Rice Distribution Structure: the Reality or Political Propaganda of Php 20.00/Kilo Price of Rice in the Market?

- Rowina Mendoza Twaño

- Mharree Joie Shynne P. Gomez

- Maria Liberty F. Isip

- Krist Mark Q. Macapugay

- 4048-4060

- Mar 20, 2025

- Marketing

Rice Distribution Structure: The Reality or Political Propaganda of Php 20.00/Kilo Price of Rice in the Market?

Rowina Mendoza Twaño, DBA, RECE; Mharree Joie Shynne P. Gomez, MBA; Maria Liberty F. Isip, MBA; Krist Mark Q. Macapugay, MBA

Don Honorio Ventura State University Bacolor Campus– College of Business Studies

DOI: https://dx.doi.org/10.47772/IJRISS.2025.9020316

Received: 13 February 2025; Accepted: 17 February 2025; Published: 21 March 2025

ABSTRACT

This multi – phased case study research principally aims to investigate the possibility of attaining the Php 20.00 per kilo price of milled rice in the market. The study explores the nature and structure of the Supply Chain distribution of Rice, tracing the changes in the level of prices in Pampanga. Relevant Quantitative cost data were derived from 10 farmers in Pampanga, who are farming land from 1 to 2 hectares. Other relevant data that make up the distribution system of rice in the market were sourced from the interviews conducted with agents, millers, wholesalers and retailers in the province. Secondary data from related literature, government and other agencies in agriculture and cooperatives were also interviewed for the needed data in the study. Results show that the estimated total cost of milled rice is Php 17.17 (manual) and Php17.28 (tractor), without yet the mark-up for profit, taking into account that farmers take the role of producers and sellers to end- users. If farmers choose to sell their produce at Php 20.00 kilo, the estimated profit is total to Php 8,490.00 (manual) and Php 8, 160.00 (tractor) for one hectare of land in one cropping which falls under the income range of Filipino families living under poverty threshold. Thus, satisfying the call for Php 20.00/kilo of rice, will further sink the Rice farmers’ families into the pit of poverty. The study recommends that the Department of Agriculture encourage the concept of direct marketing by the farmers themselves and look for ways to further decrease the actual cost incurred in production to retailing of rice.

Keywords: supply chain distribution, milled rice, market price of milled rice, rice- farmers, intermediaries

INTRODUCTION

The Philippines is still a country of farmers, particularly rice which has been a pivotal political commodity because of its importance as a staple food and calorie source for majority of the population. The Philippines became self-sufficient in rice in the 1970s and was a rice exporter to neighbouring countries such as Indonesia, China, and Myanmar). The Philippines has approximately 4.75 million ha of rice lands or about 49% of the total agricultural area (Philippine Statistics Authority, 2019) and produces about 11.2 million Metric Tons of milled rice, sufficient only for 90% of the population (Rebualos, et al., 2021). Of the total agricultural produce of the country, about 20% comes from rice. It is grown in 2.2 million farms, which is about 45% of the total number of farms in the country. However, with the rapid increase in population and limited land resources to produce the total rice requirement, and with the Climate change also aggravates the existing economic fragility of rice productivity (Stuecker et al., 2018), the country slowly turned into a net rice importer. Next to China, the Philippines is the second largest rice importer in the world (Simeon, 2019).

Philippine Rice Tariffication Law

Philippine Rice Tariffication Law (RA 11203) which basically permits the liberalization of rice imports, removes the previously placed quota and replaced with higher tariffs on rice imports, permitting traders to import a near-unlimited quantity of rice (House of Representative, 2019). The law provides safety net measures for local farmers under the Rice Competitiveness Enhancement Fund (RCEF) which is expected to help and support the rice farmers to cope up with the liberalization of the rice market. The government will allocate P10 billion annually for the next six years to support the Filipino rice farmers and this will be assessed after the first three years of its implementation.

Many farmers in the Philippines claimed that the implementation of the Rice Tariffication Law (RTL) brings an impact to the farmers (Casinillo, 2020). Farmers lost around 68 billion pesos due to the effects of the policy which saw the influx of more imported rice and the losses of rice producers exceeded the gains of consumers by as much as 34 billion in the first year of implementation of the law.

With the implementation of the law, the sector remains to be one of the most challenged as Filipino rice farmers incomes remains one of the lowest in the industry. The Department of Agriculture, the government agency responsible for agricultural development identified several barriers to growth in the farming sector. High cost of production inputs like fertilizers and pesticides accounts for almost 30% of the production cost in farming, post – harvest losses, high transportation cost of distribution of agricultural products from farm to market, inadequate irrigation and infrastructure, extreme weather conditions brought about by global warming and limited access of farmers to credit (DA, 2020). The high cost of farm inputs makes the farm gate price of paddy rice not competitive among imported rice products. Forcing farmers to accept the price set by the dealer/traders for their produce paddy rice.

