Behavioural Intention to Use Forensic Audit Services for Enhanced Financial Reporting Quality of North-Central Universities in Nigeria

- Kamaluddeen Funsho Adisa Ibrahim

- Sylvester Onyekachi Ademu

- 938-959

- Jul 4, 2024

- Accounting & Finance

Behavioural Intention to Use Forensic Audit Services for Enhanced Financial Reporting Quality of North-Central Universities in Nigeria

Kamaluddeen Funsho Adisa Ibrahim, Sylvester Onyekachi Ademu

Department of Accounting; University of Abuja, Nigeria

DOI: https://dx.doi.org/10.47772/IJRISS.2024.806072

Received: 16 May 2024; Accepted: 31 May 2024; Published: 04 July 2024

ABSTRACT

This study examined the behavioural intention to use forensic audit service for the enhancement of financial reporting quality of North-central Universities in Nigeria. The study adopts survey research design. Primary data were sourced to elicit responses from sampled audit firms (practitioners) using a four point scale Likert structured questionnaires that were distributed to a sample size of Two Hundred and thirty-eight respondents. Partial Least Square based Structural equation modelling (PLS-SEM) was employed in the investigation’s data analyses. Seven hypotheses were tested in the study. The path analysis results revealed that five out of the six hypothesized paths (perceived severity of financial fraud, perceived vulnerability to fraud, perceived collapse avoidance, perceived benefits of forensic accounting, and perceived financing preference have significant positive effects on the behavioral intention to use forensic audit services) were statistically significant (p < 0.05). However, the path from perceived risks of forensic audit to behavioral intention to use forensic audit services was not statistically significant. From the study outcomes, it was concluded that university management in Nigeria would accept use of forensic accounting for enhancing financial reporting quality if they understand the benefits, collapse avoidance, fraud susceptibility and fraud severity in their institutions. it was recommended among other options that management of Nigerian universities should ensure regular forensic audit to improve the quality of their financial reports while continuous training and retraining of both the audit and staff of in forensic accounting procedures and processes be provided to enable them meet up with the global best practices in financial reports.

Keywords: Behavioural Intention, Financial Reporting Quality, Forensic Audit Service, North-Central Universities

INTRODUCTION

The bane of mismanagement that eroded Federal universities about three decades ago, constituting one of the major causes of under-funding has mounted increasing pressure on the accounting profession to find better solutions to mitigation of financial crimes in Nigerian tertiary educational institutions. The overall essence of financial reporting for Government units is to provide high-quality financial information (as distinct from financial statement preparation and presentation) for making economic, political and social decisions and to demonstrate accountability and stewardship. Financial reporting quality refers to the capacity of an entity’s reported results to represent its true earnings or incomes. A number of forensic indices were used by investors, analysts, and management to aid forensic auditors in determining the likelihood that a company may mismanage or manipulate its performance index (Ibanichuka et al., 2020).

Forensic audit is no longer a new specialty because of its rapidly growing demand globally. Since it is still relatively young in emerging countries, university accountants in Nigeria are not well-versed in forensic accounting difficulties specific to the university accounting system (Osho, 2017).

Problem Statement

Forensic audit plays an increasingly pivotal role in fraud investigation, litigation support and other legal disputes fomented by fraud and business failure but little has been done in the area of University financial reporting system. This raises a doubt and inexplicability on University Management’s behavioural intention to utilize forensic audit services for enhanced financial reporting quality in spite of the pecuniary nature of the public tertiary institutions’ financial system which mainly encompasses financial accounting, financial and management reporting and research grant accounting.

In an attempt to carry out investigation on the behavioral intentions of University Management to utilize forensic audit service, three theories were employed, namely the Protection Motivation Theory (PMT), Forensic Accounting Theory (FAT) and Pecking Order Theory (POT). Where PMT provides threat appraisal variables, FAT contributes to the collapse avoidance variables in forensic audit perspective. POT involves the funding preference decision variable for meeting the cost of using forensic audit services. Previous empirical studies (Efionget al., 2016; Osho, 2017; Azman & Vaicondam, 2020; Milaham & Milaham, 2020; Azman, 2021) focused on behavioural intention to use forensic accounting services but none of them attempted to adopt a tripartite approach by combining PMT, FAT and POT to investigate behavioural intentions of Universities’ management, especially in Nigeria.

In light of the aforementioned, this study will expand our understanding of the relationship between forensic audit and the caliber of financial reporting at Nigeria’s federal institutions by filling in the gaps left by the shortcomings outlined above. The study is supported on the grounds that scholars, practitioners, and significant stakeholders in Nigerian tertiary institutions will benefit from it, both theoretically and practically. It is intended that the policy options advanced based on the research findings will be of immense relevance to improve the quality of financial reporting in all tertiary educational institutions, given the growing role of forensic audits in bridging the expectations gap between users of financial statements and the statutory auditors.

Objective(s) of the Study

The main objective of this study is to examine the behavioural intention to use forensic audit services for enhanced financial reporting quality of Federal universities in Nigeria.

The specific objectives of the study are to:

- investigate the influence of threat severity on Nigerian university management’s intention to use forensic audit services for enhanced financial reporting quality.

- evaluate the effect of threat vulnerability on Nigerian university management’s intention to use forensic audit services for enhanced financial reporting quality.

- ascertain if collapse avoidance on Nigerian universities’ management affects the intention to use forensic audit services for enhanced financial reporting quality.

- examine if perceived funding preference influences university management’s intention to use forensic audit services for enhanced financial reporting quality.

- evaluate the impact of universities’ perceived risks on the intention to use forensic audit services for enhanced financial reporting quality.

- assess the impact of universities’ perceived benefits on the intention to use forensic audit services for enhanced financial reporting quality.

LITERATURE REVIEW

Concept of Forensic Audit

In forensic auditing, information is gathered, validated, processed, analyzed, and reported with the goal of obtaining facts and proof regarding financial irregularities within a predefined framework (Mohd & Mazni, 2008; Cabole, 2010; Abdi (2017). According to Enofeet al.(2015), the term “forensic audit” describes how investigative auditing, criminology, litigation support, and financial expertise are summarized and applied to the task of detecting fraud. Manuel and Kumara (2019) forensic audit can be defined as a financial fraud investigation that involves the examination of accounting records to confirm or refute the financial fraud as well as the presentation of the financial fraud as an expert witness in court. Thus, forensic audit can be defined as the application of accounting, auditing, and investigative mindset to the review of an organization’s financial records with the goal of extracting evidence that can be utilized in a court of law or other legal procedure.

The performer of forensic audit function (i.e. forensic auditors) are described by Eyisi and Agbaeze (2014) as professionals in the field of finance who are skilled at identifying, looking into, and discouraging white collar crimes and fraud that should be brought up in court or for public discussion and debate.

Forensic Audit Services

Ibrahim (2018) identifies forensic audit services to include using an intuitive approach, we provide a wide range of services including litigation support engagement, fraud investigation, expert witnessing, forensic expert consultation, conflict resolution, and more. In the same vein, Imoniana et al.(2013) include a list of the most common areas in which forensic audit services are used, such as calculating economic damages, providing litigation support, investigating business and employee fraud, financial and securities fraud, business failures and interruptions, computer forensics and e-discovery, locating hidden assets, and cases of professional negligence and matrimonial disputes.

Firms providing forensic audit services demand a transparent and thorough audit strategy intended to collect information on the who, what, when, and how of any fraud perpetrated it. As accentuated by Akenbor and Ironkwe (2014), such audit plan must have clearly stipulated objectives and timeliness as well as list the necessary skills, the approximate cost, and any restrictions on the range of the tests.

Threat Severity

Threat severity plays an important role as a predictor of fear in any circumstance, whether in weak or strong fear situation. According to Muthusamy et al. (2011), the motivation to use FAS for enhanced financial reporting quality stems out of the particular expectations that it could minimize the occurrence or intensity of harms. In the words of Lin and Bautista (2016), an individual’s attitude would depend on the degree of threat severity; if the degree of fraud is larger, the person will be more motivated to carry out the advised response.

