Promoting Good Corporate Governance in Local Authorities through Dimensions of Internal Audit. A Case Study of Harare, Bulawayo, and Mutare City Councils

- Loice Magweba

- Josphat Nyoni

- Martin Dandira

- Efigenia Semente

- Davy Julian du Plessis

- 1-13

- Jun 27, 2024

- Corporate Governance

Promoting Good Corporate Governance in Local Authorities through Dimensions of Internal Audit. A Case Study of Harare, Bulawayo, and Mutare City Councils

Loice Magweba1, Josphat Nyoni1, Martin Dandira2, Efigenia Semente2, Davy Julian du Plessis2

1Women’s University in Africa

2Namibia University of Science and Technology

DOI: https://doi.org/10.51244/IJRSI.2024.1106001

Received: 19 April 2024; Revised: 13 May 2024; Accepted: 17 May 2024; Published: 27 June 2024

ABSTRACT

The aim of this study was to create an accounting-auditing framework that supports good corporate governance in local authorities in Zimbabwe. The study was driven by the low corporate governance index in all Zimbabwean local administrations. Low index contributed to inadequate service delivery in all Zimbabwean authorities. Existing literature shows that some elements of the internal audit may be used to enhance corporate governance in local authorities. It was against this background that this study sought to determine the extent to which some elements of the internal audit may be used to promote corporate governance. Pragmatism research philosophy guided the study. Due to this philosophy, mixed research design was used. The study examined the relationship between internal auditing pillars and corporate governance in local authorities using an explanatory research design. Data was gathered from internal auditing members at three local government and Accounting Association of Zimbabwe members A probability and non-probability sampling strategies were utilized to create 250 participants. The quantitative data was analysed using regression, and correlation. Qualitative data was analysed using the thematic approach. The study found that internal auditing dimensions, including audit committee, audit quality, and consulting role of internal audit, are crucial for the promotion of good corporate governance in local authorities. The study revealed that increasing the scope of internal audit to include three dimensions is crucial for building strong corporate practices in local authorities. The study found that improving the effectiveness of the three internal audit dimensions involves focusing on moderating factors such as audit committee independence, accounting experience/professional capacities, size of the audit committee, funding of internal auditing processes, internal audit staff competences, and stakeholder engagement. The study found that the three internal audit dimensions and six moderating factors can serve as a framework for local authorities to enhance good corporate governance. To promote excellent corporate governance, local authorities should adapt and expand their internal auditing operations and procedures to effectively develop and use the three dimensions and moderating elements in enhancing good corporate governance in addition to their traditional finance controlling mandate. The study suggests that local authorities adopt the presented framework which focuses on three pillars and 6 moderating variables. Future research may examine the framework’s effectiveness in other local authorities not included in this study.

Key words: Corporate governance, internal audit, dimensions of internal audit, local authorities

INTRODUCTION

Good corporate governance has remained an important area of study among scholars, because of its significant contribution to the financial stability, growth and success of organisations. Corporate Governance is now a key pillar of success for organisation, churches, universities and governments across the globe. Because of its emphasis on accountability and responsibility, corporate governance has helped organisations to remain operational, competitive and successful. This means that any research on the concept of corporate governance is therefore critical given the value of the concept to organisations. Locally, service delivery in almost all our local authorities has collapsed and this has affected the welfare of citizens as well as putting pressure on the central Government. Poor corporate governance has been cited as a key contributor to poor service delivery (Al-Ajmi 2009).. This provides the basis of this paper which seeks to develop an internal audit-oriented framework that promotes good corporate governance in the context of local authorities in developing countries.

LITERATURE REVIEW

The public’s understanding of corporate governance issues has increased significantly since the beginning of the new century as a result of a series of firm failures such as Enron, WorldCom, RBS, Northern Rock; Oceanic Bank, and Intercontinental Bank. The worldwide economic crisis that began in 2007 greatly affected corporate governance processes and regulations (Al-Ajmi. 2009). Due to these alterations in the corporate realm, investors are now more engaged than ever. Consequently, there is an increasing demand for rigorous rules that control the operations of businesses. The purpose of this measure is to ensure the prevention of wastage, fraudulent activities, and misuse of funds, while simultaneously ensuring that investors receive a justifiable return on their investments (Millstein, 2012).

Moreover, there was a call for substantial modifications to the responsibilities and obligations of executives, independent auditors, and corporate oversight in response to the widespread accounting scandals and the alarming number of false financial statements. Moreover, the prevalent failure in financial reporting has been predominantly attributed to insufficient internal controls (Bekiaris, Efthymiou and Koutoupis, A.G 2013). Subsequently, internal auditing has received exceptional attention and importance. Due to these corporate disasters, organizations are now required by corporate governance standards to disclose information about the dependability of their internal control system.

