Impact of Remittance on Financial Sector Growth in Nigeria: An Econometrics Approach

- Adewumi Olusola Anthony

- Joseph Obansa

- Oluwatosin Olushola

- Modestus Chidi Nsonwu

- 1029-1042

- May 7, 2024

- Accounting & Finance

Impact of Remittance on Financial Sector Growth in Nigeria: An Econometrics Approach

Adewumi Olusola Anthony1, Joseph Obansa2, Oluwatosin Olushola1, Modestus Chidi Nsonwu1

1Department of Economics, Veritas University Abuja.

2Department of Economics, University of Abuja.

DOI: https://dx.doi.org/10.47772/IJRISS.2024.804077

Received: 14 March 2024; Revised: 02 April 2024; Accepted: 06 April 2024; Published: 07 May 2024

ABSTRACT

Remittance inflow is one of the major sources of foreign exchange not only to individuals and financial institutions but also to the economy as a whole. The level of remittance to Nigeria has been on the increase, yet the exchange rate has been very unstable with the naira falling against the USD dollars consistently. Despite different literature on the impact of remittance on the Nigerian economy as a whole, limited studies have been carried out on the effects of remittance on the financial sector of the economy. This study investigated the impact of remittance on the financial sector in Nigeria using data between 1986 and 2022. The choice of the period is to capture the effect on the Structural Adjustment Program (SAP) on the economy while also considering other macroeconomic factors and shocks in period thereafter. An Autoregressive Distributed Lag (ARDL) was employed. Evidence from the results revealed a long-run relationship between financial sector output, Remittances (REM), Cost of remittance (CRM), Trade Openness (TRO) and Exchange Rate (EXR). Meanwhile the cost of remittance was found insignificant. The empirical findings from the ARDL result show that there is a positive relationship between financial sector output, remittance inflow, cost of remittance, trade openness and exchange rate in Nigeria. Based on the empirical findings, the study recommended that government should employ policies that will encourage judicious utilization of funds received through remittances by channelling the funds into productive investment as it will encourage more inflow of remittances and make policy measures more stable to attract more remittances.

Key Words: Remittance, Financial sector growth, Nigeria.

INTRODUCTION

The increasing significance of foreign remittance inflows to developing countries, particularly Nigeria, has been highlighted as a crucial source of income for both households and the government. At the household level, it positively influences income, consumption expenditures, and spending on health, education, savings, nutrition, and asset accumulation. For the government, remittances contribute to increased taxes and fees, while also reducing the unemployment rate (Gammeltoft, 2002; Ratha 2003). In Nigeria, remittance flows as a percentage of GDP have consistently exceeded oil revenues from 2015 to 2020. For instance, in 2018, migrants’ remittances in Nigeria reached $25 billion, representing 6.1% of GDP, with a projected growth rate of $34.8 billion by 2023 (Samuel et al., 2023). Despite extensive literature on the economic impacts of remittance on developing countries, particularly Nigeria, there is a notable gap in understanding its effects on the financial sector, particularly in recent years.

The banking sector plays a vital role in the growth and development of the Nigerian economy, providing key financial services such as collecting deposits and facilitating economic growth (Olushola, Beyai, & Anagbado,2023). Remittance, being a significant contributor to liquidity in the financial sector, prompted the Central Bank of Nigeria (CBN) to introduce guidelines for licensing International Money Transfer Operators (IMTOs). Despite a temporary decline in remittance volume in 2020 due to the COVID-19 pandemic, CBN’s continued efforts to manage foreign inflows, including the introduction of the Naira for dollar scheme in 2021, have positively impacted remittance growth above Foreign Direct Investment (FDI) figures. According to PwC (2020), Nigeria had the largest share of foreign remittances to Africa in 2017 and for four consecutive years, the inflows exceeded that of oil revenues. For example, in 2018, remittance figure translated to 83% of the federal government budget and was seven (7) times the size of the net official development assistance (foreign aid) in the preceding year.

A well-designed policy on migration, according to Samuel et al. (2023), can significantly improve remittance inflow into the country. While remittance’s contributions to the Nigerian economy are evident, its effects on the banking industry remain unclear (Utile & Olushola, 2023). This research aims to address this gap, especially considering the country’s foreign exchange shortages caused by balance of payments issues. Understanding remittance activities in Nigeria is crucial for exposing recipients to the financial system, deepening financial intermediation, and increasing total loanable funds in the financial sector. Despite the positive impact of remittance on the Nigerian economy, the financial sector has remained underdeveloped. The World Development Indicators (WDI) indicate a decline in broad money supply as a percentage of GDP, despite the increasing size of remittances. Exchange rate problems, resulting from over-dependence on oil, have negatively affected different sectors, including the financial industry. This research aims to investigate how remittance has impacted the financial sector in Nigeria, considering its leveraging effect on the economy and potential positive relationship with the size and efficiency of banks. The objective is to provide valuable insights that can guide stakeholders and policymakers in enhancing financial sector growth in Nigeria.

