Promoting Homeownership among the Underprivileged: The Role of Social Financing

- Mahazril ‘Aini Yaacob

- Farihah Hassan

- Norraidah Abu Hasan

- Saidatul Akma Hamik

- Herman Shah Shahbuddin

- 2635-2652

- Apr 22, 2024

- Accounting & Finance

Promoting Home Ownership among the Underprivileged: The Role of Social Financing

Mahazril ‘Aini Yaacob1, Farihah Hassan1, Norraidah Abu Hasan3, Saidatul Akma Hamik1, Herman Shah Shahbuddin2

1Faculty of Administrative Science and Policy Studies, Malaysia

2Bank Islam Malaysia Berhad, Malaysia

3Faculty of Administrative Science and Policy Studies, Malaysia

DOI: https://dx.doi.org/10.47772/IJRISS.2024.803183

Received: 07 March 2024; Accepted: 15 March 2024; Published: 22 April 2024

ABSTRACT

Many people struggle to obtain home ownership due to unaffordable housing and limited financing. As a result, they opted for renting, which also became a challenge due to the unstable rental sector. Therefore, this paper presents a qualitative analysis of the housing challenges and the roles of social financing in promoting home ownership among the underprivileged in Malaysia. A focus group discussion with ten participants was conducted from low-income groups living in the public housing project (PPR) Kampung Kerinchi, Kuala Lumpur, Malaysia, to validate their housing challenges in their pursuit of home ownership. The findings revealed that housing affordability is the main reason people cannot own it, which has become one of the challenges they face. The study also highlights the challenges related to financing accessibility for affordable homes. The introduction of social finance in managing unaffordability issues among people is seen as a practical tool for people towards home ownership and financial institutions as part of their social responsibility.

Keywords: home ownership, social financing, underprivileged, housing challenges, Malaysia

I. INTRODUCTION

Malaysia is currently facing a pressing concern regarding home ownership. A growing population, urbanisation, and rising property prices have led to a critical shortage of accessible and reasonably priced housing units (Khazanah Research Institute,2019; 2015). This crisis poses a significant threat to many people, especially those with lower incomes. Over the past decade, the Malaysian government has undergone substantial changes in formulating national development plans, emphasising the importance of urban and regional planning as a catalyst for sustainable and inclusive growth. The Twelfth Malaysia Plan (12MP), which covers the years 2021 to 2025, is centred on improving the socioeconomic well-being of the population through investments in infrastructure, facilities, and public services. It also aligns with Sustainable Development Goal No. 11, which allows everyone to access appropriate, safe, affordable housing and essential services by 2030 and upgrade slums (The Sustainable Development Goals Report, 2021).

Despite the various housing schemes such as Home ownership schemes, Rent-to-own, 1 Malaysia Housing Program and many more, many Malaysians still need assistance accessing adequate and decent housing, as housing costs are out of reach for most low-income people (Rangel et al., 2023; Soon et al., 2019).

As a result of increasing housing prices and the inaccessibility of housing financing, affordable housing is now beyond the reach of many Malaysians. Young people found it difficult to obtain mortgage financing. They had unstable incomes, which made home ownership unattainable for them, according to a study by Yaacob and Hassan (2024) and Bailey (2020). Similarly, another study found that most people who could not access housing had housing affordability problems associated with low income, difficulty paying for the housing deposit, and securing financing (Zamri et al., 2021; Abidoye et al., 2020; Soon & Tan, 2019).

Amidst Malaysia’s continuing struggle with housing affordability problems, the importance of social financing for promoting home ownership has become more crucial. Social financing initiatives enhance the fairness and sustainability of the country’s housing sector by promoting inclusivity, community participation, and creative financial solutions. As these models grow, they can transform the issues of home ownership, allowing it to develop into an accessible choice for a bigger segment of the population. Nevertheless, few studies (Subagyo et al., 2022; Ebekozien et al., 2019, 2022; Acri et al., 2021; Dirie et al., 2023) have looked at the role of social financing in promoting home ownership among the underprivileged, especially in Malaysia. Therefore, this study was developed to achieve the following objectives:

- To discuss the challenges faced by people, especially the underprivileged, in their pursuit of home ownership.

- To explore the role of social financing as a tool for promoting home ownership among the underprivileged.

II. LITERATURE REVIEW

II.A.1. Housing issue

The importance of providing affordable and accessible housing to the citizens of any country cannot be over emphasised. It is a basic need and a fundamental human right recognised by international organisations and human rights advocates. For instance, the Universal Declaration of Human Rights recognises the right to housing as part of the right to an adequate standard of living (United Nations Habitat, 2014). Hence, housing should be seen as a right with tenure security rather than a commodity.

Governments worldwide, both developed and developing, have implemented various programmes and projects to alleviate housing finance inaccessibility, particularly for low-income earners (LIEs), including Malaysia. Over the years, the Malaysian government has implemented several programmes (State government Housing Programme, Public Housing Programme, Low-cost Housing Programme) to make housing affordable and accessible to its citizens. Adequate housing is crucial for a healthier quality of life, especially for low-income earners, and it also serves as a social safety net.

Despite the government’s efforts, these programmes have problems and challenges. One of the significant problems is the issue of housing finance for low-income earners and house buyers. The challenge of Malaysian LIEs accessing housing loans has persisted since the mid-1990s. Accessing housing loans through a mortgage is a challenge for most LIEs. That has resulted in a high rate of rejection of LIE house buyers, as noted by researchers such as Saha et al. (2022); Ebekozien et al. (2019), Ebekozien et al. (2022); Hoek-Smit (2008); and Bakhtyar Zaharium, Sopian, and Moghimi (2013).

The rejection rate of LIE house buyers is alarming, given the various low-cost housing (LCH) programmes implemented by both federal and state governments. The desire to own a home seems deeply embedded in the minds of all Malaysians, regardless of their income groups, possibly due to Malaysia’s aspiration to become a home-owning society. However, home ownership can be challenging for most people, especially the underprivileged. They expressed concern about the housing available in the market, which is beyond their affordability.

The significant challenges people face, especially those low-income people owning houses in Malaysia, include slower income growth, financial illiteracy, and the high price of current houses. In a study in Malaysia, Ravi and Redzuan (2022) found that the B40 group faces difficulties obtaining credit from banks due to a lack of credit history and collateral, making it more challenging to buy a house and obtain financial assistance from financial institutions. This has led to accumulating house rental arrears, potentially causing them to be evicted from rented houses.

