Forensic Accounting: Investigate Fraud Cases or Develop Fraud Prevention Strategies in Oman Listed Companies

- Haitham Nasser Hamed Al Hasani

- Afnan Talib Nasser Al Wahibi

- Marah Said Mubarak Al Zuhaibi

- Dr. Shahnawaz Ali

- 1163-1174

- Jun 7, 2024

- Accounting

Forensic Accounting: Investigate Fraud Cases or Develop Fraud Prevention Strategies in Oman Listed Companies

Haitham Nasser Hamed Al Hasani, Afnan Talib Nasser Al Wahibi, Marah Said Mubarak Al Zuhaibi, Dr. Shahnawaz Ali

Oman College of Management and Technology, Oman

DOI : https://dx.doi.org/10.47772/IJRISS.2024.805081

Received: 29 April 2024; Accepted: 07 May 2024; Published: 07 June 2024

ABSTRACT

Forensic accounting makes use of concepts and methods that date back centuries. The economy, society, and laws are just a few of the factors that have formed the profession in our ever-changing world. Accounting fraud has been more common in the international corporate sector in recent years. Because businesses are still relatively new and lack experience in managing their accounts, there are now undiscovered opportunities for those who commit accounting fraud. The public’s opinion of the many fraudulent operations that occur in the nation has also been negatively impacted by this. As a result, this article looks at how the general public feels about fraud detection, which is important for company expansion. The literature study on the public’s acceptance of fraud detection is the paper’s unique selling point. The significance of fraud detection for bolstering and competing in the business is outlined in this article.

INTRODUCTION

The tripartite practice of using accounting, auditing, and investigative abilities to support legal matters is known as forensic accounting. The accounting specialty practice area pertains to engagements that arise from disputes or litigation, whether they are real or predicted. The science of forensic accounting deals with the relationship and application of knowledge in finance, accounting, taxation, and auditing to evaluate, look into, question, test, and examine issues related to criminal law, civil law, and jurisprudence. Therefore, forensic accounting can be considered a part of accounting that is appropriate for judicial scrutiny, providing the highest degree of certainty and carrying the generally accepted meaning of having been determined using scientific means. The fastest-growing area of accounting at the moment is forensic accounting. Forensic accounting is not new, despite its recent rise to prominence. Although forensic accounting as a profession was relatively unknown until a number of high-profile corporate scandals and stricter reporting and internal control regulations highlighted its significance to the business world, its roots can be traced back to Glasgow, Scotland in the early 1800s. According to Wallace (1991), forensic accounting was typically kept out of the public eye until recently when it emerged as a legitimate and expanding source of revenue from the investigative department. More than just accounting or detective work, forensic accounting is a combination that will be needed as long as people are there.

Problem statement

With the number of listed companies increasing in Oman, it is of high importance that fraud is detected and controlled in these companies. Despite all Accounting standards, still there are increasing fraudulent cases in Oman and around the world. This research aims to identify the fraud cases and suggest fraud prevention strategies in Oman Listed companies.

Research Question

- What is the objective behind fraud cases in Oman?

- Is there a role for forensic accounting in reducing financial and administrative corruption in Omani public shareholding companies?

- what are the strategies of forensic accounting to fraud prevention in Oman?

- How the frauds happened in earlier cases despite stringent standards and controls in place?

Research objectives

- To find the reasons of fraud in Omani Companies.

- A role for forensic accounting in reducing financial and administrative corruption in Omani public shareholding companies.

- To find out the strategies to reducing fraud cases in Omani Companies.

Scope of the study

Most companies in various countries of the world face fraud problems, Fraud risk assessment and the preventative function of forensic accounting are regarded as fraud preventive measures. This study also suggested that the association between effective corporate governance and fraud risk assessment is mediated by the preventive role of forensic accounting. So, this research focuses only fraud cases in Oman listed Companies.

Significance of the study

The importance of the study stems from the fact that it is one of the first studies, to the researcher’s knowledge, that will address a topic that is relatively new to the accounting profession in Oman, which is forensic accounting. Its importance also lies in timing. It comes during a period in which the phenomenon of financial and administrative corruption in Omani public shareholding companies has increased, which has resulted in serious damage that has not only affected the shareholders of those companies, but also affected other stakeholders, and indeed society in general. Hence, the results targeted by this study will serve many of the categories that use published financial data to make decisions and whose interest is to rid those data of the effects of fraud and fraud intended to mislead those groups. It will also serve the control and supervision bodies that seek to raise their standard.

Limitation of the study

Our research study is limited to Omani companies, to Investigate fraud cases we collected information by using firms in Muscat stock exchange. The other limitations include time limitations, as we had very less time to complete this research. Resources were also a constraint while conducting this research.

LITERATURE REVIEW

Forensic accounting is a specialized area of accounting focused on investigating financial fraud and providing litigation support for legal cases. It is a challenging and challenging profession that requires a deep understanding of accounting principles, investigation techniques and legal procedures. Forensic accountants are often hired by both public and private organizations to investigate financial crimes such as embezzlement, money laundering, and securities fraud. They also provide expert testimony in court cases, whose findings and opinions can have a significant impact on the outcome of the trial.

