Measuring Competency Impact on Shariah Audit Effectiveness: A Systematic Literature Review

- Mohd Suffian bin Mohamed Esa

- Hairunnizam bin Wahid

- Salmy Edawati Yaacob

- Wan Nur Fazni Wan Mohamad Nazarie

- Abdul Hayy Haziq Mohamad

- 2077-2091

- Mar 8, 2025

- Social Science

Measuring Competency Impact on Shariah Audit Effectiveness: A Systematic Literature Review

Mohd Suffian bin Mohamed Esa1*, Hairunnizam bin Wahid2, Salmy Edawati Yaacob3, Wan Nur Fazni Wan Mohamad Nazarie4, Abdul Hayy Haziq Mohamad5

1,3Institute of Islam Hadhari, Universiti Kebangsaan Malaysia, Malaysia

2Faculty of Economics and Management, Universiti Kebangsaan Malaysia, Malaysia

4Faculty of Economics and Mualamat, Universiti Sains Islam Malaysia, Malaysia

5School of Business and Management, University of Technology Sarawak, Malaysia

DOI: https://dx.doi.org/10.47772/IJRISS.2025.9020166

Received: 31 January 2025; Accepted: 04 February 2025; Published: 08 March 2025

ABSTRACT

The effectiveness of Shariah audits in Malaysia is hindered by competency issues, including inadequate skills, lack of professional certification, and insufficient experience among Shariah auditors, particularly within Islamic financial institutions and sectors like zakat and waqf. The shortage of skilled professionals and weak Shariah governance frameworks in zakat and waqf organizations pose significant challenges to ensuring financial integrity and accountability, necessitating urgent efforts to strengthen Shariah audit competencies in these areas. The objective of this paper is to review the proficiency of Shariah auditors and their influence on the efficiency of Shariah audits on a global scale. This research holds significance as it aims to assess the impact of competency on Shariah audit effectiveness through a systematic literature review, providing valuable insights for enhancing the quality and rigor of Shariah audit practices. Five major methodological phases were incorporated in the evaluation processes including the development of research questions under the guidance of the review protocol, followed by systematic search strategies based on identification, screening, and eligibility on several well-known databases, including Scopus, Web of Science and Google Scholar. Finally, the quality of the search results was evaluated, and data was extracted and analyze. Three significant themes were identified as a result of the thematic analysis: (1) Competency; (2) Institution (3) Code of Ethic. From these three basic concepts, 12 sub-themes were developed. This study gives a broad review of the most recent developments in measuring competency as an impact on shariah audit effectiveness. The results might assist policymaker, government, and public sectors idea in tackling competency issues such as developing Shariah audit competency framework. The discussion further underscores the significance of Shariah audit competency in the realm of zakat and waqf operations, highlighting its pivotal role in ensuring compliance with Islamic principles and regulations.

Keywords: Shariah Audit, Competency, Effectiveness, Shariah Audit Competency Framework, Zakat and Waqf

INTRODUCTION

In Malaysia, shariah audit practices began as part of Islamic Financial Institutions (IFI’s) audit function (MIA, 2023). Shariah Audit is defined in the Shariah Governance Policy Document (SGPD) 2019 as “a service which delivers an independent evaluation on the reliability and efficacy of the IFI’s internal control, risk management systems, governance processes, as well as the overall Shariah compliance of the IFI’s operations, business, affairs, and activities.” These wide definitions adapted from the IIA suit each sector’s varying activities/operations and needs in complying with Shariah principles.

Numerous past studies have addressed issues regarding competency in Shariah auditing, reflecting a range of global concerns (Alam, 2017; Ali, 2019; Ali 2015; Mahzan and Yahya, 2014). Among these are issues related to inadequate skills and experience among Shariah auditors, the absence of professional certification in Shariah fields, and competency problems pertaining to both Shariah jurisprudence and auditing, all of which contribute to the ineffectiveness of Shariah audits (Mahzan and Yahya, 2014). Furthermore, many studies have focused on the effectiveness of Shariah audit programs and activities. However, to the best of our knowledge, research on the role of competency in enhancing the effectiveness of Shariah audit functions and roles has been relatively limited.

The recent emphasis on Shariah audit competencies within the Islamic finance industry, particularly in banking and takaful sectors, is undoubtedly important given the sector’s significant role in the global economy. However, it could be argued that the criticality of Shariah audit competencies extends beyond banking and takaful to encompass other Islamic financial sectors such as zakat and waqf industries. Unlike banking and takaful, where regulatory frameworks and governance structures are relatively established, the zakat and waqf sectors often lack robust Shariah governance mechanisms, making competent Shariah audit even more imperative. In the absence of adequate monitoring, there exists an increased likelihood of mishandling or inappropriate utilization of funds designated for charitable aims, which undermines the reliability and effectiveness of these fundamental social welfare systems.

The findings from the White Paper on Shariah Audit underscore the pressing need for talent development in the field of Shariah audit, particularly in Malaysia. The shortage of skilled professionals in Shariah audit poses a significant obstacle to the effective implementation of Shariah governance practices, not only in Islamic financial institutions but also in State Islamic Religious Councils (SIRCs), which oversee zakat and waqf organizations (Shafii et al., 2023). Given that SIRCs function as the Islamic fiscal treasuries for Muslim communities, ensuring robust Shariah audit practices within these councils is paramount. However, the challenges highlighted in the report, such as inadequate talent and institutional hurdles, underscore the urgent need for concerted efforts to strengthen Shariah audit competencies in SIRCs to uphold financial integrity and accountability within zakat and waqf sectors, ultimately benefiting Muslim communities.

In summary, the competencies of Shariah auditors are essential for maintaining the integrity of Shariah governance, mitigating risks, ensuring ethical conduct, and upholding the trust of stakeholders. Effective Shariah audit requires individuals with a strong foundation in Islamic principles and auditing expertise. Ensuring effective Shariah audit requires a strengthening of competency aspects for Shariah auditors. Therefore, this study aims to review competency aspects in enhancing the effectiveness of Shariah auditing through a systematic literature review. An important contribution of this research lies in the identification of key concepts related to Shariah auditor competencies to be developed across various industries. Furthermore, this research will aid in introducing and preparing for the establishment and enhancement of the function and role of Shariah audit within State Islamic Religious Councils (SIRCs).