Historically, internal auditing has been viewed as a watchdog or “policeman” (Morgan, 1979), playing an important role in organizational control and expected to perform efficiently to help the firm achieve its major goals. A recent examination of internal auditing proved its ability to add significant value to a company (Bekiaris, Efthymiou and Koutoupis 2013). The financial crises heightened worries about corporate governance since there appeared to be accountability issues that worried people around the world. The debate about governance reforms has primarily focused on internal auditing procedures aimed at promoting accountability. In response to external calls for assurance on corporate governance processes, boards are increasingly relying on internal auditors, who are often knowledgeable about internal controls but are not well regarded within the organization (Broni and Velentzas 2012). Thus, Turnbull’s internal control plan has provided an opportunity to demonstrate competency in critical areas of risk management. Internal auditing is an important control method for both public and private companies. A firm uses control mechanisms to achieve its goals, which are systems that monitor, direct, encourage, or limit the behavior of employees (Drogalas Pantelidis, Vouroutzidou and Kesisi 2011). According to Drogalas , Alampourtsidis and Koutoupis (2014). internal auditing is critical to corporate and organizational financial disclosure. Internal auditors play a critical role in monitoring a firm’s risk profile and identifying techniques for improving risk management.

(a) The Relationship Between Internal Audit and Good Corporate Governance

Internal control and auditing are critical components of effective corporate governance; this assumption is endorsed by practically all ethical standards in this industry. Gstraunthaler, (2010). considers this interaction to be an integral component of the stewardship model of corporate governance. The link between internal auditing, financial reporting, and business governance has been the subject of controversy, as indicated by the Cohen Report on auditor obligations and the Treadway Report on deceptive reporting.

As indicated by the implementation of new corporate governance standards, such as the United Kingdom’s integrated code (2006), Gstraunthaler (2010). claims that the concept of “the audit explosion” has prompted a revolution in entity regulation.

According to Regoliosi and d’Eri (2012) for this strategy to be successful, the organization’s internal operations and internal control system (ICS) must be reconceptualized as a possible regulatory milieu.

As a result, the researcher has identified a significant worry and subject for additional investigation: the concept of internal auditing in connection with corporate governance. Internal auditing has seen a significant resurgence and shift in emphasis on a worldwide scale. Organizations are beginning to recognize the value of internal audits in improving reporting and corporate governance by mitigating the risks associated with non-financial disclosures (Regoliosi and d’Eri (2012)

Internal auditing has gained importance in light of the increased emphasis on risk management and the board of directors’ responsibilities to verify that management’s strategic planning is consistent with the organization’s risk tolerance. The internal auditor is responsible for risk oversight and surveillance on behalf of the audit committee, board of directors, or management. According to the IIA, internal auditors play an important role in company governance. In recent years, the relationship between internal auditing and corporate governance has grown significantly. Internal control and auditing have become more important as a result of societal and auditor-specific norms and standards governing the auditing process. Internal audits are emphasized as a risk management strategy in corporate governance legislation. (Robertso, Diyab and Al-Kahtani 2013).

Management and the audit committee are directly responsible for establishing and supervising the organization’s internal control architecture. The internal audit function (IAF) is used to meet the governance duty. As a result, among the six key components of internal audit functions and dimensions may be used to promote good corporate governance in local authorities

(b) Internal Audit Quality and the Promotion of Good Corporate Governance

Scholars have extensively studied the efficacy of internal audits and the necessity for a clear and specific definition of “Internal Audit Quality.” Due to its intangible nature, assessing the quality of internal auditing and determining its worth to a company is challenging (Regoliosi & d’Eri, 2012). It is crucial to examine the many aspects of internal audit quality due to the advisory function and the impact it has on corporate governance. According to Gstraunthaler (2010), the internal audit activity consists of two components, which together determine the quality of the audit. The initial task of an auditor is to identify irregularities in a company’s financial records. Subsequently, the auditor will document these inconsistencies throughout the subsequent step. Audit quality is determined by the internal auditor’s skill, the scope of the audit, and the level of auditor independence. For accurate disclosure of audit results, it is crucial to take these factors into mind (Karagiorgos Drogalas, Gotzamanis and Tampakoudis 2010). According to Karagiorgos et al (2010) the quality of audits is linked to the level of skill that auditors have in internal auditing. Audit quality, as defined by Palmrose (1988), refers to the likelihood that financial statements will be free from any irregularities after the audit is finished. Adhering to well-recognized accounting and auditing principles is a key factor in determining the quality of an audit. Stakeholders and shareholders consider it important to measure the satisfaction of auditees and the effectiveness of internal controls (Karagiorgos et al 2010).