Threat Vulnerability

An individual’s attitude depends on the vulnerability degree of threats, where the motivation of the individuals to perform the suggested responses would be greater if the vulnerability level of fraud is higher (Hameed & Arachchilage, 2019). It means if the vulnerability is low on threats, the motivation of persons to secure themselves from the threats will also be low.

Das and Khan (2016) describe perceived vulnerability as the probability that threats could bring forth negative outcomes. Arachchilage and Love (2016) posit that susceptibility, intensiveness, and the interactions between the two to be fundamental in determining threat perception in any situation.

Collapse Avoidance

This is one of the variables categorized as non-accounting decision hypothesis under forensic accounting theory which advocates for forensic accounting method utilization to unearth irregularities without causing any downfall or making the individual or the entity to collapse but to be punished by the court and not by the forensic investigator (Ozili, 2020). In other words, the forensic investigators must assure the management of the entity that the result of their investigation would lead to correction of the wrongdoing and not to cause the entity to wind up.

Collapse avoidance can also be used to mediate the effect of severity and vulnerability on the behavioural intention (Azman, 2021). It therefore, follows that severity and vulnerability constitute threat appraisal factors where behavioural intention acts as the dependent variable as derived from PMT in the quest to study the purpose of forensic audit services is to assist firms in reducing fraud and rectifying deliberate manipulation or alteration of important financial records and accompanying documentation.

Institution’s Decision on Revenue Sources and Associated Costs

In addition to sources of fund generated through subvention and as an avenue of proffering solution to the endless financial problems in the nation’s universities have broadened the range of sources of income they generate internally to encompass grants, student fees, commercial enterprises, alumni relations associations, private contributions, tertiary education trust funds, and research and consulting services (Dimunah, 2017). Despite many existing avenues for resource mobilization, there is persistent complaint from different stakeholders about tertiary institutions’ inabilities to generate sufficient revenues. Prioritization of sources of finance in tertiary educational institutions are expected to always be based on the cost of raising such funds through different means (Onen, 2016).

Be that as it may, management’s decision on revenues and associated cost of earning revenues is very important owing to cost and benefit of undertaking a forensic audit engagement. Investigation into every reported fraud case may be too costly (Ozili, 2020).

Funding Preference

The literary definition of credit policy as obtained in Cambridge Business English Dictionary (2016) refers to a set of principles that financial institutions employ to decide on who are entitled to be granted credit facility. Generally, Government often restricts publicly-owned institutions’ involvement in debt and equity financing (Onen, 2016).

The enabling Laws of the Nigerian public-owned universities establishing it and the Universities (Miscellaneous Provisions – (Amendment) Act 2012 often contain elaborate provisions on the functions of the Governing Councils which end with an omnibus clause empowering it to borrow money on behalf of their Universities. This can be interpreted to mean that the law only permits the Governing Council of each university to source for temporary borrowing by means of overdraft or otherwise, which must be repaid within a short period for any urgent requirements in the discharge of its statutory functions. Albeit, borrowing remains one regular means of raising funds especially in case of any urgent requirements in any institution, it is a more expensive means of financing institutional activities. However, this factor also affects university management’s unwillingness to use forensic audit services for enhanced financial reporting qualities.

Behavioural Intention

Behavioural intention is an indication of peoples readiness to carry out some particular behavior. This is based on assumption of a straightaway precedence of conduct (Ajzen, 2002). This connotes that intention is assumed to capture the motivational factors that affect a behavior. According to (Ajzen, 1991), an intention indicates how hard individuals are willing to try and how much of an effort they are planning to exert in order to perform the behavior. Therefore, threat appraisal, non-accounting decisions, decisions on revenues and associated costs/institutions’ credit policy significant factors determining the behavioural intention of university management to use forensic audit service for enhanced financial reporting quality.

Concept of Financial Reporting Quality

Financial reporting is concerned with whether a company’s stated performance accurately captures its actual profits or earnings (Ibanichuka et al.,2020). In other words, it refers to the capacity of a business’s reported results to most accurately represent its actual profits (Warshavsky, 2012). It then follows that the main purpose of financial reporting is to give economic organizations with high-quality financial reporting data, primarily of a financial nature, so they can make informed economic decisions (FASB, 2008).

In the words of Epistein and Jermakowicz (2010) while citing IASB (2008), elucidate further that the attributes of financial reporting can be divided into two categories: enhancing and essential qualitative traits. Relevance and faithful depiction are the two most crucial underlying qualitative traits that define the substance of financial reporting information. According to them, when the fundamental qualitative qualities are established, the enhancing qualitative characteristics—which are understoodability, comparability, verifiability, and timeliness—are intended to increase decision usefulness. However, they are insufficient to assess the quality of financial reporting on their own.

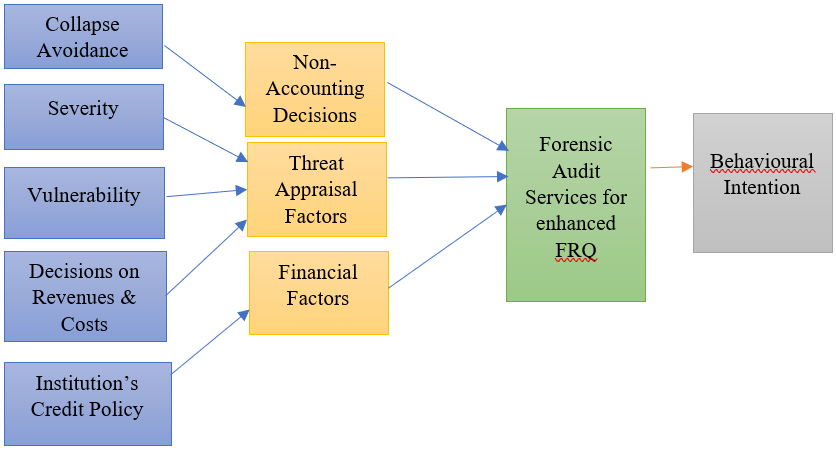

Conceptual Framework

The following conceptual framework has been developed from the TFA, PMT and POT:

Figure 2.1: Conceptual Model for Use of Forensic Audit Services for Financial Reporting Quality

Source: Modified Model from the work of Azman (2021).

From Figure 2.1, the conceptual framework has been developed using three types of variables, namely: the mediating variable (Collapse Avoidance), independent variables (Severity, Vulnerability, Revenue/Cost Decisions and Institutions’ Credit Policy) and dependent variable (Behavioural Intention). The collapse avoidance, an element of non-accounting decisions derived from FAT theory is chosen because of reluctant attitude of most organizations to use forensic audit services occasioned by fear of having bad image and outright liquidation (Azman, 2021).

Severity and vulnerability are integral parts of threat appraisal factor extracted from PMT theory which are also found to constitute most significant variables that determine the intention of individuals or companies to adopt a security response or behaviour (Bashirian et al., 2020; Ruan et al., 2020; Azman, 2021). Revenue/Cost decisions and Institution credit policy are also drawn from POT theory because of their relevance in institutions’ financial decisions which in turn affect their intentions to use forensic audit services.

Theoretical Review

Relevant theories proposed to underpin the study are FAT, PMT and POT which are meant to guide in the search to understand the behavioural intention to use forensic audit services for enhanced financial reporting quality. Each of these theories has its strength and weaknesses with different theoretical conclusions.

Forensic Accounting Theory (FAT)

Previous accounting scandals, new dimensions of fraud schemes in the world of advanced technologies as well as frequent changes in accounting policies and procedures by firms in the preparation of financial reports provoked the development of FAT by Peterson K. Ozili in 2020. The present leading researcher to first adopt this theory is Azman (2021) to examine the moderating influence of collapsed avoidance confidence on behavioural intentions to employ forensic accounting.