In the last months of 2020, paddy rice prices are still in a downtrend, and authorities have “recorded the lowest palay rate in recent memory” at 10 pesos per kilogram in November 2020 (Ocampo, 2021), much lower than the price before the start of the pandemic. Paddy prices were so low in 2020 that Samahang Industriya ng Agrikultura/ Agriculture Industry Organization (Sinag) was compelled to appeal to the government for a 36-billion peso aid, warning that “the low prices of paddy rice means that our farmers will not be able to recoup their farm expenses during this cropping period, and may force them to stop planting palay for good” (Arcalas, 2020). An early January 2021 report remarked that “while paddy rice prices are beginning to climb, the rates are still below the ideal buying price set by the National Food Authority at P19 a kilo” (Ocampo, 2021). Low prices make it all the more difficult “to convince the youth and adults in the rural population to go into rice farming as income is not lucrative enough to convince them to continue farming (Palis, 2020).

One of the proposals was to reinstitute the sole authority of the National Food Authority to import rice and regulate imported rice entry into the domestic market, which the RTA removed. Should Congress decide to amend the RTA, NMFS and Arise said that the NFA’s authority to issue permits and licenses and conduct surveillance and monitoring of the domestic rice market should be “reinstituted.” This, as a simulation exercise done by the Philippine Institute for Development Studies, a government think-tank, showed that as early as 2015, the impact of Rice Tariffication showed that paddy prices would fall alongside the entry of imported rice. But, despite the decreasing farm gate price of rice, the consumers (end- users) does not enjoyed low price of rice but rather suffers, as the market price continues to increase.

Agricultural laws created and implemented are not the only factors that affect the farm gate price of paddy rice. The supply and distribution of rice where the linkages between each of the players in the chain, from the farmers, agents, rice miller, wholesaler to the retailer, the final distribution in the chain before the consumers, adding profit margins, which are shared among the intermediaries, as the rice move from one intermediary to another. The rice distribution chain begins at the level of the farm, which produces paddy rice of different varieties. To date, the databank of the Philippine Rice Research Institute (PhilRice) lists at least 80 certified varieties just for inbred varieties suitable for irrigated systems (www.pinoyrice.com).

Milled rice falls into four categories based on official statistics: (1) Rice Special – glutinous, aromatic and those with high nutritive quality (2) Rice Premium – rice with highest grade requirement according to PHILRICE standard (3) Well Milled Rice – rice kernel in which hull, germ and outer bran layers have been removed and (4) Regular Milled Rice (dti.gov.ph). Other ways of classifying rice are: branded rice in supermarkets and groceries; and ordinary rice in wet markets and retail shops (sari-sari). The former is sold in packs of varying sizes (1 to 50 kg), the latter in loose form (and transferred to plastic bags) or also in packs.

Middlemen in the Rice Distribution

Middlemen are the main players in the distribution system of a good, especially in the rice value chain. Middlemen are the individuals/institutions who specialize in performing various marketing functions involved in the purchase and sale of goods, as these move from producers to consumers. Middlemen bridge the link between the producing farmers and the consuming market. Rice agents, dealers, pre-harvest contractors, commission men, brokers, rice millers, wholesalers and retailers constitute the group of middlemen in the Philippines.

Mostly they operate in the markets and coordinate producers with consumers under different terms and conditions. In the Philippine distribution of rice, middlemen provide many services but their role is considered as exploitative. It is generally acknowledged that middlemen get very high margins and profit, though their share is generally justified by considering provision of additional services and risks, which they usually undertake at each stage in the distribution system (Odsinada et al., 2023).

Middlemen are held responsible for farmer’s low share in the consumer consumption and buying of rice, and are blamed for exploiting the farmers. Government is usually advised to reduce or minimize the role of middlemen from the marketing chain for increasing welfare of both the consumer and producer (Badar, 2008) Developing countries, like the Philippines, the agricultural supply chain, particularly the distribution of rice is often dominated by middlemen with substantial market power. Their high profit margins often distort the price of rice in the market by driving a wedge between the price paid to farmers and the price paid by final consumers. Middlemen have the capital to finance expenses in distribution from vehicles used in transporting paddy rice and milled rice to outright cash in buying harvested paddy rice direct from the farm.

Hayamia et al (2014) in his study alleges that rice marketing in the Philippines involves a network of middlemen working closely with rice cartels which control 90% of the country’s rice supply. In fact it is likely that large selling margins are perhaps due to proliferation of traders, leaving scale economies in trade unexploited. Tadem (2012) stated that it takes about 18 marketing agents (traders and millers) to process 90,000 tons of dry palay, compared to one miller in Thailand. Philippine Statistics Authority (PSA, 2019) data indicates a large price margins between farm gate and retail prices. Some agricultural and economic experts attribute this wide price spread to ineffectiveness along the Rice Distribution structure, which was characterized by high production of farm inputs and marketing costs, driving the domestic price above that of the world market (Ranjan, 2017).

In the last three years, economic stability had been challenged yet again due to the COVID-19 pandemic that has globally disrupted food supplies and continuously exert pressure and instability in the price of imported agricultural products and rice. The United States Department of Agriculture-Foreign Agricultural Services (2020) noted that Philippine rice farmers struggle to compete with affordable imports from Southeast Asia. The pandemic cripples the supply of food from one country to another, coupled with the ongoing war between Ukraine and Russia which disrupted the price of oil per barrel in the international market, causing a further increase in cost of farm inputs.