Various elements that impact the quality of audits have been the focus of several efforts to identify and assess them. Regoliosi. and d’Eri A. (2012) discovered that twelve distinct factors influence the quality of audits. The key elements that hold the most significance include firm size, audit team composition, compliance with accounting standards, involvement of the audit committee, personal accountability of the auditor, support from executives, and alignment with organizational requirements.

According to Regoliosi and d’Eri (2012) financial managers perceive eleven criteria as the factors that determine the quality of an audit. Al-Ajmi (2009) identifies several key aspects that influence this determination, including auditors’ adherence to ethical principles, their level of expertise, their salary, their technical skills, the dynamics among team members, the frequency and punctuality of audit team meetings, and the effectiveness of communication within the team. Regoliosi and d’Eri conducted a study in 2012 where they identified the crucial criteria that lead to success for internal audit departments. The effectiveness of the internal audit function is influenced by both the hierarchical position of the internal auditor inside the organization and their level of independence. Furthermore, to guarantee the efficiency of the internal audit function, the department requires professionals who possess extensive expertise and proficiency to evaluate audit techniques. The ratio of auditors to total people has a considerable impact on the quality of an organization’s internal audits (Sarens and Abdolmohammadi, 2011). Based on these factors it can be inferred that;

H11: The Corporate Governance is positively influenced by the Internal Audit Quality.

H12: The impact of Internal Audit Quality on corporate governance is moderated by three factors (competencies, the expertise, and Funding)

(c) Audit Committee and the Promotion of Good Corporate Governance

Recently, there has been a significant focus in the business sector on the importance of establishing a corporate governance framework, such as an audit committee, to strengthen and uphold internal control. Every publicly traded corporation in the Eurozone is mandated to have an audit committee. The enactment of the Sarbanes-Oxley Act in 2002 brought about significant changes to the structure and operation of internal control systems, thereby impacting the formation and structure of audit committees. This act functioned as a model for public sector organizations in the United States. The establishment of German audit committees was suggested by the Baum and Codex commissions in 2001 and 2002, respectively. Given the information presented, it is crucial to emphasize that the duties of audit committees in the United States, Germany, and the United Kingdom are remarkably similar.

The audit committee has authority over decisions that can either enhance or diminish the organization’s value. This category encompasses the following decisions: (a) supervising the processes of financial reporting and disclosure; (b) supervising the norms and principles of accounting; and (c) supervising compliance and ethics concerning regulations. Furthermore, the audit committee must make the following decisions. Decisions that enhance the fidelity of the reported financial statements to better reflect management’s choices and compel managers to align more closely with shareholders’ interests; Decisions that influence the dependability and precision of the financial statements, enabling shareholders to make more confident evaluations of the company’s value. Decisions that mitigate the likelihood of regulatory penalties or sanctions by ensuring the firm strictly adheres to legislation or norms of good business conduct. Consequently, the audit committee is in a favourable position to contribute positively to the establishment and implementation of effective corporate governance in organizations. The study aims to address the following essential questions.

The main function of the audit committee is to support the board of directors in areas of governance, including financial reporting. The audit committee’s primary responsibility is to facilitate communication and cooperation between the board of directors and the external auditors. Furthermore, it is imperative to guarantee that the external auditors uphold their autonomy throughout the audit procedure. In addition, the audit committee is tasked with enhancing the precision of financial disclosure and guaranteeing transparency in financial reporting. The primary goal is to strengthen the influence of external directors by improving the relationship and communication between external directors, corporate directors, managers, and auditors (Suyono and Hariyanto 2012).)

The primary duty of the audit committee is to guide the board of directors regarding financial reporting and other matters related to governance. The audit committee has the responsibility of promoting communication and collaboration between the board of directors and the independent auditors of the company. In addition, it is imperative to ensure that the external auditors remain impartial during their examination. Furthermore, the audit committee is responsible for ensuring the transparency of financial reporting and the accuracy of financial disclosures. The ultimate objective is to enhance the rapport and improve the communication between auditors, corporate directors, managers, and external directors, hence augmenting the influence of the external directors (Green, 1994)

Audit committees in both the public and commercial sectors are facing increasing pressure to enhance their transparency and accountability. Effective corporate governance entails making informed decisions, ensuring accountability for the management and oversight of resources, and efficiently utilizing these resources to produce high-quality public services and create favorable outcomes for individuals. The significance of an autonomous audit committee’s ineffective company governance is well-recognized globally. Given the increasing need for public sector accountability, audit committees play a crucial role in the governance structure of local authorities. Their primary function is to advise the Council on matters related to audits, risk management, internal controls, and financial reporting. This information is being offered as part of a comprehensive assessment of the local authority’s control environment and governance procedures. Decisions that impact the precision and reliability of the financial records, allowing shareholders to make more confident assessments of the company’s value; decisions that align management with shareholders’ interests.