Forensic Accounting

You’ll probably get two different answers if you ask any two working forensic accountants to define what forensic accounting is. Although both answers might be true and there might be some overlap, there isn’t a single, accepted response given by all accountants who work in this particular field of specialization. The answers given will mostly rely on each forensic accountant’s unique history, expertise, and areas of practice. Definitions of forensic accounting frequently list fraud, fraud prevention, and fraud investigations as the forensic accountant’s responsibilities. Although those definitions don’t always provide the right meaning, they only define forensic accounting in relation to fraud. Even more books about forensic accounting have been created, with a lot of them focusing on fraud schemes and offering a plethora of information on both preventing and investigating them. This is the situation with Golden, Skalak, and Clayton’s A Guide to Forensic Accounting Investigation. Although the book is a great resource and I use it extensively in my University of Connecticut adjunct professor class, there is a problem with the title: it should say A Guide to Forensic Accounting Investigation, not A Guide to Fraud Investigation. There exist numerous other settings beyond fraud where forensic accounting can be applied, making fraud just one of the many situations in which its talents can show to be quite helpful. According to Hopwood, Leiner, and Young, the definition of Forensic Accounting:

“Forensic accounting is the application of investigative and analytical skills for the purpose of resolving financial issues in a manner that meets standards required by courts of law. Forensic accountants apply special skills in accounting, auditing, finance, quantitative methods, certain areas of the law, research and investigative skills to collect, analyze and evaluate evidential matter and to interpret and communicate findings.” (W.S. Hopwood, J.J. Leiner, and G.R. Young,2008)

Forensic Accounting Fraud

The deliberate fraud of the truth with the purpose to deceive or manipulate a business or individual is referred to as fraud in legal terminology. Senior management fraud may be engaged when businesses experience severe financial difficulties and declare bankruptcy. The deliberate falsification of accounting records, such as cost or sales records, to increase net income or sales figures is known as accounting fraud. Accounting fraud is prohibited and can result in civil actions against the company and the individuals involved. Accounting fraud is a tactic used by company authorities to cover up losses or make sure they fulfill public or shareholder expectations for profits.

According to David (2005), fraud is a probability rather than a possibility. It also illustrates how judgments made by a group rather than an individual can help prevent fraud. This isn’t the case, though, if everyone in the group is working for the same goal. Then, fraud might not be stopped. On the other hand, the group is influenced by the dominating decision maker who makes all of the final decisions. The writers also claim that fraud is occurring in a particular company because of the paper-based approach. The authors conclude that fraud would decrease if every transaction was conducted through a computerized system. But in reality, even a big business-like Enron was discovered to have engaged in fraud. This is due to the fact that high level management may always access data and alter it, whether it is in a digital or paper-based system. All of this is related to high level management and human nature. The public needs to be made aware of the purpose and application of forensic accounting in order to stop fraud from happening. This is the only way to resolve the problem. Once the general public is informed about the idea, they may really ask the company they invest in to provide the service. (David, A.,2005).

According to Albrecht (2005), fraud is rarely observed. On the other hand, fraud indications are typically noticed. The symptoms may be the result of errors; thus, they may not always indicate that fraud is occurring. The major advice is to exercise caution when fraud is reported because it can involve unfounded claims. Since fraudsters position themselves in a protected place where authorities cannot punish them, fraud is not easily demonstrated. And the defaulter may defend these blunders and errors by pointing to them as the cause of the fake symptoms. This remark can be agreed upon, but to what extent may it be justified? This has made it more difficult for forensic accountants to identify and prove fraud. A more thorough understanding of how these defaulters carry out their fraudulent acts is required. Fraud cases will be difficult to identify without ongoing public involvement and advancements in forensic accounting. This will increase the likelihood of financial fraud and result in a failure to live up to stakeholder, public, and shareholder expectations. (Albrecht, W.S., 2005).

Forensic Accounting Function

The two main areas of work for forensic accountants are litigation support and investigative accounting, according to Moncliff (2005) in the article “Forensic Accounting.” Investigative accounting takes into account a company’s business environment in addition to its numbers and documentation. Inquiring into an organization’s financial activities, forensic accountants compile data that could be utilized in a criminal or civil trial. Investigative services and litigation support are offered by forensic accountants. This illustrates what a forensic accountant does. It explains in detail the many goals of forensic accounting. It is well acknowledged that the forensic accounting method is an investigative auditing technique requiring a high level of expertise and experience. When conducting a fraud investigation, a corporation should offer forensic accounting as a service that may be obtained. It needs to be the primary resource for every fraud inquiry. It is possible to act in the best interests of the entire organization because it is an independent service free from conflicts of interest. It ought to be employed as a mechanism to keep an eye on the business’s everyday operations in order to minimize fraud. Since the business sector is still in its infancy, fraud is an issue that is only get worse. Forensic accounting procedures are now more important than ever for both medium-sized and large businesses. The most important defense against financial fraud is forensic accounting. Organizations and even government agencies should have the chance to inform the public about the primary duties of forensic accounting.

