is more likely to become faithful to the audit firm, which could lead to the auditor ignoring material misstatement or permitting management to engage in aggressive earnings management. Exorbitant fees paid to auditors, especially for non-audit services make them more reliant on their clients (Kimeli, 2016).

Audit size and organizational financial performance

The Internal audit size (IAS) is essential to improve performance of companies. The size of internal audit is measured by the number of internal audit seating on the committee of the internal audit department. Alawaqleh, Almasria and Alsawalhah (2021) argued that larger boards are often characterized by responsibility diffusion, which leads to social loafing, it encourages group fractionalization and minimizes group commitment to modifying strategy. From the perspective of resource dependence theory, it further postulates that larger board size would result in superior corporate performance owing to the various skills, knowledge, and expertise contributed into the boardroom debate. In addition, large boards could also offer the diversity that would assist companies to obtain critical resources and minimize environmental risks (Kaoje & Mohammed, 2022).

Social exchange theory

The theoretical framework for this study is centered on social exchange theory. Social exchange theory as propounded by Blau in (1964) provides a useful framework for understanding how social interaction in the workplace influence auditor’s independence with the management and in carrying out his task. Social exchange relationships are often described as subjective, relationship-oriented contracts between employees and organizations characterized by mutual exchange of socio-emotional benefits, cooperation, trust, and a long-term focus Social exchange relationships can therefore strengthen the motivation of auditors to truly assess the facts of the financial statement.

Empirical review

Augustine, Chijioke, Oba and Jonathan (2014) examined the link between audit quality and auditor independence, auditor experience, auditor accountability. Using a sample of 210 respondents made up of finance directors, auditors, shareholders, and financial analysts and employing structural equation modeling technique for data analysis, the study found that auditor independence and auditor accountability have a significant relationship with audit quality. The study found that auditor experience is not a factor affecting audit quality in Nigeria.

Al-Attar (2017) explored the impact of auditing on stock prices of Amman stock market. Impact of audit is indicated in terms of audit quality and its effect on financial performance measured by stock prices. Primary data on audit and its impact on stock prices was gathered from finance managers of listed companies on the Amman stock exchange. The results were determined using descriptive analysis, factor analysis, and structural equation models. It was discovered that audit has a direct impact on the stock prices of enterprises in the Amman stock market, and that increased audit quality leads to improved financial performance of the firms as reflected in their stock prices.

Onaolapo, Ajulo and Onifade (2017) examined the effect of audit fees on audit quality in Nigeria. The study investigated the relationship between audit fee, audit tenure, client size, leverage ratio and audit quality. Ordinary Least Square Model estimation technique was employed. Secondary data derived from the published annual reports of the selected companies for a six year period (2010-2015) was used for the study. Findings showed that audit fee, audit tenure, client size and leverage ratio exhibit a joint significant relationship with audit quality. Audit fee in particular shows a significant positive impact on audit quality. The study recommended that Government through the various professional bodies should develop robust policies that will help improve audit quality in Nigeria.

Suleiman, Ahmad and Yusof (2017) examined relationship between internal audit quality (IAQ) and organizational performance with moderating variable of top management support in the federal universities in Nigeria. The independent variables consist of internal audit competence (IAC) and internal audit independence (IAI) with organizational performance as the dependent variable. A total of 400 samples of senior internal auditors’ level were drawn from 40 Nigerian federal universities. Data was collected via questionnaires and distributed to internal auditors. 400 questionnaires were distributed, 342 were returned, 29 were rejected and 313 were retained. The data was analysed using both descriptive and inferential statistics for testing hypotheses. The results revealed that there are significant positive relationships between the variables of the study, except internal audit independence with organizational performance. However, the result of moderating effect of top management support in the relationship between the independent variables and organizational performance, turns out to revealed that internal audit independence, have positive and significant relationship with organizational performance. The result showed strong correlation between the dimensions of internal audit quality and organizational performance and optimum performance in Nigerian federal universities is attainable when internal audit quality dimensions are functional. It recommended that the dimensions of internal audit quality should always be given attention a better service delivery and efficiency.

Ugwunta, Ugwuanyi and Ngwa (2018) assessed the effect of audit quality on share prices in Nigerian oil and gas sector using regression and covariance analyses. The audit committee membership and auditor type have a considerable impact on quoted company market prices, according to the findings. According to the covariance study, whereas auditor type, auditor independence, and audit committee composition all have a significant association with share price, audit tenure has a negative link with share price.

Chen (2019) studied the relationship between internal control audit fees and internal control audit quality. Using the 2011-2016 A-share listed company data test, it is found that under the control of other possible conditions, the higher the internal control audit fee and its proportion, the lower the probability of being issued anon-standard internal control audit opinion, which means that the relatively high internal control audit fee may be paid by companies to purchase more favorable internal control audit opinions. Further, the result was found to be more significant in non-state-owned, relatively smaller companies, and clients whose total audit fees are higher. The study concluded that the high internal control audit fees can be a form of damage to the independence and quality of internal control audit.

