Design and Analysis of an AI-Driven Tax Avoidance Detection System in Big Data Environments for Public Sector Tax Administration

- Susheng Zheng

- Mary O’ Penetrante

- 3118-3130

- Jun 10, 2025

- Education

Design and Analysis of an AI-Driven Tax Avoidance Detection System in Big Data Environments for Public Sector Tax Administration

Susheng Zheng, Mary O’ Penetrante

Central Philippine University

DOI: https://dx.doi.org/10.47772/IJRISS.2025.905000241

Received: 29 April 2025; Accepted: 10 May 2025; Published: 10 June 2025

ABSTRACT

This paper presents a descriptive design and conceptual analysis of an AI-driven Tax Avoidance Detection System (TADS), developed for deployment in big data environments to support tax compliance monitoring within public sector administrations. While tax avoidance remains legally permissible, its widespread and opaque application undermines public revenue generation, exacerbates socio-economic inequality, and diminishes state fiscal capacity. TADS is proposed as a hybrid analytical framework that integrates deterministic rule-based logic with deep learning techniques—specifically Long Short-Term Memory (LSTM) networks—to identify complex, time-evolving patterns of tax avoidance across large-scale financial datasets. The study critically examines the structural limitations of existing tax compliance systems, drawing comparative insights from AI implementations in countries such as Australia, the United Kingdom, and China. It also explores the ethical, technical, and institutional considerations necessary for integrating intelligent detection tools into public governance frameworks. By synthesizing international best practices with a modular and interpretable AI architecture, this paper contributes a policy-oriented system blueprint designed to improve transparency, audit efficiency, and evidence-based enforcement in tax administration. Notably, the scope of this paper is limited to the conceptual and descriptive components of the system which form the basis for future research work.

Keywords: Tax avoidance, artificial intelligence, deep learning, rule-based systems, big data analytics, LSTM, algorithmic governance, tax compliance

REVIEW OF EXISTING AI-DRIVEN TAX COMPLIANCE SYSTEMS IN PUBLIC SECTOR ADMINISTRATION

Over the past decade, public sector institutions have increasingly turned to artificial intelligence (AI) and data analytics to enhance tax compliance, detect anomalies, and address the persistent challenge of tax avoidance. Although considerable strides have been made, most existing systems remain constrained by technical, institutional, and jurisdictional limitations. This section provides a comprehensive review of existing national-level AI-driven tax systems, identifies functional and structural gaps, and establishes the comparative foundation upon which the Tax Avoidance Detection System (TADS) is designed.

The Australian Taxation Office (ATO): Data Matching and Predictive Analytics

The Australian Taxation Office (ATO) is recognized for its Smarter Data initiative, which integrates structured data from various sources—including employer declarations, banking information, and asset records—to detect discrepancies in taxpayer reporting. Through its data-matching protocols, the ATO systematically compares internal records with external data feeds to flag non-compliant behaviors (Australian National Audit Office [ANAO], 2020).

Despite its robustness, the ATO’s intelligence systems primarily use rule-based algorithms with static thresholds and pre-coded conditions. This structure lacks the flexibility and adaptiveness to respond to emergent avoidance strategies and behavioral shifts, particularly among multinational corporations operating in dynamic financial environments (Chen, Han, & Wang, 2021).

Moreover, the ATO has not yet fully integrated deep learning technologies, such as Long Short-Term Memory (LSTM) networks, which are capable of processing sequential data and identifying subtle temporal deviations in taxpayer behavior (Zhou et al., 2022).

HM Revenue and Customs (UK): Behavioral Profiling through the Connect System

In the United Kingdom, HM Revenue and Customs (HMRC) developed the Connect system, which collects and processes more than 1 billion data points from over 30 government and private-sector sources (National Audit Office [NAO], 2022). The system utilizes behavioral profiling to uncover discrepancies between declared income and observed lifestyles, identifying individuals and firms whose tax declarations deviate significantly from statistical norms.

The Connect system incorporates basic unsupervised learning tools and anomaly detection features but does not yet include advanced sequential models like LSTM or transformer-based frameworks. Its use of social media and third-party databases has been credited with improved detection rates, yet it has also raised ethical concerns regarding taxpayer privacy and algorithmic opacity (Richards & van Zeben, 2020; Miller, 2023).

