Can International Business and Entrepreneurship be the Catalysts for Economic Growth in Africa?

- Joseph G. M. Lutta

- 465-477

- Mar 19, 2024

- Economic Development

Can International Business and Entrepreneurship be the Catalysts for Economic Growth in Africa?

Joseph G. M. Lutta

University of Fujairah, Fujairah, United Arab Emirates

DOI: https://doi.org/10.51244/IJRSI.2024.1102036

Received: 05 February 2024; Accepted: 12 February 2024; Published: 19 March 2024

ABSTRACT

Innovative entrepreneurs are important actors in regional economies of Africa. There are enormous entrepreneurial opportunities in the global markets. The World Bank’s Global Economic Prospects for 2023 indicates that the global growth has eased, but remains robust, and is projected to reach 3.1 percent in 2018. Overall, growth in global trade of goods and services combined is expected to moderate to 4.3 percent in 2018, down from a six-year high of 4.8 percent in 2017. This projection has been revised upwards due to stronger-than-expected intra-regional trade growth in Asia and Africa as well as import-demand from major advanced economies. Global trade in goods and services is projected to rise to $27 trillion in 2030 from $10.3 trillion in 2015. Trade as a share of the global economy will increase from 1/4 to 1/3. Roughly half of the increase is likely to come from developing countries that will supply over 65 % of manufactured imports to rich countries, compared with 40% today. Some developing countries are expected to have growth rate over 6%, much higher than developed countries. When trade expands, technologies will rapidly diffuse to developing countries. The dominance of globalization is transferring to China, India and Brazil. The challenge of entrepreneurship is immense in Africa. The entrepreneur’s needs differentiation of exporting and the continent has to create its own regional clusters so as to enhance the competitiveness of its enterprises. Africa may have all the possible comparative advantages in certain industries but what is required is entrepreneurial actions. International business and entrepreneurship appear to be the catalysts for much of the expected economic growth in Africa.

Keywords: Microeconomics, Entrepreneurship, Globalization, International Trade, Africa

INTRODUCTION

According to Lahti (2016), a well-known representative of the British-American Economic School of thought was Alfred Marshall, a leading British economist at Cambridge between 1890s and 1920s. Marshall in his eighth edition of his book Principles of Economics (Marshall, 1920), exerted a great influence on the development of economic thought at the time. Marshall was concerned with theories of costs, value, and distribution, and developed a concept of marginal utility. He made a distinction between the internal and external economies of the firm. According to him, external economies (such as economies of scale), depend on the firm’s adaptation to industry developments while internal economies, economies of scope, are dependent on the resources, organization and management efficiency. For primarily methodological reasons, Marshall introduced into economic analysis the concept of representative firm as the theoretical unit of analysis, instead of a real one. By stressing the concept of average costs instead of marginal one, he focused neo-classical economists’ attention to the firm’s optimizing (cost-minimizing) behavior and excluded entrepreneurial (innovative) behavior with diverse supply and demand curves.

In the early 20th century, Joseph Schumpeter, an influential writer and a member of the German Economic School of thought, proposed “Theorie der wirtschaftlichen Entwicklung” in 1911 and was published as Theory of Economic Development in 1934 (Schumpeter, 1934). Schumpeter distinguished innovation as the function of the entrepreneur. Schumpeter never denied the genius of Marshall’s writings. In his book Business Cycles (Schumpeter, 1939), Schumpeter now as a Harvard professor, referred to the fundamental problem of economic change. He argued that entrepreneurs create innovations in the face of competition and thereby generate (irregular) economic growth. Schumpeter (1939) proposed a three-cycle model of economic fluctuations or waves: (1) Kitchin inventory cycle (3-5 years), (2) Kuznets infrastructural investment cycle (15-25 years), and Kondratieff long cycle (45-60 years). During his career until the 1950s, Schumpeter gave economists food for thought with the concept of creative destruction. In his book Capitalism, Socialism and Democracy, he predicted the transition from competitive capitalism to trustified capitalism.

Consequently, in this paper, the author discusses how dynamic entrepreneurship can be used as a catalyst to achieve scale economies/agglomeration to stimulate growth and Africa’s participation in the global economy as described by Schumpeter. The author also proposes what is required for Africa to achieve scale economies, intra-regional trade, develop domestic markets, and raise its competitiveness in international trade. Based on the evidence gleaned from selected case examples of successful entrepreneurs from African nations, the author makes the case for inclusion of entrepreneurship as a catalyst for Africa’s economic growth.

ENTREPRENEURSHIP AS THE SPECIFIC ECONOMIC FUNCTION

Schumpeterian entrepreneur is a potential winner in global markets and Schumpeter (1934) argued that an entrepreneur, as innovator, creates profit opportunities by devising a new product, a production process, or a marketing strategy. An entrepreneurial discovery occurs, when an entrepreneur makes the conjecture that a set of resources is not allocated to its best use. Schumpeter suggests (Lintunen, 2000): (1) an entrepreneurial function is the act of the will of the entrepreneur for the introduction of innovation in an economy, and a source of evolution in a whole society, (2) entrepreneurial leadership is the source of creative energy for innovation and evolution, and (3) entrepreneurial profit is the temporary monopoly return on the personal activity of the entrepreneur. In order to elaborate the human behavior of the Schumpeterian entrepreneur, the author in this paper has referred to some of the contemporary writers.