Abdullahi, Norfadzilah, Umar and Lateef (2020) examined the impact of audit quality on the financial performance of listed companies Nigeria. Based on a panel data technique, 84 companies listed on the NSE were used, using 756 samples during a nine-year period from 2010 to 2018. To test the model, the study used multiple regression. The findings demonstrate that audit fee has a favorable but minor connection with ROA. This suggested that lowering the fee paid to auditors for audit services will improve the financial performance of Nigerian publicly traded companies. Auditor size has a large positive association with ROA, which supports the agency argument. This positive figure shows that as the number of enterprises audited by Big4 grows, so does financial performance (ROA). Auditor independence is likewise linked to the ROA in a positive and statistically meaningful way. Finally, auditor independence was demonstrated to have a greater impact on financial performance than auditor size.

Gana, Mohd and Peter (2020) assessed the correlation between auditor independence and audit quality of the public sector in Nigeria. The researcher expects a clear positive relationship between auditor independence and public sector audit efficiency. Generally, this study outcome is expected to agree with the view that auditors with greater independence will overcome auditors’ predispositions to generate low-quality audit reports.

Olabisi, Kajola, Abioro and Oworu (2020) examined the factors that determine audit quality among listed insurance companies in Nigeria. The study adopted Ex-post facto research design, and 15 companies are purposively selected, out of 25 listed insurance companies in Nigeria as of 2018. Panel data is extracted from the annual account and reports of the selected companies over a period of ten years (2009–2018). Pearson correlation analysis, Ordinary Least Square (OLS) and Regression are the statistical tools used for the analysis. The results of the study revealed a significant relationship between the audit firm size, audit tenure, audit fee, cash flow and audit quality (p < 0.05). However, there is no significant relationship between auditors’ independence, joint audit and audit quality (p > 0.05). The study concluded that audit fees, audit firm size, audit tenure and cash flow from operations are major determinants of audit quality as each of them has significantly contributed to audit quality of listed insurance companies in Nigeria. Therefore, the Nigerian listed insurance companies should place a high premium on audit firm size, audit fees, and short-term audit tenure when engaging services of an audit firm.

Alawaqleh, Almasria and Alsawalhah (2021) examined (1) the association between the chief executive officer tenure and audit quality, (2) the relationship between chief executive officer duality and audit quality, (3) the association between board independence and audit quality, (4) the relationship between board size and audit quality, and (5) the role of controlling variables (client size, leverage debt, and business complexity) in controlling these relationships. The research sample includes 325 financial reports from manufacturing firms listed in Amman Stock exchange over the 2014-2018 period. The study relationships are tested by using logistic regression. The results revealed a negative relationship, but not significant between CEO tenure and independent directors with audit quality. In addition, the results showed there is a negative effect of CEO duality on audit quality; also the results revealed that there is a statistically significant effect on the board of directors (board size) on the AQ. In general, the coefficient estimates of controlling variables showed that client size and leverage debt positively affect audit quality, and on the contrary, business complexity has an insignificant positive relationship with audit quality.

Najmatuzzahrah, Mulyani and Akbar (2021) examined how the auditor’s independence affects the quality of an investigative audit and its effect on the credibility of the BPK. The main finding of the study is that the auditor’s independence as a value has a positive impact on the BPK’s reputation, which is represented by the quality of investigative audits.

Egiyi, Modesta Amaka (2022) empirically investigated the relationship between audit quality and audit fees in companies listed on the Nigerian stock exchange in the financial services sector with a panel data set spanning the years 2010 to 2020. The likelihood of employing the services of a Big4 audit firm is used as the proxy for audit quality. In Nigerian companies, the data show a significant negative association between audit quality and audit size. Leverage and firm size, the two explanatory variables, had an insignificant impact on audit quality. The empirical findings suggested that high audit fees threaten auditors’ independence, which has a detrimental impact on audit quality.

Ezegbe and Jeroh (2022) examined audit quality attributes as possible determinants of companies’ financial performance. The study drew inference from quoted companies in Nigeria, with data covering 10 years (2011 to 2020). The proxy for audit quality were statutory audit services, audit tenure, auditor’s independence, and audit-firm size; whereas, firm performance was measured by Return on Assets (ROA). Firm year data which were collated from their respective annual reports were obtained from the database of MACHAMERATIOS. The study adopted the Panel Least Square technique, descriptive analysis and relevant diagnostic tests as part of the tools used in analyzing the data collated. The study found that audit independence exerts significant negative influence on ROA; audit tenure and audit firm size had positive relationship with ROA, although, this relationship was not significant. Conversely, statutory audit service on its own significantly influenced firm performance (ROA). Overall, measures of audit quality exert joint significant influence on ROA. The study recommended among others that the country’s Financial Reporting Council and other regulators should develop policy guidelines to specifically checkmate auditors’ tenure vis-à-vis compliance to existing regulatory framework for financial reporting.

Inneh, Bussary, Fankule, Adeoye, and Kolawole (2022) examined the effect of audit delay on the financial reporting quality of listed non-financial firms in Nigeria. A sample size of 45 listed firms is selected using a purposive sampling technique. The study covered a period from 2011 to 2020, resulting in 450 firm-year observations. The data obtained is analysed using the Ordinary Least Square Method (OLS). The result showed that audit delay has a significant positive association with financial reporting quality. The result indicated that delay in giving an audit report enhances the financial reporting quality, thus allowing the auditor to detect and report on material misstatements and financial irregularities.