The present government administration, during the electoral campaigned had laid down a promise on the lowering of price of rice at Php 20/kilo in the market. Six months had passed since elected to the position as the president of the Philippines, still, the promise of low rice prices for consumers remains unrealized. In December 2022, President Marcos Jr, declared in his speech in Kadiwa ng Pasko Caraban “we’re getting closer to the price I dreamed of for rice, especially since we can now buy this for 25 pesos…. that will be sold quickly. I’m sure it will be the first to be sold out.” (Department of Agriculture, 2022). The president encouraged the program to become a national program, not just for the LGUs. However, it is the National Food Authority, the agency that is selling price for local, well-milled rice is at P25 per kilo, the Department of Agriculture’s Bantay Presyo pegs rice prices in Metro Manila at still P38-50 a kilo, depending on the type of rice. The NFA sells well-milled rice at the P25 per kilo rate to government institutions and wholesale authorized retail outlets.

The Kadiwa ng Pasko caravan is a project of the Office of the President and the DA, which Marcos concurrently heads. It is aimed at addressing rising inflation by providing locally sourced goods at lower prices not only during the holiday season but all throughout the year. “Kadiwa ng Pasko,” launched by the current Marcos administration, is a holiday farmers market that gives producers a platform to sell their wares in different areas around the country. The Kadiwa program is a revival of a project first implemented under the administration of the incumbent president’s father and namesake, the late dictator Ferdinand E. Marcos. Kadiwa was later recycled during the time of President Joseph Estrada, who was also deposed from office (Department of Agriculture, 2021).

Government agencies and wholesalers may purchase rice from the NFA at P25 per kilo. The NFA follows a “buy high, sell low” formula, where it purchases paddy rice from local farmers at a set support price, mills these to rice with the help of local millers, and sells the rice at a loss.

The study aims to determine the possibility of attaining the Php 20.00 per kilo price of milled rice in the market.

Objectives of the Study:

- To examine the nature and structure of the Supply Chain Distribution of Rice in Pampanga

- To determine the change in price in the whole Distribution of Rice in Pampanga.

- To determine the possibility of attaining the Php 20.00/kilo price of rice in the market.

METHODS

Research Design.

The study used a multiphase mixed methods approach in research, which is specifically designed for large-scale investigations that employ separate and equally emphasized qualitative and quantitative methodological frameworks (Halkias et al., 2022). The order of data collection and analysis was sequential and concurrent, and each phase builds on the previous thread culminating in a fuller understanding of the overall project objectives.

Quantitative analysis was used to describe the social and economic distribution of rice in the province. Qualitative analysis was used to analysed the mapping and distribution structure in Pampanga. Farm pre and post-harvest cost, including the administrative and marketing cost of the transfer of paddy to milled rice from one intermediary to another also serve as the basis for the creation of approximate cost and benefit of running a rice distribution or retailing business. The economic analysis of costs and returns looked at the profitability of producing, aggregating, processing, and distribution of rice from farm gate to market.

The rice farmers in the province of Pampanga, according to the Philippine Rice Industry Roadmap which was mandated by the rice trade liberalization law, the provinces in Region III were identified as high – priority provinces which have medium to high yield (above 3 metric tons per hectare) and their palay production costs are less than P16.84 per kilogram. This provinces are also the top producing rice in the Philippines.

The Methods section of a research paper is like a blueprint directing to the substance of the research, guiding the readers to understand how the study will be conducted.

Participants of the Study.

Primary data was gathered from different rice farmers as the main participants in the study, all from the province of Pampanga. A total of 10 farmers were interviewed from the province of Pampanga who are farming land from 1 to 2 hectares were interviewed on the cost of farm inputs from pre harvest to post harvest.

Judgement and snow ball sampling method was used in the study, were the participants in the study were selected according to the criteria set by the researchers; rice farmers in the province of Pampanga, farming not more than 3 hectares, have farming experience of not less than five years and owns the land they are farming. Agents, millers and wholesalers and retailers that makes up the distribution system of rice in the market were also interviewed. Agents were referrals by the rice farmers themselves, have been in the industry for at least three years. Millers and wholesalers were identified based from rice farmers’ referrals as well. Retailers were chosen randomly in the local market, have been in the retailing business for not less than five years. Secondary data from related literature, government and other agencies in agriculture and cooperatives were also interviewed for the needed data in the study.

Instrument

A self-formulated questionnaire validated by an English and Filipino professor and two experts from the Department of Agriculture Regional Office III including the research director of the said agency.

RESULTS AND DISCUSSIONS

Supply Chain Distribution Structure of Rice.

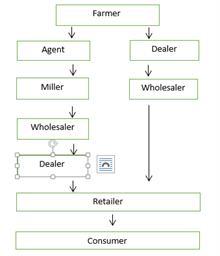

The rice distribution chain covered in this study, based from the qualitative interview of farmers in the province of Pampanga, is shown in Figure 2. A set of players along the supply chain are inter – connected through a chronological sequence from rice farmers, agents, millers, wholesaler, dealers, retailers’ to the consuming market.