Additionally, the European Federation of Accountants (FEE) (2002) provided an overview of the function of auditing and accounting in Europe. As the European representative organization for the accounting profession, they are aware that the sudden demise of a significant business listed on a stock exchange will compromise the veracity and accuracy of the data as well as the regulatory framework that is in place to safeguard investors. This demonstrates that even a well-known business, like Enron, could fail due to its involvement in billion-dollar corporate scandals. Moreover, they think that in order to give the capital markets the best possible financial data, corporate governance structures must be strengthened. An established accounting and auditing firm is then needed to prepare the financial data. Despite robust corporate governance and financial data supplied by reputable accounting and auditing firms, business scandals continue to occur. The public’s continued mistrust of the management and the corporation itself stems from the realization that these issues will never be completely resolved. Forensic accounting ought to be used as the primary instrument for looking into organizations that have committed fraud because of this. This allows the public’s interests to be served without them having to worry about losing everything.

Forensic Accounting Education

Only a few universities presently provide forensic accounting courses, and the majority of forensic accounting education has been restricted to continuing professional education programs for working accountants (Rezaee & Burton, 1997). It is reasonable for college or university accounting departments to offer and incorporate forensic accounting as one of the course options, given the current demand for forensic accounting practice and the need for greater knowledge in this field. This is to make sure that fresh graduates can function as effectively and efficiently as experienced auditors, or at the very least, fulfill the requirements of a practicing forensic accountant, in addition to auditors with extensive expertise in the field. In addition, those who do not enroll in professional accounting courses ought to have the chance to learn more about forensic accounting. This will raise public and student understanding of the use of forensic accounting as a key instrument in the examination of financial statements from companies that may contain fraudulent activity.

Responses to a survey given to auditors and undergraduate business students were gathered both before and after the students’ coursework was finished. After completing the curriculum, the students’ perceptions of auditors in the field of auditing were more similar, especially when it came to the tasks and responsibilities of auditors; yet there were still indications of the expectation difference when it came to fraud. But compared to before the students were set to begin the audit coursework, the disparity was smaller. Therefore, audit education may still be seen as a useful strategy for closing the expectation gap. This is an idea wherein one would use the educational system to improve a concept’s perception and comprehension. It is a given that if surveys on forensic accounting perceptions are conducted both before and after forensic accounting training, education will be regarded as one of the most successful strategies for enhancing public perceptions of the usage of forensic accounting services.

Any campaign aiming at narrowing the expectation gap would heavily emphasize the education process. To avoid misunderstandings, it is crucial to educate the general audience. Over the course of the semester, auditing students’ perceptions of the duties of auditors, the accuracy of audited financial data, and their prospects for the future saw substantial shifts. Smither came to the conclusion that closing the expectation gap can be accomplished through education. This is why, in order to truly know how to enhance it, it is necessary to show how the general public views and understands the role that forensic accounting plays in the corporate sector.

Audit and risk committee

The people who oversee SM’s robust and effective internal control and risk management systems, which are designed to protect the organization’s assets and the interests of its shareholders, are known as ARC. A crucial part of establishing corporate governance and achieving GCG is played by ARC. The regulatory responsibilities of ARC and their collaborative efforts with other corporate governance components—such as the board of directors, SM, internal auditors, and external auditors—are critical to the organization’s performance. There are no prerequisites for ARC establishment, however according to CMA (2016), members of the organization must be independent individuals who sit on the board of directors. There should be a minimum of three ARC members who are experts in fraud, auditing, and accounting. The primary responsibilities of ARC for the accomplishment of GCG are anti-fraud program oversight and financial policy approval recommendations. Additionally, the quantity and frequency of the ARC’s productive sessions determine how effective it is (Shir, 2013). ARC meetings should be run in a way that addresses and represents the needs of the business and all related requirements. Successful ARC meetings can improve corporate governance and lower organizational risk, both of which can eventually result in GCG accomplishment.

In addition to providing direct reports to the board of directors, ARC discloses internal control in the financial statements of the company. ARC handles issues including making sure that strategic plans are in line with corporate goals, handling finances and risk management, conducting internal and external audits, and maintaining performance transparency. Moreover, Efiong (2012) and Abbot, Park, and Parker (2000) conclude that the present ARC lowers the factors of fraud and helps to improve corporate governance. In order for ARC to fulfill its role and help achieve GCG, both internal and external auditors must report directly to ARC. The audit reports and any associated conclusions or observations should be formally discussed by the ARC and SM. Following these discussions, SM was compelled to put internal and external auditors’ suggestions into practice, which eventually decreased risk and enhanced organizational performance. The ARC should have the skills and information necessary to recognize fraud-related risks and bring them to the board of directors’ notice. Even as ARC lacks the jurisdiction to grant approval, its ensuring function can guarantee that an organization’s goals and plans are risk-free and that any instances of fraud are identified, disclosed, and minimized in order to help the business become better managed.