Kaoje and Mohammed (2022) examined the impact of audit quality on financial performance of quoted Oil and Gas marketing companies in Nigeria. The population comprised of 11 oil and gas companies quoted on the Nigeria Exchange Group Plc. The study adopted the longitudinal and ex-post facto research designs. Data were gathered from the published annual reports and accounts of the sampled oil and gas companies. The Multiple regression analysis model using the STATA Version 14.0 was employed in analyzing the data and testing of the stated hypotheses. The results revealed that audit firm type and auditors’ tenure has no significant relationship with the financial performance of the quoted oil and gas marketing companies in Nigeria which is evidenced from a p-value 0.995 and 0.730 respectively. The study recommended that quoted oil and gas marketing companies should ensure that they comply with the regulations as to the tenure of auditors as contained in CAMA 2020.

Gap in literature

Research on auditor quality reached its heights of dominance in academic circles after accounting scandals involving top corporate organizations such as Enron, WorldCom, Cendant, Adelphia, Parmalat and Satyam. Several studies have therefore been carried out in this area with various findings. However, it is worthy to note that there is no large consensus among researchers that audit quality is imperative for improved financial performance. This gap in literature creates the need for more research on the home front, that is, in Nigeria.

METHODOLOGY

Scope of the study

This study focuses on the effect of audit quality on financial performance of quoted conglomerates in Nigeria. It lays emphasis on audit quality proxies such as audit size, audit fee and audit tenure while financial performance is proxied by returns on assets. The study covers the period of 12 years from 2010-2021 using financial report of selected conglomerates quoted at the stock exchange.

Collection of data

The data sourced for this study is mainly secondary source collected from the financial report of Cadbury Nigeria Plc, Dangote Plc, Glaxo Smithkline Consumer Nig. Plc, May & Baker Nigeria Plc., PZ Cussons Nigeria Plc and Unilevers Plc. In addition, secondary sources were also used in the literature which includes journals, textbooks and internet materials.

Sample size determination

Since the study involves the use of time series data, the sample size used was period of time covers 2010-2021 which is 12 years. This was selected using purposive sampling technique. Purposive sampling technique involves selected of sample based on judgment, convenience and access. The essence of using this technique was due to access to the financial reports of the manufacturing companies.

Model specification

The model is in the stated hypotheses are expressed in the following functions:

Y= f (X)

Where, Y= Dependent variable

X= Independent variable

- Ho: There is no significant relationship between audit size and banks returns on asset.

ROA= f (Audit Size)………………………………………………..….. i

Where;

ROA = Return on asset

SIZE = Audit committee size

The relationship expressed in equation form is

ROAt = a + b1 SIZEt + Ut………… ……………………………………ii

- Ho: Audit fee does not significantly impact on banks returns on asset.

ROA= f (FEE)…………………….………………….……………….. iii

Where;

ROA = Return on asset

FEE= Audit committee remuneration or fees

The relationship expressed in equation form is

ROAt = a + b1 FEEt + Ut………… ……………………………………..…iv

- Ho: Audit tenure has no significant impact on banks returns on asset.

ROA= f (TENURE)…………………….………………….……………….v

Where;

ROA = Return on asset

TENURE= Audit committee tenure

The relationship expressed in equation form is

ROAt = a + b1 TENUREt + Ut………… ……………………………………vi

Using the multiple regression analysis, the model can be restated as

ROA = f (AUDIT SIZE, AUDIT FEES, AUDIT TENURE)……………………i

Y = F(X)

Where y= dependent variable and x= independent variable

Therefore: ROA= return on assets (y)

AUDIT SIZE= Total number of auditors per year

AUDIT FEES= The fees paid auditors annually

AUDIT TENURE= The tenure of the auditors

The relationship expressed in equation form is

ROAt = a + b1 AUDITSIZEt +b2 AUDITFEESt+ b3 AUDITTENUREt+ Ut………ii.

Where; b1, b2, b3> 0

Data analysis techniques

Panel least square regression analysis was used for data estimation since the data set involves a cross sectional time series.

DATA ANALYSIS

Data for this study is as presented in appendix 1.

Table 4.1: Result of OLS analysis

| Dependent Variable: ROA | ||||

| Included observations: 69 | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| AUDIT_SIZE | -0.007033 | 0.017385 | -0.404538 | 0.6871 |

| AUDIT FEE | -1.25E-10 | 5.44E-11 | -2.298567 | 0.0248 |

| AUDIT TENURE | 0.019718 | 0.008770 | 2.248434 | 0.0279 |

| C | -0.022821 | 0.102295 | -0.223095 | 0.8242 |

| R-squared | 0.121599 | Mean dependent var | 0.045933 | |

| Adjusted R-squared | 0.081057 | S.D. dependent var | 0.112589 | |

| S.E. of regression | 0.107930 | Akaike info criterion | -1.558446 | |

| Sum squared resid | 0.757177 | Schwarz criterion | -1.428933 | |

| Log likelihood | 57.76639 | Hannan-Quinn criter. | -1.507064 | |

| F-statistic | 2.999355 | Durbin-Watson stat | 1.491735 | |

| Prob(F-statistic) | 0.036882 | |||

Source: Author’s computation

The model for the regression is estimated as ROA = -0.00703269241807*AUDIT SIZE – 1.25061144334e-10*AUDIT FEE + 0.0197184876426*AUDIT TENURE – 0.022821404023.