An efficient distribution system means availability of quality inputs and outputs at desired place, at right time and in the suitable form which is not possible without strong infrastructure support, efficient transportation, processing, grading and storage facilities.

One source of market power lies in the fact that middlemen are also better informed about market conditions, especially the prices further down the supply chain. This raises the possibility that better access to market information can increase the prices that farmers receive from middlemen, thereby increasing their income and helping them to make better production decisions (Mitchell, 2011). A similar study conducted by Assoutoa et al. (2020), argues that the ability of farmers to use price information may be limited by the fact that they are tied in to relationships with particular middlemen and are dependent on them for credit. Since they do not have an option to trade with someone else if they are unhappy with the price they receive, being informed about the market price does not help them.

The rice distribution chain was dominated by the traditional multi -layered supply chain with many competing players in each segment from farmers to consumers and, oftentimes, with the engagement of agents in both paddy aggregation and rice distribution. The presence of multiple layers especially between farmers and millers, working as consolidators, commission agents, independent traders increases the cost of rice in the market. Millers may also procure directly from farmers or sell to retailers; likewise wholesalers can be simultaneously importers and/or retailers. Farmers who goes to the millers or “mini kono” to process their paddy rice are most often for household consumption.

Every after post-harvest of paddy rice, the Commission agents, usually performs the role of identifying who among the farmers are looking for buyers of their paddy rice. After identifying the willing seller of paddy rice, these agents make a call to all possible buyers of paddy rice: local millers; traders of paddy rice; large scale millers and dealers of paddy and milled rice; and other possible buyers. They are the one who make a contract with the farmers at the price approved by the buyers, these agents then received commission by performing this specific tasks.

Besides depending to the commission agents for supply of paddy rice, millers may also procure directly from farmers or in more common scenario, the farmers may directly sell their paddy rice to the millers, which the latter may sell the paddy rice to wholesaler and retailers. In addition, Farmers also goes to the millers or “mini kono” to process their paddy rice for household consumption.

Wholesalers can be simultaneously importers and/or retailers. These wholesalers have already established contact with various commission agents and local millers of different municipalities, that connects them to farmers. As wholesalers of paddy rice, they perform and pays for the cost of the following postharvest and distribution activities: milling paddy rice; bagging the rice into various kilograms and according to variety that suits its quality; transporting the now bagged and properly labelled rice; warehousing of the rice inventories; contacting with the retailers in the various municipalities and transporting the rice to their partnered retailers. While wholesalers have business dealings with retailers, they also have trading contact with dealer of rice, who has direct connection with retailers in faraway provinces.

Retailers are the closest to the consumer markets in the distribution channel of rice in the Country. They perform and bear the cost associated to buying and selling of rice to the end users, which includes: store merchandising techniques; inventory management; managing of receipts; customer service and other in-store related activities (Said, 2021). Pricing decision for rice by retailers also follows the quality categorization and pricing set by the dealers and wholesalers where they purchased the rice inventories

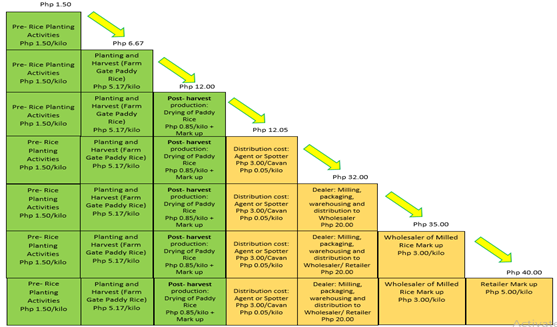

Agents or paddy traders are the first layer of players in the distribution and are often commissioned by millers and wholesalers in the area. They buy paddy direct from the farmers, most often right or during the harvest, and a Php 3.00 per cavan or roughly Php 0.05/kilo or Php 1.00/kilo and higher, is added to the farm gate price, depending on what are the activities performs by the traders in the distribution process. This traders or market players who are involve solely in paddy trading, i.e., collecting paddy for sale to large miller-traders who do not have the time to procure from scattered small farmers and their marketing activities involves trucking, handling, and storing (Mataia et al., 2020). There exists a strong relationship between farmers and this agent since they often provide credits to farmers both in cash and in the form of farm inputs like fertilizers and seedlings and interest for loans are much lowered than private lending and other informal lending entities. In exchange, farmers, specially the small farmers, sell their paddy produce directly to these market players.

Agent traders then sell paddy rice to rice mills. Rice millers process the paddy into milled rice, charges per kilo. From the mill, the rice goes to wholesalers, who may also obtain various types of milled rice from importers; rarely is rice imported in paddy form. Wholesalers then sell it to dealers who distributes and sell to retailers. The retailers which are often divided into traditional retail outlets were rice if sold in public and wet markets, or sometimes roadside stalls), as well as modern retail outlets lie supermarkets, hypermarkets, mom and pop stores and other retail chains. The latter are often pre-packed and sealed, whereas the former are often sold loose.