The most fascinating neo-Schumpeterian writer has certainly been Peter Drucker with his book Innovation and Entrepreneurship (Drucker, 1985). Most of the entrepreneurs are not really innovative. Looking back to his unique history over the 21st century as the management writer, Drucker argued that 90% of innovations are based on “creative imitation”. They provide only moderate probability of success. As to Schumpeterian entrepreneur, the most interesting entrepreneurial strategy is “being fustiest with the mostest”. This is the strategy that a Confederate cavalry general in America’s Civil War applied to win battles. Following this strategy, the entrepreneur is striving for leadership, which is the entrepreneurial strategy par excellence. This is the core content of entrepreneurial literature and, especially the one used by high-tech entrepreneurs. Drucker’s warning is that of all entrepreneurial strategies, this strategy is the advanced gamble, making no allowances for mistakes and permitting no second chance. But if successful, it is highly rewarding. To use the leadership strategy requires careful analysis. The strategy demands substantial and continuing efforts to retain a leadership position.

Silver (1985) is one of the first writers to discuss the concept of team work, which is well applicable to complex business problems. Silver characterizes his model as fundamental law of entrepreneurial process. In Silver’s thinking, the goal of investors/entrepreneurs is the creation of wealth or high valuation (V), through the process of selecting a potentially successful entrepreneurial team (E) that can identify and conceptualize a large, multidisciplinary problem (P) and create elegant solutions (S) which they intend to convey to the problem via a new company. In Silver’s thinking an understanding of the equation will save billions of dollars of capital and perhaps trillions of hours of entrepreneurial time and energy.

Where V = Wealth or high valuation of a venture

E = Successful entrepreneurial team

P = Large, multidisciplinary problem

S = Elegant solutions

Silver’s model of the valuation of business ventures adapted from Lahti (2017)

Silver’s main focus was to analyze how successful entrepreneurs have succeeded in terms of ’fundamental law of entrepreneurial process’. Utilizing the model, Silver analyzed ’the 100 greatest entrepreneurs of the last 25 years’. His ’entrepreneurial scorecard’ is inspiring since a company with high value (V) has many beneficiaries – entrepreneur, managers, employees and investors. In the epilogue, Silver summarizes that ’being an entrepreneur is like being the builder of civilization’. In Silver’s thinking, an entrepreneurial team takes holistic responsibility of the Schumpeterian process of ’creative destruction’. How can an African entrepreneur be so good in all the key personal abilities that are needed to succeed? The counter-argument is simple. Africans succeed well in summer sports because they have the team work of talented sportsmen and their experienced coaches. Why not in manufacturing? The problem-solving process in the internationally qualified manufacturing is the same as in the top sports.

Kuada (2006) is apt in explaining the link between entrepreneurship and economic growth. Quoting North and Smallbone (2006), Kuada posits that given the relationship between entrepreneurship and economic growth and development, governments and policymakers have been in search of appropriate policies for fostering the entrepreneurial capabilities of their citizens. According to Kuada (2015), not all small businesses can be considered as being truly entrepreneurial. For example, some business owners are forced into entrepreneurship not by choice but by necessity (Fitch & Myers, 2000; García-Cabrera & García-Soto, 2008; Kuada, 2015). As such, they may not have the entrepreneurial traits or skills suggested in theory and may be unable to grow their businesses due to competing demands on their resources. Their contributions to overall economic growth, including job creation, and tax revenue generation, may therefore be limited (Kuada, 2015). Furthermore, it has been noted that idiosyncratic and social factors tend to influence the determination of which firms grow and survive in a given country (Maritz, 2004; La Pira, 2010).

SCHUMPETERIAN ENTREPRENEUR FROM AFRICA MEETS THE BIG PLAYERS

At the beginning of the 21st century, “core countries” were rich and developed with their average citizen achieving high standards of living. The Unite States, the United Kingdom, the European Union, Japan, Canada and Australia are recognized as core countries. The less developed countries in Africa, Asia and Latin America have low economic growth and poorly educated, housed and fed populations. Newly industrializing countries (NICs) such as the ‘Four Dragons’ (South Korea, Taiwan, Hong Kong and Singapore) and the ‘Little Dragons’ (Malaysia, Thailand, Indonesia and GCC), owing to impressive economic growth rates in recent years, seem to improve their position in the global economy whereas many periphery countries, like the Sub-Saharan countries, are stagnating, at least comparatively. In Europe, the economic integration has created new economic regions that are rich and developed in the global perspective (Robson, 1993). Globalization has shifted the comparative advantages of international trade away from traditional inputs of production, such as land, labour and capital, towards knowledge. The knowledge intensive regions are the winners of the global economies and the large home market countries, such as the US, are often host countries of multinational company (MNC) headquarters. The role of MNCs has been recognized to be important in the present, intertwined global economy (UNCTAD, 2016).