From empirical results of the panel regression in table 4.1, the coefficient of determination R2 is 12.16%, indicating that the variables are poorly fitted on regression. The adjusted coefficient of determination is 8.11% implying that 8.11 percent of the total variation found in ROA is explained by the presence of audit size, audit fees, audit tenure while the remaining 91.89% is the presence of the unexplained variable.

The F-test ratio of 3.0 with p-value of (0.0368) shows that the overall regression is significant at 5%. The Durbin Watson statistic value 1.491 appropriates to less 2 indicating presence of positive autocorrelation. This implies the need to run further analysis such as unit root test and cointegration.

Table 4.2: Summary ADF Unit Root Test 1

| Variable | ADF Test Statistics | Stationarity | ||||

| Level | Prob | 1st Diff | Prob | Level | 1st Diff | |

| LROA | -2.207304 | 0.2081 | -4.349222 | 0.0021 | none | I(1) |

| LAUDIT SIZE | -3.977721 | 0.0048 | -6.388078 | 0.0000 | none | I(1) |

| LAUDIT FEE | -2.695734 | 0.0872 | -3.425622 | 0.0192 | none | I(1) |

| LAUDIT TENURE | -2.789992 | 0.0372 | -4.725615 | 0.0127 | none | I(1) |

Source: Author’s computation

Variables in table 4.2 are non-stationary at levels but stationary at 1st difference, i.e., they are integrated of order 1 or I (1). Because, all the variables are integrated of order 1, a Johansen Cointegration test was conducted to establish whether there is a longrun equilibrium relationship among the variables.

Table 4.3: Johansen Cointegration Test 1

| Series: ROA AUDIT_SIZE AUDIT_FEE AUDIT_TENURE | ||||

| Lags interval (in first differences): 1 to 2 | ||||

| Cointegration Rank Test (Trace) | ||||

| Hypothesized | Trace | 0.05 | ||

| No. of CE(s) | Eigenvalue | Statistic | Critical Value | Prob.** |

| None | 0.276232 | 39.41650 | 47.85613 | 0.2440 |

| At most 1 | 0.147027 | 18.07977 | 29.79707 | 0.5602 |

| At most 2 | 0.082898 | 7.583928 | 15.49471 | 0.5109 |

| At most 3 | 0.027973 | 1.872533 | 3.841466 | 0.1712 |

| Unrestricted Cointegration Rank Test (Maximum Eigenvalue) | ||||

| None | 0.276232 | 21.33673 | 27.58434 | 0.2564 |

| At most 1 | 0.147027 | 10.49584 | 21.13162 | 0.6972 |

| At most 2 | 0.082898 | 5.711395 | 14.26460 | 0.6505 |

| At most 3 | 0.027973 | 1.872533 | 3.841466 | 0.1712 |

Source: Author’s computation

Trace test and max-eigen value test indicate no cointegration equation each at the 0.05% level, denoting rejection of the hypotheses at the 0.05 level. Because of no existence of long-run equilibrium among the variables, a short-run, ECM model was used for further analysis.

Table 4.4: Long and Short Run Model 1

| Dependent Variable: D(LLAR) | ||||

| Method: Least Squares | ||||

| Date: 12/01/24 Time: 23:16 | ||||

| Sample (adjusted): 1992 2020 | ||||

| Included observations: 29 after adjustments | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| C | 0.008011 | 0.029001 | 0.276221 | 0.7846 |

| LAUDIT_SIZE | -0.074277 | 0.088333 | -0.840880 | 0.4084 |

| LAUDIT_FEE | -0.080619 | 0.061593 | -1.308897 | 0.2025 |

| LAUDIT_TENURE | 0.082898 | 0.650587 | -0.998421 | 0.4398 |

| ECM(-1) | -0.508443 | 0.189117 | -2.688516 | 0.0126 |

| R-squared | 0.255723 | Mean dependent var | 0.001544 | |

| Adjusted R-squared | 0.166410 | S.D. dependent var | 0.170079 | |

| S.E. of regression | 0.155284 | Akaike info criterion | -0.759681 | |

| Sum squared resid | 0.602828 | Schwarz criterion | -0.571088 | |

| Log likelihood | 15.01537 | Hannan-Quinn criter. | -0.700616 | |

| F-statistic | 2.863219 | Durbin-Watson stat | 1.993194 | |

| Prob(F-statistic) | 0.056915 | |||

Source: Author’s computation

The short run model is the ECM. This is:

ECM = LAUDIT SIZEt-1– β0 – β1LAUDIT FEEt-1 – β2L LAUDIT TENUREt-1. eq(1)

D(LROA)t = 0.008–0.074D (LAUDIT SIZE) t –0.081D (LAUDIT FEE) t – β2L LAUDIT TENURE (0.083) t-1 -0.508ECM (-1). ………………Eq (3)

Table 4.4 shows that a 1% change in ROA, is insignificantly but negatively affected by about 0.074 or 7% relative change in LAUDIT_SIZE.

