Effect of Internet Corporate Reporting on Financial Performance of Listed Manufacturing Firms in Nigeria

- AKINFEMIDE, Hannah Mayowa

- MUSTAFA, Murtala Oladimeji Abioye

- LASISI, Tirimisitu Kunle

- AKANO, Monsurat Olaide

- 301-321

- Jan 27, 2024

- Accounting & Finance

Effect of Internet Corporate Reporting on Financial Performance of Listed Manufacturing Firms in Nigeria

AKINFEMIDE, Hannah Mayowa1; MUSTAFA, Murtala Oladimeji Abioye1; LASISI, Tirimisiyu Kunle2; AKANO, Monsurat Olaide1

1University of Abuja, Abuja, Nigeria.

2Federal University Lafia, Nasarawa State, Nigeria.

DOI: https://dx.doi.org/10.47772/IJRISS.2024.801023

Received: 09 December 2023; Revised: 21 December 2023; Accepted: 25 December 2023; Published: 26 January 2024

ABSTRACT

The growth in the number of internet users and disclosed information has had a major impact on the performance of different legal and economic frameworks globally. This study aims to examine the relationship between online corporate reporting and financial performance of listed manufacturing firms in Nigeria during pre- and post-IFRS implementation. The population of research was comprised of all one hundred and two (102) publicly traded manufacturing companies in Nigeria as of December 2018. Secondary data were collected from the sample of thirty-one (31) publicly traded manufacturing companies for a period of 10 years, divided into 2009 to 2013 (pre-IFRS) and 2014 to 2018 (post-IFRS. The data collected were analysed using multiple regression analysis. The findings from the study show that online corporate reporting, and firm size positively affects firm value (FV), whereas firm age negatively affects firm value during pre-IFRS periods. The results also show that online corporate reporting and firm age inversely related to firm value, while firm size positively affects firm value (FV) after-IFRS adoption. The research outcome further reveal that negative relationship exists between internet corporate reporting, company size and earnings per share (EPS), meanwhile, firm age has positive influence with earnings per share (EPS) of listed manufacturing firms in Nigeria during pre-IFRS periods. It was discovered that for post-IFRS period, internet corporate reporting and leverage are positively significant with earnings per share (EPS), whereas company size and age do not. Furthermore, the study found that a negative relationship exists between internet corporate reporting and return on equity (ROE) for both pre-IFRS and post-IFRS period, while firm size has a positive relationship with return on equity (ROE) of listed manufacturing firms in Nigeria during pre-IFRS periods only. The regression results also reveal that return on equity (ROE) is negatively affected by leverage during post-IFRS periods. The study recommends that management of Nigerian quoted manufacturing companies should continue using internet as a platform in disseminating company financial information to the stakeholders since the internet corporate reporting positively improve the value of listed manufacturing firms in Nigeria. It is also recommended that the management of Nigerian quoted manufacturing companies should embrace the internet as a tool for communicating with stakeholders in order to improve value of their earnings per share and shares prospects in the market.

Keywords: Corporate Reporting, Financial Performance, Return on Equity, Pre-IFRS and Post IFRS,

INTRODUCTION

Corporations worldwide are increasingly using internet corporate reporting (ICR) to communicate with current and potential customers due to the global usage of the internet and the growing demands for information from stakeholders. The internet offers organisations a range of cost-effective possibilities to disseminate financial information to their investors and creditors. Moreover, the financial data shared online is predominantly current and is provided in many multimedia formats, enhancing its usability for decision-making purposes (Wagenhofer, 2003). Internet reporting methods exhibit variations in terms of content and technological utilisation among enterprises and nations, influenced by many environmental factors. The factors that impact ICR include the economy, capital markets, accounting and regulatory environment, enforcement mechanisms, and culture (Haniffa & Cooke, 2002).

The internet provides current financial information that is presented in diverse multimedia formats, facilitating its utilisation in decision-making (Wagenhofer, 2003). Internet reporting methods exhibit variations in terms of content and the utilisation of technology among enterprises and nations, influenced by many environmental factors. The factors that impact internet business reporting encompass the economy, capital markets, accounting and regulatory environment, enforcement procedures, and culture (Haniffa & Cooke, 2002).

An analysis of the literature reveals that the majority of studies examining the correlation between internet corporate reporting and firm financial success have been conducted in industrialised nations, whereas only a limited number of studies have been undertaken in developing nations. Adityawarmani (2018) conducted a study on the impact of internet financial reporting on the market value of manufacturing companies listed in Indonesia. In a study conducted by Elsayed, N. M. E. (2010), the researcher examined the primary factors that influence the voluntary adoption of corporate internet reporting and its impact on the value of publicly traded companies in Egypt. In addition, Munther and Rekha (2013) conducted a study on the examination of internet-based financial reporting in the United Arab Emirates. Richard and Samuel (2015) conducted a study on corporate reporting on the internet and the expectancies gap, which represents a modern manifestation of a longstanding issue. The following studies have been conducted: Akmalia, Hassan, and Hafizah in 2018, Eka in 2014, Al-ebrahem in 2017, Linda and Dhini in 2017, Ahmed, Ghassan, Bruce, and Theresa in 2018, and Nel and Baard in 2019.

Nigeria has also conducted studies on Internet Corporate Reporting, similar to other countries. Yusuf (2013) conducted studies examining the correlation between internet financial reporting and factors such as profitability, leverage, company size, foreign listing, and industry type. Nancy and Monday (2016) conducted research to assess the impact of firm size, profitability, and gearing on voluntary internet reporting. In addition, Agboola and Salawu (2012) examined the influence of firm size and auditor type on internet financial reporting by commercial banks in Nigeria. Similarly, Mustafa, Salaudeen, and Lasisi (2018) analysed the effect of corporate governance mechanisms on internet financial reporting of listed firms in Nigeria.

Previous studies on internet financial reporting in Nigeria primarily focused on the determinants and corporate governance effects, neglecting to examine the impact of internet financial reporting on financial performance in relation to IFRS adoption. This study aims to address this gap. Furthermore, the investigation of IFRS, which is another aspect of the same issue, has not yet been conducted.

As far as researchers are aware, there is a limited number of studies that specifically examine the impact of internet corporate reporting on financial performance. The relationship between internet corporate reporting and firm financial performance is anticipated to differ between developed and developing countries due to variations in the legal system, cultures, and the effectiveness of the corporate governance structure. Therefore, it is crucial to examine the influence of internet corporate reporting on business financial performance in developing countries, particularly Nigeria, where research is few. This would provide valuable knowledge regarding the effects of internet corporate reporting on firm financial performance.

This study aims to address the existing information gap by examining the correlation between internet corporate reporting and the performance of manufacturing firms listed in Nigeria, taking into account the adoption of International Financial Reporting Standards (IFRS). This study aims to address a gap in the existing literature by investigating the impact of internet corporate reporting on the value of listed manufacturing firms on the Nigeria Stock Exchange (NSE). Specifically, it will analyse the effects on firm value, earnings per share, and return on equity during both the pre and post International Financial Reporting Standards (IFRS) adoption periods.

The main objective of this study is to investigate the effect of internet corporate reporting on financial performance of listed manufacturing firms on Nigeria Stock Exchange (NSE) for both pre and post IFRS adoption periods. Thus, the specific objectives are:

- to determine the effect of internet corporate reporting (ICR) on firm value in pre and post IFRS adoption;

- to determine the effect of ICR on earnings per share in pre and post IFRS adoption; and

- to determine the effect of ICR on return on equity in pre and post IFRS adoption.

Importance of the Research

Online reporting has become indispensable for investors and analysts as a means to rapidly access information and enhance transparency and accountability (Kelton and Yang, 2008). Furthermore, it allows organisations to enhance their flexibility, rapidly convey additional information, and reduce the expenses associated with disclosure. The necessity for further comprehensive scholarly research on ICR in the Nigerian context is underscored by the imperative for Nigerian firms to give greater consideration to the importance of ICR in furnishing relevant information to protect their investors and fulfil their expectations.

The results of this study would assist standard setters and regulatory agencies in Nigeria in developing strategies to promote the disclosure of corporate information by listed firms on the internet. This will attract investors and improve their performance.

Moreover, this study will enhance managers’ understanding of the beneficial impact of sharing their organisational information on the internet. The results of this investigation will be advantageous to the financial experts. The company’s internet resources will enable clients to efficiently collect and analyse information, saving them both time and effort. The study’s results will also attract the attention of global investors, since it demonstrates that corporate information necessary for investment decisions can be readily accessed online, even for enterprises located outside their home country.