LITERATURE REVIEW

The Portfolio Theory

According to Markowitz (1952), remittances are viewed as a strategy employed by emigrant workers to diversify their savings. This decision to remit is influenced by the risk-return dynamics of assets in both the host and recipient countries. Key determinants of the decision to remit include interest rate differentials on deposit accounts, real estate returns, and inflation rates. Beyond economic factors, the desire to invest may also be motivated by the emigrant worker’s aspiration to return home with dignity, leading to a generally positive relationship between remittances and GDP, in contrast to altruistic motivations. The Portfolio Theory, also known as Modern Portfolio Theory (MPT), introduced by economist Harry Markowitz in 1952, is a foundational concept in finance. This theory provides a framework for making investment decisions by optimizing the trade-off between risk and return. Emphasizing diversification, the theory advocates building a diversified portfolio of assets to achieve maximum return for a given level of risk or to minimize risk for a desired level of return.

Diversification, a core principle of the Portfolio Theory, involves investing in various assets such as stocks, bonds, and real estate to spread risk across the portfolio. The efficient frontier, a crucial concept, represents portfolios offering the highest expected return for a given level of risk or the lowest risk for a desired return. Portfolios lying on the efficient frontier are considered optimal due to their superior risk-return trade-off. The theory introduces risk assessment, typically measured by variance or standard deviation, and emphasizes finding an optimal balance that maximizes returns while managing risk effectively. Utility theory, often applied in Portfolio Theory, captures an investor’s risk preferences and aids in determining the optimal asset allocation based on risk tolerance and desired returns. The impact of Portfolio Theory on finance and investment management is significant, leading to the development of various investment strategies and tools. Concepts like diversification, risk-return trade-offs, and efficient portfolio construction empower investors to work towards their financial goals while effectively managing risk.

The Accelerator theory

The theoretical framework employed in this study is the Accelerator theory, which elucidates the need for a certain level of capital to support specific economic activities. The theory is expressed as

K = Ky

Where k> 1, signifying that investment (I) corresponds to a change in capital stock, given by I = KΔY. In this equation, I represents investment in a specific time period, and ΔY denotes the gross domestic product for that period. Consequently, the equation becomes:

I = kY.

The role of remittances within this model is evident in the broader income determinants equation Y = C + I + G + (X-M), where C, I, G, and X – M represent private consumption, private investment, government expenditure, and earnings from net exports respectively.

The Accelerator theory’s relevance to this study lies in its capacity to convert any form of income into investment and capital, essential components for advancing financial sector development. Remittances, as a source of income, fit seamlessly into this framework, highlighting their potential role in fostering the financial sector’s growth. The theory emphasizes the pivotal concept that all income, including remittances, can effectively fuel investments. Remittances, being funds sent by individuals working abroad to their home country, are considered a form of income for the recipients. When strategically utilized as investments, remittances can significantly contribute to the expansion and development of the financial sector.

By applying the principles of the Accelerator theory, remittances emerge as a valuable resource capable of generating additional income and wealth. These additional funds can then be channelled to strengthen the financial sector’s development. This finding is significant as it underscores the transformative potential of remittances in supporting the growth and stability of the financial industry. Viewing remittances not merely as a source of immediate consumption but as a means to build capital opens new avenues for sustainable revenue generation. The theory emphasizes that remittances can be transformed into investments within the financial sector, enabling active participation in its growth. This infusion of investment has the potential to enhance financial products, services, and economic opportunities.

Empirical Review

Several empirical studies have delved into the impact of remittances on the financial sector’s development, employing diverse methodologies and tools to yield varied findings. One such study conducted by Nwachukwu, Ugwuanyi, & Ezeanyagu (2023) focused on investigating the effect of diaspora remittances on the growth of the services sector in Nigeria. The study’s dependent variable was services sector output, while independent variables included migrant remittances, workers’ remittances, and exchange rates. The data spanned from 1990 to 2022 and were sourced from the CBN Statistical Bulletin 2022 edition and the World Bank Development Indicator Database 2022 edition. To analyse the data, the Error Correction Model (ECM) technique was employed. The variables were found to be stationary at first difference and cointegrated, leading to the adoption of the ECM technique for estimating model parameters. The study’s results revealed that both migrant and workers’ remittances significantly increased the growth of the services sector in Nigeria during the reviewed period, while the exchange rate had a decreasing effect on the sector’s growth. The model estimated a speed of adjustment of 8.7% and a model fitness of 95.8%. The study concluded that remittances have positively impacted the output of the services sector in Nigeria. However, it was observed that the quantum of workers’ remittances inflow to the services sector was higher than that of migrant remittances. As a recommendation, the study proposed the intensification of technical exchange programs between Nigeria and other advanced countries, aiming to further enhance investments in the services sector. This current study employed different variables and methodologies to further explore this area of research.