Figure No. 1 Rice Supply and Distribution Structure in Pampanga (common channels in the Philippines)

Agritech-GoNegosyo launch of the Masaganang Ani 300 to reward farmers who will harvest 300 sacks (15 tons) of palay per hectare. The program awards those who can attain the 15-ton production target should be rewarded, this cannot be immediately attained by more than 95 percent of the rice farmers. Because of the inadequate agriculture support services and low hybrid rice usage, rice farmers are not yet producing the minimum 4-ton-per-hectare yield necessary to survive the rice Tariffication law (Department of Agriculture, 2022).

The price data from the Philippine Statistics Authority (PSA, 2020) show large price margins between farm gate and retail prices. Some analysts attribute this wide price spread to inefficiencies along the Rice Value Chain which was characterized by high production and marketing costs, driving the domestic price above that of the world market. Other reason is the exorbitant mark up of prices set by the middlemen.

Change in Price of Rice in the Distribution Structure

The geographical and intermediary movement of paddy and milled rice explains the importance of supply areas and demand centers and the trading practices of middlemen. It also shows the change in price as one intermediary adds’ value to the supply or paddy and rice, and the magnitude of interisland and interregional movement, as well as the relationships between production – consumption characteristics of the different regions. However, the present study is limited to the province of Pampanga, and does not compare inter regional change in prices

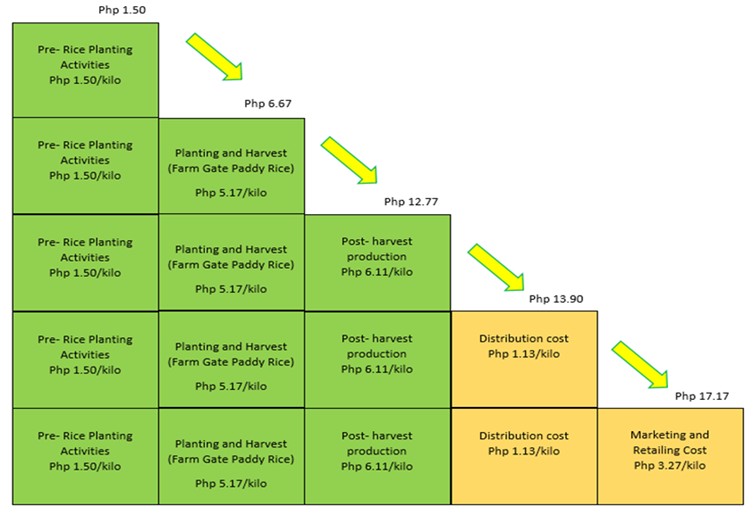

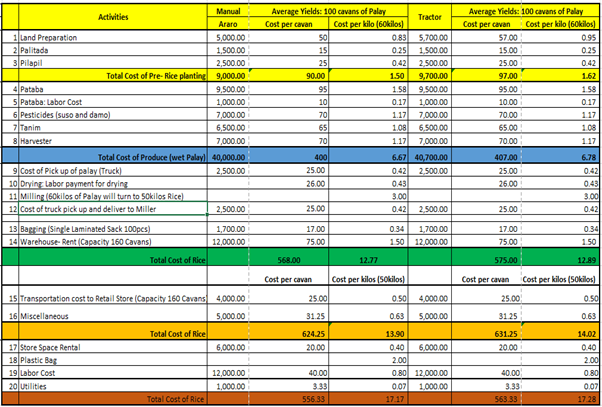

Cost of Farming from Land Preparation to Post Harvest. An approximate cost of the price of paddy rice from land preparation to harvest is given in Table No. 1. The table shows computation of manual cost and one using tractor. Farming activities of rice farmers from land preparation, to paddy rice maintenance, cost of fertilizer, cost of labour for post-harvest, milling, drying to transportation cost to retailer is computed. Farmgate price of paddy per kilo (manual) is Php 6.67 and Php 6.78 (tractor). Adding the cost of drying, milling, bagging and cost of storing, milled rice is Php 12.77 (manual) and Php 12.89 (tractor). Adding further the transportation and marketing cost, the estimated total cost of milled rice is Php 17.17 (manual) and Php17.28 (tractor), adding a mark-up for profit, the possible retail price of rice in the market could range from Php 20.00- 30.00/kilo, if the farmers will solely produce and be the one who will distribute the milled rice in the market. This is a hypothetical flawless distribution scenario where the presence of too many intermediaries between farm gate price to market are not participating in the distribution structure.

The table also shows the cost of milled rice per kilo at the market or nearest millers. Identification of all expenses in the rice production, from land preparation to post harvest, is very important since these data are among the highly requested information from major users such as policy analysts, national accounts compilers, farmers and other entrepreneurs in the agricultural sector. For paddy rice farmers, the production costs and returns data can serve as basis for the improvement of their efficiency and profitability.

The study revealed that still, more than 50% of the farmers in the region are still using manual transplanting “tanim punla” (about 25 man days) and harvesting and threshing (about 20 man days) which, according to PhilRice & IRRI (2019) contributes to high production cost due to high labor requirement in farm pre – production.