In their study, Ebekozien et al. (2019) argue that one significant contributor to the high cost of public housing is the expense associated with home finance. Within Malaysian public housing programmes, households with low and middle incomes must obtain home financing from financial institutions with a defined repayment duration. This increases housing expenses, as the buyer must repay the initial sum and the accrued interest. Households also face difficulties in acquiring home financing from financial institutions, both conventional and Islamic. Hence, the primary obstacle to offering affordable housing to low and middle-income households is limited accessibility due to their lack of financing.

The issue of housing affordability is not limited to Malaysia alone. People in other developing countries also face the difficulties of owning a home. In Nigeria, the obstacles that restrict their capacity to own include a lack of income and savings to make mortgage payments and provide housing deposits, insufficient funds for loans, and inadequate mortgage lending institutions (Nwuba & Chukwuma-Nwuba, 2018). In Central Europe, housing affordability has worsened for many people. It has resulted in urban slums, now a defining feature of the urban landscape. It affirms that the high rejection rate of LIE house buyers continues to contribute to this problem (Friesen et al., 2018). A similar situation also happens in Indonesia, where Indonesians find it difficult to access finance, especially for low-income people (Subagyo et al., 2022). This is because market fundamentals, including demand, income, land cost, and market sentiment, significantly influence housing prices in big cities, as Li and Zhi (2023) suggested in their findings.

Therefore, it is essential to address the issue of housing affordability and accessibility for people, especially low-income earners, to ensure a decent quality of life. Not only that, but evidence indicates that lockdown measures during COVID-19 led to many people’s income fluctuations, as discussed in Alharbi (2021). Evidence from this study indicates that due to the economic upheaval, many homeowners could not fulfil their monthly mortgage payment responsibilities. The situation has resulted in a shift in the income level, dropping the middle-income group to the lower-income group.

The high rate of rejection of house buyers, as highlighted in this paper, is a cause for concern that requires social financing as another alternative to the issue. More empirical evidence is needed to understand the challenges faced by the underprivileged and identify practical solutions, which become the study’s aims.

II.A.2. Housing Affordability and Policy Initiatives: Malaysia Perspectives

Malaysia has continuously debated and discussed the perceived rise in the cost of living despite the country’s current low and steady inflation phase. Cost of living is often a comprehensive phrase encompassing broader effects on household finances and personal welfare, extending beyond mere price escalations. The scarcity of affordable housing is particularly acute for households with a monthly income ranging from RM3,000 to RM5,000 (World Bank, 2020). Malaysia faces challenges in providing affordable and adequate housing for its growing population. Three significant issues affect housing affordability in Malaysia: a mismatch between housing supply and demand, biased new constructions that fall into unaffordable categories, and house price increases that are outpacing the growth of household incomes (Ling, 2017).

Housing affordability challenges in Malaysia stem from rapid urbanisation, limited land availability, property speculation, and government policies affecting land use and development (Ling, 2017). There are also questions about what is considered affordable housing in Malaysia. The National Affordable Housing Policy adopted a median multiple approach in 2022, with a monthly median household income of RM 6,338 and a median house price of RM 330,000, to provide a clear picture of house affordability in Malaysia. To afford a house priced up to RM 3300,000, a household must earn at least RM8,300 annually (Bank Negara Malaysia, 2020).

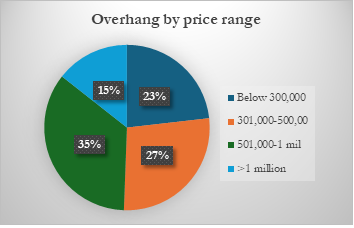

Approximately 73% of the unsold homes in Malaysia were priced above RM 250,000 (National Property Information Centre, 2023), as depicted in Fig. 1. To overcome these obstacles, immediate cost-of-living adjustments and longer-term structural changes that promote market competition and raise earnings are needed.

Fig 1 Total of residential overhang in Q1, 2023

Source: National Property Information Centre (2023)

The National Housing Policy (2018–2025) was enacted in 2018 to provide adequate and affordable housing for the needy. The National Affordable Housing Policy (NAHP) was issued in 2019 as a sub-policy to address affordable housing problems for low- and middle-income households. Both policies outline guidelines for all parties involved in affordable housing delivery, such as determining a price range for each state and establishing housing standards to be fulfilled by developers to reduce housing prices for low-income households (Liu & Ong, 2021). They also described the government’s initiatives in reducing affordable housing costs in terms of land price, development charge, compliance cost, developing an integrated housing system, and setting up a platform of education and advice on financial matters.

The NAHP created a unified policy framework for developers to build affordable and cost-saving housing for the target groups of low- and middle-income households. Several financing initiatives, such as the Rent-to-Own financing scheme, were also provided to improve the housing affordability of low- and middle-income households. In 2019, the Home Ownership Campaign was launched to promote Malaysian homeownership and overcome unsold properties. By the mid-term of the Eleventh Malaysia Plan (2016–2020), 139,329 units and 30.9% of the target had been completed for low- and middle-income households, while the homeownership of low- and middle-income households was increased through various affordable housing programmes (Economic Planning Unit, 2018). However, some still cannot access affordable housing, primarily in urban areas.

This is because attaining housing loans in Malaysia is becoming increasingly challenging, concurrent with an extended loan approval process. Due to the high monthly payments and interest rates associated with bank-issued mortgage loans, housing units have become prohibitively expensive for households (Zyed et al., 2020; Abidoye et al., 2020; Ebekozien et al., 2019). Monthly maintenance fees and monthly instalment payments impose additional financial strain, mainly on low-income households, thus limiting their housing opportunities.

II.A.3. Housing Affordability and Purchasing Power Parity

Housing affordability is closely connected to housing disparity, significantly sustaining socioeconomic inequality (Aizawa et al., 2020). With the projected growth of urban populations in Asia and the ongoing worry about housing affordability, authorities should adopt a comprehensive strategy to address this issue. Housing affordability and purchasing power parity are related to living expenses and regional or national economies.