Fraud risk assessment

FRA plays a significant role in fraud risk management and is essential to achieving GCG. FRA addresses the risks that are directly related to fraud, including its consequences and likelihood of happening. FRA supports GCG by incorporating written policies into an organization’s governance structure, which serve as an expression of the board of directors’ expectations. The board has approved these policies, and SM is responsible for putting them into effect. The FRA creates a system that evaluates the SM function for policy implementation as well as pay, performance-based bonuses, and transactions with unapproved linked parties. Through continuing compliance and mitigating program, FRA establishes tones at the top. Additionally, FRA requires ARC to examine the policies and update them as needed in order to successfully carry out the work regarding fraud and related risk. Additionally, FRA supports ARC in resolving issues from internal and external audits and putting their approved recommendations into practice. FRA is a control that helps accomplish GCG by identifying significant and essential fraud risk (Law, 2011). The Financial Reporting Authority (FRA) records historical fraudulent activities that have taken place in related industries. Because FRA is scheme-and scenario-based as opposed to intrinsic and control-based, it offers superior control over the prevention of fraud and helps the company accomplish its objectives. In addition to evaluating the efficacy of ARC and SM, FRA provides comprehensive recommendations for SM and ARC for the policies that may be influenced by fraud and its associated activities. Moreover, FRA evaluates the code of conduct, its implementation, and its procedure continuously and continuously; it is not a one-time event. FRA depends on a number of variables and components. These factors are assessed based on how frequently they occur and how they affect the organization. Anderson (2011) notes that these scales are frequently referred to as heat maps. FRA is increasingly required to be included in all kinds of audits. The Institute of Internal Auditors and the American Institute of Certified Public Accountants have added new auditing standards to better serve the FRA. Reduced financial losses from fraud, lower response costs, increased employee awareness, improved compliance with local laws, increased potential for reporting fraud (whistle blowing), and improved corporate governance with the possibility of achieving GCG are all possible outcomes of effective fraud risk reduction (FRA).

How could the practice of forensic accounting be potentially improved to prevent instances of fraud from arising?

Because forensic accounting is still a relatively new and multidisciplinary field of study that integrates knowledge from criminology, information technology, psychology, sociology, and accounting with law and accounting, it is necessary to improve the practice of forensic accounting for several reasons. This argument is reinforced by the observation that, there is, in fact, disagreement over the definition of forensic accounting, which is detrimental to both the people who perform the practice and those who are touched by its conclusion. To give an example, Botes and Saadeh (2018) identified three main approaches: (1) the narrow approach, which was popular until the mid-1990s and focused on the litigious and adversarial role of the practice; (2) the broad approach, which is used by international professional accounting associations and involves the application of specialized knowledge and investigative skills to collect, analyze, and evaluate an issue as well as to interpret and communicate; and (3) the comprehensive definition that encompasses both the investigative and adversarial roles of forensic accounting. In order to better prevent fraud from occurring in the future, it would seem that forensic accounting would benefit from a precise definition that is applicable to all parties. This way, everyone who is involved in the practice or affected by it would understand what is involved. The fact that forensic accountants are typically able to provide a variety of services to prevent instances of fraud, litigation support is thought to be their primary role, further supports the idea that the practice of forensic accounting would benefit from a single, clear definition. This is due to the recognition that the use of forensic accounting in the judicial system is intended to improve the proceedings by pushing for much higher levels of accountability from the parties engaged in a particular case. However, it’s also important to recognize that the adversarial function of forensic accounting has expanded with the addition of business valuation services, which are provided with the aim of improving accountability. Therefore, one could argue that, as part of a common understanding, forensic accounting needs to be improved by continuing to emphasize the necessity for litigation support while also acknowledging the business side of this technique for reducing instances of fraud.

Additionally, it has been discovered that forensic accounting procedures are an excellent means of protecting a certain county’s economy against fraud by identifying potential perpetrators of harm to a specific organization. According to Honigsberg (2020), for example, there are many distinct forensic accounting techniques used to identify fraud. These techniques include financial statement analysis, spotting irregularities in financial records, and recognizing the personal and behavioral traits of criminals. Therefore, it is thought to be vitally essential to include modern forensic accounting techniques into the accounting context in order to identify instances of fraud and take appropriate action to prevent and punish it (Honigsberg, 2020). Consequently, in line with the earlier points raised in this literature review about the necessity of enhancing forensic accounting procedures in order to stop fraud, it is important to highlight the significance of the various approaches that Honigsberg (2000) has acknowledged in this respect. In addition to the fact that forensic accounting is still a relatively new and multidisciplinary field of study, it has also evolved into an even more recent practice in the context of cybercrime investigation and detection (Tutino and Merlo, 2019). These factors are all related to the need for the practice to be improved upon. Thus, there is still a lot of need for development in this area even if forensic accountants try to use various computer software and methods to uncover cases of fraud in public and private organizations. This is seen to be especially true considering how recently forensic accounting procedures have been used in this context, considering that forensic accounting is very young overall (Kılıç, 2020).