Given this, it can be inferred that:

H21: Corporate Governance is positively influenced by the nature and quality of the Audit Committee.

H22: The relationship between the audit committee and corporate governance if moderated by some factors.

(d) The Consulting Role of Internal Audit and its Influence on the Development of Good Corporate Governance

Several organizational changes have taken place within Internal Audit in the last several years. There have been major shifts as a result of technological developments, the economic crisis, new requirements for internal audit, and the need for more comprehensive and continuous auditing by businesses. Bekiaris et al. (2013) found that these changes have an impact on the internal audit process, as well as on the roles of internal auditors and the overall scope of internal audit. To help internal auditors, the Institute of Internal Auditors performed an extensive review of internal audit in 2004 to determine its meaning, importance, and goals. In contrast to the widely believed notion that internal auditors are primarily concerned with financial control activities, the updated definition emphasizes a holistic and strategic approach. This fresh method brings internal audit in line with strategic management by showcasing its consulting role.

According to Bou-Raad (2000), internal audits have a critical obligation to provide management with appropriate information about corporate governance issues. Internal audits are primarily concerned with overseeing and engaging with a company’s internal control measures. The company’s advising services help to develop a strong corporate governance structure and improve the company’s overall performance. It separates itself from other corporate activities in the same way that an intangible asset does. In summary, the new strategy clearly shows that the internal audit is moving its focus from financial to managerial issues. One new trend stemming from recent changes is the use of the internal audit process to improve the firm’s risk management practices through intensive consultations. According to Lindow and Race (2002), internal audits prioritize the organization’s aspirations and objectives over transactions and regulatory compliance.

One conclusion indicates that internal audit has shifted towards a more management-focused approach compared to previous years. This notion asserts that internal audit, through the provision of assurance and advisory services, can enhance effective corporate governance, hence promoting management competence and attracting new investors for smaller organizations.

Drogalas et al. (2014) conducted a recent assessment of the public sector in Greece, specifically focusing on the deployment of internal audit in Greek Police departments and the benefits it brings to this public organization. The findings generally demonstrated that the adoption of internal control effectively oversees the actions of the business, safeguards its assets, prevents fraudulent behaviour, identifies and rectifies errors, and ensures the correctness of financial statements. Furthermore, it is emphasized that there is a necessity to revise the internal audit structure in Greek public organizations and enforce more precise standards.

According to the above, the first research hypothesis can be developed as follows:

H31: Corporate Governance is positively associated with the consulting role of Internal Audit.

H:32 The relationship between corporate governance and consulting role is moderated by factors such as management approaches, and stakeholder engagement.

A total of six hypothesize were developed from the review of the literature

H11: The Corporate Governance is positively influenced by the Internal Audit Quality.

H12: The impact of Internal Audit Quality on corporate governance is moderated by the nature of controls, level of compliance and

H21: Corporate Governance is positively influenced by the nature and quality of the Audit Committee.

H22: The relationship between the audit committee and corporate governance is moderated by three factors (Independence, Accounting Professional training, and Size of the committee)

H31: Corporate Governance is positively associated with the consulting role of Internal Audit.

H32: The relationship between corporate governance and consulting role is moderated by factors (management approaches, stakeholder engagement)

METHODOLOGY

A structured instrument was used to collect data from 230 participants drawn from three local authorities and other accounting associations. Interviews were also conducted to generate additional information.

Quantitative data analysis was done through regression analysis while the qualitative data was analyzed using the thematic approach.

Multiple regression analysis was performed to estimate the magnitude of the effect of the “Consulting role of Internal Audit”, “Internal Audit Quality” and the Audit Committee” on “Corporate Governance”. The Ordinary least squares (OLS) regression model was:

CG = a + b1 ConIA + b2 IAQ + b3 AC + ei

The variables are defined below:

| CG | = Corporate Governance |

| ConIA | = Consulting role of Internal Audit |

| IAQ | = Internal Audit Quality |

| AC | = Audit Committee Quality |

The main hypothesis is that there is no statistically significant impact of the internal audit on corporate governance in the local authorities used in the study. To test this hypothesis, multiple regression and simultaneous input were used. Data was tested for normality before regression analysis.