Housing affordability refers to the relationship between household income and the cost of housing, with housing costs typically measured as a proportion of household income (Khazanah Research Institute, 2019; Soon & Tan, 2019). Household income, housing costs, mortgage rates, and the cost of living are some variables that affect it. The percentage of income allocated to housing expenses, the availability of affordable housing concerning demand, and the ratio of median home price to median household income are some measures used to evaluate housing affordability.

Purchasing Power Parity (PPP) is an economic theory that posits that currency exchange rates ought to be adjusted to achieve parity in the purchasing power of various currencies. In another context, it implies that equivalent items should cost the same, whether expressed in different countries using the same currency, if there are no obstacles such as taxes or transportation expenses. By accounting for the relative cost of living and inflation rates, this notion is frequently used to compare the living standards between nations (Audi & Ali, 2023).

The notion of PPP is crucial to home affordability because it sheds light on the relative purchasing power of people in different countries. PPP indicates that after considering exchange rates, the prices of goods and services, including housing, should be comparable across two countries (Helble & Gia Arbo, 2021). Understanding the connection between public-private partnerships and housing affordability can help economists and policymakers make informed decisions about how best to support sustainable economic growth and guarantee that all facets of society have access to affordable housing.

III. METHODOLOGY

This paper provides a qualitative analysis of the housing challenges and the roles of social financing in promoting home ownership among citizens. It began by explicitly reviewing previous empirical studies, government documents, and annual and news reports. Given the objective of this study, which is to discuss the challenges and explore the roles of social financing in Malaysia, using social construction ism (a qualitative technique) is more suitable than positivism. A focus group discussion (FGD) procedure was employed to examine their challenges. The focus group method was used as it allows for interaction between participants and researchers (Marczky et al., 2005). The moderator in the focus group discussion plays a crucial role in guiding the conversations to obtain the desired information and ensure that participants stay focused.

The FGD lasted approximately 90 minutes and adhered to the techniques proposed by Kumar (2011) and Kamal et al. (2020), who have identified comparable methods for conducting and overseeing an FGD. The FGD was recorded and transcribed for further analysis and interpretation. The keywords were identified and categorised into relevant segments. In addition, the study reviews and synthesises the relevant literature on social financing in the housing sector, referencing Bank Islam Malaysia Berhad (BIMB) as one of the financial institutions offering social financing products for housing using secondary literature sources. A focus group of ten participants was conducted from low-income groups living in PPR Kampung Kerinchi, Kuala Lumpur, and the issues and difficulties they faced were investigated. It is significant to capture households’ opinions, as they are the targeted audience and focal point of any public housing scheme. The data was then analysed using thematic analysis to produce the findings.

IV. FINDINGS AND DISCUSSION

This section presents the findings and discussion on the profile of the informants, the housing challenges faced by the underprivileged, and the role of social financing as a tool for promoting home ownership.

IV.A. Profile of the Informants

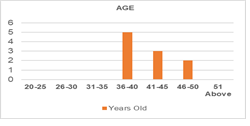

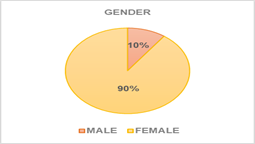

The study obtained responses from 10 informants from the low-income group, which we called underprivileged. All the informants reside in the low-cost flats in the centre of Kuala Lumpur. They are currently renting the place from the Dewan Bandara Kuala Lumpur, a city council in Malaysia that is responsible for developing public housing, especially for the underprivileged in urban areas. Figure 2 shows that the informants (underprivileged) are above 35 years old overall. The majority (90%) are female, and the remaining (10%) are Male, as shown in Fig. 3. At the time of the FGD session, most male residents were working.

Fig 2 Age of the informants’

Fig 3 Gender

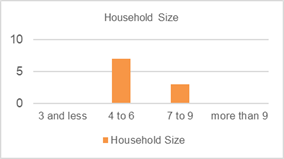

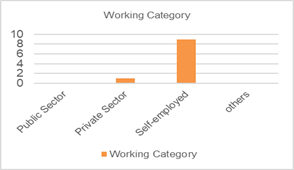

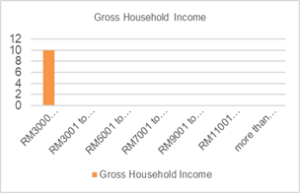

The majority are Malay, and the minority are Indians, with a household size of 4 to 9 people in a house, as depicted in Fig. 4 and 5 below. Fig. 6 shows that most of the informants are self-employed, doing small business to sustain living. Only one informant works in the private sector. For the gross household income, most of them earned RM3000 or less, thus putting them under the category of B40 according to the Malaysian income bracket. According to the Department of Statistics Malaysia (DOSM), the mean income for households in the B40 category was reported at RM3,401 in 2022. They can be considered underprivileged, with a lack of access to housing and exposed to poverty.

Fig 4 Race of the informants

Fig 5 Household

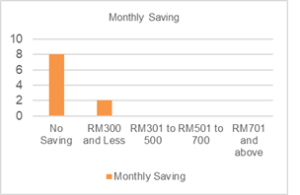

Regarding the monthly savings, almost all of them have no savings due to insufficient and low income. They confessed that their salary was only sufficient to cover their daily expenses, which prevented them from saving money. These can be seen from the following:

remark:

R1: “We cannot save money because what we get is only small.”

R3: “How to save money, to meet daily needs also we struggle.”

R6: “I save a little bit, but always used after that.”

R10: To be honest, I have no savings because all were used to cover daily expenses.”

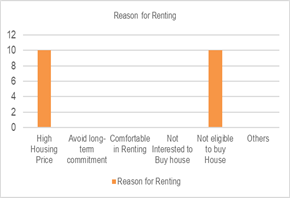

Only a few have monthly savings of RM300 or less, as shown in Fig. 8 below. They are currently renting low-cost public housing (flats). 50% of respondents declared the high housing price in the market, and another 50% disclosed that they were not eligible to buy a house, making them settled as renters, as illustrated in Fig. 9 below. They mentioned their desire to purchase but felt it was unattainable because financing was difficult to obtain.