Furthermore, Connect’s limited real-time processing capabilities constrain its ability to detect strategic avoidance schemes that evolve over time—a gap that next-generation systems like TADS aim to bridge.

China’s Golden Tax III System: Digital Integration with Deterministic Logic

The Golden Tax III System, developed by the State Administration of Taxation (SAT) of China, exemplifies the government’s ambition to centralize and digitize tax administration. It facilitates mandatory e-invoicing, tracks VAT records, and integrates data from firms’ internal accounting systems (Zhao & Zhang, 2022). This infrastructure has significantly enhanced transparency and reduced outright fraud.

Nonetheless, the system’s intelligence core remains deterministic, relying on predefined regulatory rules and thresholds, which limits its responsiveness to novel avoidance behaviors (Wang & Lee, 2021). Although Document No. 158 from SAT encourages the use of AI in tax risk detection, implementation remains limited due to a fragmented data landscape and insufficient technical capacity at the provincial level (Dang & Nguyen, 2022).

AI deployment in China’s tax domain is further hampered by inter-agency data silos, inadequate data governance protocols, and a lack of trained personnel capable of developing and managing complex learning systems (Gupta et al., 2023).

Singapore’s Inland Revenue Authority (IRAS): Citizen-Centric AI and Risk Segmentation

The Inland Revenue Authority of Singapore (IRAS) has adopted a service-oriented approach, incorporating AI-driven chatbots, NLP tools, and behavioral segmentation to personalize compliance outreach (Chua & Tan, 2021). While these systems have enhanced taxpayer experience and improved voluntary compliance, IRAS focuses more on service delivery than on robust enforcement mechanisms for corporate tax avoidance.

Deep learning applications remain limited in IRAS operations, and the system has not publicly disclosed the use of time-series models such as LSTM to monitor corporate avoidance behavior over fiscal cycles (Taylor & Wong, 2021). This reflects a broader trend in developed nations: while AI is being used for taxpayer services and audit selection, its application in automated, real-time tax avoidance detection remains underdeveloped.

Emerging Economies: Constraints and Opportunities

In Nigeria, the TaxPro Max system by the Federal Inland Revenue Service has introduced digital filing and rudimentary analytics but lacks advanced automation or cross-sector integration (Udo & Adegbite, 2021). Similar patterns exist in India’s GST Network (GSTN), where digitalization is advanced, but machine learning is primarily used for fraud detection and not yet for behavioral avoidance analytics (Bhatia & Sahu, 2022).

In Latin America, Brazil’s Public Digital Bookkeeping System (SPED) has digitized tax records, yet the underlying analytics systems remain mostly static and are rarely integrated with AI-enhanced behavioral modeling (Mannan et al., 2021). Chile has advanced in e-invoicing but faces similar limitations in deep learning integration due to institutional and resource constraints.

These examples illustrate a fundamental barrier: while digital infrastructure exists in many emerging economies, the transition to adaptive, intelligent compliance systems is hindered by regulatory fragmentation, low algorithmic literacy, and lack of inter-ministerial data coordination (Nurunnabi, 2019; Rashid et al., 2023).

Comparative Summary: Lessons and Gaps Addressed by TADS

| Criteria | ATO (Australia) | HMRC (UK) | China (Golden Tax III) | Singapore (IRAS) | Gap Addressed by TADS |

| Data Fusion | Moderate | High | Low | Moderate | Unified ingestion pipeline |

| Rule-Based Logic | Strong | Strong | Strong | Moderate | Integrated but modular |

| Deep Learning | Minimal | Emerging | Absent | Absent | Centralized LSTM modeling |

| Real-Time Analytics | Limited | Limited | Batch-based | Absent | Real-time anomaly detection |

| Behavioral Pattern Recognition | Weak | Moderate | Weak | Weak | LSTM-based temporal modeling |

| Cross-Border Capability | Absent | Absent | Absent | Absent | Multi-jurisdictional extension |

| Legal Explainability | High | Moderate | High | High | Hybrid logic + AI interpretability |

By analyzing these gaps, TADS is designed to combine the deterministic clarity of rule-based logic with the adaptive intelligence of deep learning models. Its modular architecture supports both real-time and batch processing. TADS can ingest structured, semi-structured, and unstructured data sources and apply LSTM-based models to trace longitudinal patterns in tax behavior.