Mustapha-Jaji and Adesina-Uthman (2023) conducted a study to assess the impact of remittances on financial development in Nigeria, focusing on banking sector development and stock market development over the period 1981 to 2021. Using auto-regressive distributed lag estimation techniques, they found that international remittances had a positive and significant impact on banking sector development, while their impact on stock market development was insignificant. Consequently, the study concluded that international remittances had varying effects on different measures of financial sector development. While their study centered on banking and stock market development, the current research aims to explore the impact of remittances on financial sector output.

In a study by Hussaini, Musa, and Muhammad (2021) spanning from 1986 to 2020, the researchers investigated the impact of migrants’ remittances on the development of the financial sector in Nigeria. Utilizing the autoregressive distributed lag (ARDL) technique, they found that migrants’ remittances contributed to the growth of the Nigerian financial sector. Additionally, the study observed that gross savings and interest rate spread had a negative impact on financial sector development in Nigeria. The study recommended sound economic policies to attract and stimulate remittances to Nigeria. The current study will incorporate different variables to further contribute to this research area.

Mustafa, Shah, and Iqbal (2020) explored the relationship between migrants’ remittances and financial development in Pakistan from 1976 to 2015. Employing the Auto-Regressive Distributed Lag technique, they discovered that the impact of migrants’ remittances on financial development depended on the proxy used for financial development. While migrants’ remittances significantly enhanced financial development when measured by the ratio of broad money supply to gross domestic product, their impact was insignificant when measured by the ratio of credit to the private sector to gross domestic product. The study recommended, among other things, a reduction in the high cost of remittances to keep a significant percentage within the financial system through innovative banking products. Although this study was conducted outside Nigeria, the current research will specifically focus on Nigerian financial sector output, contributing to the understanding of remittances’ impact on the local context.

Omobolanle et al. (2019) utilized the error correction estimation technique to examine the impact of migrants’ remittances on financial development in Nigeria. The study found that migrants’ remittances significantly contributed to the financial sector’s development in Nigeria. Additionally, the error correction term of the estimate was negatively signed and statistically significant. The study recommended, among other things, a reduction in the high cost of remittance. However, it was inconclusive as some variables used did not show any relationship with remittance inflow. The current study will employ a different set of variables, contributing to the ongoing research in this area.

Adigun and Ologunwa (2017) examined migrants’ remittances and their impacts on economic growth between 1980 and 2015. Utilizing multiple regression analysis, the study found a positive and significant relationship between remittances and economic growth. Investment and exchange rates also showed positive relationships, while interest rates were negatively related and not significant as a determinant of economic growth in Nigeria. The study recommended that recipients of remittances should prioritize investment over consumption to positively impact the economy. The current study will incorporate different variables.

Muktadir-Al-Mukit and Islam (2016) investigated the impact of migrants’ remittances on the disbursement of the banking sector in Bangladesh. Employing the vector error correction model (VECM) and vector autoregressive (VAR) techniques, the study found that migrants’ remittances significantly enhanced the disbursement of banking sector credit in Bangladesh. Causality results showed two-way causation between credit disbursement and migrants’ remittances. The study recommended that the government should focus on skill development, as more skills development leads to increased remittances inflow. The current study will specifically focus on Nigeria.

After conducting a comprehensive review of prior research on remittances and the financial sector in Nigeria, it has been observed that most studies predominantly focus on various aspects of social sciences, such as Sociology, Political Science, and Geography. Few scholars have adopted econometrics to explore migration effects, including remittances, the cost of remittance, and exchange rate levels, specifically on financial sector growth in Nigeria. Recognizing this gap, the current research aims to address these areas of focus and contribute valuable insights to the existing body of knowledge.

METHODOLOGY

The research design employed in this study is ex-post facto research to investigate the impact of remittances on the financial sector in Nigeria, offering a structured approach to analyse historical data and infer causal relationships. This research will use secondary data obtained from Central Bank of Nigeria (CBN) and World Bank Development Index (WDI) and the data spanned from 1986 to 2022. Remittance inflow, trade openness and exchange rate during the period under investigation are measured in percentages annually while financial sector output is measured in billion naira during the investigation period. The analyses involved descriptive statistics, trend analysis and unit root. In addition, Autoregressive Distributed Lagged (ARDL) – Bounds test procedure is used to examine the co-integration relationship between remittance and financial sector variables in Nigeria. This procedure was developed by Pesaran and Shin (1999) which was later expanded by Pesaran, Shin, and Smith (2001) and the procedure allows the researcher to use variables that are not integrated in the same order. Also, the error correction model (ECM) will be used to establish the short-run and long-run causal relations between remittance inflow and financial sector in Nigeria.