RESEARCH METHODOLOGY

The purpose of this study is to determine how Omani public listed company corporate governance is affected by fraud prevention measures. Fraud risk assessment and the preventative function of forensic accounting are regarded as fraud preventive measures. This study also suggested that the association between effective corporate governance and fraud risk assessment is mediated by the preventive role of forensic accounting. This chapter covers the methods growing body of research on the fraud cases develop fraud prevention strategies in Oman listed Companies. after collecting data, information about the topic we will analyses this results, data and results presentation and discussion. It is decided that forensic accounting is a contentious subject that will spur a lot of research in the upcoming years.

Data collection and resources:

With FAP acting as a mediator, a quantitative method using a descriptive cross-sectional survey design was used to determine and identify the link between FRA and GCG. Figure 1 defines the relationship between FRA, FAP, and GCG. The study’s unit of measurement is Oman’s publicly traded companies (Ali Rehman & Fathyah Hashim, 2020).

Figure 1 – Framework of the Study

Source: Compiled data

Organizations must adhere to the fundamentals of corporate governance, which includes running ARC meetings. However, what matters most is how well ARC meetings work; these should be documented and should outline the organization’s policies and procedures. In a similar vein, ARC plays a crucial part in strategic planning that results in the accomplishment of goals and objectives and offers improved corporate governance, or GCG. Similar to the board’s advisor, ARC works with the help of internal and external audit. These two autonomous departments carry out the duties, give ARC information to help it achieve its objectives, and formulate suggestions. In order to enable GCG to be achieved, ARC must discuss with senior management the breadth, depth, and consistency of audit findings and related recommendations in audit reports. These three factors—which have an impact on organizational performance and are closely related to organizational goals—are the major components of GCG accomplishment. According to the ACFE (2016), effective tone at the top, which is also defined as ethics and code of conduct policies, whistle blower policy and protection, assessment of executive management, and audit committee evaluation are important aspects of fraud risk governance that can improve the organizational corporate governance.

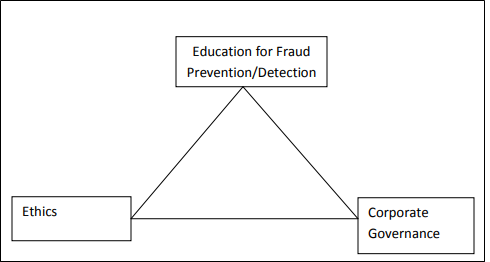

We provide the Fraud Deterrence Triangle (FAT), Figure 2, as a paradigm for fraud prevention and detection. (Hyatt, J. 2010).

Figure 2 – Fraud Deterrence Triangle

Source: Compiled data

The triangle in figure 2 shows that the following elements must be present in order to prevent or identify fraud: a) thorough and well-planned education and training on fraud prevention and detection; b) a set of ethical values; and c) robust corporate governance. This triangle shows that there are three main concerns that need to be addressed in order to prevent and identify fraud: corporate governance, ethics, and fraud prevention/detection education. First, there is the matter of educating and providing the appropriate tools (manual and technological) for auditors and accountants to detect fraudulent activity. Although the other two aspects of the fraud deterrence triangle are also important, we only address fraud prevention and detection in this study; the other two will be the subject of future investigations. We propose that the professions of accounting and auditing have a lengthy history in the world’s developed nations. These nations publish a lot of excellent accounting and auditing standards, but earlier research (Hyatt, 2010 is one example) indicates that auditors don’t play a big part in stopping or spotting fraud. As was covered in earlier parts, the primary cause of this little role is the dearth of educational and training opportunities in this crucial area of expertise. Consequently, we urge the following: 1) The Securities and Exchange Commission (SEC), the Public Company Accounting Oversight Board (PCAOB), the Institute of Certified Public Accountants, and other relevant entities to set aside funds to provide ongoing education on fraud prevention and detection for partners and key personnel in public accounting firms. Additionally, the ability to audit public firms should only be granted to individuals who can successfully complete and pass these courses. Since the Public Company Accounting Oversight Board has the authority to enforce this requirement on its registered auditors, the board ought to be interested in this requirement. The Institute of Certified Public Accountants has the authority to include questions and information from fraud courses in the CPA examinations and in the requirement for ongoing education. We stress the following: 1) training for dealing with fraud in electronic data processing and information technology is crucial; 2) training for ethics is more crucial than training for preventing or detecting fraud. The distinction between fraud and non-fraud (good and wrong) cannot be made by even the most sophisticated accounting and auditing rules and processes. The conscience of accountants and auditors alone often decides what is morally correct. Thus, providing ethics courses can enhance the moral principles of auditors and accountants and should come before fraud prevention and detection training. Therefore, we advise that: 1) public accounting firms not to forego their long-term benefits in favor of their short-term ones; and 2) regulators and policy makers, such as the SEC, PCAOB, and Institute of Certified Public Accountants, require auditors and accountants to undergo continuous education on ethical values and issues too. To teach their staff on ethical and fraud-related matters, they have to create their own training courses. Universities should be aware of the increased demand for programs and courses that focus on fraud prevention and detection following the passage of the Sarbanes-Oxley Act of 2002. Public accounting firms should also supervise and monitor employee performance and educate staff members about the significance of these issues. This area of specialty can attract a large number of students to universities and lessen their financial deficits, especially in light of the current economic downturn and budget cuts that many of them are experiencing.