Furthermore, the system includes a visual risk scoring interface, audit prioritization logic, and scenario simulation, making it suitable for integration into public sector tax administration. The comparative analysis validates the need for such a hybrid model, especially in jurisdictions where manual audits, rule-based inspections, and data fragmentation limit effective enforcement.

System Design and Architecture of the Tax Avoidance Detection System (TADS)

The Tax Avoidance Detection System (TADS) is a conceptual AI-enabled system designed for use in public sector tax administration. Its architecture combines deterministic rule-based logic with deep learning capabilities to identify both static and evolving patterns of tax avoidance in big data environments. The system design reflects the need for scalable, adaptive, and explainable AI solutions in complex regulatory domains such as taxation.

Design Philosophy and Conceptual Framework

TADS is informed by empirical evidence and theoretical frameworks that emphasize the growing complexity of tax behavior and the need for intelligent, trustworthy enforcement tools.

- Hybrid Detection Approach. Combining rule-based and AI models is increasingly regarded as a best practice in domains where legal accountability must be balanced with adaptive intelligence (Kovvali & Tan, 2021). While rule-based systems provide consistency and interpretability (Agrawal et al., 2018), deep learning adds the ability to detect novel or unobserved behavioral patterns (Zhou, Tran, & Lee, 2022).

- Modular Architecture. Modular system design ensures reusability and jurisdictional adaptability, which are critical in public sector applications with heterogeneous IT environments (Miller, 2023).

- Dual-Mode Analytical Logic. The integration of symbolic reasoning (rules) and sub symbolic learning (neural networks) is aligned with hybrid AI models shown to be effective in financial fraud detection and compliance (Gupta, Narayanan, & Zhou, 2023).

- Compliance-Focused Interface. The use of explainable, task-centered interfaces supports adoption in public agencies, where users often lack technical AI expertise. The Technology Acceptance Model (TAM) posits that perceived ease of use and usefulness are key determinants of system uptake in public administration (Davis, 1989; Venkatesh & Bala, 2008).

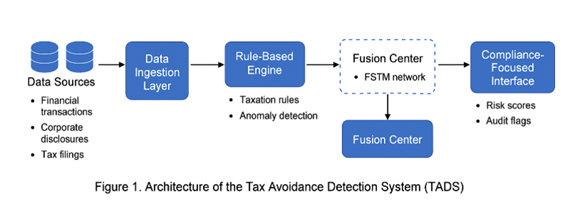

Three-Layer System Architecture

a) Data Ingestion and Preprocessing Layer

The overall architecture of TADS is structured across three functional layers, as illustrated in Figure 1. This modular and sequential design enables integration of diverse data sources, hybrid analytical processing, and audit-ready decision support in public sector tax systems.

This layer is critical to ensuring the integrity and usability of input data. Research on AI in tax systems emphasizes the importance of preprocessing to avoid model bias and improve reliability (Nurunnabi, 2019).

- Structured and Semi-Structured Data. These are core to existing digital tax systems such as India’s GSTN and China’s Golden Tax III (Wang & Lee, 2021).

- Unstructured Data Integration. Although not widely implemented, use of NLP in tax enforcement is gaining interest in countries like Singapore and the UK (Chua & Tan, 2021).

- Anonymization. Data protection laws such as the EU’s GDPR and China’s Personal Information Protection Law require de-identification and encrypted processing in AI-based systems (Richards & van Zeben, 2020).

- Time-Series Formatting. Time-dependent modeling is foundational for LSTM networks, which have been effectively used in fraud detection, behavioral finance, and medical diagnostics (Hochreiter & Schmidhuber, 1997; Chen et al., 2021).

b) Analytical Engine Layer

Rule-Based Logic Module

Rule-based systems remain essential in regulatory domains due to their legal traceability and alignment with audit standards (OECD, 2019).

- Audit Heuristics. Many national tax agencies use deterministic rules for compliance monitoring—such as persistent losses, underreporting, and transaction irregularities (NAO, 2022; ANAO, 2020).

Deep Learning Module (LSTM)

LSTM networks are ideal for capturing long-term dependencies in sequential data, such as corporate tax filings and transaction flows (Zhou et al., 2022).