REVIEW OF LITERATURES

Conceptual Issues

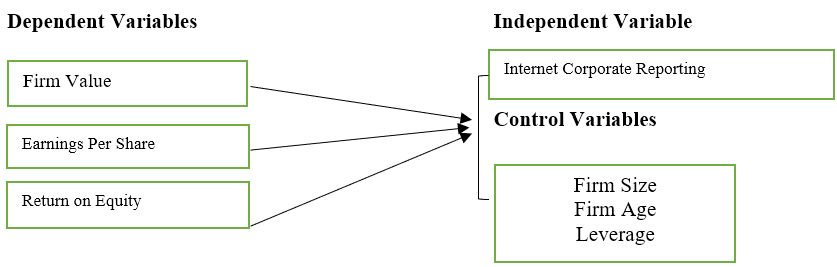

Figure 1 Conceptual Framework

Internet Corporate Reporting

Internet corporate reporting is a sort of voluntary disclosure that firms may choose to engage in. There is no obligation for companies to post information on their websites. The internet serves as a valuable tool for presenting and communicating information to different stakeholders, making it a distinctive means of disclosure (Geerlings et al., 2003). The internet can be defined by numerous attributes. Deller et al. (1999) provides a concise overview of the key characteristics of Internet technology. They state that the Internet offers distinct technological benefits that corporations can utilise to distribute their reports. In addition, the Internet offers various means of direct communication, including mailing lists, feedback forms, and online participation. These tools facilitate convenient communication between stakeholders and enterprises. Furthermore, the company’s website does not provide any conclusive information, as the decision to share information on the internet is optional.

International Financial Reporting Standards

International Financial Reporting Standards (IFRS) are guidelines established by the International Accounting Standard Board (IASB) to assist companies in creating accurate financial statements that provide comprehensive financial and non-financial information (integrated financial reporting) to investors and other stakeholders who rely on them for making economic decisions (Brabec, 2014; de Villiers, Venter, & Hsiao, 2016). The global significance of IFRS implementation has arisen due to the growing international trade and globalisation of the world’s capital market. Several nations, including Nigeria, have implemented accounting rules for the preparation of their financial statements. The guidelines were designed to establish a universal set of regulations for corporate operations, with the goal of enhancing transparency and enhancing the accuracy of financial data for existing and prospective investors. The overarching principle was to ensure that financial statements were comprehensible, comparable, pertinent, and trustworthy in global financial markets. The implementation of International Financial Reporting Standards (IFRS) has several notable advantages. These include enhanced disclosure, transparency, understandability, and comparability of financial statements. As a result, there is a decrease in information asymmetry and an increased willingness of investors to invest (Cameran, Campa, & Pettinicchio, 2014; Donnelly, 2016; Matari, Swidi, & Fadzil, 2014). Enhanced transparency regarding quality information leads to several advantages such as decreased capital expenses, more effective distribution of resources, increased economic growth, improved market efficiency, and enhanced accuracy in analyst forecasts (Matari et al., 2014; Santos, Ponte, & Mapurunga, 2013). Enhanced transparency and accuracy of information augment investors’ evaluation of a company’s financial success and their inclination to increase investment, as the more positive the evaluation, the greater the investments made. Financial performance pertains to the enhancement in a company’s economic activities, as evaluated by its net profit or loss throughout a specific timeframe.

Firm Performance

The study of a company’s performance originates from the fields of organisation theory and strategic management (Harper, 2008). Firm performance is a significant concept in strategic management research and is often employed as a dependent variable. However, there is a lack of agreement over its definition, dimensions, and measurement, despite its significance. The notion of firm performance, as discussed by Yana (2010), has been a contentious topic in finance primarily due to its multifaceted connotations.

Internet Corporate Reporting and Firm Value

The financial statement of the company serves as a means of communication, according to signalling theory, by providing information to users. This information can be taken in either a good or negative manner. Increased disclosure of information by the corporation through Internet Corporate Reporting serves as a signal to investors regarding investment activity. Revealing this information will have an additional influence on the stock price. According to the efficient securities market theory, the price of all traded securities accurately reflects all the information that is currently accessible in the market. The stock price will promptly mirror all accessible facts. As more investors purchase shares due to the release of supplementary information on the internet, the stock price will correspondingly increase. As the stock price increases, so does the perceived worth of the company by investors.

Ashbaugh et al (1999) suggest that a crucial aspect of ICR is the extent or amount of information revealed. There is a direct correlation between the extent of information disclosure and its influence on investors’ investment decisions. The more information is disclosed, the stronger the impact on investors’ decision-making process. In their study, Easley and O’Hara (2004) assert that investors who are provided with more pertinent information have a greater return on their investments. Their demonstration illustrates the impact of both the amount and the calibre of information on stock prices in a state of balance. Hirst and Hopkins (1998) establish that the presentation of a comprehensive income statement to stockholders leads to a greater degree of transparency. This, in turn, allows analysts to assess both earnings management and the fair value of a company’s shares. Furthermore, the internet can expand the range of outlets for disclosing information by integrating multiple websites into a unified reporting system. Every website inside an expanded internet network offers data regarding the operational effectiveness of a local entity, such as a subsidiary, division, or strategic business unit. Hence, an expanded network offers insights not only into the overall performance of the institution, but also into the performance of particular business units.

Internet Corporate Reporting and Earnings per Share

According to the theory of efficient markets, stock prices will only react when valuable information is introduced into the market, assuming that the markets are efficient. This prediction is supported by research conducted by Beaver (1968) and Ball & Brown (1968). According to the generally-accepted idea, valuable information must include two key features. Firstly, it must be relevant to the decision that needs to be made. Secondly, it must be supplied in a timely manner in order to be relevant to the individuals responsible for making the decision. (FASB 980, 2000). In the investment market, valuable information typically prompts investors to take activities that result in a redistribution of investment rewards, so disrupting and resetting the market equilibrium. Beaver (1968) proposed that if a firm’s profit announcement has the potential to influence the firm’s stock price, it can be considered to have information content, indicating valuable information for investors.

Theoretical Framework

After examining the theories, it has been determined that the agency theory and signalling theory are both pertinent and suitable for this study. This study employs agency theory and signalling theory to accomplish its objectives. Agency theory is utilised to disclose both mandatory and voluntary information on the internet, with the aim of mitigating agency problems. On the other hand, signalling theory is employed to reduce information asymmetry and effectively communicate the quality and performance of firms to their market, all at a lower cost.

Empirical Review

In their 2018 study, Mustafa, Salaudeen, and Lasisi examined how corporate governance structures impact the internet financial reporting of listed firms in Nigeria. The study utilised an ex-post facto research approach and applied a stratified sampling strategy to choose a total of 125 companies listed on the Nigeria Stock Exchange. The study utilised panel secondary data obtained from the Investor Relations parts of the corporate websites of the sample organisations, as well as the annual reports of the selected companies. The data covered a five-year period from 2012 to 2016. The data was analysed using ordinary least squares regression. The findings demonstrate a noteworthy and favourable correlation between internet financial reporting and board independence, board size, board competency, and board diligence. Nevertheless, there is no discernible correlation between the gender diversity of the board and internet financial reporting.

The study conducted by Salaudeen and Alayemi (2020) investigates the level of internet integration in business reporting, with a focus on manufacturing companies listed in Nigeria. The population of the research comprises all manufacturing enterprises listed on the Nigerian Stock Exchange. Forty-five out of the total of ninety listed organisations were selected using the purposive sample approach. The primary data were collected from a themed questionnaire that utilises verified scales. The acquired data were analysed utilising both descriptive and inferential statistics. Principal Component Analysis (PCA) was employed as an inferential statistic to assess the degree to which manufacturing enterprises utilise the internet to report their financial and non-financial activities. The results indicate that the manufacturing enterprises listed are currently in the exploratory phase. The internet is utilised as either an additional activity or a supplementary exercise to the traditional print-based company reporting methodology.

In her 2021 study, Putri examined the impact of internet financial reporting procedures on the market value of LQ45 companies listed on the Indonesia Stock Exchange.