Data and results analysis:

The foundation of sound corporate governance, fraud risk assessment (FRA) is a crucial tool for controlling and eradicating fraud in businesses. Policies and procedures are one way that FRA is offered as a control. Once FRA is appropriately designed and put into practice, frauds can be detected before they happen and mitigating measures can be created. Simultaneously, once the firm is free from fraud and fraudulent actions, GCG can function efficiently. A fraud-free environment also makes it possible for GCG to satisfy its investors. GCG is quantified in this study using its two primary components, ARC and SM. The goal of this study is to determine how fraud risk assessment and sound corporate governance relate to companies that are listed on the Sultanate of Oman’s Muscat Stock Market. Because of this, a quantitative survey was conducted for each of the 151 organizations included in MSM, and data from 93% of the respondents was examined and evaluated. Given that the p-value is 0.00 and the t-value is 3.351, the study’s findings suggest that FRA and GCG have a direct and significant link. In addition to contributing significantly to the literature review, this study offers companies useful applications. The practical application of this concept is not limited to Omani public listed firms; it may be extended to all organizations worldwide. GCG is a basic prerequisite for all organizations and can be used to private and government-owned businesses as well as businesses that are not publicly traded. In a similar vein, fraud affects all organizations regardless of how it is classified, so putting FRA into practice is crucial to its eradication, mitigation, and management. This study is limited in two ways. First off, only 115 public listed firms in Oman are the focus of this study; including private limited companies with paid-up share capital of at least USD 10 million would have improved the findings. Nevertheless, this study’s purview is restricted to publicly traded corporations. Due to research limitations, this study was only carried out at the company level, with one respondent speaking for the organization.

Source of data

Secondary data are used in this investigation. The secondary data includes material gleaned from books, articles, textbooks, unpublished works, websites, journals, newspapers, and other sources about specific companies within the area of interest that would support the research’s current assertions.

ANALYSIS AND FINDINGS

The idea of corporate governance is new in Oman, and much like any other nation, there are scams going on there. A small number of fraud cases have been recorded in the last five years, spanning across several businesses and sectors and with values ranging from USD 39 million to USD 2.6 million (Mukrashi, 2016; Reuter, 2011; Reuter, 2013; Reuter, 2014). Still, the most fall into the ethical wrongdoing category of fraud. According to the World Bank (2016), Oman’s governance score for the year 2016 in terms of controlling corruption remained nearly unchanged from the score attained in 2006. Additionally, the ACFE (2016) claimed that the number of fraud cases recorded in Oman is rising annually. Governance has a smaller role in controlling fraud and corruption as a result of the reasons for these fraudulent activities: a lack of ethical culture developed by SM and oversight by the board of directors. In Oman, updated corporate governance guidelines were put into effect in 2016, while the previous guidelines were approved in 2002. To meet the needs of GCG and satisfy shareholders, these new codes still need to be adjusted and modified in a few places. Scattered across the financial, industrial, and service sectors, there are 135 businesses registered on the Muscat Stock Market (MSM). Capital Market Regulations, Corporate Governance Codes, and Commercial Companies Law regulate publicly traded companies. (Ali Rehman & Fathyah Hashim, 2020).

Analysis and Interpretation

The CEO of Oman’s National Gas Company is fired for bribery.

The chief executive officer of Oman’s National Gas Company, Goutam Sen, has been let go, the company disclosed to the Muscat Securities Market (MSM) on Wednesday.

The company’s board of directors resolved in unison to promptly fire Sen. The business revealed in 2014 that it had arrested its CEO on suspicion of paying bribes to a government official.

“The Board of Directors wish to inform that the Company has received a reply from the public prosecution regarding the detention of the Company’s CEO,” National Gas Co said in a bours estatement. “The reply received states that the CEO has been accused of bribing a government official.”

In 2014, the corporation was ordered by the Public Prosecution to provide 500,000 riyals as bail for the CEO. Sen and other government officials were involved in a broad corruption scandal in Oman’s oil and gas industry.

The new CEO hasn’t been revealed by the corporation yet. Having seven strategically placed units, the company was founded in 1979 with the goal of marketing and bottling liquefied petroleum gas, which it purchases in large quantities from Omani refineries.

In compliance with Royal Decree No. 64/2013, Oman joined the United Nations Convention against Corruption in June 2015, and it has since continued to fight corruption. During the last five years, more than twenty senior officials—mostly from the oil and gas industry—have been detained and imprisoned. More severe punishments for offenders have helped to curtail the number of corruption cases in the nation.

The Oman Oil Company’s CEO, the undersecretary of the Ministry of Transport and Communication, and the previous minister of trade and industry were all found guilty of corruption in 2014 by the Muscat Primary Court. (Mukrashi, F. A. ,2016).

Prepaid card scam of $39 million hits Oman Bank Muscat.