- Behavioral Drift Detection. Behavioral analytics using LSTM has been effective in cybersecurity and e-commerce and is increasingly explored in public finance (Gupta et al., 2023).

- Model Feedback Loops. Adaptive learning mechanisms are necessary for public AI systems to remain current with tax code changes and evolving taxpayer behavior (Dang & Nguyen, 2022).

c) Output and Decision Support Layer

- Dashboards and Risk Scoring. The visual presentation of complex AI outputs improves auditor decision-making and supports “human-in-the-loop” transparency (Taylor & Wong, 2021).

- Scenario Simulation. Predictive scenario tools are becoming common in fiscal policy planning, especially in forward-looking tax compliance analytics (Bhatia & Sahu, 2022).

- Audit Trails. Legal and ethical frameworks now require AI systems to provide explainable, auditable outputs (Miller, 2023; OECD, 2021).

Data Flow and Processing Pipeline

The semi-automated pipeline approach supports interoperability and flexibility, which are necessary in public sector systems with legacy IT infrastructure (Zhao & Zhang, 2022). The fusion of rule-based and AI signals is modeled on ensemble learning methods shown to improve classification accuracy and reduce false positives (Agrawal et al., 2018).

Compliance-Aware Model Design

Public AI systems must meet higher standards of accountability. TADS incorporates several mechanisms to address this:

- Explainable AI (XAI). Tools like SHAP and LIME are now widely recommended for public-sector machine learning, ensuring transparency in high-stakes decisions (Miller, 2023).

- Bias Audits and Fairness Checks. Auditing model behavior across firm size, sector, and region helps avoid discriminatory impacts and supports just enforcement (Nurunnabi, 2019).

- Ethical Governance. Guidelines by the OECD (2021) and European Commission (2022) call for ethical-by-design principles in AI systems used by governments.

Scalability, Localization, and Interoperability

- Interoperability with Existing Systems. The ability to connect with legacy tax platforms such as China’s Golden Tax III or Australia’s Taxable Payments Reporting System is a core design consideration (Zhao & Zhang, 2022; ANAO, 2020).

- Custom Rule Libraries and Local Tax Law. A modular rule engine allows jurisdictions to implement national regulations, mirroring the logic used in compliance engines like HMRC’s Connect system (NAO, 2022).

- Role-Based Access Controls. Hierarchical data access structures reflect global best practices in public financial systems, protecting sensitive taxpayer data (Richards & van Zeben, 2020).

Analytical Logic and Detection Indicators

The Tax Avoidance Detection System (TADS) is designed with a dual analytical engine that integrates traditional rule-based logic with artificial intelligence (AI) techniques to address complex patterns of tax avoidance. Its analytical framework responds to the challenges public sector tax administrators face in identifying manipulative financial behaviors that elude detection by conventional systems. This section presents the core detection logic, risk indicators, and model reasoning that underpin the conceptual framework of TADS.

Rule-Based Detection Logic: Statutory Flags and Heuristic Triggers

The rule-based module of TADS applies predefined compliance indicators derived from fiscal statutes, audit protocols, and regulatory red flags. This deterministic logic is essential for ensuring legal traceability and procedural accountability—requirements widely endorsed in public sector applications of AI (Miller, 2023; OECD, 2021).

Key Detection Rules:

- Persistent Loss Reporting: Firms reporting negative net income for three or more consecutive years, particularly where gross revenue remains constant, are flagged for potential strategic loss creation.

- Unbalanced Wage-to-Revenue Ratio: A significant year-on-year increase in personnel costs, particularly executive compensation, in the absence of matching revenue growth, is suggestive of disguised profit transfers or inflated deductions.

- High-Frequency Related-Party Transactions: Repeated dealings with affiliated entities, especially where counterparts are based in low-tax jurisdictions, trigger alerts under transfer pricing compliance logic.

- Statement Mismatches: Discrepancies between reported income, costs, or assets across tax filings and financial statements (e.g., misalignment of VAT declarations with income tax filings) are used as cross-verification signals.

- Round Number Invoices and Fiscal Year-End Adjustments: The appearance of large, round-figure transactions or abnormal increases in liabilities during the last month of a fiscal year may indicate end-period income deferral or fictitious expenses (OECD, 2019).