The sample for this study consists of 50 LQ45 businesses that are listed on the Indonesia Stock Exchange (IDX) throughout the 2020 term. The study employed purposive sampling to choose a sample of 32 firms. The study utilised a double linear regression analysis as the chosen method for data analysis. The independent variable under consideration is internet financial reporting. The study employs control variables, including company size, profitability, and liquidity. The study’s dependent variables encompass the market worth of the company. The study concludes that internet financial reporting procedures exert a substantial impact on the market value of the company. The firm’s market value is significantly influenced by variables such as control, corporate size, liquidity, and profitability.

Adugna and Kumar (2021) examined the factors that influence the internet financial reporting of enterprises in the Ethiopian insurance and banking sectors. The study utilised cross-sectional data obtained from the central bank of Ethiopia and audited annual reports of commercial banks. The data was analysed using both descriptive and regression analysis methods, namely through the utilisation of STAT Aversion 15 software and the application of the Ordinary Least Square Estimation approach. The OLS regression model findings demonstrate that profitability, size, and ownership structure have statistically significant beneficial impacts on the practice of internet financial reporting. Conversely, this study indicates that liquidity and leverage exert substantial adverse impacts on the internet financial reporting practices of banking and insurance companies in Ethiopia. However, the age and type of business performed have negligible positive and negative effects, respectively, on the internet financial reporting practice.

Research Gap

Most of the studies examining the relationship between internet corporate reporting and firm financial performance have been conducted in developed countries, with only a few studies conducted in developing countries. These studies include those by Adityawarmani (2017), Nazieb, Mahmoud, Ezat, and Elsayed (2010), Chai, Ravenda, and Gesti (2017), Munther and Rekha (2013), Richard and Samuel (2015), Akmalia, Hassan, and Hafizah (2018), Eka (2014), Al-ebrahem (2017), Linda and Dhini (2017), Ahmed, Ghassan, Bruce, and Theresa (2018), and Nel and Baard (2019).

However, this specific component has not been adequately addressed in developing nations, namely in Nigeria. Consequently, this work aims to address this deficiency in the existing literature evaluation.

METHODOLOGY

Research Design

This study employed correlation research design to examine the relationship between the internet corporate reporting and firm performance in pre and post IFRS of listed manufacturing firms in Nigeria. The correlation research design was chosen because the aim of correlation research design is to investigate the relationships between variables and to observe the impact of the independent variable(s) on the dependent variable. It is thus, consistent with the objective of the study. The population of this study consists of the 102 manufacturing firms listed on the Nigerian Stock Exchange as at December, 2018. For the purpose of this study, stratified and random sampling techniques were used considering the sectorial grouping of firms in the stock market. The size of the sample was ascertained based on Taro Yamani Formula. Based on the formula, thirty-one (31) manufacturing firms were selected and their annual accounts for a 10 years period, 2009 to 2013 (pre IFRS) and 2014 to 2018 (post IFRS) adoption periods were used. Data were extracted from the annual reports and financial statements of the selected manufacturing firms on the Nigeria Stock Exchange as at 31 December, 2018 for the period of ten (10) years spanning from 2009 to 2018 of the selected listed firms in Nigeria.

Research model

To test the hypotheses, the model adopted is that of Al-Sartawi and Reyad, (2018), this study then developed and modified the model to specification using internet corporate reporting (ICR) as an independent variable, while firm value (FVAL), earnings per share (EPS), return on equity (ROE) are dependent variables and firm size, firm age and financial leverage as control variables.

Model 1:

FVALit = β0+β1ICRit+ β2FSIZit+β3FAGEit+β4LVRit+εi …. (1)

Model 2:

EPSit = β0+β1ICRit+ β2FSIZit+β3FAGEit+β4LVRit+εi …. (2)

Model 3:

ROEit = β0+β1ICRit+ β2FSIZit+β3FAGEit+β4LVRit+εi …. (3)

Where:

FVALit = Firm value for company in i year t

EPSit = Earnings per share for company in i year t

ROEit = Return on equity for company in i year t

β0 = Coefficient of the constant variable

ICRit = Internet corporate reporting for company in i year t

FSIZit = Firm size for company in i year t

FAGEit= Firm age for company in i year t

LVRit = Leverage for company in i year t

β1, β2, β3, β4 = Regression coefficients of independent variables

εi= error term.

RESULT

Descriptive Statistics

The nature and description of the dependent, explanatory, and control variables such as minimum, maximum, mean, and standard deviation values of pre and post-IFRS adoption models are summarised and presented in table 4.1.

Table 4.1: Summary of Descriptive Statistics

| Pre IFRS Adoption 2009 to 2013 | |||||

| Variables | Mean | Std. Dev. | Maximum | Minimum | No. Obs. |

| FVAL | 252.2229 | 361.0402 | 1729.544 | 0.2806718 | 155 |

| EPS | 0.7125806 | 1.07593 | 8.76 | 0.08 | 155 |

| ROE | 0.5222581 | 0.1962061 | 0.87 | 0.13 | 155 |

| ICR | 76.54355 | 8.275161 | 91.89 | 64.86 | 155 |

| FSIZ | 6.721293 | 1.035531 | 10.32532 | 3.687105 | 155 |

| FAGE | 44.94839 | 22.67466 | 114 | 2 | 155 |

| LVR | 1.270329 | 1.491075 | 11.94 | 0.01 | 155 |

| Post IFRS Adoption 2014 to 2018 | |||||

| Variables | Mean | Std. Dev. | Maximum | Minimum | No. Obs. |

| FVAL | 11714.86 | 63839.16 | 406534.8 | 0.6753468 | 155 |

| EPS | 2.953548 | 4.989058 | 28.08 | 0.02 | 155 |

| ROE | 12.41826 | 8.449895 | 39.31 | 3.15 | 155 |

| ICR | 77.93839 | 8.465366 | 91.89 | 64.86 | 155 |

| FSIZ | 10.09665 | 0.7928137 | 11.7 | 9.03 | 155 |

| FAGE | 49.77419 | 22.63876 | 119 | 7 | 155 |

| LVR | 0.574 | 0.1928885 | 0.95 | 0.13 | 155 |

Source: Output generated from STATA 13 Software.

Note: FVAL is firm value; EPS is earnings per share; ROE is return on equity; ICR is internet corporate reporting; FSIZ is firm size; FAGE is firm age; LVR is leverage.

The descriptive statistics of pre-IFRS adoption period from 2009 to 2013 in table 4.1 reports that firm value has mean of 252.2229 with standard deviation of 361.0402. The minimum and maximum values of share price are 0.2806718 and 1729.544 respectively. However, the minimum and the maximum of earnings per share during pre-IFRS adoption period between the sample manufacturing companies are 0.08 and 8.76 respectively with standard deviation of 1.07593 while the mean value of earnings per share is 0.7125806. The pre-IFRS adoption period from 2009 to 2013 in table 4.1 also shows that the mean of the return on equity of the sampled manufacturing firms is 0.5222581 with standard deviation of 0.1962061, and minimum and maximum values of 0.13 and 0.87 respectively. Moreover, the table 4.1 shows that the average of internet corporate reporting of the sample firms during pre-IFRS adoption is 76.54355 with standard deviation of 8.275161. The minimum and maximum values are 64.86 and 91.89 respectively. Firm size has maximum and minimum values of 10.32532 and 9.03, with a mean value of 6.721293 and a standard deviation of 1.035531 during pre-IFRS adoption. The descriptive statistics of period of pre-IFRS adoption disclose that the firm age has a mean value of 44.94839 and a standard deviation of 22.67466, while the minimum and maximum values of firm size are 2 and 114. Moreover, during pre-IFRS adoption, the leverage has a mean value of 1.270329 and a standard deviation of 1.491075, while the minimum and maximum values of leverage are respectively valued at 0.01 and 11.94.

The summary of descriptive statistics in table 4.1 shows that firm value during post-IFRS adoption has minimum and maximum values of 0.6753468 and 406534.8 respectively, while the results show that firm value has a mean value of 11714.86 and a standard deviation of 63839.16. During post-IFRS adoption, the earnings per share has a mean value of 2.953548 and a standard deviation of 4.989058, while the minimum and maximum values of earnings per share are respectively valued at 0.02 and 28.08. Furthermore, during post-IFRS adoption, the minimum and maximum values of return on equity are 3.15 and 39.31, while the mean and standard deviation values of return on equity remain at 12.41826 and 8.449895 respectively. Internet corporate reporting has maximum and minimum values of 91.89 and 64.86, with a mean value of 77.93839 and a standard deviation of 8.465366 during post-IFRS adoption. The results of table 4.1 during post-IFRS adoption show that 11.7 and 9.03 are the maximum and minimum values of firm size, while the mean and standard deviation values are 10.09665 and 0.7928137 respectively. From the summary of statistics of period of post-IFRS adoption, the firm age has a mean value of 49.77419 and a standard deviation of 22.63876, while the minimum and maximum values of firm size are 7 and 119. Finally, the results of descriptive statistics during post-IFRS adoption reveal that the mean and standard deviation of leverage of sample firms are 0.574 and 0.1928885, respectively, with minimum and maximum values of 0.13 and 0.95.