The significant ECM coefficient, -0.508, suggests that almost 51% of the discrepancy between long run and short run is corrected within a year. The table 4.5 model contains a lagged ECM as an independent variable, the Durbin-Watson, DW or d, of 1.99 or equivalent 2, which is the first instance, shows no serial correlation, becomes irrelevant. To check for serial correlation in a model that contains lags of dependent variables becoming independent variables, we apply or conduct diagnostic tests. This sub section shows the diagnostic test for serial autocorrelation and others.

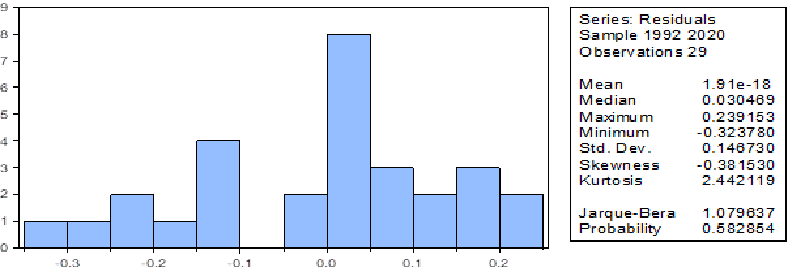

Chart 4.1 Histogram – normality test of residuals

The joint test of Jarque-Bera indicates that the JB statistic of 1.080 is insignificant (p-value=0.583) to affect the normal distribution of the residuals. The residuals are jointly, normally distributed.

Table 4.5: Breusch-Godfrey Serial Correlation LM Test

| F-statistic | 0.164493 | Prob. F (2,23) | 0.8493 |

| Obs*R-squared | 0.408959 | Prob. Chi-Square (2) | 0.8151 |

The BG, LM test in table 4.5 shows that the F-statistic and obs*R-Squared are insignificant to result to serial correlation, suggesting that there is no first order serial correction in the series with lagged ECM, an independent variable.

Table 4.6: Heteroskedasticity Test: Breusch-Pagan-Godfrey

| F-statistic | 0.785742 | Prob. F (3,25) | 0.5132 |

| Obs*R-squared | 2.498776 | Prob. Chi-Square (3) | 0.4755 |

| Scaled explained SS | 1.339006 | Prob. Chi-Square (3) | 0.7199 |

Is there any heteroskedasticity in our short run model? Table 4.6, BPG test’s F-stat, obs* R2 and scaled explained SS stats respectively suggest that the residuals in our model were insignificantly influenced by the presence of heteroskedasticity. Therefore, there is homogeneity in our model.

Test of hypotheses

Test of hypothesis one

H01: There is no significant relationship between audit size and return on assets of quoted conglomerates in Nigeria.

From the regression result, the regression coefficient of Audit size is negative (-0.074277) and insignificant (P–value=0.4084 > 0.05) with ROA. Hence, the null hypothesis is accepted that there is no significant relationship between audit size and return on assets of quoted conglomerates in Nigeria.

Test of hypothesis two

H02: Audit fee does not significantly impact on return on assets of quoted conglomerates in Nigeria

The regression coefficient of Audit fee is negative (-0.080619) and insignificant (P–value=0.2025 > 0.05) with ROA. Hence, the null hypothesis is accepted that there is no significant relationship between audit size and return on assets of quoted conglomerates in Nigeria.

Test of hypothesis three

H03: Audit fee does not significantly impact on return on assets of quoted conglomerates in Nigeria

The regression coefficient of Audit tenure is positive (-0.080619) and insignificant (P–value=0.4398 > 0.05) with ROA. Hence, the null hypothesis is accepted that Audit fee does not significantly impact on return on assets of quoted conglomerates in Nigeria.

DISCUSSION OF FINDINGS

The analysis revealed a negative and insignificant relationship between audit size and ROA. This result implies that audit size has an insignificant negative impact on firm performance. This result is consistent with findings by Ishak and Abidin (2021).

Our results also reveal a negative and significant relationship between audit fee and return on asset. This result suggests that increase in audit fee results in a decrease in return on asset of a firm, while lower audit fees results in improved return on asset. This result suggests that increase in audit fee results in a decrease in return on assets of a firm, while lower audit fees results in improved return on asset for the firm. The result is consistent with findings by Davi, Guilherme and Sidmar (2019). The findings, however, contradicts result by Oghuvwu and Orakwue (2019).

We also found a significant positive relationship between audit tenure and return on assets. This result implies that the lower a particular audit firm audits the accounts of a client firm the more improvement is recorded in terms of returns on assets. This is consistent with the findings of Kaoje and Mohammed (2022) that auditors’ tenure has no significant relationship with the financial performance.

CONCLUSION AND RECOMMENDATIONS

Conclusion

Following the study’s review, expanding audit report by increasing audit communication has some benefit and challenges to the firm. Given this assertion, we deduce that disclosing critical or key audit matters will be dependent on a couple of firm characteristics. However, from the study’s estimation, we conclude that audit tenure affects a firm propensity to disclose key audit matters. However, the audit size and audit fee may not be considered a strong driver given our findings of a non-significant relationship.

Results might suggest that the new requirement does not lead auditor to expand the audit efforts, possibly because the proposal for enhanced reporting has been made known to the profession long before its actual implementations. The study contributes to knowledge by suggesting the importance of audit tenure as a determining variable for key audit matters and audit quality.

