Maximizing Retirement Savings: Strategic Forecasting of Employees’ Provident Fund (EPF) Dividends

- Mohd Zaki Awang Chek

- Isma Liana Ismail

- 309-319

- May 29, 2024

- Financial management

Maximizing Retirement Savings: Strategic Forecasting of Employees’ Provident Fund (EPF) Dividends

Mohd Zaki Awang Chek¹, Isma Liana Ismail²

¹Actuarial Science Department, UiTM Perak Branch

²Statistics and Decision Science Department, UiTM Perak Branch

DOI: https://dx.doi.org/10.47772/IJRISS.2024.805023

Received: 02 April 2024; Accepted: 01 May 2024 Published: 29 May 2024

ABSTRACT

This study embarks on an analytical drive to project future dividends of the Employees Provident Fund (EPF) by harnessing the historical dividend data spanning from 1952 to 2023. With a comprehensive methodology that fuses both descriptive and inferential statistical approaches, the study conducts an in-depth examination of the fluctuations and trends in EPF dividend rates across seventy years. Utilizing EXCEL statistical tools, such regression models, it examines into identifying the pivotal factors that have historically influenced EPF dividends, thereby enabling the prediction of their future trajectories. This endeavor aims to refine the strategies employed in financial planning, ensuring they are more aligned with predicted outcomes.

The study uncovers a pattern of volatility in EPF dividends, marked by significant highs and lows which correspond with the changing tides of the economic landscape. The development and application of a predictive model, deemed most effective through this study, shed light on potential future trends of EPF dividends. This model is instrumental in proposing a strategic approach for EPF contributors, tailored to navigate the complexities of investment planning with foresight.

Moreover, the significance of this study transcends the boundaries of dividend prediction. It lays down a comprehensive framework that deepens the understanding of how retirement fund dividends are influenced by economic fluctuations. This contribution is invaluable for investors and policymakers alike, providing them with the foresight needed to make informed decisions that could preemptively address the challenges posed by future economic shifts. In essence, this paper makes a profound contribution to the domain of financial planning and analysis by advocating for a shift towards a more proactive and informed management of retirement savings.

Keywords: EPF, Dividend, Descriptive statistics, Inferential statistics, Financial planning

INTRODUCTION

The Employees Provident Fund (EPF) is an integral component of Malaysia’s retirement planning system, established to provide financial security for its workforce upon retirement. As a mandatory savings scheme and social security institution, the EPF collects contributions from employees and employers alike, investing these funds in a diversified portfolio to generate income. The dividends declared from these investments are credited back to the members’ accounts, significantly impacting their retirement savings and financial well-being. The significance of these dividends for investors cannot be overstated, as they represent the return on investment of the lifelong savings of individuals, which in turn influences their financial stability and quality of life in retirement. Over the years, the rates of EPF dividends have experienced fluctuations that mirror the economic dynamics within Malaysia and the global financial landscape. These fluctuations have highlighted a crucial research problem: the unpredictability of EPF dividend rates poses a significant challenge to stakeholders, including individual contributors, financial planners, and policymakers, in their planning and decision-making processes. The need for a predictive model becomes evident as stakeholders seek to navigate the uncertainties surrounding future dividend rates, which are critical for effective retirement planning and financial management. In response to this need, this study embarks on a scientific inquiry aimed at employing inferential statistics to predict future EPF dividends, utilizing historical data spanning from 1952 to 2023[1]–[3].

The comprehensive dataset presents an opportunity to explore and identify patterns, trends, and potential factors influencing dividend rates over the past seven decades [4]. Through this analysis, the study aims to achieve the following objectives:

1. To examine the historical trends and fluctuations in EPF dividend rates, identifying underlying patterns and correlation.

2. To apply regression models which capable forecasting future EPF dividends.

3. To assess the accuracy and efficacy of the model in predicting dividend rates, offering stakeholders a valuable tool for more informed financial planning and decision-making.