The success of MNCs is inevitable. In the 1970s, it was highly popular among the general public and the politicians to “see MNCs as big and bad”. Today, MNCs are innovators of new technologies. Their economies of scale depend on the size of capacity and speed with which the capacity is utilized. The key concept propagating openness in international trade is the Ricardian comparative advantage, which can be found in the accumulation of the factors, where the nation has the most favourable comparative costs. When the world trade organization (WTO) was established, the industrialized countries oriented towards Smith’s (1976) absolute advantage. An indicator of that is the adoption of Porter’s (1990) cluster model by the OECD countries. The term diamond refers to the fact that the home country (home-base) of the cluster tries to domesticate the cluster elements by the hidden mercantilism (Coleman, 1980). The most clustered countries are mainly the industrialized countries (the US, the EU and Japan), some of newly industrialized countries (China, India, Brazil, Russia, etc) and seldom developing countries.

Schumpeter (1950) projected the transition from the competitive capitalism to the trustified capitalism and argued that the success of capitalism will lead to a form of corporatism and to values that are hostile to entrepreneurship, especially among intellectuals. Schumpeter posited that free market capitalism is the best economic system, and in the 1950s, John Kenneth Galbraight (1956) supported Schumpeter’s prediction of corporatism. He argued that large firms have the countervailing power that describes a certain level of collusion between large firms and the government. Multinationals operate in all continents and markets (goods, services, financing, immaterial property rights, etc) represent trustified capitalism and not an orthodox monopoly (Stigler, 1968). Multinationals invest in countries with impressive economic growth rates. However, the newly industrialized countries (China, India, Brazil, etc) are mobilizing their own “gardes” of hungry multinationals to compete in the global market. Jensen (1992) provides an interpretation of the Schumpeterian creative destruction by comparing the growth of GNPs with R&D statistics after the oil crisis in the mid 1970s and found that the oil crisis compelled the core countries to invest in R&D. The growth of R&D expenditures has been twice as high as the growth of GNPs.

The main driving forces of globalized or industrialized economies are:

- The process of Schumpeterian dynamics, proprietary capitalism that requires policies which nurture processes of catalyzing investments in venture capital, startups, networking etc. (Putnam, Leonardi, & Nanetti, 2013). The Silicon Valley region is an example of entrepreneurial, proprietary capitalism. One of the bottlenecks of Africa is weakly developed private venture capital markets for global winner entrepreneurs. Microfinance can partly compensate that but not totally.

- The formation of globally competitive clusters of multinationals. Geographic concentration of firms has been particular to Europe and United States as noted by Alfred Marshall. Michael Porter (1990) proposes the diamond model as a doctrine for clustering that incorporates the determinants of a company’s environment, which influence the firm’s ability to create and sustain competitive advantage in the global markets. Regional clusters in general seem to perform better than the national average in the US (Sassen, 2011; Saxenia, 2014).

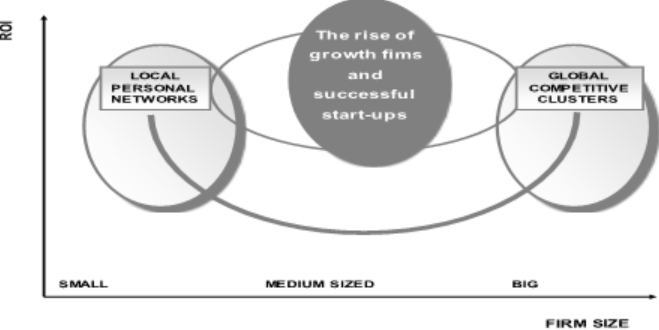

Many industries are geographically concentrated, and such clusters are an important source of international specialization and trade. The importance of geographic proximity is shaped by the role played by the scientists who will live in the regions occupied by multinationals that are best buyers of the new, scientific knowledge. The triad of New York, London and Tokyo that dominate global financial services is an example of permanent clusters. Urban ghettos are parts of the famous Silicon Valley production system as are the engineering laboratories at Stanford, or the military R&D facilities. Today, universities and their related research laboratories spread throughout most regions in the US. Geographical proximity can be expected to serve the incubation of new technologies. There seems to be some measures that can be used to anticipate the origin and initial location of new geographical clusters of firms. The most important is the existence of growth firms and new start-ups. If several new firms spin off from a common parent, or a set of parents, then a cluster of firms could begin spontaneously. The Nordic cluster model is, perhaps, the most well-known examples of how to combine the Schumpereterian entrepreneurship with the proactive internationalization of firms (Dahmen, 2016; Donelly & Hyry, 2014; Luostarinen, 1979). Schumpeterian entrepreneurship as the combination of proprietary and collective capitalism is functioning in regional clusters like Silicon Valley somewhere between local networks and global clusters (figure 1).

Figure 1: Two poles of the Schumpeterian dynamics (adopted from Lahti, 2015)

AFRICA – FROM MARGINALIZATION TO GLOBAL BRANDING

Lahti (2015) posited that Finland started its market integration through the Nordic Common Market (Nordek) in the 1950s, extended its market integration to the EFTA (European Free Trade Association) in the 1960s and finalized the full EU membership in 2005. In spite of the process of five decades, Finland could not avoid the economic crisis. Finnish Banks’ foreign borrowing was a major risk factor that was realized in the early 1990s under the period of the EU accession. One of the implications was concerns of R&D investments. Finland has been so successful because it has succeeded in developing its own world-class technology, at least in certain industries such as the ICT and paper & pulp industries. Comparatively, on generally terms the average foreign sources of technology should account for 90% of local productivity growth as noted by Drucker (1985). In 2000, the European heads of government at the Barcelona Council meeting agreed to pursue a target of 3% of GDP investment in R&D for science and technology until 2010. At the time, the EU-15 average was 1.5% when Finland and Sweden were approaching 4%.