Fig 6 Working category

Fig 7 Gross household income

Fig 8 Monthly saving

Fig 9 Reason for renting

IV.B. Housing Challenges Faced by The Underprivileged in Home ownership

The participants were asked about the housing challenges in their pursuit of home ownership. First, the findings discovered that housing affordability remains a significant challenge for them and thus requires government and private sector interventions. They were confronted with housing affordability problems associated with low income, difficulty paying for housing deposits, and difficulty securing financing, as highlighted in a study by Ebekozien et al. (2019). This can be seen from the following comments:

R5: “Make it easier to qualify for a loan. The deposit should not be too expensive, and my name is already blacklisted; I want to make a loan even if it is difficult. If I can afford it, I will buy it later.”

R7: “It is the same. Make it easier to qualify with my income, help those who have difficulty getting this loan to get our own house, and give us the info.”

R10: “People who do small business, we can afford to buy but cannot make any loan. If there is a platform, at least we can improve our lives and buy a house.”

Second, the issue of rising house prices and affordability raises concern among Malaysians, as also discovered by Ravi et al. (2022). The participants hoped for price regulation as the soaring prices of the houses in the market and the people’s average income made affordable housing opportunities deficient. The medium and low-income groups demand that the government build more affordable housing that suits their income and should relook at the measurement of affordable housing to ensure it is affordable and accessible. Not only that, during the COVID-19 pandemic, many individuals (such as T20 becoming M40) and communities experienced changes in their economic circumstances, which affected their housing opportunities. On another note, even though the housing supply is deemed adequate within the housing sector, the population’s constrained financial means curtail their housing aspirations, as highlighted in a study by Zyed et al. (2020) and Alharbi (2021). Insufficient financial standing and substantial financial obligations contribute to the restricted availability of suitable homes. This can be seen from the following comments:

R1: “Like me, after COVID, I could not afford to buy a house for four years. I do not work, so I do not have a salary. How can I pay? Not to mention, owning and paying rent is also difficult.”

R6: “We suffered a lot during Covid. We lost our income and have no other housing options. Renting is also difficult, let alone owning.”

The third challenge faced by them was related to financial literacy. Lack of knowledge about financial matters poses a significant obstacle for the specific group in their pursuit of becoming homeowners. Financial literacy includes understanding and applying diverse financial skills, such as personal financial administration, budgeting, and investment in daily life, which is absent among themselves. Most of the participants expressed their struggle to save for the housing deposit. The questionnaire survey findings from a study by Zyed et al. (2020) found that the level of awareness of the home-buying process is low in the monetary phase, which is on how to save money for a house down payment, mortgage monthly payment and finding the best interest rates for a housing loan. This deficiency contributed to the challenges people face, especially among the underprivileged. It was further confirmed by Ravi et al. (2022) that financial illiteracy is the obstacle to the targeted group owning a home.

“R6: As for me, I want to know my qualifications to be entitled to the loan, but I do not know. Maybe banks can help us to get more information on this. That is what we are wondering about. Please publicise this offer to me, who has lived here long.”

R9: We do not even know how much we have to deposit, our qualifications, and so on.”

Individuals must cultivate a robust comprehension and proficiency in effectively managing their resources. Without these skill sets, this group will not understand the importance of wealth management in tackling the problem of poverty impacting this social demographic. Financial stress can negatively impact an individual’s productivity, physical health, financial situation, and emotional state. On a broader scale, an individual without sufficient financial wealth impacts not only themselves and their immediate social circle but also a country’s economic and financial institutions.

The participants were further asked about their intention to move, and the findings from the interview discovered that most of them intend to move from their current house and plan to own a home in the future. Despite their challenges, they still dream of owning a home if they can afford it. This is perhaps due to the homeowning aspiration that most Malaysians have compared to other countries where renting will be their first option due to their affordability and commitment. This can be seen from the participants who made the following interpretations:

R5: “I want to own a house. Yes, indeed, the current location is strategic. Because city houses are not easy to get. But I do not know whether I can get the loan to buy.”

R6: “I also want to have my own house. However, I know it is difficult for me with my income.”

R7: “I would like to have it if I can afford it”

R8: Yes, that is right, I also want to own a house if possible.

R9: “I want to have it, even if I must pay. We have children, so we want to buy this house. If banks and government can help us obtain financing, it will help us greatly.”

R10: We all want to buy but cannot afford it. Having is an aspiration. However, our income is low, so it is hard to buy because we cannot qualify for a loan.

The current study’s findings support many other studies connecting housing intention and opportunities. A study regarding the housing needs of people in Turkey shows that residents in Turkey want and need more than they have, thus expressing their housing preferences (Gürsoy & Akıncı, 2022; Kaya et al., 2019). Despite their unaffordability, many preferred to own a place they could call home, as Soon and Tan (2019) and Ma et al. (2023) discussed. Many families want to own a home which serves not only as a place of shelter and comfort but also as a symbol of their lifelong achievements. The housing opportunities of many people should be considered so that we can increase the home ownership rate. As such, meeting the housing needs of people, including older adults, is crucial (García, 2024). The intention to move was also mentioned in a study by Hoxha and Zeqiraj (2019), regardless of the generations. However, the results showed that the intention varies depending on the person’s financial situation and finance accessibility.

IV.C. Roles of Social Financing as a Tool for Promoting Home Ownership

The Malaysian government has acknowledged the impact of increasing house prices on the social well-being of citizens. As such, they have intervened through several housing initiatives, such as affordable home ownership schemes and collaborations with several financial institutions, to increase access to home ownership. A potential homeowner in Malaysia has multiple options for obtaining home financing. These come from financing the public sector provides, especially for civil servants and private banking institutions, including conventional and Islamic banks (Wahab et al. (2016). Nonetheless, since the 1990s, an increase in house prices, the rejection of housing loan applications, and bankruptcy due to defaulting on housing loans have emphasised the necessity for an improved home financing method. Since traditional home financing seems inaccessible to the underprivileged, social financing is another housing financing method. Social finance refers to using financial resources, such as funds, investments, or loans, to tackle social problems and attain social goals, specifically in areas associated with reducing poverty, improving healthcare, enhancing education, and fostering community development (Bank Negara Malaysia Financial Sector Blueprint, 2022). Social finance entails allocating financial resources to initiatives and programmes that strive to generate positive social outcomes and enhance the welfare of disadvantaged individuals and communities (Ziyaviddinovna, & Sagdullaevich, 2020).