Recommendations

Based on the findings, this study recommends as follows:

- organisations should ensure that the objective of credibility and transparency is achieved, this will enhance the quality of audit report.

- disclosure of key audit items is an important attitude of audited firms; therefore, there must be willingness of management to communicate with the auditor while also enlarging the audit size.

- to have an improved audit report and minimize the adverse impact on the company, the management should make the auditor more aware of the intended disclosure and the company’s position and communicate with the auditor more actively.

Contribution to knowledge

This study has shown audit quality serves majorly as n information necessary for investors to make decisions concerning investment in companies. However, the quality of an audit may not necessarily determine the financial performance of organizations rather the various attentions to the key components of the audit report and investment decisions of the companies.

REFERENCES

- Abubakar, I., & Obansa, S. (2020). An estimate of average cost of hypertension and its catastrophic effect on the people living with hypertension: Patients’ perception from two Hospitals in Abuja, Nigeria. International Journal of Social Sciences and Economic Review, 2(2), 10-19.

- Adeleke, D. B. (2021). Audit committee characteristics and the quality of financial reports of listed financial institutions in Nigeria. IOSR Journal of Business and Management, 23 (6), 59-73

- Adeyemi, S. B., Okpala, O. & Dabor, E. L. (2012). Factors affecting audit quality in Nigeria. International Journal of Business and Social Science 3 (20), 198-209.

- Afza, T., & Nazir, M. S. (2014). Audit quality and firm value: A case of Pakistan. Research Journal of Applied Sciences, Engineering and Technology, 7(9),1803-1810.

- Alabede, J.O. (2012). The role, compromise and problems of the external auditor in corporate governance. Research Journal of Finance and Accounting, 3 (9), 114-126.

- Alawaqleh, Q. A., Almasria, N.A. & Alsawalhah, J. M. (2021). The Effect of Board of Directors and CEO on audit quality: Evidence from listed manufacturing firms in Jordan. Journal of Asian Finance, Economics and Business, 8 (2), 0243–0253. doi:10.13106/jafeb.2021.vol8.no2.0243

- Al-Thuneibal, A.A., Issa, R.T.I. & Baker, R.A.A. (2011) Do audit tenure and firm size contribute to audit quality: Empirical evidence from Jordan. Managerial Auditing Journal. 26(4), 317-334.

- Augustine, O. E., Chijioke, M., Oba, E. & Jonathan, E. (2014). Audit firm characteristics and auditing quality: The Nigerian experience. Research Journal of Finance and Accounting, 5 (6), 23-34.

- Badara, M. A. S., & Saidin, S. Z. (2014). Empirical evidence of antecedents of internal audit effectiveness from Nigerian perspective. Middle-East Journal of Scientific Research, 19, 460-471.

- Bhatti, A., & Akram, H. (2020). The moderating role of subjective norms between online shopping behaviour and its determinants. International Journal of Social Sciences and Economic Review, 2(2), 1-09.

- Bouaziz, Z. (2012). The impact of auditor size on financial performance of Tunisian companies. Paper presented at the Faculty of Economics and Management. Sfax University, Tunisia.

- Carey, P. & Simnett, R. (2006). Audit partner tenure and audit quality. Accounting Review 81(3): 653–76.

- Chen, L.-J., & Chen, S.-Y. (2011).The influence of profitability on firm value with capital structure as the mediator and firm size and industry as moderators. Investment Management and Financial Innovations, 8(3), 121–129.

- Chen, R.S. (2019). Internal control audit fee and internal control audit quality—Evidence from integrated audits. Open Journal of Business and Management, 7, 292-311. https://doi.org/10.4236/ojbm.2019.71020

- Choi, J. H., Kim, J. B., Liu, X. & Simunic, D. A. (2009). Cross-listing audit fee premiums: Theory and evidence. The Accounting Review. 84: 1429-1463.

- Egiyi, M. A. (2022). Audit quality and audit fees: The case of listed companies in the Nigerian financial services sector. Contemporary Journal of Management, 4(2), 14-24.

- Endaya, K. A., & Hanefah, M. M. (2016). Internal auditor characteristics, internal audit effectiveness, and moderating effect of senior management. Journal of Economic and Administrative Sciences, 32, 160-176.

- Ettredge, M., Scholz, S. and Li, C. (2007). Audit fees and auditor dismissals in the Sarbanes-Oxley era. Accounting Horizons, 21(4): 371-386

- Gana K. W., Mohd, N. A. & Peter T. (2020). Auditor independence and audit quality in Nigeria public sector: A critical review. Journal of Critical Reviews, 7 (7), 839

- Geiger, M., & Raghunandan, K. (2002). Auditor tenure and audit reporting failures. Auditing: A Journal of Practice and Theory 21(1), 67-78.

- Ghosh, A. & Moon, D. (2003).Auditor tenure and perceptions of auditor quality. The Accounting Review, 80(2), 585 – 612.

- Hartadi, B. (2009). Influence of audit fee, KAP rotation, and the reputation of auditors on audit quality in the Indonesia Stock Exchange. Journal of Economic and Finance.16. (1). pp. 84-103.

- Hoitash, R., Markelevich, A. & Barragato, C.A. (2007). Auditor fees and audit quality. Managerial Auditing Journal, 22 (8), 761-786.