It is discovered when comparing descriptive statistics of pre and post-IFRS adoption that the mean value of firm value is higher in the post-IFRS than pre-IFRS periods.

Furthermore, the average values of earnings per share, return on equity, internet corporate reporting, firm size, and firm age are greater in case of post-IFRS adoption However, leverage has higher mean values in pre-IFRS adoption period.

Correlation Matrix

The correlation matrix is aimed at assessing the strength and level of the association between and among the variables under investigation. The level of relationship between dependent and independent variables of the study as well as between the independent variables themselves are shown in the correlation matrix. Correlation analysis helps in detecting the degree or extent of relationship among all independent variables, as excessive correlation could lead to multicollinearity, which could consequently lead to misleading findings and conclusions.

Table 4.2: Correlation Matrix of Dependent and Independent Variables

Pre IFRS Adoption 2009 to 2013

| FVAL | EPS | ROE | ICR | FSIZ | FAGE | LVR | |

| FVAL | 1 | ||||||

| EPS | -0.7002 | 1 | |||||

| ROE | -0.1510 | 0.0897 | 1 | ||||

| ICR | 0.1445 | -0.1133 | -0.1004 | 1 | |||

| FSIZ | 0.2011 | -0.1425 | 0.1558 | 0.0009 | 1 | ||

| FAGE | -0.2520 | 0.3236 | 0.2187 | 0.0936 | 0.2966 | 1 | |

| LVR | -0.0212 | 0.1384 | -0.1178 | -0.2308 | -0.0139 | 0.0384 | 1 |

Post IFRS Adoption 2014 to 2018

| FVAL | EPS | ROE | ICR | FSIZ | FAGE | LVR | |

| FVAL | 1 | ||||||

| EPS | -0.0617 | 1 | |||||

| ROE | 0.3574 | -0.0037 | 1 | ||||

| ICR | -0.2817 | 0.2220 | -0.3984 | 1 | |||

| FSIZ | 0.1441 | 0.0553 | 0.5388 | 0.2036 | 1 | ||

| FAGE | -0.1766 | -0.0432 | -0.1371 | -0.0234 | -0.2635 | 1 | |

| LVR | 0.0071 | 0.2960 | -0.0602 | -0.1726 | -0.2006 | -0.0035 | 1 |

Source: Output generated from STATA 13 Software.

Note: FVAL is firm value; EPS is earnings per share; ROE is return on equity; ICR is internet corporate reporting; FSIZ is firm size; FAGE is firm age; LVR is leverage.

During Pre IFRS adoption, 2009 to 2013, the firm age and leverage are negatively correlated with firm value while internet corporate reporting and firm size are positively correlated with firm value. The firm age and leverage are positively correlated with earnings per share while internet corporate reporting and firm size are negatively correlated with earnings per share. However, the correlation analysis reveals that firm size and firm age are positively correlated with return on equity while internet corporate reporting and leverage are negatively correlated with return on equity. The highest correlation between independent variables during Pre IFRS adoption period is 0.2966 and this occurs between firm size and firm age.

For post-IFRS adoption period, the results of correlation analysis in table 4.2 show that the internet corporate reporting and firm age are negatively correlated with firm value while firm size and leverage are positively correlated with firm value. The internet corporate reporting, firm size and leverage are positively correlated with earnings per share while firm age is negatively correlated with earnings per share. Furthermore, the internet corporate reporting, firm age and leverage are negatively correlated with return on equity while firm size is positively correlated with return on equity. The results of correlation analysis show that the highest correlation between explanatory variables is 0.2036 and this exists between internet corporate reporting and firm size. The simple correlation between independent variables should not be considered harmful until it exceeds 0.8 or 0.9 (Judge, Griffiths, Hill, Luthepohl, & Lee, 1985).

Diagnostic Test

Multicollinearity was diagnosed in order to be sure that there was no multicollinearity among the independent and control variables.

Table 4.3: Results of Multicollinearity Test

| Pre–IFRS (2009–2013) | Post–IFRS (2014–2018) | |||

| Variables | VIF | Tolerance | VIF | Tolerance |

| FSIZ | 1.10 | 0.910247 | 1.16 | 0.862671 |

| FAGE | 1.11 | 0.898988 | 1.08 | 0.926702 |

| LVR | 1.06 | 0.941981 | 1.07 | 0.938712 |

| ICR | 1.07 | 0.935023 | 1.06 | 0.939922 |

| Mean VIF | 1.09 | 1.09 | ||

Source: Output generated from STATA 13 Software

Based on the results from table 4.3, it is obvious that the tolerance value for Pre IFRS adoption period is in the amount of 0.910247 to 0.935023 while that of Post IFRS adoption period ranges from 0.862671 to 0.939922, which is above the threshold value of 0.10. The highest VIF value of Pre IFRS adoption period is 1.11 while the highest VIF value of Post IFRS adoption period 1.16, which is less than the threshold value of 10, (Gujarati & Porter, 2009). Since all of the VIF values are below 10, there is no evidence of the existence of multicollinearity between the variables of the study. Thus, the independent variables in this study do not seem to be severely affected by multicollinearity and so a standard interpretation of the regression coefficient can be made.

Summary of Pooled ordinary least square (POLS) Results

The study ran the three models for both Pre IFRS and Post IFRS adoption periods. The Model I analysed the relationship between internet corporate reporting and firm value. The Model II analyse the relationship between internet corporate reporting and return on assets, while the relationship between internet corporate reporting and return on equity was analysed in Model III. The results of three models generated by pooled ordinary least square are presented in table 4.4.

Table 4.4: POLS Estimators of Three Models

Pre–IFRS (2009–2013)

| Model I | Model II | Model III | |||||

| Dependent Variable | Firm Value | Earnings Per Share | Return on Equity | ||||

| No. of Observation | 155 | 155 | 155 | ||||

| F-statistic | 8.22 | 9.22 | 3.96 | ||||

| Prob. > F | 0.0000 | 0.0000 | 0.0044 | ||||

| R-square | 0.1798 | 0.1974 | 0.1955 | ||||

| Adj. R-squared | 0.1580 | 0.1760 | 0.1713 | ||||

| Explanatory

Variables |

Coefficient | Sig. | Coefficient | Sig. | Coefficient | Sig. | |

| ICR | 0.1838276 | 0.015 | -0.012069 | 0.085 | -0.1619848 | 0.052 | |

| FSIZ | 2.421501 | 0.000 | -0.1935157 | 0.001 | 0.7441176 | 0.268 | |

| FAGE | -0.1297865 | 0.000 | 0.0137995 | 0.000 | 0.079834 | 0.010 | |

| LVR | 0.219467 | 0.597 | 0.0453533 | 0.241 | -0.9192363 | 0.046 | |

| (Constant) | 1.636335 | 0.818 | 11.87822 | 0.000 | 31.82214 | 0.000 | |

Source: Output generated using STATA 13 Software.

Note: Level of significance 1%, 5%, 10%

We use Adj. R2 to assess the proportion or percentage of the variation in the dependent variable that is explained by the independent variables within the model. The coefficients of the variables indicate the extent to which the dependent variable will change following any change in independent variables while other variables are held constant.

The coefficients of determination R2 in Model I for Pre–IFRS (2009–2013) shows that the explanatory variables explained approximately 17.98% the changes in firm value as influence internet corporate reporting, firm size, firm age and leverage. Furthermore, the coefficients of determination R2 in Model II for Pre–IFRS (2009–2013) shows that the explanatory variables explained approximately 19.74% the changes in earnings per share as determined by explanatory variables used (internet corporate reporting, firm size, firm age and leverage). Finally, the Model III for Pre–IFRS (2009–2013) revealed a coefficients of determination R2 of 19.55% which is changes in return on equity as determined by explanatory variables (internet corporate reporting, firm size, firm age and leverage).