DUBAI, February 26, Reuters the biggest bank in Oman, Bank Muscat, announced on Tuesday that it will incur impairment charges of up to 15 million rials, or $39 million, following the discovery of a small number of prepaid travel cards that had been compromised by fraud.

The bank reported that following the compromising of 12 prepaid travel cards outside of Oman, its board convened on Monday. Instead of using their pricey debit or credit cards when traveling, customers can carry cash with them thanks to these cards. The fraud hasn’t impacted any other customers.

“We are exploring all avenues to minimize the impact on our shareholders and will pursue the various options available to the bank,” Bank Muscat stated, tagging on that it would notify the market as additional details became available.

Bank Muscat shares saw a slight recovery on Tuesday, rising 2.1 percent at 06:25 GMT after plunging 4.3 percent on Monday—the biggest single-day decline in the stock since July 2011.

According to a report from United Securities, the impairment amounted to 10.5% of Bank Muscat’s projected 2013 earnings and was caused by an unidentified electronic crime.

The report also stated that the stock was “still under priced as compared to its domestic and regional peers,” trading at about 1.1 times book value, even after accounting for the impairment.

Last month, Bank Muscat reported an 18.5 percent increase in net profit for 2012, driven mostly by a 16.2 percent increase in loans.

According to the bank’s chief operating officer, who was mentioned by the local media earlier this month, lending growth is expected to be between 14 and 15 percent this year due to increased government spending and local residents’ greater incomes (Reuter, S.,2013).

Oman’s Renaissance uncovers fraud at Topaz unit, H1 profit falls.

DUBAI (Reuters) – As the diversified company reported a 77% decline in its net profit for the first half of the year, Renaissance Services of Oman stated it had discovered “serious” problems at its Topaz unit, including financial misbehavior and fraud.

In a statement released on the stock exchange on Monday, Renaissance’s Chairman Samir Fancy said that Topaz, which withdrew from its $500 million initial public offering (IPO) earlier in the year, had violated the company’s code of business conduct and failed to disclose material information to the board of directors. One of the largest oil services firms in the Middle East, the company found evidence of fraud and unethical behavior at one of Topaz’s overseas subsidiaries, primarily related to the company’s usage of $2.9 million in cash for operations, according to the statement.

Renaissance stated that it was acting swiftly to resolve the problems, which might have a $30 million one-time cost. In Topaz’s engineering division, the company will eliminate over 100 positions, with savings anticipated in 2012.

He further stated that on May 30, Topaz’s chief executive, Fazel Fazelbhoy, resigned and all managers of the unidentified foreign business were fired. In July, Fazelb hoy announced to Reuters that he was leaving his position as Topaz’s CEO.

The chief operating officer of Topaz Engineering and the director of the company’s finances have both accepted resignations, according to the statement.

The company’s first half had a net profit of 2.25 million rials ($5.84 million), down from a net profit of 9.8 million rials in the same period last year, which Fancy referred to as “one of the most troubled periods in our company’s history”.

In March, Renaissance withdrew its highly anticipated initial public offering of its Topaz company, citing worries about value and increasing unrest in the region. The Dubai-based unit’s market worth was estimated to be between $1.5 billion and $1.9 billion based on its $500 million London offering.

stated the chairman “Whatever external factors may affect sentiment, the problems we have encountered internally in Topaz need to be fully resolved before any further contemplation of a listing.”

He continued by saying that the business is currently negotiating a debt refinancing with lead banks. The value of Renaissance shares has decreased by 39% so far this year. (Reuters, S. ,2011).

CONCLUSION

The analysis conducted for this article makes it abundantly evident that there is need for improvement in the field of forensic accounting in order to stop fraud before it starts. The technique of forensic accounting is deemed to be very essential for recognizing unique organizations’ financial wrongdoing reporting due to its diverse nature, which is the cause for this possible improvement. This is due to the fact that forensic accountants are able to carry out their duties by, at the very least, attempting to combine their accounting expertise and legal understanding of pertinent laws. Additionally, it has been discovered that the application of forensic accounting techniques has proven helpful in protecting a nation’s economy against fraud by identifying potential perpetrators of harm to a certain organization. Furthermore, it has been stated that forensic accountants still have a big part to play in both the detection and the prevention of cyber crimes, even though their application in the context of cyber crime is still developing.Because forensic accounting would benefit from a precise definition that is generally applicable, it is possible for its practices to be improved. This is because everyone who is involved in or affected by forensic accounting would then understand what is involved in successfully preventing fraud cases from occurring in the future. Additionally, there is a degree of difference in the roles that have developed in industrialized nations where nursing is a profession and in developing nations where it has not yet become one. Furthermore, it has been discovered that the ability of forensic accounting techniques to guide policy in this area is a major factor that will determine how widely they are used in the future to stop fraud. This is corroborated by the growing perception that forensic accounting techniques have not had a significant impact on informing the creation of fraud prevention policies. The fact that the presence of fraud symptoms does not always indicate that fraud has really occurred adds another difference in the attitude of regulators and forensic accountants.