FAT describes the selection, application, and results of specific methods and techniques for the purpose of identifying creative accounting practices and fraudulent financial statement manipulations. The methods and techniques are chosen based on the accounting and non-accounting decisions that the forensic accounting investigator considers. For this reason, the theory gave birth to five constructs/hypotheses which are grouped under both accounting and non-accounting decisions. According to Azman (2021), two of these constructs (namely: materiality and ability signaling) constitute accounting decision hypotheses while the three others (bonus contract, anonymity and collapsed avoidance) relate to non-accounting decision hypotheses.

Ozili (2020) describes materiality as a variable which requires a forensic investigator to choose fraud detection techniques capable of determining if the unresolved case is material or not under legal and regulatory contexts. The ability signaling is based on the capability of the forensic investigators to uncover irregularities using the appropriate method to enhance their integrity, market and establish themselves as authorities in the industry (Ireland, 2011; Ozili, 2020). Bonus contract is based on compensation or remuneration to forensic investigator for work done (Christ et al, 2012). Anonymity refers to choice of a method to hide the identity of the forensic investigator in the event of any case threatening his safety (Chang, 2008; Azman, 2021). Collapse avoidance is based on a goal that forensic investigation should not be meant see the downfall of an accused individual or corporation but to uncover unresolved cases (Azman, 2021).

This study extracted only the collapse avoidance hypothesis from FAT theory in view of its power to demystify erroneous notion about forensic investigative goal which most organizations believe could bring about the collapse of the entity being investigated. The weakness of FAT theory is that, it does not take into consideration a firm’s financial decision (cost and benefit analysis) which is very crucial in using forensic audit services.

Protection Motivation Theory (PMT)

PMT was first developed by Rogers (1975) with its most recent iteration in 1983. The essence of its proposition was to give better understanding of why and how people react to possible threats to the peoples’ wellness and safety (Clubb & Hinkle, 2015). In other words, the theory is concerned with protective behavior which is connected to fear and self-protection. In this case, the fear element is the threat appraisal while the self-protection elements involves coping appraisal (Bashirian, 2020; Azman, 2021).

Under threat appraisal are severity and vulnerability variables (Hinkle & Yang, 2014; Kessler, 2016). This coping assessment has tripartite variables, such as: response efficiencies, self-efficiency as well as the response costs. Responses efficacy refer to the people’s belief or perceptions of whether or not a particular protective response is capable of mitigating a given threat (Rogers, 1983; Jansen, 2015).

Self-efficacy implies self-confidence of a person whether he would have the ability to apply the protectiveness in such a manner that it would be efficient to prevent the possible threats (Clubb & Hinkle, 2015). Response cost which is the third coping appraisal is the effort, time and cost required to adopt the coping response (Kusyanti & Catherina, 2018).

P.M.T. model was primarily dedicated to health-related research, but has been frequently adopted for better understanding of how protective actions against the threat of potential criminal actions may be similarly motivated. Leading researchers in PMT Model application include but not limited to Weinstein (1987) who examined understanding and encouragement of self-protective behavior; Skogan (1990) who investigated disorder and decline; Jackson (2009) who studied psychological perspective on vulnerability in the fear of crime; Clubb and Hinkle (2015) who assessed protection motivation theory as a theoretical framework for understanding the use of protective measures; Ozili (2020) who developed forensic accounting theory; Azman (2021) who evaluated mediation effect of collapse avoidance assurance on the behavioural intention to use forensic accounting.

Research using PMT model to investigate individual and contextual characteristics attributable to the use of certain protective measures often reveal several common patterns but faces two key limitations, the first of which is giving little consideration to other forms of protective behavior, especially to protect the individuals and property against criminal victimization within the home setting. Secondly, notwithstanding that studies employing PMT model to confirm the use of protective measures provide valuable information for understanding the use of protective measures, different variables and methods adopted makes comparison across studies extremely difficult. With reference to previous studies, PMT influences attitude and intention (Karahoca et al., 2019; Azman & Vaicondam, 2020).

Pecking Order Theory (POT)

The first researcher to introduce POT model was Donaldson in 1961 and later modified by Stewart C. Myers and Nicolas Majluf in 1984. The theory states that an entity first financing preference should be through retained earnings generated internally. In the event of this finance source not available, it should then opt for debt financing after which equity financing is chosen as a last resort.

Some of the leading researchers in POT model application are Zhang and Kanazaki (2007) who tested static tradeoff against pecking order models of capital structure in Japanese firms; Bensoussan and Crouhy. (2008) who examined stochastic equity volatility and the capital structure of the firm; Buttet al., (2013) who studied static trade-off theory or pecking order theory which one suits best to the financial sector.

However, POT model is confronted with two limitations. Firstly, it does not consider the implications of taxes, agency cost, financial distress of the investment opportunities as well as cost of issuing new securities. Secondly, it ignores the problems associated with financial managers’ decision to amass enough financial cushion so they are shielded from market discipline (Butt, Khan & Nafees, 2013).

Despite the above limitations, POT model is credited with some benefits, one of which is that it helps to explain changes associated to capital structure. It also recognizes managers’ motivation and opens opportunity for firms to create dynamic capital structure.

Review of Empirical Studies

Azman (2021) examined the mediation effect of collapse avoidance assurance on the behavioural intention to use forensic accounting services. Causal- comparative research design was employed with questionnaire as an instrument for data collection. The target respondents were grouped into chief executives, board of directors and audit committee members of the industrial products and services of listed companies in Malaysia. The calculated sample size of 119 was done using GPower software. The study findings revealed severity and vulnerability have significant effect on the intentions to use forensic accounting services in. The research findings also shows that collapse avoidance significantly mediates the effect of severity and vulnerability on the behavioural intentions to utilize forensic accounting.

Ibanichuka et al. (2020) examined the effect of forensic accounting on financial reporting quality of quoted banks in Nigeria.Cross-sectional data from the Nigeria Stock Exchange’s fact books from 2009 to 2018 and audited financial or monetary reports of listed banks were used. Investigative accounting services served as a proxy for the independent variable, whereas accrual quality and value relevance served as proxies for the dependent variables. The method of ordinary least square (OLS) was applied. The fixed effect model was chosen for the investigation since it was the most suitable. The 76% of the variance in accrual quality could be described by the independent variables in first equation. The model’s fitness confirmation was through the F-statistics. Also, the insignificant statistical association was evidenced by the coefficient of the p-value. The findings demonstrated the detrimental effect of investigative accounting on accrual quality. Above sixty percent of the variances in value relevance are explained by the independent variable in the second model. According to the study’s findings, forensic accountants must be hired immediately in order to improve the quality of financial reporting and win over stakeholders. Forensic accountants should also apply the necessary investigative accounting techniques.

Osho (2017) evaluated the effect of forensic accounting on University financial system in Nigeria. Without money, the university could not function, hence the administration of the university had to manage the funds properly to prevent financial mismanagement. Profession Theory and Relative Size Factor Theory are two ideas that are relevant to this study; the literature is studied in accordance with these theories. An ex-post facto research design was used in the study. Information was taken off of the 2005–2014 audited financial statements. Techniques such as stratified and purposive random sampling were used to get the testable conclusion. The results of this study project’s simple and multiple regression analysis showed that the exogenous variables taken together have a substantial impact on Nigeria’s university finance system. It is advised that in order to grow their universities, university management and stakeholders should make decisions based on the study’s conclusions regarding the effective administration of all forensic accounting components.

Muthusamy et al. (2011) studied organizational intention to use forensic accounting services for fraud detection and prevention by large Malaysian companies. A conceptual framework that was comprehensive, economical, and theoretically grounded was employed in the multi-phased mixed-method research design. The significant positive impacts of attitude, stakeholder pressure, and perceived susceptibility on fraud in the organizational intention to utilize F.A.S. for fraud detection alongside prevention was supported by quantitative data analyses by applying PLS from Structural Equation Modeling.

In order to raise knowledge, acceptability, and eventually the usage of forensic accounting services in the fight against fraud, professional bodies, accounting firms, the government, and organizational stakeholders can benefit from the research findings.