Bertel Ohlin (1933) from Swedish School of Economics revised Ricardo’s model incorporating realistic characteristics of production. The Heckscher-Ohlin theory (H-O-theory) has its historical roots in the phenomenal success of the Nordic countries from the second industrial revolution to the time of globalization. The Nordic countries have succeeded to increase their GNIs from the bottom ranking to the top. The H-O-theory is relevant to the low-tech production that is local of its nature but not the high-tech production requirement of the global operations, R&D-oriented and Schumpterian of its nature (e.g. the ICT). The H-O-theory is relevant for Africa.

Staffan Burenstam Linder (1961), a Swedish economist, tried to provide the demand-driven explanation and hypothesized that demand plays a more important role than comparative advantage in international trade. In his model, the pattern of trade is determined by the aggregated preferences for goods within a country. Demand-based international trade arises from consumers’ taste of variety. This aggregate taste for variety arises because different individuals have a different specification of their ideal variety. Countries with similar preferences are expected to have the same structures of industries. For example, the US and Germany both have large automotive industries that can be explained by a significant demand for cars in both countries. Rather than one country dominating the car industry with a comparative advantage, both countries trade different brands of cars between them. Elhanan Helpman and Paul Krugman (1985) believe that countries are trading in differentiated goods because of their similarities. The demand-driven explanation of international trade has been justified in the European integration. In the EU, the demand-based inter-regional trade is totally dominating. Africa is logistically isolated from the world trade flows and lagging behind. In order to deepen the trade links, Africa needs investments in harbors, railways, roads, electricity grids, the internet, education, etc.

In this paper, the author identifies three distinct weaknesses in Africa’s merchandise exports:

- A narrow range of products

- A lack of diversification of export markets and

- A low technology content

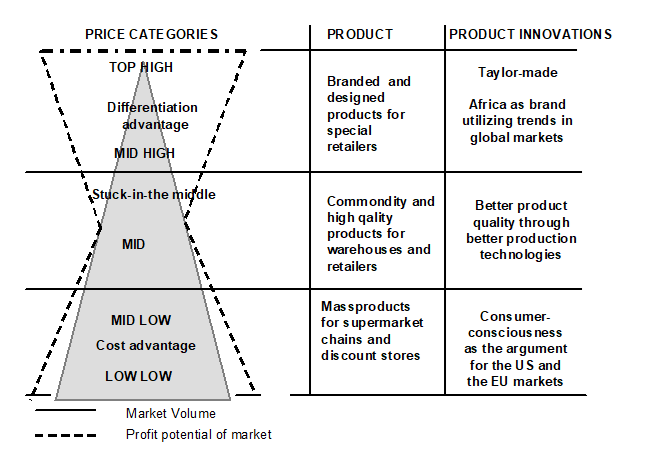

African growth firms should utilize the diverse supply and demand curves. Referring to Edward Chamberlin’s book “The Theory of Monopolistic Competition,” the author visualized the challenge in the figure below:

AFRICA’S ENTREPRENEURSHIP AND THE INTERNATIONAL TRADE

The trade patterns of African countries are usually based on crude or processed agriculture or mineral based products. This kind of factor-based exports provide only a minimum value added to firms in Africa that have the difficulty to utilize the modern technology. The technological gap between African firms and an average global firm is major in technical know-how services. The result is that the industrial structure in Africa is polarized into big and small firms. Most industrial sectors are dominated by big, diversified firms that are the major end-users of raw materials and capital inputs in Africa. Because of their size and diversity, big firms are the basic structural element of industrial clusters. Small firms are a complementary structure. The weak development of pan-African markets of industrial goods and services is the main reason for the lack of innovative medium-sized growth firms. Without dynamics of growth firms and entrepreneurship, global economic turmoils would affect African countries with severity.

According to Alfred Chandler’s book “Scale and Scope”, Africa has the same structural problem as the leading industrial countries a century ago. Because of the undeveloped inter-regional trade, the integrated big firms do not need any sub-contracting with medium-sized growth firms. Considering the share of inter-regional trade of each region’s total trade, WTO’s Trade Report (2017) indicates that European share is 73.2%, North America, 55.8% and Asia, 51.2% while Africa accounted for only 8.9%. Inter-regional trade is so important and dominating because firms are trading differentiated goods and services, not only commodities.