Model Specification

The foundation of the model will be based on the theoretical framework of the study. Also, the initial model will be adapted from the work of Mustapha-Jaji and Adesina-Uthman (2023) who examined the impact of remittances on financial development in Nigeria and their model is stated as follows:

FD= a0 + b1REM + b2PCGDP + b3INF+ b4EXT+ b5HCE + ut ………….1

where FD is financial development, “REM” is remittance inflow, “PCGDP” is per capita gross domestic product, “EXT” represents exchange rate, “HCE” is household consumption expenditure, α0 is the intercept or autonomous parameter estimate, β1 to β5 = Parameter estimate representing the coefficients of the variables and Ut = Error term (or stochastic term). However, the author will consider an accelerating which is specified as follows:

Y = C+ I+ G+ (X-M), ……………2

where C, I, G and X-M represents private consumption, private investment, government expenditure and earnings from net export respectively.

The author will augment the accelerating theory and re-written to give the model as thus: FSO= F (REM, CRM, EXR, TRO) …………. 3

Explicitly, equations 3 can be written as:

FSOt= β0+ β1REMt+ β2CRMt + β3TROt + β4EXRt + µt ……………….. 4

Where:

Financial Sector Output= Financial Sector Output

REM= Remittance Inflow

CRM= Cost of Remittance Inflow

TRO= Trade Openness EXR = Exchange Rate β0= Intercept term.

And β1-β4 are parameters known as partial regression coefficient.

The a priori expectation of the variables are as given in the table below:

Table 3.1: Description of the Variables that will be used for the Model

| Variable | Description/Measure | Type | Source | A-priori Expectation |

| FSO | Financial Sector Output is measured in billion naira | Dependent | WDI, 2021 | |

| RMT | Remittance Inflow is measured in percentage | Independent | WDI, 2022 | Β1 ,>< 0 |

| CRM | Cost of Remittance Inflow is measured in percentage | Independent | WDI,2022 | Β2,>< 0 |

| TRO | Trade Openness is measured as a ratio | Independent | WDI, 2021 | Β3,>< 0 |

| EXR | Exchange Rate is measured in percentage | Independent | WDI, 2022 | Β4 ,>< 0 |

Source: Author Compilation, 2023

EMPIRICAL RESULTS AND DISCUSSION

Table 4.1. Descriptive Statistics of remittance inflow, cost of remittance, trade openness and exchange rate and financial sector output in Nigeria

| Statistics | FSO | REM | CRM | TRO | EXR |

| Mean | 1223.733 | 2.997214 | 110.6572 | 34.35777 | 123.0889 |

| Median | 1283.872 | 2.524661 | 99.78083 | 34.32022 | 123.4016 |

| Maximum | 2318.547 | 8.333830 | 273.0094 | 53.27796 | 399.9636 |

| Minimum | 240.1863 | 0.004883 | 49.77631 | 9.135846 | 2.020575 |

| Std. Dev. | 524.3375 | 2.456944 | 53.93276 | 10.69048 | 109.2174 |

| Skewness | -0.074661 | 0.308090 | 1.822411 | -0.322777 | 0.854800 |

| Kurtosis | 2.291308 | 1.846158 | 5.671585 | 2.580779 | 3.004770 |

| Jarque-Bera | 0.786812 | 2.566541 | 30.63314 | 0.888730 | 4.384132 |

| Probability | 0.674755 | 0.277129 | 0.000000 | 0.641231 | 0.111686 |

Source: Author’s Computation, E-views Version 10.0.

From Table 4.1., the mean FSO is 1223.733, with a range of values between 240.1863 (minimum) and 2318.547 (maximum). The data has a relatively high standard deviation of 524.3375, indicating a considerable amount of variation. The skewness value of -0.074661 suggests a slightly left-skewed distribution, while the kurtosis of 2.291308 indicates a moderately peaked distribution. The Jarque-Bera statistic of 0.786812 and its associated probability of 0.674755 suggest that the data may be normally distributed.

The mean REM is 2.997214, with values ranging from 0.004883 (minimum) to 8.333830 (maximum). The standard deviation of 2.456944 indicates a relatively moderate amount of variation. The skewness value of 0.308090 suggests a slightly right-skewed distribution, while the kurtosis of 1.846158 indicates a moderately peaked distribution. The Jarque-Bera statistic of 2.566541 and its associated probability of 0.277129 suggest that the data may deviate slightly from a normal distribution.