Milahan & Milahan (2020) examined the use of forensic accounting in prevention of fraud in Bursary Department, University of Jos, Nigeria. Cross-sectional research was adopted as a design for the study. The Forensic Accounting Skills Checklists for Frauds Detection (F.A.S.C.F.D.) was utilized to produce data from primary and secondary sources. Every employee in the department of bursaries participated in the study. The research questions were analyzed using simple percentages. The results of the study showed that forensic accounting significantly affects the staff’s capacity to investigate fraudulent activity in the university’s bursary department. The outcomes as well revealed that staff members could be demoralized from perpetrating frauds pertaining to cash under the control of theirs through training and application of forensic accounting techniques. According to the report, the University’s management should make sure that the Bursary Department’s financial records are routinely subjected to forensic auditing. Forensic accounting methods and processes should be regularly taught to university bursary staff members so they may stay up to date with worldwide best practices in financial reporting.

METHODOLOGY

The study made use of qualitative with quantitative research design (i.e., mixed method). This study adopted the positivist assumption so that all meaningful problems could be framed in comprehensible frameworks and characterized by precise hypotheses. It adopted positivist approach whose deductive mode of inquiry aims for objectivity, measurability, and controllability. For this reason, both quantitative and qualitative data collection would be utilized.

The target respondents comprise of the accounting academics, senior audit staff of the North-Central universities as well as practitioners in the geo-political zone. Probabilistic and non-probabilistic sampling methods were employed in the survey research process. Close-ended questionnaire and semi-structured interview were used to obtain relevant data from the sampled respondents. Data obtained were analyzed using the structural equation modelling (SEM) technique to examine the relationships between the dependent and independent variables. The SEM is a multivariate statistical technique that is best described as a combination of both factor analysis and path analysis. It allows for examination of a series of dependence relationships between exogenous variables (dependent variables) and endogenous variables (independent or predictor variables) (Ho, 2006).

RESULTS AND DISCUSSION

Data Presentation

The sample consisted of 238 respondents in Nigeria. As shown in table 4.1,The majority of the respondents were male (59.66%), and the age group with the highest representation was 31-40 years (36.97%) and 41-50 years (36.13%). Regarding educational qualifications, most respondents held a Bachelor’s degree (41.18%) or a Master’s degree (34.45%). Additionally, a significant portion of the respondents were certified by professional accounting bodies, with ICAN (63.87%) being the most prevalent certification. In terms of job descriptions, the sample included Chartered Accountants (36.13%), General Accountants (27.73%), Auditors (23.53%), and Forensic Accountants (12.61%).

Table 4.1 Demographic Information

| Gender | Frequency | Percentage | AGE | Frequency | Percentage |

| MALE | 142 | 59.66 | 18 – 30 | 30 | 12.61 |

| FEMALE | 96 | 40.34 | 31 – 40 | 88 | 36.97 |

| TOTAL | 238 | 100 | 41 – 50 | 86 | 36.13 |

| Education | Frequency | Percentage | 51 – 60 | 28 | 11.76 |

| SSCE/OND | 12 | 5.04 | above 60 | 6 | 2.52 |

| BSc. | 98 | 41.18 | TOTAL | 238 | 100 |

| Msc./MBA/MA/Mphil | 82 | 34.45 | Certification | Frequency | Percentage |

| PhD | 46 | 19.33 | ICAN | 152 | 63.87 |

| TOTAL | 238 | 100 | ANAN | 32 | 13.45 |

| Job Description | Frequency | Percentage | ACFA | 2 | 0.84 |

| Auditor | 56 | 23.53 | ICFE | 0 | 0 |

| General Accountant | 66 | 27.73 | IFAN | 30 | 12.61 |

| Chartered Accountant | 86 | 36.13 | IICFIP | 2 | 0.84 |

| Forensic Accountant | 30 | 12.61 | None | 20 | 8.4 |

| Other: | 0 | 0 | TOTAL | 238 | 100 |

| TOTAL | 238 | 100 |

Table 4.2 Descriptive Statistics

| Variable | Mean | Max | Min | Std. Deviation | Skewness | Kurtosis |

| PSF | 10.69 | 15 | 4 | 2.13 | -0.28 | -0.19 |

| PV | 7.58 | 11 | 3 | 1.65 | -0.04 | -0.14 |

| PCA | 12.38 | 16 | 3 | 2.24 | -0.46 | 0.31 |

| PBFA | 10.79 | 15 | 5 | 2.14 | -0.17 | -0.21 |

| PRFA | 6.39 | 9 | 3 | 1.47 | -0.08 | -0.33 |

| PFP | 8.83 | 12 | 3 | 1.89 | -0.22 | -0.05 |

| BIFA | 10.84 | 14 | 7 | 1.52 | 0.02 | -0.13 |

In Table 4.2, The mean value of 10.69 for PSF suggests that respondents generally perceive financial reporting fraud as a severe issue in North-Central Universities in Nigeria. The maximum value of 15 and the minimum value of 4 indicate a wide range of perceptions among the respondents. The responses is negatively skewed (-0.28) and the kurtosis value of -0.19 indicates a platykurtic distribution, which is flatter than a normal distribution. These values imply that while most respondents perceive financial reporting fraud as a severe issue, there is some variation in their perceptions, with a tendency towards higher severity ratings.

For PV, in Table 4.2, The mean value is 7.58 suggesting that respondents perceive a moderate level of vulnerability to fraud in North-Central Universities. The maximum value of 11 and the minimum value of 3 indicate a relatively wide range of perceptions. The skewness value of -0.04 is close to zero, suggesting a nearly symmetrical distribution. The kurtosis value of -0.14 indicates a slightly platykurtic distribution. These values imply that while respondents generally perceive a moderate level of vulnerability to fraud, there is some variation in their perceptions, with a tendency towards higher vulnerability ratings.

The mean value of 12.38 for PCA as shown in Table 4.2 suggests that respondents strongly perceive forensic audit services as a means to avoid institutional collapse. The maximum value of 16 and the minimum value of 3 indicate a wide range of perceptions. The negative skewness value of -0.46 suggests that the distribution is skewed to the left, with more respondents perceiving higher levels of collapse avoidance. The kurtosis value of 0.31 indicates a leptokurtic distribution, which is more peaked than a normal distribution. These values imply that most respondents strongly perceive forensic audit services as a way to avoid institutional collapse, with a tendency towards higher ratings.

PBFA has a mean value of 10.79 in table 4.2 suggesting that respondents generally perceive forensic accounting as beneficial. The maximum value of 15 and the minimum value of 5 indicate a wide range of perceptions. The negative skewness value of -0.17 suggests a slight skew to the left, with more respondents perceiving higher levels of benefits. The kurtosis value of -0.21 indicates a platykurtic distribution, which is flatter than a normal distribution. These values imply that while most respondents perceive forensic accounting as beneficial, there is some variation in their perceptions, with a tendency towards higher benefit ratings.

As shown in Table 4.2, the average respondents’ score mean for PRFA is 6.39 indicating that respondents perceive a moderate level of risk associated with forensic audit services. The maximum value of 9 and the minimum value of 3 indicate a relatively narrow range of perceptions. The skewness value of -0.08 is close to zero, suggesting a nearly symmetrical distribution. The kurtosis value of -0.33 indicates a platykurtic distribution, which is flatter than a normal distribution. These values imply that while respondents generally perceive a moderate level of risk associated with forensic audit services, there is less variation in their perceptions compared to other variables.

The mean value of 8.83 for PFP in Table 4.2 suggests that respondents perceive a moderate level of preference for financing forensic audit services. The maximum value of 12 and the minimum value of 3 indicate a wide range of perceptions. The negative skewness value of -0.22 suggests a slight skew to the left, with more respondents perceiving higher levels of financing preference. The kurtosis value of -0.05 is close to zero, indicating a distribution that is close to a normal distribution. These values imply that while respondents generally perceive a moderate level of preference for financing forensic audit services, there is some variation in their perceptions, with a tendency towards higher preference ratings.