Table 4.5: POLS Estimators of Three Models

Post–IFRS (2014–2018)

| Model I | Model II | Model III | |||||

| Dependent Variable | Firm Value | Earnings Per Share | Return on Equity | ||||

| No. of Observation | 155 | 155 | 155 | ||||

| F-statistic | 6.09 | 7.66 | 47.85 | ||||

| Prob. > F | 0.0001 | 0.0000 | 0.0000 | ||||

| R-square | 0.1398 | 0.1697 | 0.5606 | ||||

| Adj. R-squared | 0.1168 | 0.1475 | 0.5489 | ||||

| Explanatory

Variables |

Coefficient | Sig. | Coefficient | Sig. | Coefficient | Sig. | |

| ICR | -2429.48 | 0.000 | 0.1587407 | 0.001 | -0.5328353 | 0.000 | |

| FSIZ | 13686.37 | 0.039 | 0.4226683 | 0.403 | 6.913644 | 0.000 | |

| FAGE | -393.0761 | 0.078 | -0.0039648 | 0.816 | 0.0079477 | 0.705 | |

| LVR | -4936.126 | 0.849 | 9.206611 | 0.000 | -0.968248 | 0.693 | |

| (Constant) | 85276.56 | 0.300 | -18.77323 | 0.003 | -15.69785 | 0.045 | |

Source: Output generated using STATA 13 Software.

Note: Level of significance 1%, 5%, 10%

The coefficients of determination R2 in Model I for Post–IFRS (2014–2018) shows that the explanatory variables explained approximately 13.98% the changes in firm value as influence internet corporate reporting, firm size, firm age and leverage. Furthermore, the coefficients of determination R2 in Model II for Post–IFRS (2014–2018) shows that the explanatory variables explained approximately 16.97% the changes in earnings per share as determined by expanatory variables used (internet corporate reporting, firm size, firm age and leverage). Finally, the Model III for Post–IFRS (2014–2018) revealed a coefficients of determination R2 of 56.06% which is changes in return on equity as determined by expanatory variables (internet corporate reporting, firm size, firm age and leverage).

DISCUSSION OF FINDINGS

Internet Corporate Reporting and Firm Value

The results from Model I, obtained through Pooled Ordinary Least Squares analysis in Table 4.4, reveal that internet corporate reporting exhibits a positive coefficient of 0.1838276 with a p-value of 0.015 during the pre-IFRS period. However, during the post-IFRS period, internet corporate reporting demonstrates a negative coefficient of -2429.48 with a p-value of 0.000, which is statistically significant at a level lower than 1%. This study demonstrates a strong positive correlation between internet corporate reporting and the firm value of listed manufacturing companies in Nigeria before the implementation of IFRS. However, it reveals a significant negative correlation between internet corporate reporting and the firm value of Nigerian listed manufacturing firms after the implementation of IFRS. Manufacturing firms in Nigeria tend to provide more information on the internet before the implementation of IFRS to attract potential investors. However, after the adoption of IFRS, manufacturing firms with high market value disclose less information to avoid political attention and the associated pressures for social responsibility and increased regulations, such as price control and higher corporate taxes. The results of this investigation corroborate the conclusions of Mustafa and Lasisi (2018). However, the results of the study contradict the findings of Maryati (2014), which indicated a substantial positive correlation between internet corporate reporting and firm value.

The findings from Model I, as presented in table 4.4, indicate that firm size has a positive and statistically significant impact during both the pre-IFRS and post-IFRS adoption eras. The coefficient for firm size is 0.1838276 (p-value 0.000) in the pre-IFRS period and 13686.37 (p-value 0.039) in the post-IFRS period. These findings indicate that the size of a firm has a notable beneficial impact on the valuation of manufacturing firms listed in Nigeria, both before and after the implementation of IFRS. Consequently, larger companies have a greater likelihood of achieving superior performance by capitalising on economies of scale and leveraging their bargaining power with clients and suppliers. The findings of this research corroborate the findings of Abiodun (2013), who established a statistically significant positive correlation between the size of a corporation and its worth. In contrast to the findings of Maja and Josipa (2012), this analysis reveals a positive and substantial relationship between business size and firm value.

The results from the Pooled Ordinary Least Squares analysis of Model I, as presented in Table 4.4, indicate that firm age has a negative and statistically significant impact during both the pre-IFRS and post-IFRS adoption periods. The coefficients for firm age are -0.1297865 (p-value 0.000) and -393.0761 (p-value 0.078) respectively. Furthermore, the p-values for both coefficients are lower than the 10% level of significance. There is a clear and important negative correlation between the age of a company and its value among manufacturing firms listed in Nigeria, both before and after the implementation of IFRS. This finding suggests that older organisations may have established routines that are disconnected from current market conditions, leading to a negative correlation with firm value. This outcome corroborates the discovery made by Sumaira and Amjad (2013), however it contradicts the findings of Malik (2011), who saw no substantial correlation between the age of a corporation and its worth.

The results obtained from the Pooled Ordinary Least Squares analysis of Model I indicate that the leverage variable had p-values of 0.597 and 0.849 for the pre-IFRS and post-IFRS adoption periods, respectively. With a p-value that exceeds the 10% criterion of significance. This demonstrates that there is no substantial correlation between leverage and the valuation of manufacturing firms listed in Nigeria, both before and after the implementation of IFRS. This finding is consistent with the investigations conducted by Sumaira and Amjad (2013) as well as Daniel and Tilahun (2012). However, this finding contradicts the study conducted by Almajali and Yahya (2012), who discovered a positive correlation between leverage and business value.

Internet Corporate Reporting and Earnings per Share

During the era before the adoption of International Financial Reporting Standards (IFRS), the analysis using Pooled Ordinary Least Squares in Model II indicates that internet corporate reporting has a negative coefficient of -0.012069 and a p-value of 0.085, which is below the 10% significance level. The findings indicate that internet corporate reporting has a detrimental impact on the earnings per share of industrial firms listed in Nigeria prior to the implementation of IFRS. Meanwhile, the findings of the Pooled Ordinary Least Squares analysis for Model II in table 4.4, during the post-IFRS years, indicate that internet corporate reporting has a positive coefficient of 0.1587407. The p-value associated with this coefficient is 0.001, which is lower than the 1% level of significance. The findings indicate that the use of internet corporate reporting has a significant positive impact on the earnings per share of industrial firms listed in Nigeria, following the implementation of International Financial Reporting Standards (IFRS). Consequently, in the investment market, the presence of valuable information typically prompts investors to take activities that result in the redistribution of investment rewards, thereby disrupting and resetting the market’s equilibrium. The present study’s findings corroborate the results of Maryati (2014) as well as Agustina and Suryandari (2017).

During the pre-IFRS adoption periods, the findings from the Pooled Ordinary Least Squares analysis of Model II in table 4.4 indicate that the coefficient for firm size is -0.1935157 with a p-value of 0.001. This suggests that the size of a firm has a negative impact on the earnings per share of listed manufacturing firms in Nigeria prior to the implementation of IFRS. The results following the implementation of IFRS indicate that the coefficient for firm size is 0.4226683, with a p-value of 0.403. This p-value above the 10% significance level. After the implementation of IFRS, the size of a company does not have a major impact on the earnings per share of manufacturing enterprises listed in Nigeria. The outcome corroborates the discovery made by Adams and Buckle (2000) that there is no substantial correlation between the size of a company and its earnings per share. However, the study’s outcome contradicts the findings of Yavaraj and Abate (2013) as well as Daniel and Tilahun (2012).

The results obtained from the Pooled Ordinary Least Squares analysis in Table 4.4, conducted during the pre-IFRS adoption periods, reveal that the variable “firm age” has a positive coefficient of 0.0137995 and a p-value of 0.000. These findings indicate that the age of a firm has a positive impact on the earnings per share of listed manufacturing firms in Nigeria prior to the implementation of IFRS. Subsequent to the implementation of IFRS, the findings indicate that the coefficient for company age is -0.0039648, indicating a negative relationship. The p-value associated with this coefficient is 0.816, which exceeds the 10% significance level. Consequently, this outcome indicates that the age of a company does not have a noteworthy correlation with the earnings per share of manufacturing firms listed in Nigeria during the post-IFRS periods. The conclusions of this study are consistent with the findings of Malik (2011) and Daniel and Tilahun (2012). However, the results of the study contradict the findings of Yuqili (2007), which indicated a statistically significant positive association between the age of a corporation and its earnings per share.