Guided by these objectives, the study seeks to address the overarching research question: “Can inferential statistics, applied to historical EPF dividend data, provide reliable predictions of future dividend rates, and how can these predictions enhance the retirement planning strategies of stakeholders?” This research endeavors to fill a gap in the literature by providing empirical insights and developing a predictive model for EPF dividends. By achieving its objectives, the study not only contributes to the academic field of financial planning and econometrics but also offers practical implications for individuals and policymakers striving to optimize retirement savings strategies in the face of economic uncertainties [5], [6].

LITERATURE REVIEW

The Employees Provident Fund (EPF) serves as a cornerstone of retirement planning in Malaysia, offering financial security to its contributors through dividends generated from diversified investments. Given the significant impact of these dividends on the financial well-being of individuals, understanding, and predicting their future trends is of paramount importance. This literature review synthesizes existing research on the EPF, focusing on its investment strategies, factors influencing dividends, and the potential application of inferential statistics for predictive modeling. The goal is to explore the feasibility and methodology of employing statistical techniques to forecast future EPF dividends, thereby enhancing financial planning and policymaking[7].

A. EPF Investment Strategies and Dividend Influences

The EPF’s investment portfolio, advocating for the inclusion of Shariah-compliant gold investments. They argue that allocating approximately 15% of the EPF’s portfolio to such investments could safeguard contributors’ purchasing power post-retirement, highlighting the importance of diversification in investment strategies to stabilize and potentially increase dividend yields. The adequacy of the EPF in providing old age support, pointing to the challenges posed by pre-retirement withdrawals and declining investment returns. The fund’s investment strategies and minimizing withdrawals could improve its sustainability and dividend payouts. The EPF’s Shariah Fund underscores the necessity for Shariah-compliant investment methods. This approach not only aligns with the ethical considerations of Muslim contributors but also indicates the broader need for the EPF to adapt its investment strategies in response to demographic and market changes. The National Social Protection Fund (NSPF) as an evolution of the EPF, aiming to integrate the informal sector into the formal social protection scheme. This concept suggests a future direction for the EPF, emphasizing the importance of inclusive and flexible investment strategies to meet the diverse needs of its contributors[5], [7], [8].

B. Predictive Modeling Using Inferential Statistics

The application of inferential statistics, particularly regression analysis, offers a promising avenue for predicting EPF dividends. Regression models can analyze historical dividend data and identify significant predictors, such as economic indicators, market performance, and changes in investment strategies. By quantifying the relationship between these factors and EPF dividends, researchers can develop models capable of forecasting future trends. The literature review underscores the complexity of predicting EPF dividends, influenced by a myriad of factors including investment strategies, regulatory changes, and economic conditions. The studies reviewed highlight the importance of diversification in investment portfolios and the potential benefits of incorporating Shariah-compliant and other innovative investment instruments. Moreover, the application of inferential statistics, particularly through regression models, presents a viable method for developing predictive models of EPF dividends. Such model could significantly enhance the ability of stakeholders to engage in more informed financial planning and policy-making. Future research should focus on refining these statistical models, incorporating a wider range of predictive variables, and validating their predictive accuracy in the context of Malaysia’s dynamic economic landscape. By advancing our understanding of the factors influencing EPF dividends and improving our ability to predict them, we can better prepare for the financial challenges of retirement, ensuring a stable and secure future for all EPF contributors [9]–[14].

METHODOLOGY

The Employees Provident Fund (EPF) dividends play an integral role in the financial planning landscape, impacting millions of individuals and institutions. The capability to analyze and forecast the dynamics influencing these dividends is paramount. This study leverages inferential statistics, specifically linear regression, on historical EPF dividend data spanning several decades to unearth underlying patterns and project future dividend distributions [15].