In table 4.2, the Average score for BIFA is at 10.84 implying that respondents generally intend to use forensic audit services in North-Central Universities. The maximum value of 14 and the minimum value of 7 indicate a relatively narrow range of intentions. The skewness value of 0.02 is close to zero, suggesting a nearly symmetrical distribution. The kurtosis value of -0.13 indicates a slightly platykurtic distribution, which is flatter than a normal distribution. These values imply that while most respondents intend to use forensic audit services, there is less variation in their intentions compared to other variables.

Assumption Tests

Test of Normality

The assumption of normality was assessed using the Shapiro-Wilk test on the composite variables. As shown in Table 4.3, most variables did not significantly deviate from a normal distribution (p > 0.05), except for PCA which showed a significant departure from normality. However, given the relatively large sample size (N = 238), the analysis is robust to this minor violation of normality.

Table 4.3 Tests of Normality

| Variable | Shapiro-Wilk | p-value |

| PSF | 0.987 | 0.072 |

| PV | 0.979 | 0.149 |

| PCA | 0.951 | 0.003 |

| PBFA | 0.986 | 0.058 |

| PRFA | 0.972 | 0.062 |

| PFP | 0.981 | 0.115 |

| BIFA | 0.976 | 0.089 |

Test of Multicollinearity

Multicollinearity was assessed by examining the variance inflation factors (VIFs) for all independent variables. As shown in Table 4.4, all VIF values were below the recommended threshold of 5 (Hair et al., 2010), indicating no severe multicollinearity issues.

Table 4.4 Tests of Multicollinearity

| Variable | VIF |

| PSF | 2.41 |

| PV | 1.93 |

| PCA | 2.67 |

| PBFA | 3.15 |

| PRFA | 1.78 |

| PFP | 2.29 |

Test for Heteroscedasticity

The Breusch-Pagan test was conducted to assess the assumption of homoscedasticity (constant variance of errors) in the structural model.

Table 4.4 Breusch-Pagan Test for Heteroscedasticity

| Test Statistic | P-value |

| 8.15 | 0.227 |

The results in Table 4.4 show that the Breusch-Pagan test statistic is not significant (p = 0.227), indicating no presence of heteroscedasticity in the data. Thus, the assumption of homoscedasticity required for structural equation modeling is met. Having satisfied the assumption of homoscedasticity, along with the earlier assumptions of normality and no multicollinearity, the structural model estimation can proceed using the standard methods and output without the need for any corrections or robust standard errors.

Reliability and Validity Analysis

The reliability and validity of the measurement model were thoroughly assessed to ensure the trustworthiness of the study’s findings. Both traditional methods, such as Cronbach’s alpha, and more advanced techniques, including confirmatory factor analysis (CFA) and tests of convergent and discriminant validity, were employed.

Cronbach’s Alpha

Cronbach’s alpha was calculated to assess the internal consistency reliability of the measurement scales. As shown in Table 4.5, all constructs exhibited Cronbach’s alpha values above the recommended threshold of 0.70 (Nunnally & Bernstein, 1994), indicating acceptable reliability.

Table 4.5 Cronbach’s Alpha

| Construct | Cronbach’s Alpha |

| PSF | 0.87 |

| PV | 0.84 |

| PCA | 0.85 |

| PBFA | 0.91 |

| PRFA | 0.81 |

| PFP | 0.77 |

| BIFA | 0.89 |

Confirmatory Factor Analysis (CFA)

CFA was performed to assess the measurement model’s fit and construct validity. The results, demonstrated an acceptable model fit based on various fit indices (e.g., CFI, TLI, RMSEA). Furthermore, all factor loadings were statistically significant and above the recommended threshold of 0.60, indicating convergent validity.

Table 4.6 Factor Loadings, Reliability and Validity

| Construct | Item | Loading |

| PSF | PSF1 | 0.82 |

| PSF2 | 0.81 | |

| PSF3 | 0.85 | |

| PSF4 | 0.76 | |

| PV | PV1 | 0.79 |

| PV2 | 0.86 | |

| PV3 | 0.77 | |

| PCA | PCA1 | 0.68 |

| PCA2 | 0.80 | |

| PCA3 | 0.83 | |

| PCA4 | 0.74 | |

| PBFA | PBFA1 | 0.77 |

| PBFA2 | 0.86 | |

| PBFA3 | 0.92 | |

| PBFA4 | 0.82 | |

| PRFA | PRFA1 | 0.75 |

| PRFA2 | 0.83 | |

| PRFA3 | 0.77 | |

| PFP | PFP1 | 0.70 |

| PFP2 | 0.81 | |

| PFP3 | 0.76 | |

| BIFA | BIFA1 | 0.87 |

| BIFA2 | 0.88 | |

| BIFA3 | 0.76 | |

| BIFA4 | 0.86 |

Convergent and Discriminant Validity

In addition to the factor loadings, convergent validity was further evaluated using the average variance extracted (AVE) values. As shown in Table 4.6, all AVE values exceeded the recommended threshold of 0.50 (Hair et al., 2010), providing evidence of convergent validity.

Discriminant validity was assessed by comparing the square root of the AVE for each construct with its correlations with other constructs. Table 4.6 shows that the square root of the AVE (values on the diagonal) is greater than the inter-construct correlations (off-diagonal values), supporting discriminant validity (Fornell & Larcker, 1981).

Table 4.7 Convergent and Discriminant Validity

| Construct | PSF | PV | PCA | PBFA | PRFA | PFP | BIFA |

| PSF | 0.81 | ||||||

| PV | 0.51 | 0.82 | |||||

| PCA | 0.63 | 0.44 | 0.77 | ||||

| PBFA | 0.58 | 0.39 | 0.51 | 0.85 | |||

| PRFA | 0.27 | 0.31 | 0.28 | 0.35 | 0.78 | ||

| PFP | 0.43 | 0.37 | 0.41 | 0.29 | 0.19 | 0.75 | |

| BIFA | 0.65 | 0.47 | 0.56 | 0.62 | 0.22 | 0.39 | 0.83 |

Diagonal values are square roots of AVE; off-diagonal values are correlations.

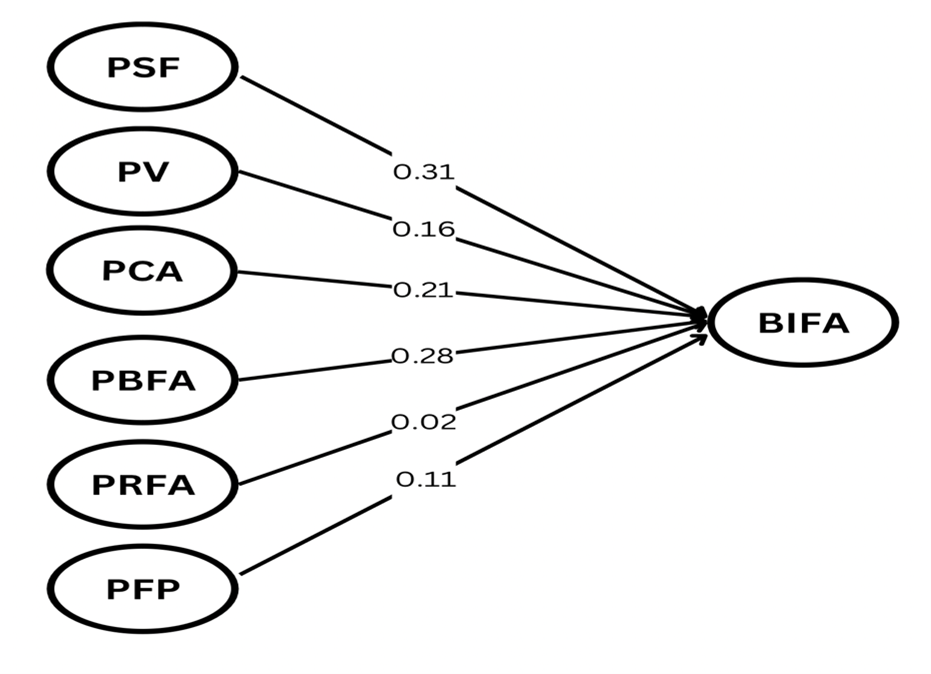

Structural Equation Model (Path Analysis)

After establishing a satisfactory measurement model, the structural model was estimated to test the hypothesized relationships among the study’s constructs. The structural model analysis was conducted using the maximum likelihood estimation method in AMOS. The model included six exogenous variables (PSF, PV, PCA, PBFA, PRFA, PFP) and one endogenous variable (BIFA – Behavioral Intention to Use Forensic Audit Services). The hypothesized paths from the exogenous variables to the endogenous variable were specified.