The direct relationship between the three dimensions and corporate governance excluded the constructs b1, b2, and b3

The moderated analysis included the construct factors and the regression was run based on the regression equation given below. The results of the direct relationship were compared with the regression result with moderating factors b1, b2, b3

CG = a + b1 ConIA + b2 IAQ + b3 AC + ei

The hypothesis tested in the study

Table 1: Results of hypotheses test

| Hypothesized path | Relationship | Standardized coefficient Beta | t- values | p-values | Comment |

| Positive | 0.25 | 7.4 | 0.000 | Supported | |

| Audit committee corporate governance (without moderation factor) | 0.45 | ||||

| Audit committee > moderating factors > corporate governance-b1 | Positive | 0.47 | 8.8 | 0.000 | Supported |

| Audit quality corporate governance (without moderation factor) | 0.33 | ||||

| Audit quality > moderating factors > corporate governace-b2 | 0.40 | 11.2 | 0.000 | Supported | |

| consulting role of Internal Audit > corporate governace (without moderation factor) | 0.01 | 0.000 | supported | ||

| Consulting role of Internal Audit > moderating factors > corporate governace-b3 | Positive | 0.11 | 9.7 | 0.000 | Supported |

Table 1 Summary the of the direct relationships and the moderated effect moderating factors

(a) Audit committee, corporate governance, and moderating factors.

Each of the three audit committee characteristics—committee size, independence level, and professional training and certifications—modified the association between audit committee corporate governance, as shown in Table 1. As seen by the beta value of 0.47 in comparison to the control group’s beta value of 0.45, the audit committee’s influence on corporate governance grew. This demonstrates that a larger audit committee, one with a high level of independence, and one whose members have extensive professional training and experience is better able to promote good corporate governance. A bigger audit committee is thought to be more successful in enhancing corporate performance, according to the resource dependence theory (Pearce & Zahra, 1992; Pfeffer, 1987). In particular, due to the diverse expertise and experience of its members, a bigger audit committee is better able to oversee management (Hamdan, Sarea&Reyad, 2013). Good corporate governance also relies on the audit committee’s competence, independence, honesty, trustworthiness, impartiality, objectivity, impartiality and authority (Kantudu & Samaila, 2015)

(b) Audit quality, corporate governance, and moderating factors.

Table 1 illustrates that two key moderating elements, sufficient finance and the skills and accounting capacities of the audit team, boost the effectiveness of audit quality in promoting good corporate governance. The moderating factors enhanced the impact of audit quality on corporate governance, as shown by the beta values of 0.40 compared to the beta value of 0.33 without their influence. It is evident that having sufficient financing, as well as the competencies and accounting capacities of the audit team, enhances the effectiveness of audit quality in promoting good corporate governance. If the market is to remain ethical and mergers and acquisitions are to be advanced, then experts in auditing procedures are required (Kantudu & Samaila, 2015). To guarantee that auditing effectively promotes excellent business practices, competencies like personnel competence, service scope, and efficient planning, performance, and relaying of internal audit results are essential. Findings also indicate that the scope of controls was not a more important moderator of the correlation between audit quality and corporate governance.

(c) Consulting role of Internal Audit, moderating factors and corporate governance

Internal Audit’s consulting role in promoting good corporate governance is enhanced by two main moderating factors, as shown in Table 1: management-oriented auditing and comprehensive and strategic approach stakeholder engagement. The moderating factors enhanced the impact of Internal Audit’s consulting function on corporate governance, as shown by the beta values of 0.11, compared to the beta value of 0.01 without their influence. The association between Internal Audit’s consulting functions and excellent corporate governance was more effectively impacted by the moderating factors as seen by its higher beta value of 0.11. This discovery lends credence to the current literate’s claims that modern internal auditors need knowledge of and experience in areas like business management, systems development, strategic management, and other related fields, in addition to keeping up of pertinent developments. To achieve success, one must have an in-depth knowledge of the market’s practical choices, their pros and cons, operational procedures, and implementation techniques (Nuryanah & Islam, 2011). For auditing to contribute to good corporate governance, management-oriented methods are required.