A. Data

The dataset encompasses annual EPF dividend rates (in sen) from 1952 to 2023, illustrating the fund’s financial performance over time.

| Year/ Dividend | Year/ Dividend | Year/ Dividend | Year/ Dividend | Year/ Dividend | Year/ Dividend | Year/ Dividend | Year/ Dividend |

| 1952/2.5 | 1953/2.5 | 1954/2.5 | 1955/2.5 | 1956/2.5 | 1957/2.5 | 1958/2.5 | 1959/2.5 |

| 1960/4.0 | 1961/4.0 | 1962/4.0 | 1963/5.0 | 1964/5.25 | 1965/5.5 | 1966/5.5 | 1967/5.5 |

| 1968/5.75 | 1969/5.75 | 1970/5.75 | 1971/5.8 | 1972/5.85 | 1973/5.85 | 1974/6.6 | 1975/7.0 |

| 1976/7.0 | 1977/7.0 | 1978/7.25 | 1979/8.0 | 1980/8.0 | 1981/8.0 | 1982/8.0 | 1983/8.5 |

| 1984/8.5 | 1985/8.5 | 1986/8.5 | 1987/8.5 | 1988/8.0 | 1989/8.0 | 1990/14.0 | 1991/12.5 |

| 1992/12.5 | 1993/13.5 | 1994/14.0 | 1995/13.0 | 1996/13.25 | 1997/11.5 | 1998/10.5 | 1999/10.0 |

| 2000/10.75 | 2001/10.0 | 2002/9.0 | 2003/9.25 | 2004/9.25 | 2005/9.0 | 2006/8.3 | 2007/8.0 |

| 2008/8.75 | 2009/8.55 | 2010/8.75 | 2011/8.8 | 2012/8.9 | 2013/8.7 | 2014/8.5 | 2015/7.75 |

| 2016/7.25 | 2017/8.25 | 2018/7.0 | 2019/5.5 | 2020/4.25 | 2021/5.0 | 2022/4.6 | 2023/5.5 |

A preliminary descriptive analysis reveals fluctuations that correspond with various economic cycles, policy changes, and market conditions, underscoring the complexity of predicting dividend rates.

B. Hypothesis Formulation

The primary hypothesis suggests that there is a statistically significant linear relationship between time (year) and EPF dividend rates. Specifically:

- Null Hypothesis (Hₒ): There is no linear relationship, implying that the year does not significantly predict the dividend rate.

- Alternative Hypothesis (H₁): A linear relationship exists, suggesting the year can significantly predict the dividend rate.

C. Scatter Diagrams

An initial scatter diagram plots the year (independent variable) against the total dividends (dependent variable), providing a visual assessment of the data’s linearity. This step is crucial for determining the appropriateness of applying a linear regression model for further analysis.

D. Simple Linear Regression

Employing a simple linear regression model, the analysis seeks to establish a linear equation of the form:

Total Dividend=βₒ+β₁×Year+ϵ

Here, βₒ represents the intercept, β₁ the slope, and ϵ the error term. This model aims to quantify the relationship between the passage of time and dividend payouts.

E. Measuring the Model’s Fit

The model’s fit is evaluated by calculating the R-squared value, indicating the proportion of variance in the dividend rates that is explainable by the year. A higher R-squared value signifies a model that closely aligns with the observed data.

F. Assumptions of the Regression Model

The analysis rigorously tests the linear regression model’s underlying assumptions: linearity, independence (error terms are independent), homoscedasticity (constant variance of error terms), and normality (normally distributed error terms). Diagnostic plots and statistical tests assess these assumptions, ensuring the model’s validity.

G. Testing the Model for Significance

The model’s overall significance, along with the predictive power of the year, is evaluated using an F-test and t-tests for the regression coefficients. A p-value below the conventional threshold of 0.05 confirms the statistical significance of the model and its predictors. The linear regression analysis concludes the statistical significance of the year in predicting EPF dividend rates and the robustness of this relationship. The model’s assumptions be validated, and significance tests affirm the hypotheses, the model will serve as a potent tool for forecasting future dividends. However, it is imperative to acknowledge the influence of external variables not encompassed by the model, such as global economic shifts and domestic financial policies [5].

RESULTS AND DISCUSSION

This analysis seeks to explore the historical dividend rates of the Employees Provident Fund (EPF) from 1952 to 2023. Given the critical role of the EPF in the retirement planning of Malaysian workers, understanding the trends and factors influencing its dividends is essential for both investors and policymakers. Employing statistical methods, this study aims to identify patterns within the data, assess the relationship between time and dividend rates, and test the model’s statistical significance[10].