Islamic social financing mechanisms, such as Zakat (mandatory charity), Sadaqat (voluntary charity), Waaf (charitable endowment) and Qard-hasan (collateral and interest-free loan), can help accomplish the Sustainable Development Goals because they aim to improve communal or individual well-being by giving monetary assistance (Dirie et al., 2023). Waqf can be employed to address funding issues and establish social welfare systems, as mentioned by Faturohman et al. (2021). Maulina, Dhewanto, and Faturrahman (2023) findings corroborated that the integration between Islamic social and commercial finance has effectively addressed various economic and social issues confronting the Ummah (people). Besides, the findings by Alharbi (2021) suggest the need for strong relationships with relevant stakeholders, such as non-government organisations (NGOs), to guarantee housing finance and achieve the objective of housing for all. The collaborations were further highlighted by Nastiti and Kasri (2019) in their study on the development of Islamic banking financing in Indonesia.

Islamic house financing, such as Musharakah Mutanaqisah (MM), fosters societal welfare and is a viable alternative, as Lim et al. (2019) argued. A study was also conducted regarding the role of Islamic home financing in tackling the sustainability of home ownership affordability and found that the method could enhance home ownership affordability (Yusof et al., 2023). A study in China also discussed the proposed home financing model. The researchers investigated the Chinese acceptance of an Islamic principle-based integrated solution to housing affordability. The findings disclosed that the proposed model was well-received by the communities. However, they expressed concern over the implementation due to their lack of understanding of the principles of Shariah and business, thus suggesting the pilot study among the Muslim majority areas (Ma et al., 2023).

Due to the unaffordability of many people to access home ownership, housing experts and various agencies, such as the National Affordable Housing Council (MPMMN), have called for Bank Negara Malaysia (BNM) to reassess its financing framework to facilitate home ownership for individuals belonging to the B40 and M40 segments (The Malay Reserved, 2021). Meanwhile, economists are urging BNM to implement social finance mechanisms to cater to these groups of potential home buyers (Property Guru, 2022). Similarly, Bilal et al. (2019) proposed an alternative model for housing financing due to the inaccessibility of home financing facilities. Their findings found that a significant number of applicants are unable to secure home financing from financial institutions due to various reasons such as unemployment, irregular income, bank default or being blacklisted low income, and insufficient funds for a down payment.

Several banking institutions that provide social financing took up the initiatives as part of their efforts to support socioeconomic empowerment. Taking Bank Islam Malaysia Berhad (BIMB) as an example, this institution initiated social financing to assist those in the underprivileged category to obtain financing. The aim is to foster the long-term growth and viability of the communities that advance financial inclusion and assist vulnerable groups. In 2018, Bank Islam initiated Sadaqa House, the crowdfunding platform that promotes financial inclusivity by offering banking facilities to under banked segments through their microfinance offering (Bank Islam Integrated Report, 2022). While Islamic banks are for-profit businesses, evaluations of their operations consider social and financial factors, as Nugraheni and Muhammad (2023) argued.

Bank Islam has collaborated with the Zakat Board to provide home financing for the underprivileged from the Asnaf groups, who are eligible for the aid. The scheme was established through a joint venture with the state Zakat management agency, where both organisations will invest half of the home financing that benefits the underprivileged. The initiatives provide them with housing opportunities, thus indirectly improving their well-being. In a media release published in May 2021, Bank Islam acknowledges and is responsive to the community’s requirements and the hardship experienced by the disadvantaged, particularly in the current demanding economic circumstances.

Several initiatives have been implemented to support and aid those in need, including providing affordable housing. To address this matter, they established the Bank Islam Housing Aid Programme in 2008 to offer suitable homes to the most impacted and deserving individuals. The programme began in Kelantan and was extended to Terengganu before being implemented nationwide. So far, almost 300 Asnaf have received more than RM9 million in benefits offered by them (Bank Islam Media Release, 2021). The program handled by Bank Islam has proven to reduce the people’s financial burden and increase their home ownership of KAFA (Quran and Fardu Ain) teachers in Malaysia, who were previously not entitled to home financing due to their low income. Under this project, the Kedah Zakat Board will support 50% of the cost of building a house in Kedah. The recipient will bear another 50% through the i-Asnaf personal financing with BIMB, as reported by the World Zakat and Waqf Forum (2021).

Social financing can enhance the economic mobility of individuals from areas that cannot access conventional banking facilities, enabling them to become part of the banking system. In this role, banking institutions are not solely focused on monetary figures but rather extend their priorities beyond that. Serving the underprivileged can create a long-term relationship with them and eventually create financial sustainability for the people with them, benefiting the banking institutions in the long run. Therefore, the activity is expected to encourage greater customer loyalty to Islamic banks, as Nugraheni and Muhammad (2023) agreed when discussing the role of Islamic banking in Indonesia.

Implementing Islamic banking (IB), which involves using cash waqf as a practical personal financial model, can benefit consumers and improve the bank’s image and reputation, as highlighted in Maulina et al. (2023). A finding by Wahab et al. (2023) confirmed that Islamic banking significantly enhances affordability by providing fair and sustainable finance. The study emphasises that Islamic banking has, to some degree, successfully adhered to its principles in attaining the Maqasid al-shariah.

An alternative housing unaffordability solution based on the Islamic finance principle was also proposed in a study conducted by Dirie et al. (2023) and Ma et al. (2023) to ensure the inclusiveness of the financing for all. Another study by Acri et al. (2021) also proposed housing construction and purchase through the social financing model to manage housing problems in Russia. Similarly, Ravi and Redzuan (2022), in their study on the residential development of the low-income group, disclosed that most individuals in the B40 demographic face challenges in accessing credit from financial institutions due to their limited credit history and lack of collateral. Hence, it proposed that the collaboration between Islamic banks could play a significant role by acting as a collection agent from the public as a source of funding and channelling the funds to the waqf organisations or directly to the affordable housing project.

The underprivileged in Malaysia, the bottom 40 category (B40) demographic, face challenges securing financing from financial institutions. This impedes their ability to purchase a home and acquire financial aid from financial institutions. Social financing can be seen as an effort by banks to subside hidden charges on low-income housing as part of their corporate social responsibility, thus increasing the chances of LIEs accessing housing loans. Blakeley (2021) suggested that the government could de-financialise the housing system and ensure that housing is seen as a human right rather than a speculative financial asset. Hence, Islamic social finance systems, which ensure environmental, social, and economic sustainability following the SDGs, can address various social issues and improve well-being (Dirie et al., 2023).