Few farmers uses the trans-planter, which they rent from cooperatives and local agriculture agency. Some trans planter equipment were donated by the Department of Agriculture, lessens the number of man days required to plant rice seeds in the field, which in turn lessens the cost of production of palay. The highest variable cost/ha are those areas with the highest production cost/ha. are seed, land preparation, transplanting, fertilizer, weed control and pest control. Actual figures of cost and relative rankings may vary across regions in the country. According to the Philippine Rice Industry Roadmap which was mandated by the rice trade liberalization law, the provinces in Region III were identified as high – priority provinces which have medium to high yield (above 3 metric tons per hectare) and their palay production costs are less than P16.84 per kilogram, and can be seen in the table the cost is Php12.77 and Php12.89 for manual and tractor respectively. With this data, rice farmers in the region could realize their approximate additional income if they would engage in the rice distribution business.

Cost and returns analysis of paddy production

Figure no. 3 shows the change in price of rice as it moves from farm gate to different types of intermediaries in the structure. Agents or paddy traders add a Php 3.00 to 7.00 per kilo to the farm gate price, this cost covers drying, handling, trucking and storing of paddy. Sun drying, is the process of drying threshed paddy. The process is normally less than artificial drying and no special skills required, agents have access to artificial drying for they have transport to bring the wet threshed paddy to this facility. Normal profit of agents or paddy traders’ rangers from Php1.00 to Php3.00 kilo.

Rice milling is one of the post – harvest activities in rice farming where in mechanical milling machines are operated at milling facilities. Rice milling is the removal or separation of the husk (dehusking) and the bran (polishing) to produce the edible portion (endosperm) for consumption. Actual milling process, however, removes also the germ and a portion of the endosperm as broken or powdery materials reducing the quantity of grains recovered in the process. The extent of losses on the edible portion of the grain during milling depends on so many factors as variety of paddy, condition of paddy during milling, degree of milling required, the kind of rice mill used, the operators, insect infestation and others. Millers charge Php 2.50 – 3.00 per kilo of paddy rice milled to rice milling facilities. Those who are members of cooperatives with mechanical milling machines charge their members P0.25 to P0.50 lower than non – members.

Miller traders or Wholesalers perform various function in the rice distribution. Two options could happen, wholesalers could either buy the milled rice from agents or paddy traders or buy them as paddy rice and do the milling. This wholesalers have the fast milling equipment, have big storages or warehouses that could accommodate paddy rice and milled rice. Pampanga millers are often underutilize due to low volume supply of paddy rice, unlike Bulacan and Nueva Ecija were most millers have the new technology that could mill paddy rice at 2 tons per hour (Mataia, 2020). However, Beltran et al (2018) stated that most millers in the Philippines are underutilize as they do not operate at full capacity of 8hr/day during normal season and 16hrs/day during peak season.

It is thru the wholesalers of paddy rice where the bulk of cost is incurred. An average of Php 20.00/kg of milled rice is added as this constitute the cost of milling, handling, labour, storage and working capital. Transportation, administrative cost and other marketing costs like packaging were also included in the added cost.

The milled rice, would sometimes flow to the wholesalers of rice, who then adds P3.00/kilo of rice and delivers the goods to market retailers. Retailers are the final intermediary in the rice distribution structure. An average of Php3.00 to Php5.00 per kilo of milled rice is added when sold per kilo, while Php100.00 is added when retailed per half cavan.

Based from this cost analysis, if farmers choose to sell their produce at Php 20.00 kilo, the mark up is equal to Php 2.83 kilo (manual) Php 2.72 (tractor), giving the farmers an estimated profit of Php 8,490.00 (manual) and Php 8, 160.00 for one hectare of land in one cropping (3months: P 2,830.00/mo.; P2,720.00/mo.). This estimated amount of profit falls under the income range of Filipino families living under poverty threshold. Thus, satisfying the call for Php 20.00/kilo of rice, will further sink the Rice farmers’ family into the pit of poverty. The Php20.00 per kilo promised by the present administration is far off and quite unrealistic. NFA distributed rice particularly in the National Capita Region sold imported medium class milled rice for Php25.00 per kilo. However, this was done with the principle of “buy high and sell low” and is only distributed in smaller areas.

While, increasing the mark up and selling the rice for Php 35.00 kilo, the estimated profit is total to Php 53, 490.00 and Php 53, 160.00 for manual and tractor method as follows. In addition, the P 35.00/ kilo of rice in the market is 13% lower than the Php 40.00 average prevailing price of rice in the market with the different level of intermediaries at the center of rice distribution.

Figure No. 3 Farm to market cost of Rice product with Farmers taking the role of producers and sellers to the retail market (end users)

Figure No. 4 Farm to market cost of Rice product with Farmers taking the role of producers selling to intermediaries

Table No. 1 Cost of Pre and Post production of paddy rice

The implementation of the Rice Tariffication Law or R.A. No. 11203 paved way for the proliferation of imported rice from our neighbouring countries. The excessive rice importation from private companies that sell this at a much lower price than local milled rice made it difficult for the local farmers to compete.