The results of Model II in table 4.4 indicate that there is no significant relationship between leverage and earnings per share of Nigerian listed manufacturing firms during pre-IFRS periods. This is supported by a p-value of 0.241, which is greater than the 10% level of significance. In contrast, the findings from Model II in table 4.4 after the implementation of IFRS revealed that the use of leverage as a control variable resulted in a positive coefficient of 9.206611 and a p-value of 0.000, indicating statistical significance at a level lower than 1%. The presence of a positive coefficient value indicates a statistically significant positive correlation between the leverage and earnings per share of Nigerian listed manufacturing firms following the implementation of IFRS. Financing with debt funds might be regarded as favourable to the shareholder’s return on investment due to the utilisation of tax benefits linked to the borrowed money. The conclusion so corroborates the findings of the study conducted by Daniel and Tilahun (2012). In contrast, the findings of Sumaira and Amjad (2013) which indicated a negative and substantial correlation between leverage and earnings per share are contradicted by the results of the present study.

Internet Corporate Reporting and Return on Equity

The results obtained from the Pooled Ordinary Least Squares analysis of Model III indicate that internet corporate reporting has a negative coefficient of -0.1619848 (with a p-value of 0.052) and -0.5328353 (with a p-value of 0.000) for both the pre-IFRS and post-IFRS adoption periods, respectively. With a p-value that is less than the 10% level of significance. The presence of negative coefficient values suggests a significant negative correlation between internet corporate reporting and the return on equity of listed manufacturing firms in Nigeria, both before and after the implementation of IFRS. This negative significance can be explained based on management’s decision to withhold information regarding the positive firm value and favourable market position, which predicts an increase in shareholder demand for dividends. The outcome of the present investigation aligns with the discoveries of Monday and Nancy (2016). However, this finding contradicts the findings of Aly, Simon, and Hussainey (2010).

The findings from Model III, as presented in table 4.4, indicate that the size of the firm does not have a significant impact on the return on equity of Nigerian manufacturing firms listed during the pre-IFRS periods. This is supported by a p-value of 0.268, which is higher than the 10% significance level. In contrast, the findings from the Model III in table 4.4 revealed that after the adoption of IFRS, firm size had a positive coefficient of 6.913644 and a p-value of 0.000, which is below the 1% level of significance. Consequently, the implementation of IFRS in Nigeria has resulted in a significant and favourable impact of firm size on the return on equity of listed manufacturing enterprises. For each incremental unit of firm size, there will be a corresponding increase of 6.913644 in the return on equity. Large enterprises possess greater capabilities to effectively mobilise additional cash for their depositors, resulting in elevated returns and enhanced performance. The outcome corroborates the conclusions drawn by Srairi (2010) and Eriki and Osifo (2015), however it contradicts the findings of Kosmidou and Pasiouras (2007), who saw an inverse correlation between company size and return on equity.

The results obtained from the Pooled Ordinary Least Squares analysis in table 4.4, conducted during the pre-IFRS adoption periods, reveal that the variable “firm age” has a positive coefficient of 0.079834 and a p-value of 0.010. This indicates that the age of a firm has a positive impact on the return on equity of listed manufacturing firms in Nigeria prior to the implementation of IFRS. During the post-IFRS period, the data indicate that the coefficient value for firm age is 0.0079477, with a p-value of 0.705. This p-value is greater than the 10% significance level. However, this indicates that there is no substantial correlation between the age of a company and its return on equity in Nigerian manufacturing enterprises. The results of this study align with those of Daniel and Tilahun (2012), who also found no statistically significant correlation between age and return on equity. However, these findings contradict the study conducted by Yuqili (2007), which reported a positive and substantial association between age and return on equity.

During the period before the adoption of International Financial Reporting Standards (IFRS), the analysis using Pooled Ordinary Least Squares in Model III indicates that leverage has a coefficient of -0.9192363 and a p-value of 0.046. This p-value is below the 10% significance level. The findings indicate that leverage has a detrimental impact on the return on equity of manufacturing firms listed in Nigeria prior to the implementation of IFRS. Meanwhile, the results from Model III in table 4.4 indicate that the leverage coefficient is -0.968248, and the p-value is 0.693, which above the 10% significance level. This suggests that there is no substantial correlation between debt and return on equity of manufacturing companies listed in Nigeria throughout the periods following the implementation of IFRS. This result contradicts the findings of Daniel and Tilahun (2012), who discovered a statistically significant positive link between leverage and return on equity.

CONCLUSION

After careful analysis and discussion of the findings, the study ultimately concludes that there is a strong and positive correlation between internet corporate reporting and business size with firm value during the pre-IFRS period, as indicated by the results of Model I. The results of Model I indicate a substantial negative association between firm age and firm value during the pre-IFRS period. According to the findings of Model I, the study concludes that leverage does not have a significant impact on company value during the pre-IFRS period. In addition, based on the findings of Model I, it can be inferred that during the time following the implementation of IFRS, internet corporate reporting and firm age have a negative impact on firm value, whereas firm size has a positive and substantial correlation with firm value. The study additionally determines that there is no substantial correlation between leverage and business value.

Furthermore, the analysis indicates that in the time before the implementation of International Financial Reporting Standards (IFRS), internet corporate reporting and firm size exerted a significant negative impact on earnings per share, although firm age exhibited a significant positive association with earnings per share. Moreover, the results of Model II indicate that leverage does not have a major impact on earnings per share in pre-IFRS periods. Consistent with the findings of Model II, the analysis shows that with the implementation of IFRS, there is a substantial positive correlation between internet corporate reporting and leverage with earnings per share. However, firm size and firm age do not have a significant impact on earnings per share.

Based on the findings of Model III, the study concludes that internet corporate reporting has a negative correlation with return on equity during both the pre-IFRS and post-IFRS periods. Additionally, firm size has a positive and significant correlation with return on equity during both periods. Furthermore, it has been determined that the age of the company has a positive and substantial correlation with return on equity before the implementation of IFRS. However, the findings from Model III indicate that both the age of the company and its leverage do not have a significant impact on return on equity after the implementation of IFRS.

RECOMMENDATIONS

According to the findings from Model I (Pre-IFRS) and Model II (Post-IFRS), this study suggests that Nigerian manufacturing companies listed on the stock exchange should continue using the internet to share their financial information with stakeholders. This is because internet corporate reporting has a positive impact on the value of these companies in Nigeria.

Based on the findings from Model I (Pre-IFRS) and Model II (Post-IFRS), it is advisable for the management of Nigerian quoted manufacturing companies to utilise the internet as a means of communication with stakeholders. This will enhance the value of their earnings per share and improve their prospects in the market.

Consistent with the findings of Model I (Pre-IFRS) and Model II (Post-IFRS), the study also suggests that listed manufacturing firms in Nigeria should use the internet to communicate corporate financial information to stakeholders. This is expected to lead to a future increase in the return on equity shares.

Furthermore, the management of publicly traded manufacturing companies in Nigeria should enhance their stakeholder engagement strategies and optimise their websites to offer stakeholders a comprehensive range of pertinent financial information. Effectively harnessing the power of the internet can foster competitiveness and serve as a remedy for improving corporate performance and facilitating growth.

Furthermore, individuals in the accounting field should prioritise and promote the enhancement of augmented content, enhanced accessibility, enhanced verification, and more advanced use of the website as a means of receiving feedback. Companies can improve their capacity to engage in bi-directional communication with a wider array of prospective stakeholders.

Regulatory bodies like the Financial Reporting Council of Nigeria (FRCN) and the Nigeria Stock Exchange (NSE) should establish guidelines for disclosing information online. This will enhance transparency and make it compulsory for listed manufacturing companies in Nigeria to disclose their financial reports on the internet.

REFERENCE

- Abate, G. (2012). Factors affecting profitability of insurance company in Ethiopia: panel evidence. Thesis Submitted to the Department of Accounting and Finance Addis Ababa University, Ethiopia.

- Abd-elsalam, O. H. (1999). The introduction and application of international accounting standards to accounting disclosure regulations of a capital market in a developing country: The case of Egypt. Unpublished Ph.D. Thesis, Herriot-Watt University, Edinburgh, UK.