IV.C.1 Good Governance as a Driver for Social Change

Social finance providers must practice good governance to distribute resources efficiently and fairly. A government that is approachable, aware of the people’s needs, and responsive to those needs can be described as practising good governance (Taryono et al., 2021). In this setting, good governance is facilitated by the following fundamental ideas and practices: transparency, accountability, participation, stakeholder engagement, and monitoring and evaluation.

To foster confidence among stakeholders, social financing must be transparent. The public should have access to transparent information regarding the distribution, allocation, and use of funds. In addition to facilitating public and beneficiary scrutiny, this transparency ensures accountability. Moreover, transparency influences higher organisational performance and fosters a culture of responsibility within a company (Gold & Heikkurinen, 2018). When transparency is successful, it improves public trust in the government by fostering good governance and government accountability. In addition, through improvements to administrative processes and systems at both the regional and national levels, transparency can alter and impact enterprises, political institutions, the environment, and culture (Wanna, 2018).

Besides, effective governance creates supervision and accountability systems, ensuring that individuals in charge of housing resource management are held accountable for their deeds. Frequent audits and evaluations assist in locating and resolving any problems with the distribution or upkeep of housing resources. Moreover, robust accountability systems help prevent financial mismanagement and corruption. Regular reporting procedures, audits, and performance reviews should be in place to hold all parties responsible for their activities. This is because, due to the effectiveness of internal auditing, it can prevent risks, battle corruption, preserve assets, and improve the accuracy of financial reports. (Alaswad & Stanišić, 2016; Postula et al., 2020). Additionally, outstanding accountability would enable organisations to determine to whom accountability is made and for what reason and to build more robust governance within their organisational framework. (Karunia et al., 2023).

Communities with good governance are more likely to participate actively in housing decision-making. With the assistance of the public, local needs, preferences, and priorities can be identified, resulting in a more informed and community-focused housing policy. Therefore, involving the target community in decision-making will ensure their needs are accurately assessed and met. Establishing mechanisms for public consultation and feedback helps create inclusive policies that address the population’s diverse needs. Specifically, we encouraged strong stakeholder involvement while developing decision-making aids for residents, community organisations, and city officials (Stonewall et al., 2019).

According to Naidoo (2012), efforts to achieve good governance must include monitoring and evaluation, which should result in observable advancements in how the government runs its affairs and its services to its constituents. When Ojok (2016) looked at how monitoring and evaluation helped promote good governance in Uganda’s public sector, she discovered that organisational learning, management choices, and monitoring and evaluation (M&E) accountability had a significant impact. She also suggested that M&E should be used to support evidence-based decision-making. Public officials should be held accountable for their actions and make decisions based on the best available evidence to improve good governance standards in public institutions. Effective monitoring and evaluation offer many benefits, including capacity enhancement, community involvement, employee motivation, quality of service delivery quality, and increasing transparency and accountability (Mohamed & Kulmie, 2023).

V. CONCLUDING REMARKS

The present study’s findings have raised some important policy implications. Based on the evidence, housing affordability is the main reason people cannot own it, which has become one of the challenges they face. Some people failed to obtain bank loan financing and were called ‘unbankable’. The government, banking institutions, and house developers can collaborate to devise alternate eligibility requirements. The discovery highlights that individuals struggle to follow their goals due to stringent eligibility criteria. They face difficulties obtaining a loan due to their low incomes, poor credit history, and stringent bank lending regulations. The findings from the study also highlight the challenges related to financing accessibility for affordable homes. There is a significant loan rejection rate among those looking for affordable homes, leading to an inability to become homeowners. Therefore, it is imperative to relax or loosen the regulations regarding housing and lending to facilitate their access to housing financing.

Other financial alternatives, particularly for individuals with the potential for ownership (such as small business owners) yet ineligible for conventional bank financing, should be provided to facilitate purchasing a place of their own. This can be seen from social financing as an alternative to conventional financing to boost the homeownership rate among Malaysians, particularly the underprivileged. In conclusion, this study emphasises the importance of offering alternative housing financing that caters to the needs of people, especially the underprivileged. The introduction of social financing in managing unaffordability issues among the people is seen as a practical tool for the underprivileged to pursue homeownership and financial institutions as part of their social responsibility. Although this study provides insights, it has some limitations. The sample size of 10 participants is small, so the findings may not represent all underprivileged people. More quantitative studies would be needed. Additionally, the study focused on Kuala Lumpur, but the housing challenges and needs for housing among the underprivileged may vary in different states and socio-cultural groups. Future research can build on these findings by including a more diverse sample to comprehensively understand their challenges and how social financing can help improve their housing opportunities.

VI. ACKNOWLEDGEMENT

The authors would like to acknowledge the participation of the residents of PPR Kerinchi, Kuala Lumpur, in this study. This work was supported by the Institut Masa Depan Malaysia (MASA), under the Research grant MASA Policy Development Program (P22/2023/022).

VII. REFERENCES

- Abidoye, R. B., Puspitasari, G., Sunindijo, R. Y., & Adabre, M. A. (2020). Young adults and homeownership in Jakarta, Indonesia. International Journal of Housing Markets and Analysis, 14(2), 333–350. https://doi.org/10.1108/ijhma-03-2020-0030

- Acri, E. P., Vorontsova, N. V., & Egorova, I. P. (2021). Housing construction and purchase through the model of social financing. IOP Conference Series: Materials Science and Engineering, 1079(2), 022011. https://doi.org/10.1088/1757-899x/1079/2/022011

- Aizawa, T., Helble, M., & Lee, K. O. (2020). Housing inequality in developing Asia and the United States. Cityscape, 22(2), 23-60.

- Alaswad, S. A. M., & Stanišić, M. (2016). Role of internal audit in performance of Libyan financial organizations. International journal of applied research, 2(2), 352-356.

- Alharbi, R. K. (2021). Early Impact of Covid-19 on Private Sector Employees Finance Homeownership in the Kingdom of Saudi Arabia. International Journal of Housing Markets and Analysis, 16(1), 5–21. https://doi.org/10.1108/ijhma-08-2021-0093

- Audi, M., & Ali, A. (2023). The Role of Environmental Conditions and Purchasing Power Parity in Determining Quality of Life among Big Asian Cities. International Journal of Energy Economics and Policy, 13(3), 292–305. https://doi.org/10.32479/ijeep.13583

- Bakhtyar, B., Zaharim, A., Sopian, K., & Moghimi, S. (2013). Housing for poor people: A review on low-cost housing process in Malaysia. WSEAS transactions on environment and development, 9(2), 126-136.