Helpman and Krugman, (2005) found that countries are trading, not because they are different, but because they are similar as postulated by the demand-driven explanation. Burenstam-Linder (1961) hypothesized that demand plays a more important role than comparative advantage in trade. Demand-based international trade arises from consumers’ taste of variety and this aggregate taste for variety arises because different individuals have a different specification of their ideal variety. Countries with similar preferences are expected to have the same structures of industries. Africa needs differentiated goods and services as export articles and the basic strategic capability that is needed is strategic marketing. African growth firms should learn to utilize the diverse supply and demand curves as visualized in the figure in the previous page. The demand-based benefits are the driver of international trade. Increasing trade of differentiated articles gives consumers in various countries a wider choice of goods and services to select. Africa needs export articles with high value added, because the prices of commodities are falling.

The challenge of African entrepreneurship is to deepen the consumer or customer orientation in the near future. The poor African enterprises need to create agglomeration economies and social/trust capital between global clusters and local networks. Whereas the clustering of firms is a top-down perspective, the poor African countries should focus on bottom-up approaches to create social or trust capital between global markets and local entrepreneurs and communities.

Globalization reinforces the interdependencies of states in various continents. Africa should deepen the spatial linkages of states in a mutually beneficial way. The problem is demand structure. Whereas China and India have large domestic markets, Africa with 54 countries is difficult to reach. Finding the right customers and reliable business partners in the African market is a time-consuming process. Most of the business sectors in African countries are small and firms have established methods of procurement that differ from one sector to another. There are only few agents who serve a particular sector on an exclusive basis, but, because they are well established within the sector, they deal in many other sectors. Pan-African markets are the best available home market for African firms to start globalization. Demand-based international trade arises from consumers’ taste of variety. Countries with similar preferences are expected to have the same structures of industries. Pan-African entrepreneurs are the ones that could enable African firms to learn global market demand in their own continent. Therefore, Africa needs market integration at the regional level. The first stage might be regional custom unions. The problems with regional integration emanate from the political/legal processes that often overshadow the national economic development agenda.

The following are some selected case examples of successful entrepreneurs in Africa:

Selected Case Examples of Successful Entrepreneurs in Africa:

Source: Iwuoha, J. P., & Bokrezion, H. (2015):

Case 1: Fomba Trawally (Liberia)

When the civil war broke out in 1989, Fomba Trawally fled Liberia and settled as a refugee in the Gambia. In 1991, he returned to his country and started a trading business with a sole focus on rubber slippers (flip flops) which were very much in demand at that time. His startup capital totaled $200, being from his life’s savings. That initial investment in rubber slippers made quick returns and the business grew steadily. By 2005, this self-made multi-millionaire entrepreneur owned three retail stores in Monrovia, selling items such as paper products and cosmetics imported from all over the world. In 2010, Trawally made the transition from being an importer to a manufacturer. He set up National Toiletries Incorporated, Liberia’s first paper and toiletry products manufacturing company. Annual sales from his factories have crossed the $1 million mark and he’s making plans to double production capacity soon. Fomba’s is an inspiring story of a former refugee who turned his life around, and is now one of Liberia’s richest and most successful entrepreneurs.

Case 2: Bethlehem Tilahun Alemu (Ethiopia)

Bethlehem Alemu grew up in Zenabwork, a poor village in the suburbs of Addis Ababa, Ethiopia. Her business – SoleRebels – is one of the most popular and fastest-growing African footwear brands in the world! Her collection of eco-friendly footwear (made from recycled materials) have been sold in more than 50 countries across the world, including the USA, Canada, Japan and Switzerland. Currently, her business rakes in annual revenues in excess of $1 million. But her business dream would have never been possible without nearly $10,000 in capital she raised from family and relatives in 2004. Buoyed by her success with SoleRebels, Bethlehem recently launched Republic of Leather, a new business that trades in luxury leather products like bags, belts and other non-footwear leather accessories. Her inspiring success story has been featured on Forbes, the BBC and CNN. And she has been described by Forbes as ‘One of The World’s Most Powerful Women’.

Case 3: Jason Njoku (Nigeria)

Jason Njoku is the co-founder and CEO of Iroko TV, a mobile entertainment and internet Television platform that’s particularly popular for its impressive catalogue of African ‘Nollywood’ movies. The growth of this business has been very remarkable. To date, Iroko TV has attracted up to $40 million in investment funding from foreign investors. But the struggle in the early days of this business was not as glamourous. After a few failed attempts at previous businesses in the UK, Jason returned to Nigeria in 2010 to build local relationships and purchase content rights for his new startup, Iroko TV. Cash was tight, and starting this business would have been impossible without the £90,000 contribution of Jason’s friend and business partner, Sebastian Gotter. That single ‘small’ investment in what was a very ambitious idea, has created a multi-million-dollar company that’s now dubbed as the ‘Netflix of Africa’. Iroko TV recently raised $19 million in additional funding to expand its business across Africa.

Case 4: Adii Pienaar (South Africa)

Adii Pienaar is co-founder of WooThemes, a South Africa-based tech company that was recently acquired by Automattic, a US-based online tech giant, for $30 million. Adii Pienaar started WooThemes in 2008, at age 23 while he was still in university. Adii worked part-time as an online freelancer and consultant on the side while he continued to work hard on WooThemes, using his savings and earnings at the time to support the business. This strategy of starting a business with no money — or, at least, very little money, is commonly referred to as ‘bootstrapping’. It is the art of making personal sacrifices, using personal savings and limited financial resources to support a business in its early days. Despite his impressive success with WooThemes, Adii Pienaar remains a serial entrepreneur and continues to work on several promising startup projects.