The mean CRM is 110.6572, with values ranging from 49.77631 (minimum) to 273.0094 (maximum). The standard deviation of 53.93276 indicates a moderate amount of variation. The skewness value of 1.822411 suggests a significantly right-skewed distribution, while the kurtosis of 5.671585 indicates a heavily peaked distribution. The Jarque-Bera statistic of 30.63314 and its associated probability of 0.000000 suggest that the data significantly deviates from a normal distribution.

The mean TRO is 34.35777, with values ranging from 9.135846 (minimum) to 53.27796 (maximum). The standard deviation of 10.69048 indicates a moderate amount of variation. The skewness value of -0.322777 suggests a slightly left-skewed distribution, while the kurtosis of 2.580779 indicates a moderately peaked distribution. The Jarque-Bera statistic of 0.888730 and its associated probability of 0.641231 suggest that the data may be normally distributed.

The mean EXR is 123.0889, with values ranging from 2.020575 (minimum) to 399.9636 (maximum). The standard deviation of 109.2174 indicates a relatively high amount of variation. The skewness value of 0.854800 suggests a slightly right-skewed distribution, while the kurtosis of 3.004770 indicates a moderately peaked distribution. The Jarque-Bera statistic of 4.384132 and its associated probability of 0.111686 suggest that the data may deviate slightly from a normal distribution.

Unit Root Test

The unit root test was carried out based on the augmented dickey fuller (ADF) test at a 5% level of significance.

Table 4.2 Result of Augmented Dickey-Fuller Unit Root Test

| Variables | ADF Statistics | 5% Critical Value | Order of Integration |

| FSO | -4.910082 | -1.950687 | I(1) |

| REM | -6.216656 | -1.950687 | I(1) |

| CRM | -7.334395 | -1.950687 | I(1) |

| TRO | -3.640761 | -3.544284 | I(0) |

| EXR | -3.565048 | -1.950687 | I(1) |

Source: Author’s Computation Using E-views-10

Based on the above result of the Augmented Dickey-Fuller unit root test, the variables are a mixture of 1(1) and I(0) and are significant at a 5% level. This means that the null hypothesis will not be accepted. We, therefore, conclude that the time series collected in the models are all stationary at 5per per cent level and proceeded to check for co-integration among the variables.

ARDL Bound Cointegration Test

Table 4.5. ARDL Bound cointegration Test Results

| Test Statistic | Value | K | |

| 4.69584 | 4 | ||

| F-statistic | 7 | ||

| Critical Value Bounds | |||

| Significance | I0 Bound | I1 Bound | |

| 10% | 2.45 | 3.52 | |

| 5% | 2.86 | 4.01 | |

| 2.5% | 3.25 | 4.49 | |

| 1% | 3.74 | 5.06 | |

Source: Author’s Computation using E-views-10 (2023)

From these results, it is clear that there is a long-run relationship among the variables when FSO is the dependent variable because and F-statistic (4.696) are higher than the upper-bound critical values (4.01) at the 5% level. This implies that the null hypothesis of no cointegration among the variables in the equation is rejected.

ARDL Results

Table 6. Error Correction and Long Run Equation Coefficients

| Cointegrating Form | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| D(REM) | 6.093459 | 12.73025 | 0.478660 | 0.0367 |

| D(CRM) | 0.222910 | 0.416811 | 0.534799 | 0.1479 |

| D(TRO) | -5.040389 | 3.073215 | -1.640103 | 0.0146 |

| D(EXR) | 0.272572 | 1.246054 | 0.218748 | 0.8288 |

| D (EXR (-1)) | 3.617036 | 1.756431 | 2.059310 | 0.0410 |

| D (EXR (-2)) | -3.692336 | 1.254240 | -2.943882 | 0.0073 |

| CointEq (-1) | -0.547252 | 0.133622 | -4.095507 | 0.0004 |

| Cointeq = FSO – (11.1347*REM 4.6350*EXR + 755.2676) | 0.4073*CR | M + 0.5241 | *TRO + | |

| Long Run Coefficients | ||||

| Variable | Coefficient | Std. Error | t-Statistic | Prob. |

| REM | 11.134657 | 22.071642 | 0.504478 | 0.0187 |

| CRM | 0.407327 | 0.743408 | 0.547919 | 0.1490 |

| TRO | 0.524125 | 5.527001 | 0.094830 | 0.9253 |

| EXR | 4.635025 | 0.685501 | 6.761515 | 0.0000 |

| C | 755.267629 | 253.402386 | 2.980507 | 0.0067 |

Source: Author’s Computation using E-views-10 (2023)

REM: The coefficient of REM is 11.134657, indicating that a one-unit increase in REM is associated with an increase of approximately 11.13 units in the financial sector output in the long run. However, the coefficient is statistically significant, as the corresponding probability value of 0.0187 is less than the typical significance level of 0.05. Therefore, it is possible to conclude that REM has a significant long-run impact on the financial sector output.