METHODOLOGY

Review Protocol – ROSES

ROSES (Reporting Standards for Systematic Evidence Syntheses) serve as the SLR’s guiding principle. Gusenbauer and Haddaway (2020) developed ROSES with the intention of improving and maintaining a sound approach for creating an SLR through improved transparency as well as to guarantee and manage the review’s quality (Higgins et al., 2011). ROSES served as a guide for the SLR process, which started with the formulation of the research questions using the PICo technique, which stands for Problem or Population, Interest, and Context. Identifying, screening, and eligibility were the next three systematic phases of the approach for document searching that were established and carried out. A quality appraisal process was then conducted based on the adapted criteria outlined by (Hong et al., 2018). Here, the caliber of each chosen item was evaluated prior to its inclusion in the review. The chosen papers were then put through several steps, including data extraction and data analysis. The core research topic served as the basis for the data extraction procedure, and the qualitative data synthesis (thematic synthesis) approach was used to analyze the gathered data. To make sure the review process achieved the review’s purpose, the authors followed the recommendations made in the review when it was appropriate.

Formulation of the research question

Initially, concepts from earlier works by (Shafii et al., 2013), (Haron and Khalid, 2018), and (Kamaruddin et al., 2023) were used to develop the research topic. Those articles discussed competency or effectiveness in shariah auditing. Furthermore, this study using the PICo approach, which stands for “P” (population or problem), “I” (interest), and “Co” (context) (Lockwood et al., 2015). Based on these ideas, the authors included three key elements in the review: the population of the global, interest in competency and effectiveness, and context on shariah audit. As a result, the authors were able to develop the study’s core research question: “How does the development of competency impact Shariah audit effectiveness?”

The strategies of systematic searching

(Shaffril et al., 2018) proposed three systematic procedures for identification, screening, and eligibility. The authors were able to comprehensively discover and synthesize the research using these strategies.

Identification

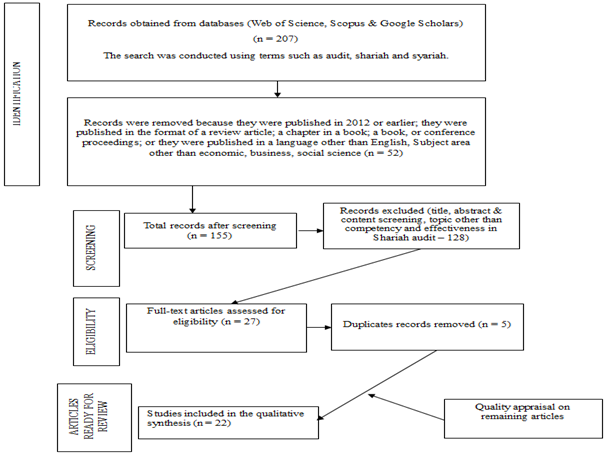

Two significant keywords were identified based on the research questions: shariah and audit. To improve these keywords, the authors used an online thesaurus, referred to keywords used in prior studies, referred to keywords suggested by Scopus, and collaborated with specialists. These term combinations were examined using search features such as field code functions, phrase searching, wildcards, truncation, and Boolean operators in two databases: Web of Science and Scopus. (Table 1). Moreover, the search was conducted using a manual search technique in databases such as Google Scholar. Due to the search efforts, a total of 207 potential articles were found from the selected databases.

Table 1. Search string used in the selected database

| Database | String |

| Scopus | TITLE-ABS-KEY ( audit AND ( shariah OR syariah ) ) |

| Web of Science | TS=( audit AND ( shariah OR syariah ) ) |

Screening

The next step was screening, whereby papers were either included or excluded from the study (through the database or manually by the authors) according to a set of criteria (see Table 2). Considering the significance of research field maturity, as mentioned by (Kraus et al., 2020), the selection procedure for this study was limited to articles published between 2013 and 2023. This timeframe was chosen because there was sufficient published research to conduct a representative evaluation. Because empirical research publications give primary data, the writers selected to review these. To avoid misunderstanding, only those written in English were evaluated. Because this study focuses on management influence, research studies in economic, business, and social sciences were chosen to increase the possibility of receiving more publications relevant to economic studies. 52 articles were removed from the evaluation during this stage because they did not match the inclusion criteria. As a consequence, 155 items were left for consideration in the following phase.

Table 2. Inclusion and exclusion criteria

| Inclusion Criteria | Exclusion Criteria |

| 2013 – 2023

Articles (with empirical data) |

2012 and earlier

Review article, chapter in a book, book, conference proceeding, etc |

| English | Non-English |

| Economic, business, social science | Subject areas other than economics, business, and social science |

Eligibility

The remaining papers were manually checked by the authors to see if they fulfilled the defined inclusion criteria (by reading their titles, abstracts, and full text) and only concentrated on the competency and effectiveness subject. During this stage, 128 articles were omitted because they did not emphasize shariah auditing and did not focus on competency and effectiveness. There were 22 papers in total for the quality assessment stage. (See Fig. 1)

Figure 1. Flow diagram of searching process

Quality appraisal

The quality evaluation stage was carried out to ensure that the method and analysis of the chosen studies were conducted appropriately. The Mixed-Method Appraisal Tool (MMAT) developed by (Hong et al., 2018) was utilized for this purpose. MMAT allows researchers to evaluate a systematic mixed studies review and encompasses five types of studies: qualitative research, randomized controlled trials, non-randomised studies, quantitative descriptive studies, and mixed techniques studies (Hong et al., 2018).

MMAT assisted in emphasizing criteria such as the relevancy of the research questions to provide sufficient data, the adequacy of qualitative data collection to address the research questions, and the coherence between qualitative data sources, gathering, analysing, and interpreting the data. The authors relied on assessment criteria such as the relevance of the sampling approach to the research questions, the sample’s representativeness to its population, the appropriateness of the measurement, and the adequacy of the analysis done for quantitative research design. Furthermore, MMAT assisted in providing direction pertaining to the rationale for using the mixed-method to address the research questions, the effectiveness of the different research designs to answer the research questions, the integration of qualitative and quantitative, and the ability to address the divergence and differences between research designs in order to control the quality from a methodological and analysis perspective for mixed-method research designs.