- Inneh, E., Bussary R., Fankule, I. Adeoye, E. & Kolawole, P. (2022). Does audit delay enhance financial report quality? Evidence from Nigeria listed non—financial institutions. Research Journal of Finance and Accounting. 12 (14) 19-26.

- Kaoje, N.A, Babangida, M.A & Kaoje, R.M (2022). Sustainability reporting and financial performance of oil and gas firms in Nigeria: A paradox of environmental cost. 1st Annual Faculty of Arts, Social and Management Sciences National Conference, Federal University, Birnin Kebbi, Kebbi State.

- Kimeli, E. K. (2016). Determinants of audit fees pricing: Evidence from Nairobi Securities Exchange (NSE). International Journal of Research in Business Studies and Management, 3 (1), pp. 23-35.

- Lyon & Maher (2005). The importance of business risk in setting audit fees: Evidence from cases of client misconduct. Journal of Accounting Research, 43 (1): pp 133-151.

- Najmatuzzahrah, W. S., Mulyani, S. & Akbar, B. (2021). Research audit quality and its impact on an organization’s reputation. Utopíay Praxis Latinoamericana, 26 (1), 207

- Olabisi J., Kajola S.O., Abioro M.A. & Oworu O.O. (2020) Determinants of Audit Quality: Evidence from Nigerian Listed Insurance Companies. Journal of Volgograd State University. Economics, 22 (2), 182-192. DOI: https://doi.org/10.15688/ek.jvolsu.2020.2.17

- Oladipupo, A.O. and Monye-Emina, H.E. (2016). Do abnormal audit fees matter in the Nigerian audit market? International Journal of Business and Finance Management Research, 4(6), 64-73.

- Onaolapo A. A., Ajulo O. B. & Onifade, H. O. (2017). Effect of audit fees on audit quality: Evidence from cement manufacturing companies in Nigeria. European Journal of Accounting, Auditing and Finance Research, 5 (1), 6-17,

- Santos,J.B. & Brito, L. A. L. (2012).Toward a subjective measurement model for firm performance. BAR-Brazilian Administration Review, 9(SPE),95-117.

- Solomon, O. (2012). Evaluation of the auditors roles and performance in the public sector. www.independent.academia.edu/kingsooloo

- Suleiman, M. B., Ahmad, C. A. & Yusof, M. Z. (2017). Investigating the relationship between internal audit quality and organisational performance of public universities in Nigeria. European Journal of Accounting, Auditing and Finance Research, 5 (6), pp.1-23.

- Thu, T. H, Lam, A.L, Thi, T. L., Dung, M. T. & Dang, T.T (2020). The impact to audit quality on performance of enterprises listed on Hanoi Stock Exchange. Management Science Letters.

- Suharli, M. & Nurlaelah, E. (2008). The concentration of the auditor and the audit fee determination: Investigation on SOEs. Journal Akuntansi dan Auditing Indonesia.12. (2). pp. 133-148

- Turley .S. & Willekens .M. (2008). Auditing, trust and governance: Regulation in Europe. 1st edition. Oxon, England: Routledge

- Wood, A., & Small, K. (2019). An assessment of corporate governance in financial institutions in Barbados. Journal of Governance & Regulation, 8(1), 47-58.

- Yakubu, R. & Williams, T. (2020). A theoretical approach to auditor independence and audit quality. Corporate Ownership & Control, 17 (2), 124

- Yeboah, E. (2020). Critical literature review on internal audit effectiveness. Open Journal of Business and Management, 8, 1977-1987

- Yuniarti, R. (2011). Audit firm size, audit fee and audit quality. Journal of Global Management.2. (1). pp. 84-97.

- Velte, P., & Loy, T. (2018). The impact of auditor rotation, audit firm rotation and non-audit services on earnings quality, audit quality and investor perceptions: A literature review. Journal of Governance and Regulation, 7(2), 74-90.