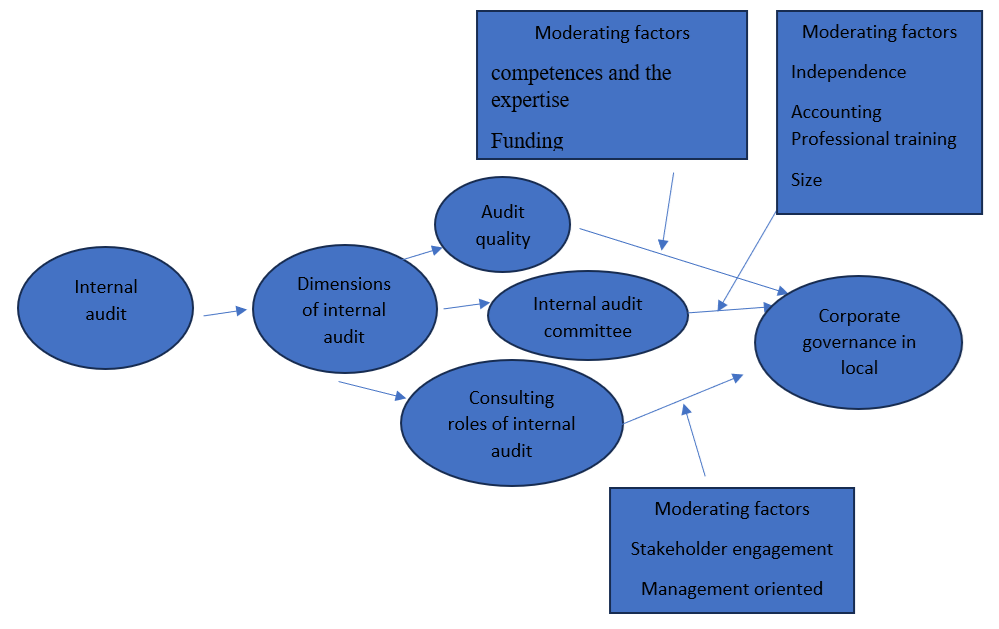

(d) Integrated internal audit framework that promotes good corporate governance in local authorities.

Local authorities can encourage excellent corporate governance by using the internal audit model, which is shown in Table 1. Since the model’s foundation is based on auditing processes and procedures, it represents an accounting viewpoint on the development of good corporate governance. In addition to the three tenets of internal auditing, the study looked at how moderating factors affected the connections between IG and CG. The result was a unified framework with the following components: the pillars of internal auditing and the moderating elements for each pillar.

Framework for integrated internal audits that encourages strong corporate governance at the municipal level. The model states that to promote corporate governance effectively from an internal audit perspective, one must carefully examine the many aspects of internal audit as well as any moderating factors. By utilizing the audit committee, the audit committee, and the consulting role of internal audit, the model demonstrates how local authorities can promote good corporate governance through the aspects of internal auditing. The reason for this is the strong positive correlation between the variables. Furthermore, the model shows that moderating factors improve the dimensions’ effectiveness in developing excellent corporate governance. Some of the factors that can be considered as moderators include the following: the audit committee’s independence, the internal audit committee’s size, the funding of auditing processes, the competencies and expertise of the internal auditing staff, the audit committee’s ability to effectively engage stakeholders, and the audit committee’s management-oriented approaches.

Figure 4.67 Integrated internal audit model that promotes good corporate governance in local authorities.

CONCLUSIONS

The research found a theoretical relationship between policy-level internal auditing and corporate governance in local governments. This link has the potential to inform policymaking about the promotion of corporate governance in municipal governments. The results of this inquiry led to the deduction of multiple conclusions. According to the research, local governments can strengthen their corporate governance systems and practices through the use of internal audits. To successfully encourage the formation of solid corporate governance norms in local authorities, the study found that numerous crucial aspects of the internal audit could be improved. There are strong foundational elements present. Protecting the organization’s financial resources and promoting strong corporate governance norms are the two main goals of the internal audit function. The present knowledge of the relationship between internal audit and corporate governance in the particular context of developing nations is greatly enhanced by this study. To promote efficient corporate governance in local authorities, the study argues that a financial strategy is essential. Quality internal auditing, an effective internal audit committee, and strong internal audit consultation capabilities were determined to be the three most important aspects of internal auditing in fostering excellent corporate governance, according to the study’s findings. According to the research, audit committees are crucial for local governments to have good corporate governance. The study’s most important takeaway is that there are moderating factors that affect the impact of each aspect of internal audit. Considerations include the independence of the audit committee, the presence of qualified internal auditors, and compliance with IIA criteria One or more internal audit factors may affect the degree to which internal audit has an impact on corporate governance. When it comes to internal auditing and corporate governance, this is a significant step forward

New Knowledge Contribution

By looking at local government corporate governance via an internal audit lens, the study improved our understanding of the topic. By drawing attention to the importance of internal auditing within the framework of corporate governance, the study significantly advanced the area of corporate governance. Researchers have previously looked at internal audits and corporate governance as they pertain to local government bodies; this study adds to that body of work. By showing how internal auditing helps improve effective corporate governance, this study has expanded the function and reach of internal auditing in local governments. By clarifying what good corporate governance is and how local government internal audits might be organized to encourage the adoption of excellent corporate governance practices, this study contributes to the body of literature on audit quality.

Improving upon what is already known about corporate governance, an integrated internal model has been developed to help local authorities practice good corporate governance. To improve corporate governance in local governments, the study created a model based on accounting principles. In addition to the three tenets of internal auditing, the study looked at how moderating factors affected the connections between IG and CG. The result was a unified model with internal audit pillars and attributes that moderated their effectiveness.