The path coefficients, representing the strengths and directions of the hypothesized relationships, were estimated as shown in figure 4.1. Table 4.7 presents the standardized path coefficients and their significance levels.

Figure 4.1: Path Diagram

Table 4.8 Path Analysis Results

| Path | Std. Est. | S.E. | C.R. | p-value |

| PSF → BIFA | 0.31 | 0.07 | 4.52 | < 0.001 |

| PV → BIFA | 0.16 | 0.05 | 3.09 | 0.002 |

| PCA → BIFA | 0.21 | 0.06 | 3.67 | < 0.001 |

| PBFA → BIFA | 0.28 | 0.06 | 4.45 | < 0.001 |

| PRFA → BIFA | 0.02 | 0.04 | 0.48 | 0.630 |

| PFP → BIFA | 0.11 | 0.05 | 2.24 | 0.025 |

In Table 4.8, The path analysis results revealed that five out of the six hypothesized paths were statistically significant (p < 0.05). Specifically, Perceived Severity of Financial Fraud (PSF), Perceived Vulnerability to Fraud (PV), Perceived Collapse Avoidance (PCA), Perceived Benefits of Forensic Accounting (PBFA), and Perceived Financing Preference (PFP) had significant positive effects on the Behavioral Intention to Use Forensic Audit Services (BIFA). However, the path from Perceived Risks of Forensic Audit (PRFA) to BIFA was not statistically significant.

Discussion of Findings

The structural equation modeling and path analysis yielded insightful findings regarding the factors influencing the behavioral intention to use forensic audit services in North-Central Universities in Nigeria. The results provide valuable insights into the perceptions, attitudes, and considerations that shape the intention to adopt forensic audit practices in Nigerian tertiary institutions.

In Table 4.8, The path analysis revealed a significant positive relationship between perceived severity of financial reporting fraud and the behavioral intention to use forensic audit services (β = 0.31, p < 0.001). This finding suggests that when university management perceives financial reporting fraud as a severe issue, they are more likely to intend to adopt forensic audit services as a measure to address and mitigate such fraudulent practices. In the context of financial reporting fraud, university management may recognize the potential consequences of such fraudulent activities, including reputational damage, financial losses, and legal implications. Consequently, they may be motivated to take proactive measures, such as implementing forensic audit services, to identify and prevent financial reporting fraud. The finding is consistent with Muthusamy et al. (2010) and Lokanan (2015) that have highlighted the importance of perceived severity in shaping behavioral intentions and decision-making processes related to fraud prevention and detection. It underscores the need for raising awareness about the severity of financial reporting fraud within universities, as this perception can drive the adoption of forensic audit practices.

Perceived Vulnerability to Fraud (PV) revealed a significant positive relationship with the behavioral intention to use forensic audit services (β = 0.16, p = 0.002) as shown in Table 4.8. This finding suggests that when North-Central university managements perceives their institution as vulnerable to fraud may recognize the potential risks and consequences associated with such fraudulent activities, including financial losses, reputational damage, and legal implications and they are more likely to intend to adopt forensic audit services as a protective measure. The finding is in conformity with Muthusamy et al.(2010) which has highlighted the importance of perceived vulnerability in shaping behavioral intentions and decision-making processes related to fraud prevention and detection. The result further supports the need for conducting risk assessments and fostering an awareness of fraud vulnerabilities within universities, as this perception can drive the adoption of forensic audit practices.

In Table 4.8, Perceived Collapse Avoidance (PCA) showed a significant positive relationship with the behavioral intention to use forensic audit services (β = 0.21, p < 0.001). This finding suggests that when university management perceives forensic audit services as a means to avoid institutional collapse, they are more likely to intend to adopt such services. Universities may perceive financial reporting fraud and other fraudulent activities as potential threats to their institutional integrity, reputation, and long-term viability. By adopting forensic audit services, university management may perceive an opportunity to identify and address fraudulent practices proactively, mitigating the risk of institutional collapse or severe consequences that could jeopardize the university’s continued operations. The finding resonates with previous research that has emphasized the importance of organizational survival and avoidance of severe consequences as drivers of organizational decision-making and risk management strategies (Vaughan, 1999; Reason, 2000). The finding highlights the need for university management to recognize the potential consequences of financial reporting fraud and other fraudulent activities, and to perceive forensic audit services as a means to safeguard the institution’s long-term viability.

The path analysis revealed a significant positive relationship between perceived benefits of forensic accounting and the behavioral intention to use forensic audit services (β = 0.28, p < 0.001) as seen in table 4.8. This finding suggests that when university management perceives forensic accounting as beneficial, they are more likely to intend to adopt forensic audit services. In the context of this study, university management’s positive perceptions of the benefits of forensic accounting, such as fraud prevention, detection, and deterrence, as well as improved financial reporting quality and institutional integrity, may shape their attitudes toward the adoption of forensic audit services. The finding is consistent with previous research that has highlighted the importance of perceived benefits in shaping behavioral intentions and decision-making processes related to the adoption of new technologies, practices, or services (e.g., Venkatesh et al., 2003; Lai, 2017). It underscores the need for education and awareness campaigns that highlight the potential benefits of forensic accounting and forensic audit services to university management, as these perceptions can foster a positive attitude and intention to adopt such services.

In Table 4.8, Perceived Risks of Forensic Audit (PRFA) did not have a significant relationship with the behavioral intention to use forensic audit services (β = 0.02, p = 0.630). This finding suggests that university management’s perceptions of the potential risks associated with forensic audit services, such as cost, technological requirements, or additional training needs, do not significantly influence their intention to adopt such services. This result may be interpreted in light of the perceived benefits and potential consequences of not addressing financial reporting fraud. While university management may recognize certain risks associated with forensic audit services, these risks may be outweighed by the perceived benefits and the perceived severity of financial reporting fraud. Additionally, the perceived vulnerability to fraud and the desire to avoid institutional collapse may override concerns about potential risks, leading university management to prioritize the adoption of forensic audit services despite potential risks. While the perceived risks of forensic audit did not significantly influence the intention to use forensic audit services in this study, previous research has highlighted the importance of perceived risks in shaping individuals’ and organizations’ decision-making processes ( Featherman & Pavlou, 2003; Luo et al., 2010). Therefore, further investigation into the specific risks perceived by university management and their relative importance compared to other factors may be warranted.

The path analysis revealed a significant positive relationship between perceived financing preference and the behavioral intention to use forensic audit services in Table 4.8 (β = 0.11, p = 0.025). This finding suggests that when university management perceives a preference for financing forensic audit services, they are more likely to intend to adopt such services. university management’s perception of financing preferences for forensic audit services may be influenced by resource considerations, such as the availability of funds, budgetary constraints, or the perceived value and return on investment associated with adopting these services. The finding is consistent with previous research that has highlighted the importance of resource availability and financing preferences in shaping organizational decision-making processes related to the adoption of new technologies, practices, or services (e.g., Tornatzky & Fleischer, 1990; Oliveira & Martins, 2011). It underscores the need for universities to allocate appropriate resources and develop financing strategies that support the adoption of forensic audit services, as these perceptions can positively influence the intention to adopt such services.