APPENDIX 1

Data Presentation

| COMPANY | Year | ROA | Audit Fee | Audit Size | Audit Tenure |

| Dangote Plc | 2010 | 0.016 | 193000000 | 6 | 8 |

| Dangote Plc | 2011 | 0.019 | 284000000 | 6 | 8 |

| Dangote Plc | 2012 | 0.026 | 429000000 | 6 | 8 |

| Dangote Plc | 2013 | 0.018 | 425000000 | 6 | 8 |

| Dangote Plc | 2014 | 0.019 | 567000000 | 6 | 10 |

| Dangote Plc | 2015 | 0.004 | 803000000 | 6 | 10 |

| Dangote Plc | 2016 | 0.003 | 856000000 | 6 | 10 |

| Dangote Plc | 2017 | 0.008 | 901100300 | 6 | 10 |

| Dangote Plc | 2018 | 0.007 | 964000000 | 6 | 10 |

| Dangote Plc | 2019 | 0.112 | 977000000 | 6 | 10 |

| Dangote Plc | 2020 | 0.004 | 984000000 | 6 | 10 |

| Dangote Plc | 2021 | 0.005 | 992400000 | 6 | 10 |

| Unilevers Plc | 2010 | 0.035398 | 217761300 | 6 | 8 |

| Unilevers Plc | 2011 | 0.034560 | 228062000 | 6 | 8 |

| Unilevers Plc | 2012 | 0.052622 | 252000000 | 6 | 8 |

| Unilevers Plc | 2013 | 0.044921 | 256600000 | 6 | 9 |

| Unilevers Plc | 2014 | 0.041931 | 300000000 | 6 | 9 |

| Unilevers Plc | 2015 | 0.041406 | 330000000 | 6 | 9 |

| Unilevers Plc | 2016 | 0.048534 | 400000000 | 6 | 9 |

| Unilevers Plc | 2017 | 0.057093 | 475000000 | 6 | 10 |

| Unilevers Plc | 2018 | 0.034412 | 500000000 | 6 | 10 |

| Unilevers Plc | 2019 | 0.061661 | 550000000 | 6 | 10 |

| Unilevers Plc | 2020 | 0.023911 | 607500000 | 6 | 10 |

| Unilevers Plc | 2021 | 0.040812 | 713600000 | 6 | 10 |

| Cadbury Nigeria Plc | 2011 | 0.019 | 254000000 | 6 | 7 |

| Cadbury Nigeria Plc | 2012 | 0.039 | 281000000 | 6 | 7 |

| Cadbury Nigeria Plc | 2013 | 0.029 | 429000000 | 6 | 7 |

| Cadbury Nigeria Plc | 2014 | 0.027 | 401000000 | 6 | 7 |

| Cadbury Nigeria Plc | 2015 | 0.025 | 447000000 | 8 | 7 |

| Cadbury Nigeria Plc | 2016 | 0.029 | 486000000 | 8 | 7 |

| Cadbury Nigeria Plc | 2017 | 0.032 | 510000000 | 6 | 7 |

| Cadbury Nigeria Plc | 2018 | 0.033 | 535000000 | 6 | 7 |

| Cadbury Nigeria Plc | 2019 | 0.031 | 590000000 | 6 | 7 |

| Cadbury Nigeria Plc | 2020 | 0.028 | 380000000 | 6 | 7 |

| Cadbury Nigeria Plc | 2021 | 0.041 | 471000000 | 6 | 8 |

| Glaxo Smithkline Consumer Nig. Plc. | 2011 | -0.002 | 113000000 | 5 | 5 |

| Glaxo Smithkline Consumer Nig. Plc. | 2012 | 0.026 | 179000000 | 5 | 5 |

| Glaxo Smithkline Consumer Nig. Plc. | 2013 | 0.025 | 180000000 | 4 | 6 |

| Glaxo Smithkline Consumer Nig. Plc. | 2014 | 0.017 | 748000000 | 4 | 6 |

| Glaxo Smithkline Consumer Nig. Plc. | 2015 | 0.025 | 670000000 | 4 | 7 |

| Glaxo Smithkline Consumer Nig. Plc. | 2016 | 0.029 | 319000000 | 4 | 7 |

| Glaxo Smithkline Consumer Nig. Plc. | 2017 | 0.019 | 321000000 | 4 | 7 |

| Glaxo Smithkline Consumer Nig. Plc. | 2018 | 0.008 | 350000000 | 4 | 7 |

| Glaxo Smithkline Consumer Nig. Plc. | 2019 | 0.027 | 360000000 | 4 | 7 |

| Glaxo Smithkline Consumer Nig. Plc. | 2020 | 0.012 | 608000000 | 4 | 7 |

| Glaxo Smithkline Consumer Nig. Plc. | 2021 | 0.081 | 612910000 | 4 | 7 |

| May & Baker Nigeria Plc. | 2011 | 0.006 | 200000000 | 5 | 5 |

| May & Baker Nigeria Plc. | 2012 | 0.024 | 220000000 | 6 | 5 |

| May & Baker Nigeria Plc. | 2013 | 0.015 | 250000000 | 6 | 6 |

| May & Baker Nigeria Plc. | 2014 | 0.02 | 260000000 | 6 | 6 |

| May & Baker Nigeria Plc. | 2015 | 0.027 | 300000000 | 6 | 7 |

| May & Baker Nigeria Plc. | 2016 | 0.02 | 360000000 | 6 | 7 |

| May & Baker Nigeria Plc. | 2017 | 0.015 | 400000000 | 6 | 7 |

| May & Baker Nigeria Plc. | 2018 | 0.019 | 420000000 | 6 | 7 |

| May & Baker Nigeria Plc. | 2019 | 0.011 | 603000000 | 6 | 7 |

| May & Baker Nigeria Plc. | 2020 | 0.010 | 603000000 | 6 | 7 |

| May & Baker Nigeria Plc. | 2021 | 0.031 | 621000000 | 6 | 7 |

| P Z Cussons Nigeria Plc. | 2010 | 0.0987 | 95000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2011 | 0.1396 | 108000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2012 | 0.3576 | 80000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2013 | 0.8856 | 84000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2014 | 0.0222 | 98000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2015 | 0.0176 | 131000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2016 | 0.0141 | 131000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2017 | 0.0096 | 159000000 | 7 | 10 |

| P Z Cussons Nigeria Plc. | 2018 | 0.0139 | 192000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2019 | 0.0142 | 175000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2020 | 0.0119 | 172000000 | 6 | 10 |

| P Z Cussons Nigeria Plc. | 2021 | 0.0281 | 183150000 | 6 | 10 |

Source: Authors computation