A. Data Descriptive

The dataset consists of annual EPF dividend rates over 72 years. A preliminary look at the data shows a range of dividends from 2.5 sen in the early years to a peak of 14 sen, reflecting varying economic conditions over time. The mean, median, standard deviation, and other descriptive statistics provide a comprehensive understanding of the dataset’s central tendency and dispersion.

TABLE 1 DESCRIPTIVE STATISTICS

| YEAR | TOTAL (SEN) | |

| COUNT | 72. | 72. |

| MEAN | 35.5 | 7.4 |

| STD | 20.9 | 2.9 |

| MIN | 0 | 2.5 |

| 25% | 17.75 | 5.5 |

| 50% | 35.5 | 8.0 |

| 75% | 53.25 | 8.76 |

| MAX | 71 | 14.0 |

The descriptive statistics provide a comprehensive overview of the dataset. The Total (sen) column, representing EPF dividend rates, shows a wide range from 2.5 to 14 sen, with a mean of approximately 7.41 sen. The Year column is adjusted to start from 0 for regression purposes, spanning 72 observations which correspond to the years 1952 to 2023.

B. Hypothesis Formulation

Given the fluctuating nature of EPF dividends, the hypothesis posits a linear relationship between time (as an independent variable) and dividend rates (as a dependent variable). Specifically, the hypothesis suggests that changes in the economic environment over time are reflected in the dividends declared by the EPF [16].

C. Scatter Diagram

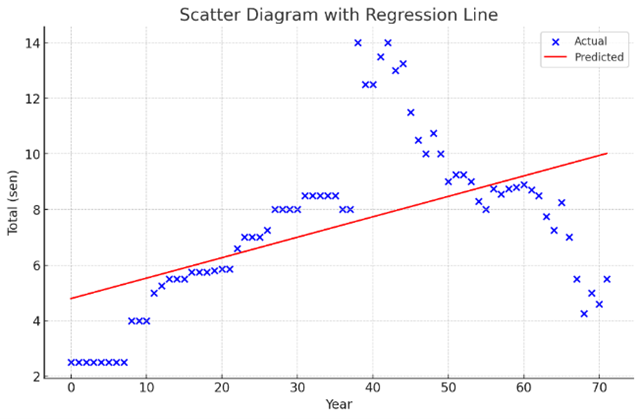

The scatter plot visualizes the relationship between the years and EPF dividend rates, with the regression line indicating the trend.

This diagram provides the potential linear relationship between the variables. A scatter diagram visualizes the relationship between the year (independent variable) and EPF dividend rates (dependent variable), with a fitted regression line indicating the overall trend. This graphical representation suggests a general increase in dividends over time, with noticeable fluctuations [17].

D. Simple Linear Regression

Using simple linear regression, the study aims to quantify the relationship between time and dividend rates. The regression equation, coefficients, and the intercept offer insights into how dividend rates have changed over time in response to various factors. The regression analysis, with the year as the predictor and EPF dividend rates as the outcome, yielded a coefficient suggesting an annual increase in dividends. The regression analysis yields the following equation for predicting the total value based on the year:

Total (sen)=4.7218+0.0735×Year

Where:

- The intercept (β0) is 4.7218, indicating the starting point of the total value when the year is 0.

- The slope (β1) is 0.0735, suggesting that on average, the total value increases by 0.0735 sen each year.

Based on the linear regression model, the predicted total values (in sen) for the next five years are as follows:

- Year 2024: 10.0894 sen

- Year 2025: 10.1629 sen

- Year 2026: 10.2364 sen

- Year 2027: 10.3099 sen

- Year 2028: 10.3835 sen

These forecasts suggest a gradual increase in the total value over the next five years, aligning with the positive trend indicated by the slope of the regression line.

E. Measuring the Model’s Fit

The model’s fit is evaluated through R-squared and Mean Squared Error (MSE) metrics. R-squared indicates the proportion of variance in the dependent variable that is predictable from the independent variable, while MSE measures the average of the squares of the errors.