- Bank Islam Malaysia Berhad, May 9 (2021). Bank Islam Hand Overs 11 Housing Units to Asnaf Ahead of Raya Celebrations. Press release. https://www.bankislam.com/wp-content/uploads/Media-Release-Bank-Islam-Hand-Overs-11-Housing- Units-To-Asnaf-Ahead-Of.pdf

- Bank Negara Malaysia. (2020). “Bank Negara Malaysia Financial Sector Blueprint 2022-2026”. Accessed Jan 29, 2024. https://www.bnm.gov.my/social-finance

- Bilal, M., Meera, A. K. M., & Abdul Razak, D. (2019). Issues and challenges in contemporary affordable public housing schemes in Malaysia: Developing an alternative model. International Journal of Housing Markets and Analysis, 12(6), 1004-1027.

- Corsetti, G., Duarte, J. B., & Mann, S. (2020). One money, many markets: monetary transmission and housing financing in the euro area. International Monetary Fund.

- Department of Statistics, Malaysia (DOSM). “Household Income Estimates and Incidence of Poverty Report”. Accessed Jan 29, 2024. https://v1.dosm.gov.my/v1/index.php?

- Dirie, K. A., Alam, M. M., & Maamor, S. (2023). Islamic social finance for achieving sustainable development goals: a systematic literature review and future research agenda. International Journal of Ethics and Systems. https://doi.org/10.1108/ijoes-12-2022-0317

- Duan, M. (2011). Investigation on housing affordability in Lanzhou, Northwest China. International Journal of Housing Markets and Analysis, 4(2), 180–190. https://doi.org/10.1108/17538271111137958

- Economic Planning Unit. “Mid-Term Review of the Eleventh Malaysia Plan, 2016–2020”: New Priorities and Emphases; Ministry of Economic Affairs: Putrajaya, Malaysia, 2018; ISBN 9789675842139.

- Ebekozien, A., Abdul‐Aziz, A., & Jaafar, M. (2019). Housing finance inaccessibility for low-income earners in Malaysia: Factors and solutions. Habitat International, 87, 27–35. https://doi.org/10.1016/j.habitatint.2019.03.009

- Ebekozien, A., Aigbavboa, C., Aigbedion, M., Ogbaini, I. F., & Awe, E. O. (2022). Housing finance inaccessibility: evidence from the Nigerian Pensioners. Property Management, 40(5), 671–689. https://doi.org/10.1108/pm-09-2021-0064

- Faturohman, T., Rasyid, M. F. A., Rahadi, R. A., Darmansyah, A., & Afgani, K. F. (2021). The potential role of Islamic social finance in the time of COVID-19 pandemic. Review of Integrative Business and Economics Research, 10, 95-105.

- Friesen, J., Taubenböck, H., Wurm, M., & Pelz, P. F. (2018). The similar size of slums. Habitat International, 73, 79-88.

- Gold, S., & Heikkurinen, P. (2018). Transparency fallacy. Accounting, Auditing & Accountability, 31(1), 318–337. https://doi.org/10.1108/aaaj-06-2015-2088

- Gürsoy, Ö., & Akıncı, N. F. (2022). Examining housing quality in Turkey through resident preferences and their housing conditions: a survey study. Property Management. https://doi.org/10.1108/pm-06-2021-0039

- Helble, M., Lee, K. O., & Arbo, M. a. G. (2020). How (Un)affordable is housing in developing Asia? International Journal of Urban Sciences, 25(sup1), 80–110. https://doi.org/10.1080/12265934.2020.1810104

- Hoek-Smit, M. C., & Diamond, D. (2008). Subsidizing housing finance for the poor. University of Pennsylvania.

- Hoxha, V., & Zeqiraj, E. (2019). The Impact of Generation Z in the Intention to Purchase Real Estate in Kosovo. Property Management, 38(1), 1–24. https://doi.org/10.1108/pm-12-2018-0060

- Kamal, E. M., Lai, K. S., & Yusof, N. A. (2020). The low-middle income housing challenges in Malaysia. Planning Malaysia, 18.

- Kaya, S. K., Ozdemir, Y., & Dal, M. (2019). “Home-buying behaviour model of Generation Y in Turkey.” International Journal of Housing Markets and Analysis, 13(5), 713–736. https://doi.org/10.1108/ijhma-05-2019-0048

- Khazanah Research Institute (2015). Making House Affordable. Khazanah Research Institute, Kuala Lumpur, Malaysia. August2015, ISBN: 978-967-12929-2-1.

- Khazanah Research Institute (2019). Rethinking Housing: between State, Market and Society: A Special Report for the Formulation of the National Housing Policy (2018 – 2025), Malaysia.Khazanah Research Institute, Kuala Lumpur, Malaysia. April2019, ISBN: 978-967-16335-8-8

- Kumar, R. (2018). Research methodology: A step-by-step guide for beginners. Research methodology, 1-528.

- Li, W., & Zhi, L. (2023). Diversified Urban Housing Markets and Decentralized Market Regulation in China. International Journal of Housing Markets and Analysis. https://doi.org/10.1108/ijhma-03-2023-0036

- Lim, H. E., Yusof, R. M., & Khan, S. J. M. (2019). Musharakah Mutanaqisah (Mm) Home Financing for Affordability of Homeownership: A Simulation Case Study Approach. Planning Malaysia Journal, 17(9). https://doi.org/10.21837/pmjournal.v17.i9.583

- Ling, C. S., Almeida, S. J., & Wei, H. S. (2017). Affordable housing: challenges and the way forward. BNM Quarterly Bulletin: Box Article, Fourth Quarter, 19-26.

- Liu, J., & Ong, H. Y. (2021). Can Malaysia’s National Affordable Housing Policy guarantee housing affordability of Low-Income households? Sustainability, 13(16), 8841. https://doi.org/10.3390/su13168841

- Ma, Y., Taib, F. M., & Gold, N. O. (2023). An Islamic Principle-based Integrated Solution for China’s Housing Affordability Issues. International Journal of Housing Markets and Analysis. https://doi.org/10.1108/ijhma-10-2022-0152

- Marczyk, G. R., DeMatteo, D., & Festinger, D. (2010). Essentials of research design and methodology (Vol. 2). John Wiley & Sons.