The corresponding author then assessed the methodological and analytical rigour of each publication with the help of two co-authors. Each publication was thoroughly reviewed, with an emphasis on the methods component and the analysis performed. The writers examined the publications using MMAT as a guide. Each item was evaluated based on five criteria, with three options to give their answers: “yes”, “no”, and “do not know/cannot tell”. The papers were only considered for the review if they met at least three criteria. All assessment judgments were made by consensus, and any disagreements were immediately resolved by discussion among the writers. Based on this procedure, all authors agreed that the selected publications satisfied the bare minimum of quality in terms of technique and analysis. In total, 15 articles met all criteria, 3 articles met at least four criteria, and 4 articles met at least three criteria. (Table 3).

Table 3. Results of the quality assessment

| Previous Study | Design of research | QA1 | QA2 | QA3 | QA4 | QA5 | Score | Inclusion in the analysis |

| (Kamaruddin and Hanefah, 2023) | QT (DC) | / | / | / | / | / | 5/5 | / |

| (Ali et al., 2020) | QL | / | / | / | / | / | 5/5 | / |

| (Alam et al. 2023) | QL | / | / | / | / | / | 5/5 | / |

| (Haron and Khalid, 2018) | QL | / | / | / | / | / | 5/5 | / |

| (Khalid, 2019) | QL | / | / | / | / | / | 5/5 | / |

| (Khalid, 2020) | QL | / | / | / | / | / | 5/5 | / |

| (Kamaruddin et al., 2023) | QL | / | / | / | / | / | 5/5 | / |

| (Najeeb and Ibrahim, 2014) | QL | / | X | X | / | / | 3/5 | / |

| (Khalid et al., 2021) | QT (DC) | / | / | X | / | / | 4/5 | / |

| (Ahmad, 2017) | QT (DC) | / | / | X | / | / | 4/5 | / |

| (Tawfik and Bilal, 2020) | QT (DC) | / | / | X | X | / | 3/5 | / |

| (Khalid et al., 2017) | QT (DC) | / | / | / | / | / | 5/5 | / |

| (Yasoa et al., 2020) | QL | / | / | X | X | / | 3/5 | / |

| (Ali and Kasim, 2019) | QL | / | / | / | / | / | 5/5 | / |

| (Islam and Bhuiyan, 2021) | QT (DC) | / | / | / | / | / | 5/5 | / |

| (Algabry et al., 2021) | QL | / | / | / | / | / | 5/5 | / |

| (Ahmed and Sarea, 2019) | QT (DC) | / | / | / | / | / | 5/5 | / |

| (Othman and Ameer, 2015) | QL | / | / | / | / | / | 5/5 | / |

| (Shafii et al., 2013) | QL | / | / | / | / | / | 5/5 | / |

| (Ali et al., 2015) | QL | / | / | / | / | / | 5/5 | / |

| (Alam et al., 2017) | MM | / | / | X | X | / | 3/5 | / |

| (Ab Ghani et al., 2019) | MM | X | / | / | / | / | 4/5 | / |

QA=Quality assessment; QN (DC)=Quantitative descriptive; QN (NR)=Quantitative non-randomised; QL=Qualitative; MX=Mixed-Method; C=Do not know/Cannot tell

Extraction and analysis of data

Since the review depended on different study designs, the papers were thematically examined, presenting the best strategies to reconcile the discrepancies through qualitative synthesis (Whittemore and Knafl, 2005). While there are several qualitative syntheses that might be used, the current review is based on the method proposed by (Flemming et al., 2019). Thematic synthesis was stressed for synthesizing data from various study designs due to its versatility. Thematic analysis is a sort of analysis that seeks to discover and notify existing research patterns by recognizing any parallels or similarities in given data (Braun and Clarke, 2019). This study’s thematic synthesis was based on the methodology presented by (Kiger and Varpio, 2020). First, the researchers familiarize themselves with the entire dataset through active and frequent readings. This technique provided the researchers with valuable orientation to the raw data and created the framework for all following operations. The next step was to generate initialization codes. The data was organized at a granular and level by the researchers. During this stage, the researchers examined all the selected articles and extracted any data relevant to the main study issue. The final step was to come up with a topic. The researchers employed inductive coding frameworks to manually detect any overlaps, similarities, or linkages between the retrieved and coded data. The synthesis employed an inductive coding approach, with themes generated from coded data. The following step was to review the topics that had been established. The researchers examined the relevance of the main themes and sub-themes. Finally, there were three major themes and twelve sub-themes. The themes and sub-themes were then presented to two experts in qualitative synthesis and Islamic finance, who were asked to validate them. Both experts were also questioned about the applicability of the themes to the study issues. Following this procedure, all three themes and twelve sub-themes were retained.

FINDINGS

Overview of the chosen studies

10 of the 22 articles focused their research in Malaysia (Kamaruddin and Hanefah, 2023; Ali et al., 2020; Kamaruddin et al., 2023; Najeeb and Ibrahim, 2014; Yasoa et al., 2020; Ali and Kasim, 2019; Othman and Ameer, 2015; Shafii et al., 2013; Ali et al., 2015; Ab Ghani et al., 2019), five in Bahrain (Haron and Khalid, 2018; Khalid, 2020; Khalid et al., 2021; Khalid et al., 2017; Ahmed and Sarea, 2019), two in Bangladesh (Alam et al., 2023; Islam and Bhuiyan, 2021) and Pakistan (Ahmad, 2017; Alam et al., 2017). Likewise, each study was concentrated on Yemen (Algabry et al., 2021), Oman (Tawfik and Bilal, 2020) and worldwide (Khalid, 2019).

There was a total of 13 research that focused on qualitative analysis (Ali et al., 2020; Alam et al., 2023; Haron and Khalid, 2018; Khalid, 2019; Khalid, 2020; Kamaruddin et al., 2023; Najeeb and Ibrahim, 2014; Yasoa et al., 2020; Ali and Kasim, 2019; Algabry et al., 2021; Othman and Ameer, 2015; Shafii et al., 2013; Ali et al., 2015), seven on quantitative analysis (Kamaruddin and Hanefah, 2023; Khalid et al., 2021; Ahmad, 2017; Tawfik and Bilal, 2020; Khalid et al., 2017; Islam and Bhuiyan, 2021; Ahmed and Sarea, 2019). Whereas the remaining two research concentrated on mixed method (Alam et al., 2017; Ab Ghani et al., 2019).