Overall, the findings from the structural equation modeling provide valuable insights into the key factors influencing the behavioral intention to use forensic audit services in North-Central Universities in Nigeria. The significant relationships identified between perceived severity of financial reporting fraud, perceived vulnerability to fraud, perceived collapse avoidance, perceived benefits of forensic accounting, and perceived financing preference with the intention to use forensic audit services offer theoretical and practical implications for understanding and promoting the adoption of forensic audit practices in higher education institutions.

CONCLUSION

The study set out to investigate the factors influencing the behavioral intention to use forensic audit services in North-Central Universities in Nigeria. Through a comprehensive quantitative analysis employing structural equation modeling, several significant relationships were identified. The findings revealed that perceived severity of financial reporting fraud, perceived vulnerability to fraud, perceived collapse avoidance, perceived benefits of forensic accounting, and perceived financing preference positively influenced the intention to use forensic audit services among university management.

The positive relationship between perceived severity of financial reporting fraud and intention to use forensic audit services proves that when university management recognizes the severity of fraudulent financial reporting, they are more likely to seek protective measures such as forensic audits. Similarly, the positive influence of perceived vulnerability to fraud resonates with the same theory, suggesting that a heightened perception of the institution’s vulnerability to fraud motivates the adoption of forensic audit services as a safeguard.

The study also found that perceived collapse avoidance positively influenced the intention to use forensic audit services, underscoring the desire of university management to ensure the long-term viability and continuity of their institutions. By adopting forensic audit practices, they may perceive an opportunity to identify and address fraudulent activities proactively, mitigating the risk of severe consequences or institutional collapse.

Furthermore, the perceived benefits of forensic accounting emerged as a significant positive predictor of the intention to use forensic audit services suggesting that when university management recognizes the potential benefits of forensic accounting, such as fraud prevention, detection, and deterrence, as well as improved financial reporting quality and institutional integrity, they are more likely to develop a positive attitude toward adopting forensic audit services.

The perceived risks of forensic audit services did not significantly influence the intention to use these services, potentially indicating that the perceived benefits and the desire to address financial reporting fraud outweigh the perceived risks in the minds of university management.

Finally, the influence of perceived financing preference on the intention to use forensic audit services highlights the importance of resource considerations and the availability of funds to support the adoption of these practices. There is a need for universities to allocate appropriate resources and develop financing strategies that facilitate the implementation of forensic audit services.

RECOMMENDATIONS

Based on the findings of this study, the study recommends relevant stakeholders to:

- Raise awareness about the severity of financial reporting fraud and its potential consequences within universities. Educational campaigns and training programs can be developed to sensitize university management and stakeholders about the severity of fraudulent financial reporting and their implications for institutional reputation, financial losses, and legal repercussions

- Conduct comprehensive risk assessments to identify threat collapse avoidance, vulnerabilities to fraud within universities. By evaluating existing controls, policies, and procedures, universities can gain insights into their susceptibility to fraud and take proactive measures to address identified vulnerabilities, including the adoption of forensic audit services,

- Workshops, seminars and informational resources can be developed to highlight the potential benefits of regular use of forensic audit services for fraud prevention, detection and deterrence, as well as improved financial reporting quality and institutional integrity. Fostering a positive perception of these benefits can promote a favorable attitude toward adopting forensic audit services.

- Develop financing preference/strategies and allocate resources to support and meet the costs of introducing forensic audit services. Universities should assess their budgetary constraints and explore various financing options, including allocating dedicated funds, seeking external funding sources, or collaborating with relevant stakeholders to ensure the availability of resources for implementing forensic audit services.

LIMITATIONS OF THE STUDY AND SUGGESTIONS FOR FURTHER RESEARCH

While this study provides valuable insights into the factors influencing the intention to use forensic audit services in North-Central Universities in Nigeria, it is important to acknowledge its limitations and suggest avenues for further research:

Geographical Scope: The study focused specifically on North-Central Universities in Nigeria. Future research could investigate the factors influencing the adoption of forensic audit services in universities across different regions of the country or in other countries, considering potential cultural, regulatory, and institutional differences.

Sampling and Generalizability: The study utilized a sample of respondents from North-Central Universities in Nigeria. While the sampling technique aimed to ensure representativeness, future research could employ larger and more diverse samples to enhance the generalizability of the findings.

Cross-Sectional Design: The study employed a cross-sectional design, capturing data at a single point in time. Longitudinal studies or repeated measurements could provide insights into how the factors influencing the intention to use forensic audit services may evolve over time, considering potential changes in institutional contexts, policies, or stakeholder perceptions.

Qualitative Exploration: While the quantitative approach employed in this study provided valuable insights, future research could incorporate qualitative methods, such as in-depth interviews or focus group discussions, to gain a deeper understanding of the underlying motivations, barriers, and decision-making processes related to the adoption of forensic audit services in universities.

Additional Factors: The study focused on specific factors influencing the intention to use forensic audit services. Future research could explore additional factors, such as organizational culture, leadership support, regulatory environment, or industry-specific factors, that may influence the adoption of forensic audit practices in higher education institutions.

Comparative Studies: Conducting comparative studies across different sectors or types of organizations could provide valuable insights into the unique challenges and considerations faced by universities in adopting forensic audit services, as well as identify best practices and lessons learned from other sectors.

Implementation and Impact: While this study focused on the intention to use forensic audit services, future research could investigate the actual implementation and impact of these services within universities, assessing their effectiveness in preventing, detecting, and deterring financial reporting fraud, as well as their influence on financial reporting quality and institutional integrity.

By addressing these limitations and exploring the suggested avenues for further research, a more comprehensive understanding of the factors influencing the adoption of forensic audit services in higher education institutions can be achieved, ultimately contributing to the development of effective strategies and policies to promote transparency, accountability, and ethical practices in financial reporting.

REFERENCES

- Abernathy, J. L., Beyer, B., Masli, A., & Stefaniak, C. (2014). The association between characteristics of audit committee accounting experts, audit committee chairs, and financial reporting timeliness. Advances in Accounting 30 (2):283-297.

- Ajzen, I. (1991). The Theory of Planned Behavior. Organizational behavior and human decision processes. https://www.researchgate.net/publication/272790646.

- Abdi, A.G. (2017). The Impact of Forensic Audit Service on Fraud Detection among Commercial Banks in Kenya. MSc. Dissertation submitted to School of Business, University of Nairobi, Kenya. 1-71.

- Akenbor, C.O. & Ironkwe, U. (2014). Forensic Auditing Techniques and Fraudulent Practices of Public Institutions in Nigeria. Journal of Modern Accounting and Auditin 10(4): 451-459.

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50, 179-211.

- Arachchilage, N. A. G., Love, S., & Beznosov, K. (2016). Phishing Threat Avoidance Behaviour: An Empirical Investigation. Computers in Human Behavior, 60, 185-197

- Azman, N.L.A. (2021). Structural Equation Modelling (SEM) Analysis in Determining the Mediation Effect of Collapse Avoidance Assurance on Threat Appraisal and Intention in Forensic Accounting. Asian Journal of Accounting and Finance, 3(1): 1-9.

- Azman, N.L.A. & Vaicondam.Y (2020). Behavioral Intention in Forensic Accounting Services. International Journal of Psychosocial Rehabilitation, 24: 1837-1846.

- Bashirian, S., Jenabi, E., Khazaei, S., Barati, M., Karimi-Shahanjarini, A., Zareian, S. Moeini, B.(2020). Factors associated with preventive behaviours of COVID-19 among hospital staff in Iran in 2020: an application of the Protection Motivation Theory. Journal of Hospital Infection, 105, 430–433. https://doi.org/10.1016/j.jhin.2020.04.035.

- Bensoussan.A.,M. & Crouhy, D. G. (1995). Stochastic equity volatility and capital structure firm. Mathematical Modeles in Finance. Edited by S.D Howison, F.P Kelly and P. Wilmostt.Published by Chapman and Hall, London. ISBN 0421 63070 2.

- Butt, S., Khan, Z. A., Nafees, B. (2013). Static Trade-off theory or Pecking order theory which one suits best to the financial sector. Evidence from Pakistan. European Journal of Business and Management, 5(23), 131–140.