- Maulina, R., Dhewanto, W., & Faturrahman, T. (2023). The Integration of Islamic Social and Commercial Finance (IISCF): Systematic Literature Review, Bibliometric Analysis, Conceptual Framework, and Future Research Opportunities. Heliyon, 9(11), e21612. https://doi.org/10.1016/j.heliyon.2023.e21612.

- Mohamed, N., & Kulmie, D. A. (2023). Role of effective monitoring and evaluation in promoting good governance in public institutions. Public Administration Research, 12(2), 48. https://doi.org/10.5539/par.v12n2p48

- Naidoo, I. A. (2011). The role of monitoring and evaluation in promoting good governance in South Africa: A case study of the Department of Social Development. Johannesburg: University of Witwatersrand.

- Nwuba, C. C., & Chukwuma-Nwuba, E. O. (2018). Barriers to accessing mortgages in Nigeria’s housing markets. International Journal of Housing Markets and Analysis, 11(4), 716–733. https://doi.org/10.1108/ijhma-10-2017-0089

- Ojok, J., & Basheka, B. C. (2016). Measuring the Effective Role of Public Sector Monitoring and Evaluation in Promoting Good Governance in Uganda: Implications from the Ministry of Local Government. Africa’s Public Service Delivery and Performance Review, 4(3), 410. https://doi.org/10.4102/apsdpr.v4i3.122

- Property Guru. (2022, February 14). BNM Urged to Review Financing Model for Home Buyers, Economists Want BNM To Introduce Social Financing Mechanism to Boost Home Ownership, And More. The Property Guru. https://www.propertyguru.com.my/property-news/2022/2/203565/bnm-urged-to-review-financing-model-for-home-buyers-economists-want-bnm-to-introduce-social-financing-mechanism-to-boost-home-ownership-and-more

- Rangel, G. J., Ng, J. W. J., Murugasu, T. T., & Poon, W. C. (2023). Measuring long-run housing affordability for Malaysian millennial households: a geospatial and income distribution analysis. International Journal of Housing Markets and Analysis. https://doi.org/10.1108/ijhma-02-2023-0017

- Ravi, M. I. M. R., & Redzuan, N. H. (2022). Development Residential Property for B40: A Proposed Collaboration Framework Between Islamic Bank, Waqf, and Zakat Institutions. International Journal of Islamic Business, 7(2), 13-43.

- Saha, A., Lim, H. E., & Yeok, S. G. (2022). Housing loan default in Malaysia: an analytical insight and policy implications. International Journal of Housing Markets and Analysis, 16(2), 273–291. https://doi.org/10.1108/ijhma-01-2022-0002

- Soon, A., & Tan, C. (2019). An analysis on housing affordability in Malaysian housing markets and the home buyers’ preference. International Journal of Housing Markets and Analysis, 13(3), 375–392. https://doi.org/10.1108/ijhma-01-2019-0009

- Subagyo, A., Syari’udin, A., & Yunani, A. (2022). Determinant residential real estate of millennial generation in adapting housing microfinance case Indonesia chapter. International Journal of Housing Markets and Analysis, 16(5), 1007–1020. https://doi.org/10.1108/ijhma-04-2022-0063

- Taryono, T., Anggraeni, R. D., Yunus, N. R., & Rezki, A. (2021). Good Governance and Leadership; Sustainable National Development with Good Governance and Leadership in Indonesia. Salam, 8(2), 649–662. https://doi.org/10.15408/sjsbs.v8i2.20253

- The Sustainable Development Goals Report 2021. (2021). The Sustainable Development Goals Report. https://doi.org/10.18356/9789210056083.

- United Nations Habitat. (2014). The Right to Adequate Housing [Fact sheet]. https://www.ohchr.org/en/special-procedures/sr-housing/human-right-adequate-housing

- Wahab, N. A., Bin-Nashwan, S. A., Chik, M. N., & Hussin, M. Y. M. (2023). Islamic Social Finance Initiatives: An Insight into Bank Islam Malaysia Berhad’s Innovative BangKIT Microfinance Product. ISRA International Journal of Islamic Finance, 15(1), 22–35. https://doi.org/10.55188/ijif.v15i1.483

- Wanna, J., & Vincent, S. (2018). Opening government: Transparency and engagement in the information age (p.178). ANU Press. Retrieved from https://www.jstor.org/stable/j.ctv1rmjnq.5.

- World Bank. (2020). Aspirations Unfulfilled: Malaysia’s Cost of Living Challenges, retrieved at https://www.worldbank.org/en/country/malaysia/publication/aspirations-unfulfilled-malaysias-cost-of-living-challenges, accessed on Jan 31, 2023

- Yaacob, M.A., & Hassan, N. (2023). Exploring the challenges faced by the urban squatter dwellers in Sentul, Kuala Lumpur, Malaysia. Journal of Population and Social Studies (Online), 32, 14–35. https://doi.org/10.25133/jpssv322024.002

- Yusof, N., Shafiei, M. W. M., Yahya, S., & Ridzuan, M. M. (2010). Strategies to implement the “build then sell” housing delivery system in Malaysia. Habitat International, 34(1), 53–58. https://doi.org/10.1016/j.habitatint.2009.06.001

- Zamri, N. E. M. M., Yaacob, M. ‘., & Suki, N. M. (2021). Assessing housing preferences of young civil servants in Malaysia: do location, financial capability and neighbourhood really matter? International Journal of Housing Markets and Analysis, 15(3), 579–591. https://doi.org/10.1108/ijhma-02-2021-0012

- Ziyaviddinovna, M. M., & Sagdullaevich, K. K. (2020). Poverty reduction by Islamic waqf system. Journal of Critical Reviews, 7(4), 68-73.

- Zyed, Z. a. S., Low, C. S., & Tedong, P. A. (2020). Delivery mechanism on homeownership education among millennials in Kuala Lumpur. International Journal of Housing Markets and Analysis, 14(2), 410–423. https://doi.org/10.1108/ijhma-02-2020-0009