RECOMMENDATIONS

Despite the existence of safeguards, regulatory directions, and governance principles, organizational fraud continues to occur. Rather of being used to determine corporate governance maturity and control weaknesses, these rules, guidelines, and controls are merely used as a compliance checkbox. An activity that may be offered within an organization is the forensic accounting detective function. Mature corporate governance can influence and reform this role, which in turn can help businesses reduce fraud and its related activities. The board of directors, the audit and risk committee, and senior management, or executive management, are the three main components of established corporate governance. The fulfillment of corporate goals and the happiness of shareholders depend on all three of these important components. This study explained to determine the relationship between sophisticated corporate governance and the investigative role of forensic accounting in publicly traded companies located in the Sultanate of Oman by applying agency theory. The findings imply that the investigative function of forensic accounting is directly impacted by established corporate governance. It is strongly advised that companies establish an internal forensic accounting detective position in order to reduce or eradicate fraud. This role can be reinforced by having mature corporate governance.

Research Gap

The nature and significance of audit report messages, the role and responsibilities of auditors, the quality of the audit function, and the structure and regulations governing the profession are the four main recurrent concerns that are at the center of the audit expectation gap argument. The public expects auditors to identify financial asset falsification or even fraudulent activity from the financial statements, therefore the primary issue is the ongoing misunderstanding of the function and responsibilities of the auditor. This has long been the accepted understanding of the duties of an auditor. As a result, this perception needs to be updated and renewed. Auditors having experience in forensic accounting would be designated as forensic accountants with the express purpose of looking into the financial statements of the organization. It is their responsibility to identify financial misstatements. This public view of auditors could be changed or perhaps erased with the correct education.

REFERENCES

- S. Hopwood, J.J. Leiner, and G.R. Young, Forensic Accounting. (New York: McGraw-Hill Irwin, 2008), 3, 5.

- Albrecht, W.S. (2005). Identifying Fraudulent Financial Transactions: A Framework for Detecting Financial Statement Fraud. Brigham Young University.

- David, A. (2005). Low Level Fraud is a High-Level Issue, Supply Management. [Online] Available: http://www.highbeam.com/doc/1P3-821992191.html. (Retrieved from 26th November 2008).

- Mukrashi, F. A. (2016), “Oman’s National Gas Company fires CEO over bribery “Available at http://gulfnews.com/news/gulf/oman/oman-s-national-gas-company-fires-ceo-overbribery-1.1674858 (19 August 20181)

- Reuter, S. (2013), “Oman’s Bank Muscat hit by $39 mln prepaid card fraud”. Available at https://www.reuters.com/article/us-renaissance-results/omans-renaissance-uncovers-fraud-at-topaz-unit-h1-profit-falls-idUSTRE77E0NW20110815 (25 December 2018)

- Reuters, S. (2011), “Oman’s Renaissance uncovers fraud at Topaz unit, H1 profit falls”. Available at https://www.reuters.com/article/us-renaissance-results/omans-renaissanceuncovers-fraud-at-topaz-unit-h1-profit-falls-idUSTRE77E0NW20110815 (25 December 2018)

- Reuters, S. (2014), “Oman court jails businessman to 15 years over bribes”. Available at Oman court jails businessman to 15 years over bribes | Reuters (25 December 2018).

- Hyatt, J. 2010. Who detects corporate fraud? (Tip: It’s not usually SEC …) Business Ethics: The Magazine of Corporate Responsibility. Available at: http://business-ethics.com/2010/02/16/1035-who-detects-corporate-fraud-tip-its-not-usually-the-sec/

- Adrian Nicholas Koh, Lawrence Arokiasamy & Cristal Lee Ah Suat (2009), Forensic Accounting: Public Acceptance towards Occurrence of Fraud Detection Available at: https://www.ccsenet.org/journal/index.php/ijbm/article/view/4229.

- Abdulrahman Atllah Alharbi, (2022), A critical evaluation of forensic accounting studies with a view to discerning how practice can be improved to prevent cases of fraud, Available at: https://journals.ajsrp.com/index.php/jeals/article/view/5432/5175, Journal of Economic, Administrative and Legal Sciences, Volume (6), Issue (18):30Jul2022P: 155-162

- Kristen Dreyer (2014), A History of Forensic Accounting, Available at: Grand Valley State University Scholar Works@GVSU, Available at: https://scholarworks.gvsu.edu/cgi/viewcontent.cgi?article=1339&context=honorsprojects.

- Ali Rehman & Fathyah Hashim (2020), Impact of Fraud Preventive Measures on Good Corporate Governance, Available at: https://doi.org/10.5296/jcgr.v4i1.17490, Journal of Corporate Governance Research ISSN 1948-4658, 2020, Vol. 4, No. 1, Published: October 8, 2020.

- Emmanuel Ikechukwu Okoye (2009), The Role of Forensic Accounting in Fraud Investigation and Litigation Support, Available at: php (ssrn.com), The Nigerian Academic Forum, Vol. 17, No. 1, November 2009, 9 Pages Posted: 24 Mar 2011