In terms of year of publication, one paper was published in 2013 (Shafii et al., 2013), one in 2014 (Najeeb and Ibrahim, 2014), two in 2015 (Othman and Ameer, 2015; Ali et al., 2015), three in 2017 (Ahmad, 2017; Khalid et al., 2017), one in 2018 (Haron and Khalid, 2018), four in 2019 (Khalid, 2019; Ali and Kasim, 2019; Ahmed and Sarea, 2019; Ab Ghani et al., 2019), four in 2020 (Ali et al., 2020; Khalid, 2020; Tawfik and Bilal, 2020; Yasoa et al., 2020), three in 2021 (Khalid et al., 2021; Islam and Bhuiyan, 2021; Algabry et al., 2021), while remaining three is in 2023 (Kamaruddin and Hanefah, 2023; Alam et al., 2023; Kamaruddin et al., 2023).

The developed themes

Thematic analysis of 22 selected pieces identified three major themes: (1) competency; (2) institutions; and (3) code of ethics. These three topics have produced 12 sub-themes (see Table 4). The findings provided a respond to the SLR’s main research question, “How is the development of competency contributing to the effectiveness of the Shariah audit function globally?” The following part describes the context of the selected studies.

Table 4. Findings

| Authors/countries | Study design | Competency | Institution | Code of Ethic | |||||||||

| PRO | QUA | KNW | SKL | TRN | EXP | BNK | OFI | ZWI | GOV | RSK | IDP | ||

| (Kamaruddin and Hanefah, 2023) – Malaysia | QT | / | / | / | / | / | |||||||

| (Ali et al., 2020) – Malaysia | QL | / | / | / | / | / | / | ||||||

| (Alam et al., 2023) – Bangladesh | QL | / | / | ||||||||||

| (Haron and Khalid, 2018) – Bahrain | QL | / | / | ||||||||||

| (Khalid, 2019) – Worldwide | QL | / | / | / | |||||||||

| (Khalid, 2020) – Bahrain | QL | / | |||||||||||

| (Kamaruddin et al., 2023)- Malaysia | QL | / | / | ||||||||||

| (Najeeb and Ibrahim, 2014)- Malaysia | QL | / | / | ||||||||||

| (Khalid et al., 2021) – Bahrain | QT | / | |||||||||||

| (Ahmad, 2017) – Pakistan | QT | / | / | / | |||||||||

| (Tawfik and Bilal, 2020) – Oman | QT | / | / | / | / | / | |||||||

| (Khalid et al., 2017) -Bahrain | QT | / | / | ||||||||||

| (Yasoa et al., 2020) -Malaysia | QL | / | / | / | |||||||||

| (Ali and Kasim, 2019) – Malaysia | QL | / | / | / | |||||||||

| (Islam and Bhuiyan, 2021) -Bangladesh | QT | / | |||||||||||

| (Algabry et al., 2021) – Yemen | QL | / | / | / | / | ||||||||

| (Ahmed and Sarea, 2019) – Bahrain | QT | / | |||||||||||

| (Othman and Ameer, 2015) – Malaysia | QL | / | / | ||||||||||

| (Shafii et al., 2013) – Malaysia | QL | / | / | / | / | / | / | ||||||

| (Ali et al., 2015) – Malaysia | QL | / | / | / | / | ||||||||

| (Alam et al., 2017) -Pakistan | MM | / | / | / | / | / | / | ||||||

| (Ab Ghani et al., 2019) – Malaysia | MM | / | / | ||||||||||

Competency

The first sub-theme under competency was professional. Professional certification will be a significant component of internal Shariah audit’s main capability to affect effectiveness (Khalid et al., 2017). This is because regulators and management of Islamic Finance Institutions must fulfil their obligations to stakeholders (Othman and Ameer, 2015). Therefore, a need for skilful and professional manpower to ensure the operations of the Shariah audit efficiently and effectively (Ab Ghani et al., 2019). According to one prior suggestion, Malaysia could take the lead in developing an Association of Chartered Shari’ah Accountants and Auditors (ACSAA) as a professional credential that can result in long-term financial advantages for the country (Najeeb and Ibrahim, 2014). There are a few challenges with meeting the aim, particularly during the Covid-19 pandemic. According to Kamaruddin and Hanefah (2023), failure to do a greater amount of hands-on group and physical activities, various perspectives based on educational backgrounds, problems in learning hands-on and relevant topics, technical difficulties, and problems during e-learning sessions are some of the major challenges for conducting the professional shariah audit training program.

Qualification was the second sub-theme. Shariah audit performance in Islamic financial institutions will be influenced by qualification (Haron and Khalid, 2018). The current issue with shariah auditing is how present Islamic accounting and auditing qualification providers have failed to supply and create holistic Shariah accountants/auditors needed to function in an ideal Islamic economy (Najeeb and Ibrahim, 2014). As a result, the majority of Shariah auditors working in IFIs lack experience and qualifications in Shariah auditing and Islamic banking (Ab Ghani et al., 2019). The ineffectiveness of Shariah audit operations would be hampered by a lack of appropriately qualified Shariah auditors (Tawfik and Bilal, 2020). In Yemen, for example, they depend more on the qualifications and experience of the internal Shariah auditor than on statutory norms and regulations (Algabry et al., 2021). If Shariah auditors lack the essential qualifications, their experience in Islamic banking may be considered (Shafii et al., 2013). Finally, past research suggests that the qualification part of Shariah audit be improved by addressing the criteria required to hire qualified Shariah auditors in Islamic financial institutions (IFIs) (Haron and Khalid, 2018; Ali et al., 2020).

The third sub-theme was knowledge. Knowledge is one of the factors which contribute in developing competent shariah auditor. Shariah, Islamic banking, accounting, and Fiqh Muamalat knowledge are considered required for Shariah auditors (Ab Ghani et al., 2019; Ali and Kasim, 2019; Ali et al., 2020; Shafii et al., 2013). Furthermore, understanding the efficacy of internal Shariah audit structure among internal auditors will improve Shariah knowledge (Algabry et al. 2021). Some research examined the prospects of information gained through e-learning (Kamaruddin and Hanefah, 2023). These are the essential skills that a Shariah Auditor should possess to undertake an efficient Shariah audit. Personal traits such as the desire to learn and cooperate were discovered by (Ali et al., 2015) as complimenting characteristics to the knowledge and skill components, as a package required for a competent Shariah Auditor. According to studies, there is an urgent need to establish competency requirements that incorporate knowledge, abilities, and other qualities in order to assure an adequate supply of competent shariah auditors to satisfy the rising market demand (Ali et al., 2015) and to improve Shariah Auditors’ insufficient understanding (Khalid, 2020).