CRM: The coefficient of CRM is 0.407327. This suggests that a one-unit increase in CRM is associated with a small increase of approximately 0.41 units in the financial sector output in the long run. The coefficient is not statistically significant with a probability value of 0.1490, which is greater than 0.05. This indicates that CRM is statistically insignificant in the long run and short run.

TRO: The coefficient of TRO is 0.524125. This implies that a one-unit increase in TRO is associated with a small increase of approximately 0.52 units in the financial sector output in the long run. However, the coefficient is not statistically significant, as the corresponding probability value of 0.9253 is much greater than 0.05. Therefore, it is not possible to conclude that TRO has a significant long-run impact on the financial sector output but is statistically significant in the short-run but statistically significant in the short-run.

EXR: The coefficient of EXR is 4.635025, suggesting that a one-unit increase in EXR is associated with a substantial increase of approximately 4.64 units in the financial sector output in the long run. The coefficient is highly statistically significant, as the probability value is 0.0000 (less than 0.05). This indicates that EXR has a highly significant long-run impact on the financial sector output and is statistically significant in the short-run.

However, as expected, the coefficient of the co-integrating equation (ECM1t-1) is negative and statistically significant at 5%. This revealed that once there is disequilibrium in the model or system, it took an average (annual) speed of 55% to adjust towards equilibrium in the long run between remittance inflow, cost of remittance, trade openness, exchange rate and financial sector in Nigeria. This also means that the errors will continue to be corrected at 55% annually.

Post Estimation Test Result

Serial Correlation

This is the test for serial correlation in the model. The Breusch -Geofrey Serial correlation LM test is used to test the existence of serial correlation in the model.

Table 5. Breusch-Godfrey Serial Correlation LM Test:

| F-statistic | 0.276700 | Prob. F (2,21) | 0.7610 |

| Obs*R-squared | 0.847301 | Prob. Chi-Square (2) | 0.6547 |

Source: Author’s Computation using E-views-10 (2023)

From the table, considering the prob. Chi-Square value which is greater than 0.05 level., The decision rule is to accept the Null hypothesis (Ho) if the prob. value is greater than 0.05; hence accepting the null hypothesis means there is no serial correlation in the model.

Heteroscedasticity Test

Table 6. Heteroskedasticity Test: ARCH

| F-statistic | 0.000301 | Prob. F (1,30) | 0.9863 |

| Obs*R-squared | 0.000321 | Prob. ChiSquare (1) | 0.9857 |

Source: Author’s Computation using E-views-10 (2023)

The ARCH LM test result on the model showed the rejection of the null hypothesis of no ARCH effect with a probability Chi-Square value greater than 0.05. That is, there is an absence of heteroscedasticity in the models and the presence of homoscedasticity in the models.

Stability Test

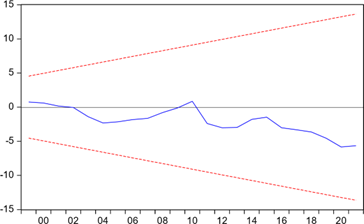

Recursive least square tests (CUSUM TESTS) have been also applied to check parameter stability for the variables. Figure 2. shows recursive coefficients estimates where estimated values of parameters for regressand variable i: e financial sector output and explanatory variables i: e remittance inflow, cost of remittance, trade openness and exchange rate are plotted against each iteration. The graphs show the stability analysis during the year 1986 to 2022. During the intervals, the data looks stable because it falls at 0.05%.

CUSUM 5% Significance

Figure 2. Stability Test Source: Author’s Computation using E-views-10 (2022)

4.3.3 Ramsey Rest Test

Table 7. Ramsey RESET Test

Equation: UNTITLED

Specification: FSO FSO (-1) REM CRM TRO TRO (-1) EXR

EXR (-1)

EXR (-2) EXR (-3) C

Omitted Variables: Squares of fitted values

| Value | df | Probability | |

| t-statistic | 1.072065 | 22 | 0.2953 |

| F-statistic | 1.149323 | (1, 22) | 0.2953 |

| Likelihood ratio | 1.680462 | 1 | 0.1949 |

Source: Author’s Computation using E-views-10 (2023)

From the table, the p-value of our F-statistics in all the models is greater than a 5% significance level, we fail to reject the Ramsey Reset test null hypotheses of correct specification. This indicates that the functional forms are correct, and our models do not suffer from omitted variables.