Case 5: Patrick Ngowi (Tanzania)

Patrick dipped his feet into the world of business at age 19 when he started selling Chinese-made mobile phones. Today, he owns one of East Africa’s most successful solar energy companies – Helvetic Solar Contractors. But his journey to the top wasn’t an easy one. To get started, he took a loan of $1,800 from his mother, and a close friend sponsored his travel to China. In 2013, his business made more than $5 million in revenues and the company was valued (in 2014) by KPMG East Africa at $15 million! To date, his company, Helvetic Solar Contractors, has installed more than 6,000 small rooftop solar systems in Tanzania and other East African countries, including Kenya, Uganda, Rwanda and Burundi. Currently, through his Light for Life Foundation, Patrick Ngowi is giving back to his community by providing better access to clean renewable energy.

He has been featured by Forbes as one of ‘10 Young African Millionaires to Watch.’

Case 6: Lorna Rutto (Kenya)

In 2010, Lorna Rutto quit her bank job to start a waste recycling business. Her company, EcoPost, collects and recycles waste plastic into aesthetic, durable and environmentally-friendly fencing posts, an alternative material to wood. Through these efforts, she has contributed immensely towards the conservation of forests, employs hundreds of Kenyans and is expected to create 100,000 new positions in the next 15 years. Her business and its remarkable achievements wouldn’t have been possible without the financial support of international and local NGOs. In 2010, she applied for and won a $6,000 SEED Award which served as start-up capital for her business. In the same year, she won a grant award of $12,700 from the Enablis Energy Globe-Safaricom Foundation. She also won a business plan competition organized by the Cartier Women’s Initiative, and received a prize award of nearly $12,000. Recently, her business attracted an equity investment from the Blue Haven Initiative and the Opus Foundation amounting to USD 495,000. Lorna’s business which started as a small cottage venture has now moved to a large manufacturing facility equipped with advanced recycling machinery.

Case 7: Anna Phosa (South Africa)

Anna Phosa is one of Africa’s most successful pig farmers. She’s often referred to as a ‘celebrity pig farmer.’ But her business journey wasn’t rosy. In 2004, after a close friend introduced her to the business, Anna started her pig farm in Soweto with $100 contributed from her personal savings. She started with only 4 small pigs. In 2008, Anna was contracted by Pick ‘n Pay, the South African supermarket chain, to supply its stores with 10 pigs per week. This was a first breakthrough and the request grew quickly to 20 pigs per week. in 2010, she signed a huge contract with Pick ‘n Pay to supply 100 pigs over the next five years under a 25 million Rand deal – that’s nearly $2.5 million. With a contract in hand, Anna received funding from ABSA Bank and USAID to buy a 350-hectare farm property. Currently, her farm employs about 20 staff rearing 4,000 pigs at a time.

Case 8: Aliko Dangote (Nigeria)

Africa’s richest man, Aliko Dangote, currently worth $18.3 billion, is a role model to entrepreneurs on the African continent. While his business interests currently spread across Africa, Dangote’s impressive fortune was built from very humble beginnings. He started his business in 1978 with 500,000 Naira borrowed from his grandfather. Yes, his grandfather. And because business flourished, he paid back the loan in just six months. In the early years, Dangote focused on importing soft commodities, especially rice, frozen fish, sugar and baby food into Nigeria. Today, his business interests have expanded into local production of cement, salt, flour and very recently, petroleum refining. His aggressive business expansion and diversification efforts have led to huge investments in Nigeria, Benin, Cameroon, Ghana, South Africa, Togo, Tanzania, and Zambia.

Dangote is really consolidating his wealth and may just remain Africa’s richest man in the coming years.

Case 9: Fred Deegbe (Ghana)

Fred Deegbe is the brain behind Heel The World, a luxury footwear brand that’s wholly made by hand by skilled craftsmen in Ghana. In 2011, he quit his bank job to found the business, which he started from his parents’ house in Accra, Ghana. Fred’s startup story is another classic example of bootstrapping at work. Using savings from his bank job, and the help of his business partner, Vijay Manu, he bought shoe machines and equipment, and hired the first set of workers.

Today, Heel The World has an impressive range of footwear – anything from retro brogues and elegant loafers, to stylish dress slippers and eye-catching Oxfords. Fred Deegbe has been featured on the BBC and CNN. In 2012, he was on the panel at the World Economic Forum in Addis Ababa, Ethiopia.

Case 10: Desmond Mabuza (South Africa)

In an industry dominated by white South Africans, Desmond Mabuza is the first black person to own and successfully operate a fine dining restaurant business that serves his country’s rich and famous people. Born and raised in a poor neighbourhood in Soweto, and trained as a civil engineer in the United States, Desmond returned to South Africa before the end of the Apartheid era to start a small civil engineering firm. After a few years, he abandoned his engineering practice and invested the money he had made into the fine dining restaurant business. He opened his first restaurant in 2001 (at age 28) and currently owns two remarkably profitable and well-run restaurants – Signature and Wall Street – both situated in Johannesburg. In 2014, he opened another Signature restaurant in Abuja, Nigeria and is already making moves to expand the brand across Africa.