Skill was the fourth sub-theme under the competency theme. Most studies found that the main Shariah audit competency that influenced effectiveness was having skills (Ali and Kasim, 2019; Khalid et al., 2017; Tawfik and Bilal, 2020). Previous research in Pakistan, however, has not identified the precise knowledge, skills, and other attributes required for shariah auditors (Ab Ghani et al., 2019). Furthermore, auditing is recognized to be the essential competence Shariah Auditor should have in order to do Shariah audit efficiently (Ali et al., 2020). While the demand for skilled labour is well established in Malaysia, the fundamental difficulty is a misalignment in the talent pool between what the institution requires and what the labour market has offer (Ali et al. 2015).

The fifth sub-theme was training. There is a lot of efforts in conducted training for the development of competent shariah auditor (Shafii et al. 2013; Ahmad, 2017; Kamaruddin and Hanefah, 2023). Due to COVID-19, Malaysia is using e-learning to deliver professional shariah audit training (Kamaruddin and Hanefah, 2023). Normal practices kind of training through conducting trainings sessions, seminars, and workshops in the banking sector for promotion and awareness of shariah audit (Ahmad, 2017). The majority of Shariah auditors are either shariah or auditing discipline trained (Ali et al., 2015). Previous study in Oman suggests that Shariah auditing necessitates highly trained and competent personnel (Tawfik and Bilal, 2020). The main issues regarding on the training for shariah Audit in banking industry is incompatibility in the skill pool between what banks require and what the market offers (Ali et al., 2015). Developing curriculum and training modules for Shariah audit is critical to meeting Shariah and the industry needs (Shafii et al., 2013).

The last sub-theme under this theme was experience. Many previous research on Shariah auditors agreed on the necessity for years of experience as one of the factors required to become competent (Shafii et al., 2013; Haron and Khalid, 2018; Khalid, 2019; Ali and Kasim, 2019; Ali et al., 2020). According to one study, if Shariah auditors lack the essential qualifications, experience in Islamic banking could be acceptable (Shafii et al., 2013). Unfortunately, previous study raised few challenges on shariah audit effectiveness. According to (Alam et al., 2017), the majority of Shariah auditors working in IFIs lack experience and qualifications in Shariah auditing and Islamic banking. The other challenge is relying on the qualifications and experience of the internal Shariah auditor rather than official rules and standards (Algabry et al., 2021). Lastly, element of time will be significant to the effectiveness of job performance (Ali et al., 2020).

Institutions

There is a lot of studies about shariah audit competency and effectiveness in banking sector which was name as the first sub-theme. Most banks prefer to use their currently employed internal auditors rather than hire new graduates or experienced Shariah auditors from other financial institutions (Ali et al., 2020). This is mainly due to the function and responsibilities of auditors in Islamic banks are much bigger compared to those in conventional banks (Othman and Ameer, 2015). There are a few issues related to Shariah audit in the banking sector, such as a lack of commitment from Islamic banks in Oman (Tawfik and Bilal, 2020), an imbalance of skilled workers between what is required by the banks and what is offered by the market in Malaysia (Ali et al., 2015), and an inability to effectively understand the Shariah audit set of regulations that has been established in Pakistan’s Islamic banking industry (Ab Ghani et al., 2019). In addition, relied on the credentials and experience of the internal Shariah auditor, more than official norms and regulations in the Yemeni (Algabry et al., 2021). Some past study suggesting a different solution (Alam et al., 2023) suggested that existing mechanisms be improved to benefit Islamic banks in Bangladesh. Another study proposes more structured and explicit criteria for Shariah auditors’ roles and responsibilities in Malaysian Islamic banks (Yasoa et al., 2020) suggest an Islamic world view for Islamic banks’ AGC (Khalid, 2020), and (Khalid et al., 2021) discuss the level of development for an effective internal Shariah audit framework in Islamic banks using Islamic agency theory as their framework. In Pakistan, government-owned banks play an important role in encouraging and bolstering shariah auditing (Ahmad, 2017).

The second sub-theme was other financial institutions. Only three study related to other financial institution (Islam and Bhuiyan, 2021; Ali et al., 2020; Shafii et al., 2013). Overall, the previous study emphasized the significance of increasing the performance of Shariah-based internal auditing systems in Islamic financial organizations (Islam and Bhuiyan, 2021; Shafii et al., 2013). Finally, the final sub-theme is zakat and waqf institutions. (Kamaruddin et al., 2023) is one of the earliest papers that examine Shariah audit operations in Malaysian zakat and waqf institutions.

Code of Ethics

The first sub-theme under the theme code of ethics was governance. Shariah governance is a crucial component of determining the effectiveness of an internal Shariah audit function (Ab Ghani et al., 2019). One study in Malaysia emphasizes existing Shariah governance practices, particularly in terms of Shariah oversight duties, Shariah audit implementation in terms of Shariah audit scopes and frequent findings, Shariah audit competency, Shariah audit effectiveness, particularly the requirement for an external Shariah audit function, and Shariah audit problems and obstacles encountered in the implementation of Shariah audit practices (Kamaruddin et al., 2023). A previous study suggests that the Shariah auditor competencies framework can be used to better their Shariah governance system (Alam et al., 2023). Other things include Shariah governance module (Kamaruddin and Hanefah 2023) and guideline (Algabry et al., 2021; Yasoa et al., 2020). Otherwise, previous studies in Oman identified a shortage of suitably competent Shariah auditors and a lack of commitment from Islamic banks as the primary hurdles in improving the Shariah governance system (Tawfik and Bilal, 2020). Finally, another study reveals that increasing awareness of the strengthening internal Sharah audit structure can help to improve the process of improving internal Sharah governance elements (Algabry et al., 2021).