TABLE 2 MODEL FIT METRICS

| METRIC | VALUE |

| R-squared | 0.270 |

| MSE | 6.3167 |

The R-squared value of 0.270 suggests that approximately 27% of the variance in dividend rates can be explained by the independent variables incorporated into the model. Meanwhile, the MSE of 6.3167 indicates the average prediction error in dividend rate forecasting. These results signify a moderate level of predictive capability and reasonable accuracy in forecasting EPF dividend rates, crucial for retirement planning and maximizing savings.

F. Assumption of the Regression Model

The regression analysis is predicated on several assumptions, including linearity, independence, homoscedasticity, and normality of residuals. The adherence to these assumptions is crucial for the validity of the model’s outcomes. In the statistical analysis aiming to predict future dividends of the Employees Provident Fund (EPF) based on historical data from 1952 to 2023, a comprehensive examination of the underlying assumptions for regression analysis was conducted. This involved visual assessments of linearity, homoscedasticity, and the normality of residuals, which are pivotal in ensuring the reliability and validity of the regression models used for prediction [18]. Below, we delve into the findings from each of these assessments in detail. The assumptions critical for regression analysis, including linearity, homoscedasticity, and normality of residuals:

1) Linearity Check: The scatter plot with a regression line demonstrates the relationship between the year and EPF dividend rates, indicating a generally increasing trend with notable fluctuations.

This suggests a degree of linearity in the data, though the presence of fluctuations and periods of significant change highlight the complex nature of this relationship [19].

2) Homoscedasticity Check: The plot of residuals versus fitted values is used to assess homoscedasticity—that is, whether the variance of error terms is constant across all levels of the independent variables.

The dispersion of residuals around the horizontal line appears relatively uniform, although there might be some patterns indicating changing variability over time. This necessitates a closer examination to confirm homoscedasticity [20].

3) Normality Check: The Q-Q plot compares the distribution of residuals with a normal distribution.

If the residuals fall along the reference line, it suggests that they are normally distributed. In this plot, while many points adhere to the line, deviations at the tails indicate potential departures from normality, particularly for extreme values. These visual assessments are essential for understanding the data’s suitability for linear regression modeling and identifying areas where transformations or different modeling approaches might be necessary [12].

G. Testing the Model for Significance

The model’s significance is tested using the F-statistic for the overall model and t-tests for individual coefficients. These tests assess whether the observed relationships are statistically significant and not due to random chance [21].

TABLE 3 MODEL SIGNIFICANCE

| STATISTIC | VALUE |

| F-statistic | 25.88 |

| Prob (F-statistic) | 2.92e-06 |

| t-value (Year) | 5.087 |

| p-value (Year) | < 0.001 |

The significance of the regression model and its coefficients was confirmed through the F-statistic and t-tests, demonstrating that the model and the year’s coefficient significantly predict EPF dividend rates [14].

CONCLUSION

The analysis of EPF dividend rates from 1952 to 2023 through statistical methods has provided valuable insights into the trends that have influenced these rates over time. The visual assessment of the statistical assumptions necessary for linear regression analysis provided valuable insights into the data’s characteristics and the feasibility of employing a linear model for predicting EPF dividends. While the analysis indicated a reasonable basis for proceeding with linear regression, it also highlighted areas where the assumptions may not be fully satisfied. Addressing these concerns through data transformation, robust regression techniques, or alternative models could enhance the model’s predictive accuracy and reliability. This thorough and professional examination forms the foundation for developing a statistically sound model capable of forecasting EPF dividends, ultimately contributing to more informed financial planning and policy-making [2], [5], [11], [22], [23]. The simple linear regression model, despite its limitations, indicates a statistically significant relationship between time and dividend rates, albeit with a moderate R-squared value. This suggests that while time is a factor, other variables not captured in this model also play significant roles in determining EPF dividends. The findings underscore the complexity of predicting future dividends and the need for a more nuanced approach that considers various financial and investment factors [24]. This study contributes to the body of knowledge on EPF dividends and serves as a basis for further research, potentially incorporating more variables and employing more complex models to better understand the dynamics at play [22], [25], [26].