- Adams, M., & Buckle, M. (2000). The determinants of operational performance in the Bermuda insurance market. Applied Financial Economics, 13, 133-143.

- Adebimpe, O. U. & Ikenna, E. A. (2013). Internet financial reporting and company characteristics: A case of quoted companies in Nigeria. Research Journal of Finance and Accounting, 4(12), 72-80.

- Adugna, B.M. & Kumar, B. (2021). Determinants of internet financial reporting: In the case of Ethiopian insurance and banking sector companies. Innovations, 66, 760-778.

- Adhikari, A. & Tondkar, R. H. (1992). Environmental factors influencing accounting disclosure requirements of global stock exchanges. Journal of International Financial Management and Accounting, 4(2), 75-105.

- Adityawarman, A., & Khudri, T. B. Y. (2018). The impact of internet financial reporting practices on the company’s market value: a study of listed manufacturing companies in Indonesia. Advances in Economics, Business and Management Research, 55, 48–53. https://doi.org/10.2991/iac-17.2018.9

- Agboola, A. A., & Salawu, M. K. (2012). The determinants of internet financial reporting: Empirical evidence from Nigeria. Research Journal of Finance and Accounting. 3(11), 95 – 105.

- Agustina, L. & Suryandari, D. (2017). Financial performance and firm value: does internet financial reporting moderate the relationship in Indonesian manufacturing companies? Proceedings of INTCESS 2017 4th International Conference on Education and Social Sciences, 6-8, 305-309.

- Akeelof, G. A. (1970). The market for “LEMONS”: quality uncertainty and the market mechanism. Quarterly Journal of Economics, 84, 488-500.

- Al Arussi, A. S., Selamat, M. H., & Hanefah, M. M. (2011). The determinants of internet financial disclosure: The perspective of Malaysian listed companies. International Journal of Management Studies (IJMS), 18(1), 1-29.

- Alchian, A.A. & Demsetz, H. (1972). Production, information costs, and economic organization. American Economic Review LXII, no. 5 (December): 777-795.

- Alebrahem, N. (2017). Internet corporate reporting, firm characteristics, corporate governance and firm financial performance of Saudi listed companies. Unpublished Ph.D. Thesis, University of Plymouth.

- Alexander, D. & Archer, S. (1995). European Accounting Guide (2nd ed.). Hartcourt Brace & Company: New York, US.

- Al-htaybat, K. (2005). Financial disclosure practices: Theoretical Foundation, and an Empirical Investigation on Jordanian Printed and Internet formats. Unpublished Ph.D. thesis, University of Southampton, UK.

- Almajali, A., & Yahya, Z. (2012). Factors affecting the financial performance of Jordanian insurance companies listed at Amman Stock Exchange. Macro think institute, journal of management research, 4(2).

- Aly, D., Simon, J. & Hussainey, K. (2010). Determinants of internet corporate reporting: Evidence from Egypt. Managerial Auditing Journal, 25(2), 182-202.

- Arnold, B. & De Lange, P. (2004) Enron: an examination of agency problems. Critical Perspectives on Accounting, 15,751-765.

- Ashbaugh, H., Johnstone, K. & Warfield, T. (1999). Corporate reporting on the Internet. Accounting Horizons, 13(3), 241-257.

- Bakos, J. Y. (1991). A strategic analysis of electronic marketplaces. MIS Quarterly, 15(3), 295-310.

- Beaver, W. H. (1968). The information content of annual earnings announcements. Journal of Accounting Research, 6, 67-92.

- Bharadwaj, A. S., Bharadwaj, S. G., & Konsynski, B. R. (1999). Information technology effects on firm performance as measured by Tobin’s q. Management Science, 45(7), 1008-1024.

- Blair, M. M. (1995) Ownership and control: Rethinking corporate governance for the twenty-first century. The Brookings Institution, Washington, DC, US.

- Bolivar, M. P. R. & Garcia, B. S. (2004). The corporate environmental disclosures on the internet: the case of IBEX 35 Spanish companies. International Journal of Accounting, Auditing and Performance Evaluation, 1, 215-266.

- Brynjolfsson, E. & Hitt, L. (1996). Paradox lost? Firm-level evidence on the returns to information systems spending. Management Science, 42(4), 541-558.

- Chao, C. F., Hsu, C. C., & Yeh, H. S. (2010). The relationship between information transparency and firm value: Evidence from Taiwan. International Journal Business Excellence, 3(2), 125-141.

- Cho, H. J., & Pucik, V. (2005). Relationship between innovativeness, quality, growth, profitability, and market value. Strategic Management Journal, 26(6), 555-575.

- Chow, C. W. & Wong-Boren, A. (1987). Voluntary financial disclosure by Mexican corporations. Accounting Review, 62, 533-541.

- Cooke, T. E. (1989). Voluntary disclosure by Swedish companies. Journal of International Financial Management and Accounting, 1, 1-25.

- Cooke, T. E. (1993) Disclosure in Japanese corporate annual reports. Journal of Business Finance and Accounting, June, 521-536.

- Copeland, T. E. & Galai, D. (1983) Information effects on the bid-ask spread. Journal of Finance, 38, 1457-1469.

- Craswell, A. & Taylor, S. (1992) Discretionary disclosure of reserves by oil and gas companies: An economic analysis. Journal of Business Finance and Accounting, 19, 295-308.

- Craven, B. M. & Marston, C. L. (1999). Financial reporting on the internet by leading UK companies. The European Accounting Review, 8(2), 321-333.

- Deegan, C. (2002). Introduction: The legitimising effect of social and environmental disclosures -a theoretical foundation. Accounting Auditing & Accountability Journal, 15, 282-311.

- Deller, D., Stubenrath, M. & Weber, C. (1999). A survey on the use of the internet for investor relations in the USA, the UK, and Germany. The European Accounting Review, 8(2), 351–364.

- Demski, J. (1974). Choice among financial reporting alternatives. The Accounting Review, 49, 221-232.

- Diamond, D. W. & Verrecchia, R. E. (1991). Disclosure, liquidity and the cost of capital. The Journal of Finance, 46(4), 1325 – 1359.

- Gigler, F. (1994). Self-enforcing voluntary disclosures. Journal of Accounting Research, 32, 224-240.

- Gray, R., Owen, D. & Adams, C. (1996). Accounting and accountability. Prentice Hall Europe, Essex, UK.

- Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics (5th ed.). Boston, MA: McGraw-Hill.

- Hackston, D. & Milne, M. J. (1996). Some determinants of social and environmental disclosures in New Zealand companies. Accounting, Auditing & Accountability Journal, 9(1), 77-108.

- Haddad, A. E. (2005). The impact of voluntary disclosure level on the cost of equity capital in an emerging capital market: The case of the Amman Stock Exchange. Unpublished Ph.D. Thesis, East Anglia, UK.

- Haniffa, R. & Cooke, T. (2005). The impact of culture and governance on corporate social reporting. Journal of Accounting and Public Policy, 24(5), 391-430.

- Healy, P. M. & Palepu, K. G. (2001) Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31, 405-440.

- Hossain, M., Tan, M. L. & Adams, M. B. (1994). Voluntary disclosure in an emerging capital market: Some empirical evidence from companies listed on the KLS. The International Journal of Accounting, 29, 334-351.

- Howitt, D. & Cramer, D. (2005). Introduction to Statistics in Psychology, (3rd): Pearson Education Limited, Essex, UK.

- Jensen, M. C. & Meckling, W. H. (1976). Theory of the firm: Managerial behaviour, agency costs, and ownership structure. Journal of Financial Economics, 3, 305-360.

- Jones, M. J. & Xiao, J. Z. (2003). Internet reporting: current trends and trends by 2010. Accounting Forum, 27(2), 132-165.

- Jonker, J. & Foster, D. (2002) Stakeholder excellence? Framing the evolution and complexity of a stakeholder perspective of the firm. Corporate Social Responsibility and Environmental Management, 9, 187-195.

- Ibrahim, K, (2015). The impact of firm characteristics on IFRS 8 disclosure in the transition period in Nigeria. International Journal of Economic Sciences, 4(4), 1-13.

- Kelton, A. S., & Yang, Y. W. (2008). The impact of corporate governance on internet financial reporting. Journal of Accounting and Public Policy, 27(1), 62- 87.

- Khan, M. N. A. A. & Ismail, N. A. (2011). The level of internet financial reporting of Malaysian companies. Asian Journal of Accounting and Governance, 2, 27-39.