The model states that to promote corporate governance effectively from an internal audit perspective, one must carefully examine the many aspects of internal audit as well as any moderating factors. The audit committee’s independence, the internal audit committee’s accounting experience and professional capacities, the committee’s size, the funding of auditing processes, the competencies and expertise of the internal auditing staff, the audit committee’s effective engagement with stakeholders, and the audit committee’s management-oriented approaches are the moderating factors

RECOMMENDATIONS

The research found a theoretical relationship between policy-level internal auditing and corporate governance in local governments. This link has the potential to inform policymaking about the promotion of corporate governance in municipal governments

To promote excellent corporate governance, the model suggests that local authorities strengthen internal audits in regions where they are deficient. As part of this effort, it is crucial to make sure that the internal audit follows all the latest guidelines and is up to par with international standards.

The study suggests that future research should broaden its scope by investigating the contextual factors of other developing countries that share similar institutional traits

REFERENCES

- Abbott L.J., Park Y. and Parker S. (2000). “The effects of audit committee activity and independence on corporate fraud”. Managerial Finance. Vol. 26, No. 11, pp. 55–68.

- Agrawal R., Johnson C., Kiernan J. and Leymann F. (2006). “Taming Compliance with Sarbanes-Oxley Internal Controls Using Database Technology”. 22nd International Conference on Data Engineering. Atlanta, 03-08 April 2006.

- Al-Ajmi J. (2009). “Audit firm, corporate governance, and audit quality: Evidence from Bahrain”. Advances in Accounting, incorporating Advances in International Accounting. 25, No. 1, pp. 64-74.

- Bekiaris, M., Efthymiou, T. and Koutoupis, A.G., (2013). Economic crisis impact on corporate governance and internal audit: the case of Greece. Corporate Ownership and Control, 11(1), pp.55-64.

- Bou-Raad G. (2000). “Internal auditors and a value-added approach: The new business regime”. Managerial Auditing Journal. Vol. 15, No. 4, pp. 182–187.

- BRC (1999). Report and Recommendation of the Blue Ribbon Committee on Improving the Effectiveness of Corporate Audit Committees. Blue Ribbon Committee. New York Stock Exchange and National Association of Securities Dealers. New York, NY.

- Broni G. and Velentzas J. (2012). “Corporate governance, control and individualism as a definition of business success. The idea of a “post-heroic” leadership”. Procedia Economics and Finance. Vol. 1, pp. 61-70.

- Canadian Institute of Chartered Accountants (1981). Audit Committees. Toronto: CICA.

- Carcello J.V., Hermanson D.R. and McGrath N.T. (1992). “Audit Quality Attributes: The Perceptions of Audit Partners, Preparers, and Financial Statement Users”. Auditing: A Journal of Practice and Theory. Vol. 11, pp. 1−15.

- Cohen J., Krishnamoorthy G. and Wright A.M. (2002). “Corporate Governance and the Audit Process”. Contemporary Accounting Research. Vol. 19, No. 4, pp. 573-594.

- Committee of Sponsoring Organizations of the Treadway Commission (COSO) (1992). Internal Control – Integrated Framework. New York: The Committee of Sponsoring Organizations of the Treadway Commission.

- Core J.E., Holthausen R.W. and Larcker D.F. (1999).” Corporate governance, chief executive officer compensation, and firm performance”. Journal of Financial Economics. Vol. 51, No. 3, pp. 371–406.

- Davidson R.A. and Neu D. (1993). “A note on the association between audit firm size and audit quality”. Contemporary Accounting Research. Vol. 9, No. 2, pp. 479−488.

- DeAngelo L.E. (1981). “Auditor size and audit quality”. Journal of Accounting and Economics. Vol. 3, No. 3, pp. 183–199.

- Dewing I.P. and Russell P.O. (2004). “Accounting, Auditing and Corporate Governance of European Listed Countries: EU Policy Developments Before and After Enron”. JCMS: Journal of Common Market Studies. 42, No. 2, pp. 289-319.

- Drogalas G., Pantelidis P., Vouroutzidou R. and Kesisi E. (2011). “Assessment of corporate governance via internal audit”, New Horizons in Industry, Business and Education (NHIBE2011), Chios, Greece, Conference Proceedings, pp. 333-337.

- Drogalas G., Alampourtsidis S. and Koutoupis A. (2014). “Value-added approach of Internal Audit in the Hellenic Police”, Corporate Ownership and Control. 11(4), pp.692-698

- Dühnfort, A.M., Klein, C. and Lampenius, N., (2008). Theoretical foundations of corporate governance revisited: A critical review. Corporate Ownership & Control, 6(2), pp.424-433.

- Eichenseher J.W. and Shields D. (1983). “The correlates of CPA-firm change for publicly-held corporations”. Auditing: A Journal of Practice and Theory. Vol. 2, No. 2, pp. 23−37.