CONCLUSION: FROM THE EXOGENOUS AND ENDOGENOUS GROWTH THEORY

Economics has its underpinnings in the growth of markets. This is the standpoint of basic and famous British economists, from Adam Smith to David Ricardo to Alfred Marshall. Since the neo-classical economics or the Walrasian System was laid down in the first decades of the 20th century, neo-classical theorists have been reluctant to expand their models. According to neo-classical or exogenous growth theory, the main determinants of long-run economic growth are not influenced by economic incentives of human agents that are the core ingredient of Schumpeter’s thinking. The analysis on growth factor of nations has been based on residual analysis. Solow (2000) advanced the neo-classical growth model. Later, Solow explained that the technology progress in western countries has been the most important input factor allowing long-run growth in real wages and the standard of living. Solow (1987) referred to the rivalry (or occasional complementarities) as the catalyst of innovations. Solow appreciated Schumpeter’s thinking. The new or endogenous growth theory has become popular during the last decades, when Romer (1990) recognized that technology (and the knowledge on which it is based) has to be viewed as an equivalent third factor along with capital and land in leading economies. Romer has found that an economy’s increased openness raises domestic productivity, and hence has a positive effect on the living standards of a nation. Endogenous growth theory is based on the idea that the long-run growth is determined by economic incentives. Like Schumpter, Romer maintains that inventions are intentional and generate technological spillovers that lower the cost of future innovations. An educated workforce plays a special role in determining the rate of long-run growth. This is the challenge of Africa in the light of Naude (2017).

For African firms to be able to integrate into the global value chain and to increase their inter-regional trade activities, most countries in Africa should not only be specialized in or dependent on extracting and exporting primary commodities but need to add value. Consequently, infrastructure development such as roads, rail lines, energy, and physical network to support international trade should be aggressively embarked upon. Limited infrastructure increases the costs of getting products to the market. For entrepreneurship and international business to serve as catalysts for economic growth in Africa, governments should have the political courage to fight corruption which impedes the innovativeness of the firms to compete successfully in the international market arena. Improvement in weaker governance structures is required to eliminate fraud, many non-tariff barriers to trade such as cross-border restrictions that delay trade flows and invest in growth of R&D expenditures. Additionally, African countries need to increase regional cooperation and share information on key areas of economy. Increased regional trading blocs like economic community of west African states (ECOWAS), East African Community, Southern African development cooperation (SADC), etc., should provide a firm foundation in attracting foreign direct investment. The latter is a good leverage for international business and entrepreneurship. For these regional economic and trading blocs to achieve success, individual and regional governments have to provide requisite legal and policy frameworks that support the operationalization of the blocs. Additionally, each state must reorient their educational, social, developmental, trade and political agendas to facilitate integration.

REFERENCES

- Burenstam-Linder, S. (1961). An Essay on Trade and Transformation. Stockholm, Sweden: Almqvist & Wicksley.

- Chamberlin, E. (1933). The theory of monopolistic competition. Cambridge, MA: Harvard University Press.

- Chandler, A. (1962). Strategy and structure. Cambridge, MA: The M.I.T. Press.

- Chandler, A. (1990). Scale and scope. The dynamics of industrial capitalism. Cambridge, MA: The Belknap Press of Harvard University Press.

- Coleman, D. (1980). Mercantilism Revisited, The Historical Journal, 23(4), 773-791.

- Dahmen, E. (2016). Schumpeterian Dynamics. Some Methodological Notes. In R. Day & G. Eliasson (eds.), The dynamics of market economies, Stockholm, Sweden: Elsevier Science Ltd.

- Donnelly, T., & Hyry, M. (2014). Urban and Regional High Technologies: The Case of Oulu, Local Economy, 19(2), 134-149.

- Drucker, P. (1985). Innovation and entrepreneurship. London: Heinemann Publishers.

- Fitch, C. A., & Myers, S. L. Jr. (2000). Testing the survivalist entrepreneurship model. Social Science Quarterly, 81(4), 985-991.

- Galbraight, J. K. (1956). American capitalism: The concept of countervailing power. Boston, MA: Houghton Mifflin.

- Garcia-Cabrera, A. M., & Garcia-Soto, M. G. (2008). Cultural differences and entrepreneurial behaviour: an intra-country cross-cultural analysis in Cape Verde. Entrepreneurship and Regional Development, 20(5), 451-483.

- Helpman, E. & Krugman, P. (2005). Trade policy and market structure. Cambridge, MA: MIT Press.

- Iwuoha, J. P., & Bokrezion, H. (2015). 101 ways to make money in Africa: Lucrative business ideas, inspiring success stories, and business opportunities. Blurb Publications. Accessed on 17 February, 2024 at: https://www.linkedin.com/pulse/how-10-super-successful-african-entrepreneurs-raised-money-iwuoha/

- Jensen, M. (1993). The Modern Industrial Revolution, Exit, and Failure of Internal Control Systems. Journal of Finance, 48(3), 831-880.

- Krugman, P. (1991). Geography and Trade, Cambridge, Cambridge University Press.