The risk sub-theme was the second. In the previous study, there is a proposal for an improvement of shariah audit implementation regarding on risk. In Malaysia, past study recommend Shariah risk management module (Kamaruddin and Hanefah, 2023) and the Shariah Governance Framework approaches has shifted from compliance to risk-based auditing (Yasoa et al., 2020).

The last sub-theme was independent. Being independent in a vital part in auditing. Previous study clearly stated that Shariah Auditor must be independent for their decisions and policy making process (Ahmad, 2017). According to the notion, internal Shariah audit efficacy might be improved by increasing their independence (Ab Ghani et al., 2019; Ahmed and Sarea, 2019; Haron and Khalid, 2018; Khalid, 2019). According to Shafii et al. (2013), the Shariah audit role will now be attached to the internal audit department to ensure their independence (Shafii et al. 2013).

DISCUSSION

All parts of the competence theme, such as professionalism, skills, qualification, training, knowledge, and experience, contribute to the efficiency of Shariah auditing in an organization (Khalid et al., 2017; Ali and Kasim, 2019; Ab Ghani et al., 2019; Ali et al., 2020; Tawfik and Bilal, 2020). The enhancement of Shariah auditor competence can be facilitated through access to a comprehensive training model encompassing expertise in both auditing and Shariah disciplines (Ali et al., 2015). Broadly, significant advancements have been identified across all facets of competence aimed at augmenting the Shariah auditor’s proficiency and capabilities. Furthermore, in developing the Shariah auditor competency framework, policymakers must take into account all key concepts acquired during the process.

Addressing the challenges and issues highlighted in prior research is imperative to bolstering Shariah auditor competency. Principal obstacles encompass a disparity between the expertise offered in the market and the requisite talent for Islamic banking, inadequately experienced Shariah auditors, and technical complexities in implementing training modules. These challenges stem from practitioners predominantly adhering to conventional norms and a shortage of auditors possessing both Shariah and accounting/auditing qualifications (Kasim et al., 2013; Kasim and Sanusi, 2013). Enhanced Shariah auditor competency also facilitates the development of proficient Shariah audit functions within organizations.

Moreover, there exists an imbalance in the development of expertise within the realm of Shariah auditing. While numerous studies have endeavoured to enhance Shariah audit competency in the Islamic banking and Islamic financial institution (IFI) sectors, limited research has been conducted on competency development, concerns, and issues within zakat and waqf institutions. These institutions, overseen by State Islamic Religious Councils (SIRC), play a pivotal role in the Islamic economy, with estimates suggesting that global zakat contributions range between $200 billion and $1 trillion annually (Stirk, 2015). Given the significant fiscal role of State Islamic Religious Councils (SIRC) as guardians of Islamic finances for Muslim communities, it is crucial to establish Shariah audit functions under their purview to uphold regulatory compliance.

However, establishing Shariah audit programs in zakat and waqf organizations presents significant challenges. Operational differences in Shariah procedural practices and resolutions compared to the Islamic banking sector, coupled with unclear Shariah governance structures, hinder the implementation process. As a result of the above, the role of shariah audits in the zakat and waqf sectors remains ineffective. A report by Shafii et al., (2023) advocates for the establishment of a structured framework for the implementation of Shariah audit. Striking a balance in implementing comprehensive competency development programs is crucial to furnishing Shariah auditors with the requisite skills and expertise in Shariah matters, not only within Islamic banking and finance but also across other sectors such as zakat and waqf institutions.

The second factor influencing the effectiveness of Shariah audit lies in adherence to ethical principles outlined in audit codes. Professional auditors must adhere to established ethical standards during audit procedures, which includes maintaining principles of governance and independence to ensure a cohesive and efficient audit process. Current trends in auditing also emphasize risk-based audit approaches, necessitating consideration of effective risk management elements to enhance the efficacy of Shariah audits. Concerns about inadequate implementation of risk-based Shariah internal audits within SIRC organizations have been highlighted in the White Paper on Shariah Audit by Shafii et al., (2023). Furthermore, fulfilling the principles outlined in the auditor’s code of ethics can be achieved through the development of Shariah auditor competency. By integrating the principle of competence with the values and ethics upheld by Shariah auditors, the role and function of the Shariah audit department can be strengthened more effectively.

Move forward, it is imperative to develop a Shariah auditor competency framework tailored specifically for the SIRCs industry. Additionally, establishing a Shariah committee tasked with formulating Shariah resolutions for zakat and waqf operations is essential. Given that The Islamic Legal Consultative Commissions is already burdened with numerous responsibilities and primarily focuses on policy iqh matters, the establishment of a separate Shariah committee dedicated to zakat and waqf operations is necessary. This will ensure a more focused and effective approach to addressing the intricate legal issues surrounding these charitable mechanisms. Furthermore, collaboration between SIRCs and researchers is crucial for the development of certified professional Shariah audit courses, with a particular emphasis on Baitulmal operations. By pooling expertise and resources, SIRCs can work alongside researchers to design comprehensive training programs that equip auditors with the necessary skills and knowledge to effectively conduct Shariah audits within Baitulmal institutions. This collaborative effort will not only enhance the competency of Shariah auditors but also contribute to the overall improvement of governance and transparency in Baitulmal operations.

Implications, research gaps and future study recommendations

Standard 1200, The International Professional Practices Framework (IPPF), Institute of Internal Auditors emphasizes the significance of an internal audit team that possesses the knowledge, skills, and other competences required to perform their obligations effectively (IPPF,). Therefore, exploring the enhancement of Shariah auditor competency is vital to maintaining the efficacy of Shariah auditing. However, challenges in implementation planning may emerge due to substantial costs and budgets, as well as time constraints and obligations from various stakeholders. This scenario presents an opening for governmental bodies, the private sector, and other stakeholders to address issues such as the shortage of proficient and experienced Shariah auditors, ambiguity in Shariah frameworks, and the reinforcement of Shariah auditing in SIRCs moving forward.

As a result of the Systematic Literature Review (SLR), several gaps in research have come to light. Firstly, since 2013, there has been significant attention given to the topic of Shariah audit competency, notably highlighted in the White Paper on Shariah Audit. Secondly, limited research exists regarding Shariah audit competency within zakat and waqf organizations (Kamaruddin et al., 2024). Lastly, there is a lack of investigation into factors beyond skills that contribute to the effectiveness of Shariah auditing roles within organizations.