DISCUSSION OF RESULTS

The bound test analysis results indicate the presence of a long-run equilibrium relationship among the variables in the model. Examining the coefficients, we find that remittance inflow (REM) exhibits a significant long-run impact on financial sector output. The coefficient of REM is 11.134657, signifying that a one-unit increase in REM corresponds to a moderate increase of approximately 11.13 units in the financial sector output in the long run. This result aligns with the findings of Mustapha-Jaji and Adesina-Uthman (2023), supporting the significant long-run influence of remittances on financial development in Nigeria. In contrast, corporate remittance (CRM) has a coefficient of 0.407327, indicating a small long-run increase of approximately 0.41 units in financial sector output with a one-unit increase in CRM. However, this coefficient is not statistically significant, with a probability value of 0.1490 exceeding the typical significance level of 0.05. Therefore, it is not possible to assert a significant long-run impact of CRM on financial sector output, though it may have some short-run significance. Similarly, tourism revenue (TRO) exhibits a non-significant long-run impact, with a coefficient of 0.524125 and a probability value of 0.9253, suggesting a small long-run increase of approximately 0.52 units in financial sector output with a one-unit increase in TRO. While inconclusive for long-run impact, TRO may possess some short-run significance.

On the other hand, exchange rates (EXR) play a highly significant role in the long run, as indicated by a coefficient of 4.635025. A one-unit increase in EXR is associated with a substantial long-run increase of approximately 4.64 units in financial sector output. The statistical significance is confirmed by a probability value of 0.0000, reinforcing the substantial long-run impact of EXR on the financial sector output. This significance persists in the short run as well. Additionally, the negative and statistically significant coefficient of the co-integrating equation (ECMt-1) reveals that the model takes an average annual speed of 55% to adjust towards equilibrium in the long run. This implies that when there is disequilibrium in the model or system, correction will occur at a rate of 55% annually. The absence of serial correlation and heteroscedasticity, coupled with the correct functional forms and absence of omitted variables, further attests to the reliability of the analysis.

The data analysis has provided valuable insights into the influence of various factors on Nigeria’s financial sector. Notably, the data reveals a sustained, long-term relationship among these factors, indicating their interconnectedness over an extended period. This is a crucial finding as it signifies that alterations in any of these factors can have enduring consequences for the financial sector. Remittance Inflow (REM), representing funds sent from individuals working abroad back to Nigeria, demonstrates a positive impact on the financial sector with an increase in these funds. In simple terms, a rise in overseas funds entering the country tends to positively stimulate the financial sector, underscoring the positive role of remittances. Capital Remittances (CRM), a specific category of funds sent from abroad, exhibits a minor positive impact on the financial sector. However, this impact is not substantial enough to be considered significant. In other words, it does not exert a substantial influence on the financial sector. Total Remittances Outflows (TRO), representing the overall money flow in and out of the country, has a marginal impact on the financial sector, and this impact is not statistically significant. Simply put, the total money flow in and out of the country does not have a significant effect on the financial sector in the long run.

The analysis highlights the substantial impact of changes in the exchange rate on the financial sector. An increase in the exchange rate tends to positively influence the financial sector, emphasizing the significant role of exchange rate dynamics. Additionally, the analysis indicates that when there is a disparity between the long-term and short-term relationships of these factors, it takes approximately 55% of a year, on average, to restore equilibrium. This implies that disruptions in the balance between these factors require time for correction. Essentially, the study posits that remittances and the exchange rate significantly influence Nigeria’s financial sector positively. Remittances, in particular, emerge as beneficial for the financial sector. On the other hand, capital remittances and the total money flow in and out of the country do not exert a substantial impact on the financial sector. This information holds importance for policymakers and researchers seeking a deeper understanding of how these factors shape the financial sector in Nigeria.

CONCLUSION AND RECOMMENDATIONS

This study examines the impact of remittances on Nigeria’s financial sector over the period from 1986 to 2022, with financial sector output serving as the key metric.The bounds test outcomes indicated a sustained long-term relationship between remittances and the financial sector, signifying that alterations in remittance inflow could lead to corresponding changes in financial sector output in Nigeria. The study’s results demonstrated that remittances played a significant role in fostering the development of the financial sector in Nigeria. Consequently, the conclusion was drawn that remittances had distinct impacts on the two facets of financial sector development measured.

Furthermore, the study unveiled that the cost associated with remittance transactions (CRM) exhibited a positive influence on financial sector output in Nigeria. The exchange rate (EXR) was identified as having a positive and statistically significant impact on financial sector output. Additionally, trade openness (TRO) was found to exert a positive and statistically significant impact on financial sector output in Nigeria. This comprehensive analysis sheds light on the multifaceted influences of remittances, transaction costs, exchange rates, and trade openness on Nigeria’s financial sector, providing valuable insights for policymakers and researchers.