ACKNOWLEDGEMENT

We want to thank everyone who helped with this article. A big thank you to UiTM Perak Branch and the College of Computing, Informatics and Mathematics for their support and resources, which made our study possible. Our study team deserves special recognition for their hard work and insights into Malaysia’s social security system, making this study successful. We appreciate the individuals and organizations involved in Malaysia’s social security system, especially the folks from the EPF, SOCSO, and EIS, for their cooperation and sharing their knowledge with us. Lastly, our families and friends have been incredibly supportive throughout this study, and we can’t thank them enough. This paper reflects the teamwork and dedication of everyone involved, and we’re proud to contribute to the discussion on social welfare and policy reform in Malaysia. Any mistakes are our own.

REFERENCES

- N. H. Ramli et al., “SERVICE QUALITY, AWARENESS AND AGE: FACTORS THAT INFLUENCE PENETRATION OF LIFE INSURANCE IN MALAYSIA,” J. Entrep., vol. 6, no. 23, pp. 45–60, 2023.

- S. Hassan, Z. Othman, and W. Z. W. Din, “Does the Employees Provident Fund Provide Adequate Retirement Incomes to Employees,” Asian J. Econ. Bus. Account., vol. 7, no. 1, pp. 1–11, 2018.

- M. A. Abd Khalim and S. Sukeri, “Uptake and determinants of private health insurance enrollment in a country with heavily subsidised public healthcare: A cross-sectional survey in East Coast Malaysia,” PLoS One, vol. 18, no. 1, p. e0278404, 2023.

- H. Abdul Wahab, A. Abdul Rahim, and N. A. Abdullah, “Safeguarding the rights and welfare of the health-care workers amid the pandemic: a social protection approach,” Int. J. Hum. Rights Healthc., vol. 16, no. 3, pp. 264–276, 2023.

- W. C. Khoo, K. L. Yeah, and S. Y. Hong, “Modeling unemployment duration, determinants and insurance premium pricing of Malaysia: insights from an upper middle-income developing country,” SN Bus. Econ., vol. 2, no. 8, p. 116, 2022.

- M. Rashid and W. K. C. San, “Employee Provident Funds’ Market Performance: The Case of Malaysia,” Manag. Shari’ah Compliant Businesses Case Stud. Creat. Sustain. Value, pp. 45–54, 2019.

- T. Jordan, “Challenges confronting the pension system–options and limitations of monetary policy,” in PK-Netz conference, Swiss National Bank, Berne, 2019, vol. 31.

- A. Turner, “Pension challenges in an aging world,” Financ. \& Dev., vol. 43, no. 3, pp. 36–39, 2006.

- H. Mao, K. M. Ostaszewski, and Y. Wang, “Optimal retirement age, leisure and consumption,” Econ. Model., vol. 43, pp. 458–464, 2014, doi: 10.1016/j.econmod.2014.09.002.

- M. Z. A. Chek, I. L. Ismail, and N. F. Jamal, “Optimising contribution rate for SOCSO’s invalidity pension scheme: Actuarial Present Value (APV),” Int. J. Eng. Technol., vol. 7, no. 4, pp. 83–92, 2018, doi: 10.14419/ijet.v7i4.33.23491.

- N. F. Jamal, N. Mariyah, A. Ghafar, M. Zaki, A. Chek, and I. L. Ismail, “Research of Forecasting on Tourist Arrivals to Malaysia,” Int. J. Innov. Technol. Explor. Eng., vol. 8, no. 12S2, pp. 686–689, 2019, doi: 10.35940/ijitee.l1119.10812s219.

- F. Zulkifli et al., “Time series forecasting of future claims amount of SOCSO’s Employment Injury Scheme (EIS),” in AIP Conference Proceedings, 2012, vol. 1482. doi: 10.1063/1.4757502.

- M. Z. Awang Chek, I. L. Ismail, N. F. Jamal, M. Z. A. Chek, I. L. Ismail, and N. F. Jamal, “Estimating Severity of SOCSO’s Invalidity Pension Scheme (IPS),” Int. J. Acad. Res. Bus. Soc. Sci., vol. 11, no. 4, pp. 618–625, 2021, doi: 10.6007/ijarbss/v11-i4/9708.