To address this research gap, a proposed Shariah audit competency framework could be implemented to ensure ongoing growth in the pool of talent within the Shariah auditing field. A comprehensive mixed-methods study could be undertaken to explore Shariah audit practices within zakat and waqf departments, followed by an examination of drivers influencing the effectiveness of Shariah audit functions in the industry. Subsequently, qualitative research could be conducted to identify additional characteristics, beyond competency, that impact the success of Shariah auditing.

CONCLUSION

The fundamental issues in the practice of Shariah auditing revolve around a serious shortage of skilled and experienced Shariah auditors. This scarcity of talent severely impedes the efficient implementation of Shariah-compliant activities. Furthermore, the scarcity of comprehensive research and exposure to Shariah auditing in the context of zakat and waqf institutions exacerbates the problem, impeding the establishment of solid and specialized auditing procedures for this specific sector.

The present study conducted an extensive examination of previous research investigating the impact of competency on the effectiveness of Shariah audits. Through this process, the rigor of certain studies was called into question, allowing for the identification of gaps and avenues for future research. Utilizing a Systematic Literature Review (SLR) approach, 22 publications were meticulously assessed for quality. Additionally, thematic analysis was employed to categorize these publications into three main themes: competency, institutional factors, and the code of ethics. The findings of this review offer several recommendations for future research endeavours. Firstly, it is imperative to incorporate a comprehensive range of key competency concepts, such as professionalism, skills, qualifications, training, knowledge, and experience, to ensure robust data collection for the development of a competency framework. This holistic approach is essential for addressing existing challenges and improving the effectiveness of Shariah audits.

Lastly, there is a compelling necessity for further research into Shariah audit practices within the zakat and waqf industry (SIRCs). This arises from the significant divergence in Shariah knowledge and interpretations that impact their operations. A more comprehensive understanding of these variations and their implications is crucial for the development of robust Shariah-compliant frameworks and practices within this sector. SIRCs could establish partnerships with academic institutions, forming joint research ventures aimed at identifying gaps in Shariah audit competency and developing tailored training curricula. This collaborative approach would ensure that training programs are aligned with industry standards and informed by the latest research findings, thus maximizing their effectiveness in enhancing Shariah audit competency within Baitulmal institutions.

ACKNOWLEDGEMENT

This research is supported by the Faculty of Economics and Management Research Innovation Grant, Universiti Kebangsaan Malaysia. [Grant No: EP-2023-076].

REFERENCES

- Ab Ghani, N. L., Ariffin, N. M., & Rahman, A. R. A. (2019). The measurement of effective internal shariah audit function in Islamic financial institutions. International Journal of Economics, Management and Accounting, 27(1), 141-165. https://doi.org/10.31436/ijema.v27i1.600

- Ahmad, S. (2017). Practice of Shariah audit in Islamic banking in Pakistan. Journal of Islamic Economics, Banking and Finance, 13(2), 102-127.

- Ahmed, A. A. K., & Sarea, A. M. (2019). Factors influencing internal shariah audit effectiveness: evidence from Bahrain. International Journal of Financial Research, 10(6), 196-210. https://doi.org/10.5430/ijfr.v10n6p196

- Alam, M. K., Tabash, M. I., Thakur, O. A., Rahman, M. M., Siddiquii, M. N., & Hasan, S. (2023). Independence and effectiveness of Shariah department officers to ensure Shariah compliance: evidence from Islamic banks in Bangladesh. Asian Journal of Accounting Research, 8(1), 15-26. https://doi.org/10.1108/AJAR-01-2022-0022

- Alam, T., Hassan, T., & Ferdous, K. (2017). Competency of Shariah auditors: Issues and challenges in Pakistan. Journal of Internet Banking and Commerce, 22(2).

- Algabry, L., Alhabshi, S. M., Soualhi, Y., & Othman, A. H. A. (2021). Assessing the effectiveness of internal Sharīʿah audit structure and its practices in Islamic financial institutions: a case study of Islamic banks in Yemen. Asian Journal of Accounting Research, 6(1), 2-22. https://doi.org/10.1108/AJAR-04-2019-0025

- Ali, N. A. M., & Kasim, N. (2019). Talent management for Shariah auditors: Case study evidence from the practitioners. International Journal of Financial Research, 10(3), 252-266. https://doi.org/10.5430/ijfr.v10n3p252

- Ali, N. A. M., Mohamed, Z. M., Shahimi, S., & Shafii, Z. (2015). Competency of Shariah auditors in Malaysia: issues and challenges. Journal of Islamic Finance, 4(1), 22-30. https://doi.org/10.31436/jif.v4i1.67

- Ali, N. A. M, Shafii, Z., & Shahimi, S. (2020). Competency model for Shari’ah auditors in Islamic banks. Journal of Islamic Accounting and Business Research, 11(2), 377-399. http://dx.doi.org/10.1108/JIABR-09-2016-0106

- Braun, V., & Clarke, V. (2019). Reflecting on reflexive thematic analysis. Qualitative research in sport, exercise and health, 11(4), 589-597. https://doi.org/10.1080/2159676X.2019.1628806

- Flemming, K., Booth, A., Garside, R., Tunçalp, Ö., & Noyes, J. (2019). Qualitative evidence synthesis for complex interventions and guideline development: clarification of the purpose, designs and relevant methods. BMJ global health, 4(Suppl 1), e000882. https://doi.org/10.1136/bmjgh-2018-000882

- Gusenbauer, M., & Haddaway, N. R. (2020). Which academic search systems are suitable for systematic reviews or meta‐analyses? Evaluating retrieval qualities of Google Scholar, PubMed, and 26 other resources. Research synthesis methods, 11(2), 181-217. https://doi.org/10.1002/jrsm.1378

- Haron, H. B. H., & Khalid, A. A. (2018). The role of shariah supervisory board on internal Shariah audit effectiveness: Evidence from Bahrain. Academy of Accounting and Financial Studies Journal, 22(5), 1-15.