- Kuada, J. (2015). Entrepreneurship in Africa – a classificatory framework and a research agenda. African Journal of Economic and Management Studies, 6(2),148-163. Accessed on October 23, 2023 @ http://dx.doi.org/10.1108/AJEMS-10-2014-0076

- Lahti, A. (1983). Strategy and Performance of a Firm: An empirical investigation in the knitwear industry in Finland 1969-1981 (dissertation), Helsinki School of Economics, A-41, Helsinki.

- Lahti, A. (1989). A Contingency Theory of Entrepreneurial Strategy for a Small Scale Company Operating from a Small and Open Economy in Open European Competition. Entrepreneurship & Regional Development, 1, 221-236.

- Lahti, A. (1991). Entrepreneurial Strategy Making, Arenas of strategic thinking. In N. Juha (eds.). Helsinki, Finland: Foundation of Economic Education (pp.146-162).

- Lahti, A. (2000). Creative Entrepreneurship and New Economy: The Challenge of the Nordic IT Cluster. Helsinki, Finland: Publications of Helsinki School of Economics.

- Lahti, A. (2007). The resource-based exporting and industrialization – how to learn from the Nordic countries? The UNECA/ The ADP: Africa’s Economic Conference, Addis Ababa, 2007.

- La Pira, F. (2010). The motivational drivers of repeat entrepreneurs. Available at: www.aabri.com/OC2010Manuscripts/OC10002.pdf (Accessed 24 October 2023).

- Levitt, T. (1983). The Globalization of Markets, Harvard Business Review, 1983: May-June.

- Lintunen, L. (2000). Who Is the Winner Entrepreneur? An Epistomological Study of the Schumpeterian Entrepreneur (dissertation), Helsinki School of Economics, series A-180, Helsinki, Finland.

- Luostarinen, R. (1979). Internationalization of the firm. An empirical study of the internationalization of the firm with small and open domestic markets with special emphasis on lateral rigidity as a behavioral characteristic in strategic decision making (dissertation), Helsinki School of Economics, A-30, Helsinki, Finland.

- Maritz, A. (2004). New Zealand necessity entrepreneurs. International Journal of Entrepreneurship and Small Business, 1(3/4), 255-264.

- Marshall, A. (1920). Principles of economics. An introductory volume. London: Macmillan.

- McGee, J., & Thomas, H. (1986). Strategic Groups: Theory Research and Taxonomy. Strategic Management Journal, 7(2), 141-160.

- Naude, W. (2017). Peace, Prosperity, and Pro-Growth Entrepreneurship, WIDER Discussion paper, 2017/2.

- North, D. (1993). Institutions, institutional change and economic performance. Cambridge, MA: Cambridge University Press.

- North, D., & Smallbone, D. (2006). Developing entrepreneurship and enterprise in Europe’s peripheral rural areas: some issues facing policy-makers. European Planning Studies, 14(1), 41-60.

- Ohlin, B. (1933). Interregional and international trade. Cambridge, MA: Harvard University Press.

- Porter, M. (1990). Competitive advantages of nations. New York: Macmillan Free Press.

- Putnam, R., Leonardi, R., & Nanetti, R. (2013). Making democracy work: Civic traditions in modern Italy. Princeton, NJ: Princeton University Press.

- Ricardo, D. (1817). On the principles of political economy and taxation. Ontario, Canada: Batoche Books. https://socialsciences.mcmaster.ca/econ/ugcm/3ll3/ricardo/Principles.pdf.

- Robson, P. (1993). The New Regionalism and Developing Countries. Journal of Common Market Studies, 31(3), 329-348.

- Romer, Paul (1989). Increasing return and new development in the theory of growth. Chicago, IL: National Bureau of Economic Research.

- Sassen, S. (2011). Global cities. Princeton, NJ: Princeton University Press.

- Saxenian, A. (2014). Culture and competition in Silicon Valley and Route 128. Cambridge, MA: Harvard University Press.

- Schumpeter, J. A. (1950). Capitalism, socialism and democracy. New York: Harper Perennial Modern Classics.

- Schumpeter, J. A. (1934). The theory of economic development. Cambridge, MA: Harvard Economic Studies.

- Schumpeter, J. A. (1939). Business Cycles: A theoretical, historical, and statistical analysis of the capitalist process. New York: McGraw-Hill.

- Silver, D. (1985). Entrepreneurial megabucks. The 100 greatest entrepreneurs of the last 25 years. New York: John Wiley & Sons.

- Smith, A. (1976). An inquiry into the nature and causes of the wealth of nations. Oxford, MA: Clarendon Press.

- Solow, R. M. (1987). Lecture to the memory of Alfred Nobel, December 8, 1987: Growth Theory and After.

- Solow, R. (2000). Growth theory: An exposition. London: Oxford University Press.

- Stigler, G. J. (1968). The Organization of Industry. Chicago, IL: University of Chicago Press.

- The World Bank’s Global Economic Prospects 2017

- UNCTAD (2016). World Investment Report 2016: Promoting Linkages, New York and Geneva, United Nations.

- World Bank Group (2018). Global Economic Prospects, June 2018. Washington, DC: https://openknowledge.worldbank.org/handle/10986/29801