- Cabole (2009), Forensic Accounting: A paper presented in the Hilton Hotel Lagos, Certified Public Accountant (CPA) Journal, New York accessed on line File;//C:/user/document/accessed on 1/6/2013.

- Cambridge Business English Dictionary. (2016). Definition of credit policy from the Cambridge Business English Dictionary, Cambridge: Cambridge University Press. Downloaded on 20/01/2016 from Cambridge Business English Dictionary.

- Chang, J. (2008). The Role of Anonymity in Deindividuated Behavior : A Comparison of Deindividuation Theory and the Social Identity Model of Deindividuation Effects (SIDE). The Pulse, 6(1), 1–8.

- Christ, M. H., Sedatole, K. L., & Towry, K. L. (2012). Sticks and Carrots: The Effect of Contract Frame on Effort in Incomplete Contracts. The Accounting Review, 87(6), 1913– 1938. https://doi.org/10.2308/accr-50219

- Clubb, A. C., & Hinkle, J. C. (2015). Protection motivation theory as a theoretical framework for understanding the use of protective measures. Criminal Justice Studies, 1–20. https://doi.org/10.1080/1478601X.2015.1050590.

- Dimunah, V.O. (2017). Underfunding of Federal University in Nigeria and Perceived Impact on Administration: An Exploratory Case Study. Ph.D. Thesis submitted to the School of Education, 1-204.

- Efiong, E. J., Inyang, I. O., Mbu-Ogar, G. & Inyang, E. (2016). Accountants’ Behavioural Intention to Use Forensic Accounting Techniques for Fraud Prevention and Detection in Nigeria. Scholars Journal of Economics, Business and Management, 3(7):364-381.

- Enofe, A. 0., Idemudia. N. G. & Emmanuel, G. U. (2015). Forensic accounting a panacea to fraud reduction in Nigeria firms. Journal of Accounting and Financial Management. Vol. 1(8), 49-64. www.iiardpub.org.

- Epstein, B J. & Jermakowicz, E. K. (2010). Wiley Interpretation and Application of International Financial Reporting Standards. Hoboken, New Jersey: John Wiley & Sons, Inc.

- Eyisi, A.Z. & Agbaeze, E.K. (2014). The impact of forensic auditors in corporate governance. International Journal of Development and Sustainability. 3(2): 404-417.

- Featherman, M. S., & Pavlou, P. A. (2003). Predicting e-services adoption: A perceived risk facets perspective. International Journal of Human-Computer Studies, 59(4), 451-474.

- Hameed, M.A. & Arachchilage (2019). Impact of Perceived Vulnerability in the Adoption of Information Systems Security Innovations. International Journal of Computer Network and Information Security, 11(4): 9-18.

- Hinkle, J. C., & Yang, S. (2014). A new look into broken windows: What shapes individuals’ perceptions of social disorder? Journal of Criminal Justice, 42, 26–35.

- Ho, R. (2006) Handbook of Univariate and Multivariate Data Analysis and Interpretation with SPSS. Broken Sound Parkway NW: Queensland University Rockhampton.

- IASB (2008). Exposure Draft on an improved conceptual framework for financial reporting: The objective of financial reporting and qualitative characteristics of decision-useful financial reporting information. London

- Ibanichuka, E. A. L., Ejimofor, L. C. & Okwu, P. I. (2020). Forensic Accounting and Quality of Financial Reporting of Quoted Banks in Nigeria. International Journal of Innovative Finance and Economics Research, 8(3):77-91.

- Ibrahim, K.F.A. (2018). Effect of Forensic Accounting on Fraud Detection in the Nigerian Deposit Money Banks. Ph.D Thesis Submitted to the School of Postgraduate Studies, Nasarawa State University Keffi, Nigeria, 1-169.

- Jackson, J. (2009). A psychological perspective on vulnerability in the fear of crime. 15 (4): 1-25.

- Jansen, J. (2015). Studying Safe Online Banking Behaviour : A Protection Motivation Theory Approach. In Proceedings of the Ninth International Symposium on Human Aspects of. Information Security & Assurance.

- Karahoca, A., Karahoca, D., & Aksoz, M. (2019). Examining intention to adopt to internet of things in healthcare technology products. Kybernetes, 47(4), 742–770.

- Kessler, W. A. (2016). Effectiveness of the Protection Motivation Theory on Small Business Employee Security Risk Behavior. Northcentral University.

- Kusyanti, A., & Catherina, H. P. A. (2018). An Empirical Study of App Permissions : A User Protection Motivation Behaviour. International Journal of Advanced Computer Science and Applications, 9(11), 106– 111.

- Lokanan, M. E. (2015). Challenges to the fraud triangle: Questions on its use and beefy observations. Journal of Financial Crime, 22(4), 449-459.

- Moniana, J.O., Antunes, M.T.P. & Formigoni, H. (2013). The forensic accounting and corporate fraud. Journal of Information Technology and Management, 10, 119 —

- Manuel, A. & Kumara, N. (2019). Significance of Forensic Audit in the Conduct of Audit of Financial Books. International Journal of Research and Analytical Reviews. 6(1): 919-926.

- Milahan, N. & Milahan, M. (2020). Milaham, N. S. (2019). Effects of forensic accounting skills on prevention of revenue leakages in University of Jos: Journal of Educational Research in Developing Areas, 1(1):

- Mohd, S. I., & Mazni, A. (2008). An overview of forensic accounting in Malaysia. Kuala Lumpur: University of Malaysia Press Inc.

- Muthusamy, G., Quaddus, M. & Evans, R., (2010) Organizational intention to use forensic accounting services for fraud detection and prevention, large Malaysian companies. Oxford Business & Economic Conference Program. ISBN: 978-0- 9742 114-1-9.

- Myers, S.C. & Majluf, N. (1984). Corporate financing and investment decisions when firms have information that investors do not have, Journal of Financial Economics, 13, 187-221.

- Onen, D. (2016). Pecking Order Theory and Financial Management in the Context of Higher Education: A Study of Makerere University Business School in Uganda. Journal of Educational Policy and Entrepreneurial Research, l3 (1): 110-120.

- Osho, A. (2017). Impact of Forensic Accounting on University Financial System in Nigeria. European Scientific Journal, 13(31): 571-590.

- Ozili, P.K. (2020). Forensic Accounting Theory. Finance, Insurance and Risk Management Theory and Practices, Vol. 1, Emerald: 2-16.

- Reason, J. (2000). Human error: Models and management. BMJ, 320(7237), 768-770.

- Roger, R.W. (1975). Protection Motivation Theory of Fear Appeal and Attitude Change. Journal of Psychology, 91: 93-114.

- Roger, R.W. (1983). Cognitive and Physiological in Fear Appeal and Attitude Change: A revised theory of protection motivation. In J. Cacioppo & R. Petty (Ed%). Social psychophysiology. New York: Guilford Press.

- Ruan, W., Kang, S., & Song, H. (2020). Applying protection motivation theory to understand international tourists’ behavioural intentions under the threat of air pollution: A case of Beijing, China. Journal of Current Issues in Tourism, 23(16), 2027–2041. https://doi.org/10.1080/13683500.2020.1743242

- Skogan, W. G. (1990). Disorder and decline. New York: Free Press.

- Vaughan, D. (1999). The dark side of organizations: Mistake, misconduct, and disaster. Annual Review of Sociology, 25, 271-305.

- Warshavsky, M., Marcus, G. S. & Woodbury, L. (2012). Earnings Quality and the Beneish Model: Analyzing earnings quality as a financial forensic tool (accessed online, 20th May, 2014).

- Weinstein, N. D. (1987). Taking care: Understanding and encouraging self-protective behavior. Cambridge University Press. https://doi.org/10.1017/CBO9780511527760

- Zhang, R. & Kanazaki, Y (2007). Testing Static Tradeoff against Pecking Order Models of Capital Structure in Japanese Firms.