- Higgins, J. P., Altman, D. G., Gøtzsche, P. C., Jüni, P., Moher, D., Oxman, A. D., … & Sterne, J. A. (2011). The Cochrane Collaboration’s tool for assessing risk of bias in randomised trials. Bmj, 343. https://doi.org/10.1136/bmj.d5928

- Hong, Q. N., Gonzalez‐Reyes, A., & Pluye, P. (2018). Improving the usefulness of a tool for appraising the quality of qualitative, quantitative and mixed methods studies, the Mixed Methods Appraisal Tool (MMAT). Journal of evaluation in clinical practice, 24(3), 459-467. https://doi.org/10.1111/jep.12884

- Islam, K. M., & Bhuiyan, A. B. (2021). Determinants of the effectiveness of internal Shariah audit: Evidence from Islamic banks in Bangladesh. The Journal of Asian Finance, Economics and Business, 8(2), 223-230. https://doi.org/10.13106/jafeb.2021.vol8.no2.0223

- Kamaruddin, M. I. H., & Hanefah, M. M. (2023). Professional shariah audit training via the e-learning approach during COVID-19: challenges and prospects. Asian journal of accounting research, 8(3), 250-268. https://doi.org/10.1108/AJAR-12-2021-0284

- Kamaruddin, M. I. H., Shafii, Z., Hanefah, M. M., Salleh, S., & Zakaria, N. (2024). Exploring Shariah audit practices in zakat and waqf institutions in Malaysia. Journal of Islamic Accounting and Business Research, 15(3), 402-421. https://doi.org/10.1108/JIABR-07-2022-0190

- Kasim, N., & Sanusi, Z. M. (2013). Emerging issues for auditing in Islamic Financial Institutions: Empirical evidence from Malaysia. IOSR Journal of Business and Management, 8(5), 10-17. http://dx.doi.org/9790/487X-0851017

- Kasim, N., Sanusi, Z. M., Mutamimah, T., & Handoyo, S. (2013). Assessing the current practice of Auditing in Islamic Financial Institutions in Malaysia and Indonesia. International Journal of Trade, Economics and Finance, 4(6), 414. http://dx.doi.org/10.7763/IJTEF.2013.V4.328

- Khalid, A. A. (2019). The impact of audit and governance committee on internal Shariah audit performance: An Islamic-worldview based. International Journal of Recent Technology and Engineering, 8(2), 426-431.

- Khalid, A. A. (2020). Role of audit and governance committee for internal Shariah audit effectiveness in Islamic banks. Asian Journal of Accounting Research, 5(1), 81-89. https://doi.org/10.1108/AJAR-10-2019-0075

- Khalid, A. A., Haron, H. H., & Masron, T. A. (2017). Relationship between internal Shariah audit characteristics and its effectiveness. Humanomics, 33(2), 221-238. https://doi.org/1108/H-11-2016-0084

- Khalid, A. A., Hussin, M. Y. M., Sarea, A., & Shaarani, A. Z. B. M. (2021). Development of effective Internal Shariah audit framework using Islamic agency theory. Asian Economic and Financial Review, 11(8), 682. https://doi.org/10.18488/journal.aefr.2021.118.682.692

- Kiger, M. E., & Varpio, L. (2020). Thematic analysis of qualitative data: AMEE Guide No. 131. Medical teacher, 42(8), 846-854. https://doi.org/10.1080/0142159X.2020.1755030

- Kraus, S., Breier, M., & Dasí-Rodríguez, S. (2020). The art of crafting a systematic literature review in entrepreneurship research. International Entrepreneurship and Management Journal, 16, 1023-1042. https://doi.org/10.1007/s11365-020-00635-4

- Lockwood, C., Munn, Z., & Porritt, K. (2015). Qualitative research synthesis: methodological guidance for systematic reviewers utilizing meta-aggregation. JBI Evidence Implementation, 13(3), 179-187. https://doi.org/10.1097/XEB.0000000000000062

- Mahzan, N., & Yahya, Y. (2014). Syariah audit practices in Malaysian Islamic financial institutions (IFIs). In National Symposium and Exhibition on Business and Accounting 2014(pp. 1-9).

- Najeeb, S. F., & Ibrahim, S. H. M. (2014). Professionalizing the role of Shari’ah auditors: How Malaysia can generate economic benefits. Pacific-Basin Finance Journal, 28, 91-109. https://doi.org/10.1016/j.pacfin.2013.10.009

- Othman, R., & Ameer, R. (2015). Conceptualizing the duties and roles of auditors in Islamic financial institutions: what makes them different?. Humanomics, 31(2), 201-213. https://doi.org/10.1108/H-04-2013-0027

- Shaffril, H. A. M., Krauss, S. E., & Samsuddin, S. F. (2018). A systematic review on Asian’s farmers’ adaptation practices towards climate change. Science of the total Environment, 644, 683-695. https://doi.org/10.1016/j.scitotenv.2018.06.349

- Shafii, Z., Hanefah, M. M., Zakaria, N., Salleh, S., Muhammad Iqmal Hisham Kamaruddin, M. I. H. (2023). White Paper on Shariah Audit. Malaysian Institute of Accountants (Malaysian Institute of Accountants). https://mia.org.my/wp-content/uploads/2023/07/White-Paper-on-Shariah-Audit.pdf

- Shafii, Z., Salleh, S., Hanefah, H. M. M., & Jusoff, K. (2013). Human capital development in Shariah audit. Middle East journal of scientific research. https://doi.org/10.5829/idosi.mejsr.2013.13.1878

- Stirk, C. (2015). An Act of Faith: Humanitarian Financing and Zakat, Global Humanitarian Assistance. Belgium. Retrieved from https://policycommons.net/artifacts/1847628/an-act-of-faith/2593833/on 12 May 2024. CID: 20.500.12592/813z8w.

- Tawfik, O. I., & Bilal, Z. O. (2020). The impact of sharīʿah auditing requirements on the service quality of Islamic banks in the sultanate of Oman. Journal of King Abdulaziz University, Islamic Economics, 33(1), 101-116. https://doi.org/10.4197/Islec. 33-1.8

- Whittemore, R., & Knafl, K. (2005). The integrative review: updated methodology. Journal of advanced nursing, 52(5), 546-553. https://doi.org/10.1111/j.1365-2648.2005.03621.x

- Yasoa, M. R., Abdullah, W. A. W., & Endut, W. A. (2020). The role of shariah auditor in islamic banks: The effect of shariah governance framework (SGF) 2011. International Journal of Financial Research. https://doi.org/10.5430/ijfr.v11n4p443