- Lai, S. C., Lin, C., Li, H. C., & Wu, F. H. (2010). An empirical study of the impact of internet financial reporting on stock prices. The International Journal of Digital Accounting Research, 10, 1-26.

- Liargovas, P., & Skandalis, K. (2008). Factor affecting firm‟s financial performance: The Case of Greece, University of Peloponnese.

- Lumpkin, G., &. Dess, G. (1999).Linking two dimensions of entrepreneurial orientation to firm performance: The moderating role of environment, firm age, and industry life cycle. Journal of Business, 76, 150-167.

- Majumdar, S. (1997). The Impact of Size and Age on Firm-Level Performance: Some Evidence from India Review of Industrial Organization, 12, 231–241.

- Malik, H. (2011).Determinants of Insurance Companies Profitability: An Analysis of Insurance Sector of Pakistan, Academic Research International, 1(3), 315-321.

- Marston, C. & Leow, C. Y. (1998). Financial reporting on the internet by leading UK companies. The 21st Annual Congress of the European Accounting Association Antwerp. Belgium, 6-8 April.

- Marston, C. (1996). The organization of the investor relations function by the large UK quoted companies. International Journal of Management Science, 24(4), 477-488.

- Marston, C. (2003). Financial reporting on the internet by leading Japanese companies. Corporate Communication: An International Journal, 8(1), 23-34.

- Marston, C., & Polei, A. (2004). Corporate reporting on the internet by German companies. International Journal of Accounting Information Systems, 5(3), 285-311.

- Maryati, E. R. (2014). The effect of Internet Financial Reporting (IFR) on firm value, stock price, and stock return in the manufacturing companies listed in Indonesia Stock Exchange. The Indonesian Accounting Review, 4(1), 71–80.

- Mckinnon, J. & Dalimunthe, L. (1993). Voluntary disclosure of segment information by Australian diversified companies. Accounting and Finance, May, 31, 33-50.

- Meek, G. K. & Gray, S. J. (1989). Globalization of stock markets and foreign listing requirements voluntary disclosures by continental European companies listed on the London stock exchange. Journal of International Business Studies, summer, 316-336.

- Mohamed, E. K., Oyelere, P. & Al-Busaidi, M. (2009). A survey of internet financial reporting in Oman. International Journal of Emerging Markets, 4(1), 56-71.

- Monday, I. I. & Nancy, A. (2016). Determinant of voluntary disclosure quality in emerging economies: Evidence from firms listed in Nigeria Stock Exchange. International Journal of Research in Engineering & Technology, 4(6), 37-45.

- Morris, R. D. (1987). Signalling, agency theory & accounting policy choice. Accounting and Business Research, 18, 47-56.

- Mueller, G. G., Gernon, H. & Meeh, G. K. (1987). Accounting: An international perspective. IRWIN, Illinois, US.

- Murdayanti, Y., & Ali Khan, M.N.A. (2021). The development of internet financial reporting publications: A concise of bibliometric analysis. Heliyon,7, 1-12.

- Mustafa, M.O.A & Lasisi, T.K. (2018). Determinants of internet financial reporting: Evidence from selected companies listed on Nigeria stock exchange. International Journal of Innovative Research and Advanced Studies, 5(1), 232-241.

- Mustafa, M.O.A., Salaudeen, Y.M., & Lasisi, T.K. (2018). Corporate governance mechanism and internet financial reporting of listed companies in Nigeria. Research Journal of Finance and Accounting, 9(14), 90-101.

- Myers, S. C. (1984). The capital structure puzzle. The Journal of Finance, 39(3), 575- 592.

- Oyelere, P., Laswad, F. & Fisher, R. (2003). Determinants of internet financial reporting by New Zealand companies. Journal of International Financial Management and Accounting, 14(1), 26-63.

- Pi, L., & Timme, G. (1993). Corporate control and bank efficiency.Journal of Banking and Finance, 17, 515-530.

- Puspitaningrum, D., & Sari, A. (2012). Corporate governance mechanism and the level of internet financial reporting: Evidence from Indonesian companies. Procedia Economics and Finance, 2, 157-166.

- Putri, D.A. (2021). The influence of internet financial reporting on the market value of case study companies on LQ45 companies listed on the Indonesia stock exchange. Proceedings of the 5th International Conference on Sustainable Innovation (ICOSI), 9-14.

- Rawy, A. A. (2004). Financial reporting and contemporary changes in the Egyptian environment. Unpublished Ph.D. Thesis, University of Hull, UK.

- Richard T. Fisher & Samuel T. Naylor (2015): Corporate reporting on the internet and the expectations gap: new face of an old problem, Accounting and Business Research, 1-25.

- Ross, S. (1979). Disclosure regulation in financial markets: Implications of modern finance theory and signaling theory. IN EDWARDS, F. (Ed.) Issues in financial regulation. McGraw-Hill, New York, US.

- Ruland, W., Tung, S. & George, N. (1990). Factors associated with the disclosure of managers’ forecasts. Accounting Review, 65,710-721.

- Salawu, M. K. (2013). The extent and forms of voluntary disclosure of financial information on the internet in Nigeria: An exploratory study. International Journal of Financial Research, 4(1), 110–119.

- Salawu, R. (2009). Financial reporting on the internet by quoted companies in Nigeria. Repositioning African Business and Development for the 21st Century.

- Salaudeen, H.A & Alayemi, S.A. (2020). The level of internet adoption in business reporting: the Nigerian perspectives. International Journal of Applied Business Research, 2(2), 107-121.

- Salewski, M., Teuteberg, T., & Zülch, H. (2016). Short-term and long-term effects of IFRS adoption on disclosure quality and earnings management. Corporate Ownership & Control, 13(2),

- Sanni, M. R., Akinpelu, Y. A., Fatona, L. A. & Olatunde, J. O. (2009). ‘Internet financial reporting by commercial banks in Nigeria. Economic and Policy Review, 15(4).

- Shehata, N. F. (2014). Theories and determinants of voluntary disclosure. Accounting and Finance Research, 3(1), 18-26.

- Sia, C, J., Rayenda Brahmana, R., & Memarista, G. (2017). Internet corporate reporting and firm performance: Evidence from Malaysia. Contemporary Economics, 12(2), 153-164.

- Skinner, D. (1994). Why firms voluntarily disclose bad news. Journal of Accounting Research, 32, 38-60.

- Smith, B. & Pierce, A. (2005). An investigation of the integrity of internet financial reporting. International Journal of Digital Accounting Research, 5(9), 47-78.

- Solomon, J. (2007). Corporate governance and accountability. (2nd ed.). John Wiley & Sons, Chichester, UK.

- Sternberg, E. (1997). The defects of stakeholder theory. Corporate governance: An international review, 5, 3-10.

- Sumaira, B., & Amjad, T. (2013). Determinants of profitability panel data evidence from insurance sector of Pakistan. Elixir Financial Management International Journal, Pakistan.

- Sushila, S & Amol, D. (2016). A study of corporate web-based reporting in hotel industry. Asian Economic and Financial Review, 6(11), 661-680.

- Swiss Re. (2008). World insurance in 2007: emerging markets leading the way. Zurich: Sigma, 3.

- Tahat 1, Y., Dunne, T., Fifield, S., & Power, D. (2016). The impact of IFRS 7 on the significance of financial instruments disclosure: Evidence from Jordan. Accounting Research Journal, 29(3), 1-49.

- Verrecchia, R.E. (1983). Discretionary disclosure. Journal of Accounting and Economics, 5(3), 179-194.

- Wachira, M., 2019. Corporate governance and corporate risk reportings: An empirical study of listed companies in Kenya. African Journal of Business Management, 13(17), 572-578.

- Wagenhofer, A. (2003). Economic consequences of internet financial reporting. Schmalenbach Business Review, 55(4), 262–279.

- Wallace, R. S. O., Naser, K. & Mora, A. (1994). The Relationship between the comprehensiveness of corporate annual reports and firm characteristics in Spain. Accounting and Business Research, 25, 41-53.

- Xiao, J., Yang, H. & Chow, C. (2004). The Determinants and characteristics of voluntary Internet-based disclosures by listed Chinese companies. Journal of Accounting and Public Policy, 23(3), 191-225.

- Yusuf (2013). Internet corporate financial reporting: A study of quoted Nigerian companies. African Journal of Accounting, Auditing, and Finance, 2(3) 233-259.