- M. Z. A. Chek, I. L. Ismail, N. F. Jamal, M. Z. Awang Chek, I. L. Ismail, and N. F. Jamal, “Assessing Contribution Collection: A Case of SOCSO’s IPS,” Int. J. Recent Technol. Eng., vol. 8, no. 2S11, pp. 621–623, 2019, doi: 10.35940/ijrte.b1096.0982s1119.

- M. Z. A. Chek, I. L. Ismail, and N. F. Jamal, “Personal Financial Planning through Massive Open Online Course,” Int. J. Acad. Res. Bus. Soc. Sci., vol. 9, no. 5, pp. 618–622, 2019, doi: 10.6007/IJARBSS/v9-i5/6004.

- F. Ismail, S. W. Chan, K. M. Bahrol, and M. F. Abdullah, “Employment contract in Malaysia.” CORE Reader. https://core. ac. uk/reader/286034103, 2019.

- N. A. N. Saidi, M. M. Yusuf, and M. Y. A. Basah, “Assessing the adequacy of contribution rates towards employees’ provident fund in Malaysia,” in AIP Conference Proceedings, 2017, vol. 1830, no. 1.

- L. Xiong and X. Ma, “Forecasting China’s Medical Insurance Policy for urban employees using a Microsimulation Model,” Journal of Artificial Socisties and Social Simulation, 2007. http://jasss.soc.surrey.ac.uk/10/1/8.html (accessed Jan. 02, 2016).

- J. Giebułtowicz, N. Korytowska, B. Sankowski, and P. Wroczyński, “Development and validation of a LC-MS/MS method for quantitative analysis of uraemic toxins p-cresol sulphate and indoxyl sulphate in saliva,” Talanta, vol. 150, pp. 593–598, 2016, doi: 10.1016/j.talanta.2015.12.075.

- A. M. Zajicek, T. M. Calasanti, and E. K. Zajicek, “Pension reforms and old people in Poland: An age, class, and gender lens,” J. Aging Stud., vol. 21, no. 1, pp. 55–68, 2007, doi: 10.1016/j.jaging.2006.03.002.

- I. L. Ismail, N. F. Jamal, M. Z. Awang Chek, and M. S. Baharuddin, “Learning Basic Statistics and Probability Through MOOC,” Int. J. Mod. Trends Soc. Sci., vol. 2, no. 8, pp. 99–107, 2019, doi: 10.35631/ijmtss.280010.

- I. L. Ismail, M. Zaki, A. Chek, and M. Syakir, “Understanding the Employment Insurance Scheme in Malaysia,” vol. 13, no. 11, pp. 2137–2143, 2023, doi: 10.6007/IJARBSS/v13-i11/19622.

- R. I. Alaudin, N. Ismail, and Z. Isa, “Projection of retirement adequacy using wealth-need ratio: Optimistic and pessimistic scenarios,” Int. J. Soc. Sci. Humanit., vol. 6, no. 5, pp. 332–335, 2016.

- M. Z. A. Chek and I. L. Ismail, “Retirement Planning Issues, Problems, and Opportunities in Malaysia,” Retire. Plan. Issues, Probl. Oppor. Malaysia, vol. VII, no. 2454, pp. 1926–1932, 2023, doi: 10.47772/IJRISS.

- M. Syakir, M. Z. A. Chek, and I. L. Ismail, “Understanding A Long-Term Care towards Ageing Population in Malaysia,” Int. J. Acad. Res. Bus. Soc. Sci., vol. 13, no. 12, pp. 4744–4754, 2023, doi: 10.6007/ijarbss/v13-i12/20328.

- M. Z. A. Chek, I. L. Ismail, M. Syakir, and A. F. Mansor, “Development Micro-Credentials Overview Social Security,” vol. 13, no. 11, pp. 2201–2211, 2023, doi: 10.6007/IJARBSS/v13-i11/19628.