The continuous rise in prices of land preparation and other farm inputs that are mostly imported and vulnerable to external changes like the peso devaluation, the low yield in production of paddy rice, the high cost of transportation from farm to market, the presence and exploitation of farmers by middlemen who often dictate farm gate prices per kilo of paddy rice, resulted to high retail price of rice in the market. The decrease of the farm gate price of paddy rice by almost 20% proves the thinning income of farmers while the middlemen enjoy the bulk of the profit, at the same time, rice consumers are not benefiting from the decline in the price per kilo of the paddy rice since the retail price of rice in the market drop by only 10% or even remains the same.

Based from the change in price between intermediaries in the rice distribution, the promised of Php 20.00 per kilo by the present administration remains unrealistic and impossible to attain, thus, the Php 20.00 per kilo retail price of rice was used as a political propaganda during the election campaign of the present government.

RECOMMENDATIONS

Government through the agriculture agency, Department of Agriculture and local counterpart, should encourage the concept of direct marketing by facilitating the farmers and arranging farmer’s market enabling them to become dealers and/or retailers and come into direct contact with consumers and receive payment directly from consumers. Direct marketing will reduce distribution cost by making the distribution channel shorter, thereby minimising the number of middle players adding cost in the price of rice, but not value.

Provide suitable sustenance in farming production like stabilization of the price of inputs (fertilizers, seeds, pesticides, etc) to lessen the cost of paddy farm gate price.

Maximise the usage of millers located in different local municipalities and barangays to lower down the cost of milling per kilo.

The policy measures that can be obtained from the output of the study should look into ways in lowering the change in the price of rice from farm gate to market. While reforms on the change in price are necessary, it needs to be carried out carefully, starting with changes in imported farm inputs like fertilizers.

Revisions of some of the provisions stated in the Rice Tarrification Law, like placing a limit on the allowable tons of rice importation from other countries.

Other policy measures that may have positive longer-term consequences include productivity improvement through a vigorous program of intensified use of high-yielding rice varieties, irrigation, better and rehabilitation of agricultural transportation from farm-to-market roads, and measures to encourage the growth of other non-rice crops.

A policy towards Farmers entrance to the Rice Supply Chain

While market reform is generally necessary, it has to be carried out carefully, especially if implemented on a critical commodity such as rice. Although market reforms in rice can potentially have favorable effects on consumer prices in general, some household groups may be adversely affected by the expected surge in rice imports. Policy measures may have to be designed to counter these effects. Among the various poverty offsetting measures experimented with in the paper, the results indicate that an increase in direct government transfers to the adversely affected household groups provides a better safety net. However, this is more of a short-run policy measure.

Research findings, reveals that even with the increasing cost of farm inputs and post-harvest activities, farmers have no say nor they cannot impose/ dictate the farm gate price of milled rice. Farmers are not receiving high economic returns from farming, given the high market price of rice, who gains more and how can prices be decreased while protecting the rice farmers’ income. According to the rice farmers, in most cases, the spotter/agents, already has a set price in mind, giving little to no space for rice farmers to negotiate. Because of the need to collect immediate cash to pay off several loans, most farmers have no choice but to give in to the brought by the agent/ spotter that represent the large scale wholesalers/millers. This scenario clearly shows the reality that rice farmers have little to zero participation in the rice distribution. And that the rice supply chain is inter connected through a chronological sequence from rice farmers, agents, millers, wholesaler, dealers, retailers to the consuming market (Twano, et.al, 2019).

Assuming a hypothetical flawless distribution scenario where the presence of too many intermediaries between farm gate price to market are not participating in the distribution structure, and the farmers assumes the role of producers and retailers of milled rice, the approximate possible retail price of rice in the market could range from Php 20.00- 30.00/kilo. This is lower than the Php 38-40.00/kilo, average market price of rice. Consumers will enjoy lower price of rice, and at the same time, rice farmers will enjoy higher economic benefits in rice farming activities.

The aforementioned points, establish the significance of the issues of: farmers’ low participation in the Rice supply chain; the high cost of pre and post production of rice; and high retail price of rice.

Policy options:

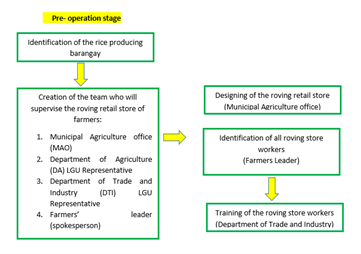

A. Farmers’ roving retail store

Farmers Roving Retail store, is a policy strategy that will enables the farmers to sell their produce rice products directly to consumers from nearby towns, municipality and City. This project will be funded by the local government unit, and spearheaded by Municipal Agriculture Unit, together with the local representative from the department of agriculture and department of trade and industry. Through this venture, farmers will gain higher return from their farm outputs and provide the households much lower price of rice products.

The Municipal Agriculture Unit with the approval of the Municipal Mayor’s, will coordinate with the other Municipalities, with regards to the schedule permit of the roving retail store in the public market of their jurisdiction.