Based on the obtained results, the study proposes the following recommendations:

- The government should implement policies encouraging the prudent use of funds received through remittances, directing them into productive investments. This strategy can stimulate increased inflow of remittances into the country.

- Nigerian government should strive to establish more stable policy measures, enhancing the attractiveness of the country for remittance inflows.

- Policymakers should focus on initiatives that simplify and streamline the process of remittance transfers. This includes reducing transaction fees, simplifying documentation requirements, and collaborating with financial institutions to enhance formal remittance channels.

- Recognizing the substantial positive impact of remittances on the financial sector, policymakers should prioritize initiatives fostering the growth and development of this sector. Measures could include improving access to financial services for remittance-receiving households, promoting financial literacy programs, and supporting the expansion of financial infrastructure.

- To ensure the stability and integrity of the financial sector, policymakers should reinforce regulatory frameworks and supervisory mechanisms. This involves actively monitoring and mitigating risks associated with large remittance inflows, enhancing anti-money laundering and counter-terrorism financing measures, and promoting transparency in remittance transactions.

- Policymakers should persist in pursuing policies promoting trade openness and economic integration. By diversifying the economy and reducing dependency on remittances, Nigeria can strengthen its financial sector and reduce vulnerability to external shocks.

- The Nigerian government, through the Federal ministry of Science and Technology, should allocate resources to develop and upgrade digital infrastructure, particularly in rural areas with limited access to financial services. Embracing financial technology solutions and digital platforms can improve the efficiency, security, and affordability of remittance transfers, stimulating the growth of the financial sector.

REFERENCES

- Adigun, A.O, & Ologunwa, O.P (2017). Remittance and economic growth in Nigeria. International Journal of Research in Management, 7, 29-41

- Engle, R. F., & Granger, C. W. (1987). Co-integration and error correction: representation, estimation, and testing. Econometrica: journal of the Econometric Society, 251-276.

- Gammeltoft, P (2002). Remittances and other financial flows to developing countries. International Migration, 40(5), 181-211

- Muktadir-Al-Mukit, D., & Islam, N. (2016). Relationship between remittance and credit disbursement of the banking sector: A study from Bangladesh. Journal of Business and Management Research 1 (1), 39.

- Ratha, D. (2003). Worker’s Remittances: An Important and stable source of external development finance. Global Development Finance, World Bank, Washinton DC.

- Samuel Osei-Gyebi, Alexander, O., Mary, O.& Lucresse (2023). The effect of remittance inflow on savings in Nigeria: The role of financial inclusion. Article 2220599, accepted 29 May 2023 published online 05 Jun 2023.

- PWC. (2020). The economic power of Nigerians in Diaspora. Retrieved from https://wwwpwc.com

- Larsson, P., & Ångman, J. (2014). Remittances and development: Empirical evidence from 99 developing countries.

- Omobolanle, Y.R, Sheriffdeen, T., &Adesoye, B. (2019). Effect of Remittances on Financial Development in Nigeria. Ife Social Sciences Review Journal 27(1), 48-59

- Markowitz, H. (1952). Portfolio Selection. Journal of Finance. Vol. 7, No 1 (Mar., 1952), pp.77-91(15 pages). Https://doi.org/10.2307/2975974

- Mustapha-Jaji, O. K., &Adesina-Uthman, G. A. (2023). The impact of international remittances on financial development in Nigeria: 1981-2021. Acta Universitatis Danubius.

- Muhammad, D. (2021). Impact of remittances on Nigerian financial sector development: An ARDL Approach. Gusau International Journal of Management and Social Sciences, 4(2), 20-20.

- Mustafa, G., Shah, S. Z., & Iqbal, A. (2020). Impact of foreign remittances on financial development of Pakistan. Journal of Accounting and Finance in Emerging Economies, 6(1), 331-342.

- Nwachukwu, A. C., Ugwuanyi, C. U., & Ezeanyagu, U. K. (2023). Effect of diaspora

- remittances on services sector of the Nigerian economy. Sapientia Global Journal of Arts, Humanities and Development Studies, 6(3).

- Olushola, O., Beyai, P.L, & Anagbado, A. (2023). Taxation and the Challenge of Fiscal Sustainability in a Resource-Rich Developing Country: A Re-evaluation of the Nigerian Perspective. IntechOpen. doi: 10.5772/intechopen.111406

- Pesaran, M. H., Shin, Y., & Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American statistical Association, 94(446), 621-634.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of applied econometrics, 16(3), 289-326.

- Utile, J.S. & Olushola, O. (2023). The Effects of Fiscal Policy on Nigeria’s Economic Growth. International Journal of Humanities Social Science and Management, 3(6), 180-194.