Each rule is assigned a weighted score, contributing to a Rule-Based Risk Score (RRS) ranging from 0–100. Thresholds for audit recommendation are typically set between 70–80, based on institutional capacity and risk tolerance levels.

AI-Based Logic: Behavioral Anomaly Detection via LSTM

To detect patterns not captured by fixed rules, TADS incorporates a behavioral anomaly detection module using Long Short-Term Memory (LSTM) networks. LSTM is a class of recurrent neural networks (RNNs) designed for learning sequential patterns in time-dependent datasets (Hochreiter & Schmidhuber, 1997). In tax administration, this supports detection of behavioral drift and latent strategies deployed over multiple fiscal periods.

Model Features and Inputs:

- Monthly time-series data: net profit margin, operational expenses, gross income, taxable base.

- Ratios such as effective tax rate, profit-before-tax-to-income ratio.

- Frequency and value of intra-group transactions.

- Sector-normalized financial metrics (e.g., Z-scores for industry deviation).

Detected Patterns:

- Sequential Underreporting: Firms whose reported income remains just below exemption thresholds over multiple periods.

- Behavioral Breakpoints: Sudden and unexplained shifts in income or expenses, inconsistent with seasonal or industry trends.

- Temporal Clustering: Detection of abnormal transaction patterns near policy deadlines or audit windows, signaling potential regulatory arbitrage.

- Co-behavioral Clustering: Groups of firms showing synchronized reporting trends, often linked to shared consultants or ownership networks.

Model outputs generate an Anomaly Risk Score (ARS), also scaled 0–100. LSTM models are trained on historical labeled datasets, refined through supervised learning, and tested using metrics such as AUC, precision, and recall, as commonly applied in financial anomaly detection systems (Gupta, Narayanan, & Zhou, 2023; Zhou, Tran, & Lee, 2022).

Composite Risk Scoring and Decision Prioritization

TADS integrates deterministic and AI-derived insights into a Composite Risk Score (CRS) to inform audit prioritization.

Risk Score Fusion Model:

CRS=α⋅RRS+(1−α)⋅ARSCRS = \alpha \cdot RRS + (1 – \alpha) \cdot ARSCRS=α⋅RRS+(1−α)⋅ARS

Where α\alphaα is a tunable parameter (e.g., 0.6–0.7) that emphasizes legal rule adherence over probabilistic output, particularly appropriate for public sector applications where due process and legal auditability are mandatory.

Cases with CRS scores above a configured threshold (e.g., 75) are marked for review, while borderline cases (e.g., 60–74) may be manually escalated based on additional context.

This fusion approach reflects current best practices in hybrid fraud detection systems and improves the balance between interpretability and sensitivity (Agrawal, Gans, & Goldfarb, 2018; Wang & Lee, 2021).

Model Interpretability and Interface Logic

In public sector environments, the legitimacy of AI-based decisions hinges on transparency and user trust. TADS includes multiple components to support explainable decision-making:

- SHAP-Based Feature Attribution: Each anomaly flag is accompanied by an explanation showing the key financial features (e.g., profit margin deviation, wage spikes) that influenced the LSTM output (Lundberg & Lee, 2017).

- Rule Flag Visualizations: Each flagged firm is shown with corresponding triggered rules, risk weights, and thresholds, enabling tax officers to trace logic step-by-step.

- Interactive Simulation Panel: Auditors can simulate what-if scenarios, such as adjusting deductible expenses or excluding outliers, to observe how risk scores would change.

- Override and Feedback Loops: Human auditors can annotate model outputs, confirm or dismiss alerts, and provide qualitative inputs, supporting a human-in-the-loop governance model (Miller, 2023; OECD, 2021).

These components promote algorithmic transparency, institutional accountability, and enhance user adoption, consistent with ethical AI guidelines in the public sector (Richards & van Zeben, 2020).

Core Indicators Used in Detection Framework

TADS integrates a range of rule-based and statistical indicators across its modules. Table 1 summarizes the key categories:

| Indicator Category |

Example Indicators |

| Statutory Violations | Overstated deductions, non-declared income, excessive related-party expenses |

| Financial Behavior Flags | Year-over-year volatility, round-figure patterns, fiscal-year-end adjustments |

| Temporal Patterns | Sudden declines in taxable income, clustering of deductions before audit cycles |

| Cross-Reporting Mismatches | Discrepancies between VAT returns and income tax filings |

| Comparative Deviations | Deviations from industry ratios or peer group norms (e.g., cost-to-income ratio) |

These indicators support layered detection and allow flexible customization by tax authorities, depending on sector-specific risks or national audit policies.