Prior to the start of the roving stores operations, farmers will select among themselves or from their family members, the person who will be working in the roving store. Each worker in the roving store will undergoes retail business training under the department of trade and industry.

B. “Retail Stores” Fixed Commercial space for Farmers in every Municipality’s public market

The fixed Retail store (commercial space) for farmers will used by rice farmers in retailing their produce goods. The DA- LGU representative will coordinates with the farmers’ leader regarding the schedule of retail stores, and ensuring that farmers will be given the opportunity to retail their products. The DA- LGU representative will coordinates the schedule with the MAO and supervisor of the LGU public market. Once the scheduled are deemed final, the farmers’ leader will disseminate the schedule to all participating farmers.

Prior to the launching of the “Farmers’ Retail Store”, the DTI- LGU representative will organized a series of training workshop for farmers or their family members who will be in charge in the retailing and merchandising activities. This is to ensure they are equipping with necessary knowledge and competencies in retailing and merchandising.

REFERENCES

- Arcalas, J. Y. (2020, October 12). Drop in palay price prompts group to seek P36-billion aid for farmers. BusinessMirror.https://businessmirror.com.ph/2020/10/12/drop-inpalay-price-prompts-group- to-seek-p36-billion-aidfor-farmers/

- Beltran, J.C, F.H. Bordey, P.F. Moya, et al., (2016). Rice Prices and Marketing Margins. In F.H. Bordey, P.F. Moya, J.C. Beltran, and D.C. Dawe (eds.), Competitiveness of Philippine Rice in Asia. Science City of Muñoz (Philippines): Philippine Rice Research Institute and Manila (Philippines): International Rice Research Institute, 55–73.

- Bordey, F.H., P.F. Moya, J.C. Beltran, D.C. Dawe, (2018). Competitiveness of Philippine Rice in Asia. Science City of Muñoz (Philippines): Philippine Rice Research Institute and Manila (Philippines): International Rice Research Institute. Casinillo, L. F. (2020). Econometric modelling on satisfaction in rice farming under philippine rice tariffication law. Journal of Research and Multidisciplinary, 3(2), 326-336.

- Cororaton, C.B & Yu, KD S. (2019). Assessing the Poverty and Distributional Impact of Alternative Rice Policies in the Philippines. DLSU Business & Economics Review 28, pp. 169–182.

- Halkias, Daphne, Neubert, Michael, Thurman, Paul W. and Harkiolakis, Nicholas (2022). The Multiple Case Study Design Methodology and Application for Management Education 1st Edition. ISBN 9781032156088, Published February 28, 2022 by Routledge

- Hayamia, Y., Kikuchib, M. and Marcianoc, E. (2014). Middlemen and peasants in rice marketing in the Philippines House of Representatives. (2019). An Act liberalizing the importation, exportation, and trading of rice, lifting for the purpose the quantitative import restriction on rice, and for other purposes. http://www.congress.gov.ph/legisdocs/ra_17/RA11203.pdf. Accessed: April 14, 2019

- Mataia, Alice B., Beltan, Jesusa C., Manalili, Beltran, Rowena G., Catudan, Betzaida M., Francisco, Nefriend M. and Flores, Adrielle C. (2020). Rice Value Chain Analysis in the

- Philippines: Value Addition, Constraints, and Upgrading Strategies. Asian Journal of Agriculture and Development Volume 17 | Number 2

- Mitchell, P.L. and Shennhy, J.E. (2011). Supercharging rice photosynthesis to increase yield. New Phytologist 171, 68-693

- Ocampo, K. R. (2021, January 4). Palay farm gate prices improving, average rate hits 8-week high. INQUIRER.net. https://business.inquirer.net/315146/palay-farmgate-prices-improving- average-rate-hits-8-week-high

- PhilRice (2016). PhilRice – IRRI study to boost PH rice competitiveness, News, Features & Broadcast Releases. Retrieved from www.philrice.gov.ph/philrice-irri-study-boost- ph- rice-competitiveness

- Rebualos, J. V., Vistal, J. P., Sato, S. M. B., Cano, J. C., Camino, J. R., and Dagohoy, R. (2021).

- Rice Tariffication Law through the Lens of the Farmers: A Case in the Municipality of Carmen. International Journal of Research and Innovation in Social Science (IJRISS), 5(8), 2454-6186. Rice Tariffication Law of 2019, Rep. Act No. 11203 (Feb.14, 2009) (Phil.), https://www.officialgazette.gov.ph/downloads/2019/02feb/20190214-RA-11203-RRD.pdf

- Simeon, (2019). Department of Agriculture will not ask for higher allocation in 2019, http://businessmirror.com.ph/2018/01/16/2-millionfarmers-to-get-free-crop-insurance

- Tadem, T., 2002. NGOs Organizing Cooperatives: The Philippine Case. In: Asian Review 2002, Vol. 15: Popular Movements. Institute of Asian Studies, Chulalongkorn University, Bangkok. pp. 62-77.

- Yao, R., G. Shively, and W. Masters, 2007. How Successful are Government Interventions in Food Markets? Insights from the Philippine Rice Market. Philippine Journal of Development, 62 v. 34 (1), 35-59.