- Goodwin-Stewart J. and Kent P. (2006). “The use of internal audit by Australian companies”. Managerial Auditing Journal. Vol. 21, No. 1, pp. 81–101.

- Green D.L. (1994). “Canadian Audit Committees and Their Contribution to Corporate Governance”. Journal of International Accounting, Auditing and Taxation. Vol. 3, No. 2, pp. 135-151.

- Gstraunthaler, T., (2010). Corporate governance in South Africa: the introduction of King III and reporting practices at the JSE Alt-X. Corporate Ownership and Control, 7(3), pp.146-154.

- Hart O. (1995). “Corporate Governance: Some Theory and Implications”. The Economic Journal. Vol. 105, No. 430, pp. 678-689.

- Hass S., Abdolmohammadi J.M. and Burnaby P. (2006). “The Americas literature review on internal auditing”. Managerial Auditing Journal. Vol. 21, No. 8, pp. 835-844.

- Karagiorgos T., Drogalas G., Gotzamanis Ε. and Tampakoudis I. (2010). “Internal Auditing as an Effective Tool For Corporate Governance”, Journal of Business Management, 2(1), International Science Press, pp. 15-24.

- Klein A. (2002b). “Economic determinants of audit committee independence”. The Accounting Review. Vol. 77, No. 2, pp. 435–452.

- Knapp M. (1987). “An empirical study of audit committee support for auditors involved in technical disputes with client management”. The Accounting Review. Vol. 62, No. 3, pp. 578–588.

- KPMG International, Audit Committee Institute, (2006). Five guiding principles for audit committees. Geneva: KPMG International.

- Krishnan J. (2001). “Corporate governance and internal control: An empirical analysis”. American Accounting Association (AAA) Annual Meeting. Atlanta, 2006.

- Lindow E.P. and Race D.J. (2002). “Beyond Traditional Audit Techniques”. Journal of Accountancy. Vol. 194, No. 1, pp. 28-33.

- OECD (2004). OECD Principles of Corporate Governance. Organization for Economic Co-Operation and Development.

- O’Sullivan N. (2000). “The Impact of Board Composition and Ownership on Audit Quality: Evidence from Large UK Companies”. The British Accounting Review. Vol. 32, No. 4, pp. 397-414.

- Paape L., Scheffe J. and Snoep P. (2003). “The Relationship Between the Internal Audit Function and Corporate Governance in the EU – a Survey”. International Journal of Auditing. Vol. 7, No. 3, pp. 247-262.

- Palmrose Z. (1988). “An Analysis of auditor litigation and audit service quality”. The Accounting Review. Vol. 63, pp. 55−73.

- PwC 2006. PricewaterhouseCoopers’ State of the internal audit profession study: internal audit post Sarbanes-Oxley. New York: PricewaterhouseCoopers LLP.

- Regoliosi C. and d’Eri A. (2012). ““Good” corporate governance and the quality of internal auditing departments in Italian listed firms. An exploratory investigation in Italian listed firms”. Journal of Management & Governance. [Online] Available from: http://link.springer.com/article/10.1007/s10997-012-9254-1/fulltext.html#Sec1

- Rezaee Z., Olibe K.O. and Minmier G. (2003). “Improving corporate governance: the role of audit committee disclosures”. Managerial Auditing Journal. Vol. 18, No. 6/7, pp. 530-537.

- Robertson C.J., Diyab A.A. and Al-Kahtani A. (2013). “A cross-national analysis of perceptions of corporate governance principles”. International Business Review. Vol. 22, No. 1, pp. 315-325.

- Rustam S., Rashid K. and Zaman K. (2013). “The relationship between audit committees, compensation incentives and corporate audit fees in Pakistan”. Economic Modelling. Vol. 31, pp. 697-716.

- Sarens G. and Abdolmohammadi J.M. (2011). “Monitoring Effects of the Internal Audit Function: Agency Theory versus other Explanatory Variables”. International Journal of Auditing. Vol. 15, No. 1, pp. 1-20.

- SOX 2002. Sarbanes-Oxley Act of (2002). One Hundred Seventh Congress of the United States of America. Washington.

- Suyono E. and Hariyanto E. (2012). “Relationship Between Internal Control, Internal Audit, and Organization Commitment With Good Governance: Indonesian Case”. China-USA Business Review. Vol. 11, No. 9, pp. 1237-1245.

- The Institute of Internal Auditors, 2004. The Professional Practices Framework. Florida: The IIA Research Foundation.

- Turley S. and Zaman M. (2004). “The Corporate Governance Effects of Audit Committees”. Journal of Management and Governance. Vol. 8, No. 3, 305-332.