Discussion and Policy Implications

The conceptual design of the Tax Avoidance Detection System (TADS) illustrates a forward-looking response to the persistent and evolving issue of tax avoidance in public revenue systems. Through the integration of rule-based and AI-enabled analytical logic, TADS addresses the need for intelligent, explainable, and adaptive systems in public tax administration. It explore the broader implications across four core domains: algorithmic governance, developing country applications, legal-ethical design, and public sector institutional transformation.

Advancing Algorithmic Governance in Tax Compliance

TADS advances the discourse on algorithmic governance—the structured use of AI in administrative decision-making—by proposing a hybrid compliance monitoring framework that is both technically robust and legally auditable. Traditional tax detection systems rely on static thresholds and deterministic rule sets that are transparent but often too rigid to adapt to evolving avoidance strategies. TADS combines these strengths with machine learning models capable of identifying non-obvious behavioral patterns, thus enabling a more nuanced detection process.

This hybrid approach allows for multi-level governance. At the strategic level, tax authorities can adjust detection parameters based on policy shifts, emerging threats, or political directives. At the operational level, auditors gain a real-time, data-driven risk signal that assists with targeting limited investigative resources. By embedding transparency mechanisms—such as model explainability tools and rule traceability—TADS adheres to the public sector’s ethical and procedural expectations. It thus exemplifies how AI can support, rather than undermine, administrative legitimacy.

Implications for Tax Authorities in Developing and Transition Economies

Developing and transition economies face significant constraints in implementing advanced digital tax systems, including limited access to skilled personnel, fragmented data infrastructures, and low taxpayer compliance culture. TADS offers a pragmatic, scalable solution for such contexts.

Its modular architecture enables incremental adoption. For example, a national revenue agency could initially deploy only the rule-based engine, enforcing known statutory triggers and improving data validation procedures. As technical capacity improves, machine learning modules can be integrated without reengineering the entire system. This ensures cost-effectiveness and reduces technological dependency.

TADS is also designed to be data-flexible, accepting inputs from spreadsheets, XML-based reports, and even semi-structured records from legacy financial systems. This flexibility makes it particularly suitable for countries that are digitizing gradually and lack centralized tax data repositories.

Moreover, by prioritizing risk-based audit selection, the system supports more efficient use of scarce enforcement resources. In jurisdictions where audit coverage is limited, intelligent targeting mechanisms can significantly improve audit yield and reduce fiscal leakage. TADS empowers institutions to shift from reactive enforcement to strategic compliance management, contributing to long-term improvements in fiscal governance.

Ethical, Legal, and Institutional Considerations

The deployment of AI in public tax systems raises legitimate concerns about fairness, due process, and institutional accountability. Unlike private sector applications where performance metrics dominate, public systems must demonstrate not only efficiency but also equity and transparency.

TADS addresses these risks through several embedded safeguards. First, all risk assessments generated by the AI model are accompanied by explainable outputs—visual displays of feature importance and causal inference that help auditors understand why a particular firm or transaction was flagged. This reduces the opacity of deep learning systems and enables informed decision-making.

Second, the system includes a rule traceability protocol, where every deterministic flag includes a reference to the triggering rule, its legal basis, and the observed data. This ensures that any punitive action taken by the state can be backed by auditable, statutory justifications.

Third, TADS is designed for human-in-the-loop governance, allowing tax officers to override automated alerts, annotate edge cases, and contribute feedback to the model’s learning process. This aligns with administrative law principles and maintains the integrity of public decision-making processes.

Finally, the system incorporates bias mitigation mechanisms, ensuring that its models are tested across firm sizes, sectors, and regions. This prevents systematic discrimination and upholds the principle of horizontal equity in taxation—where similarly situated entities are treated equally.

Practical Applications and Institutional Benefits

From an implementation standpoint, the TADS framework holds considerable value for institutional modernization and operational efficiency in public tax administrations.

The system enables risk-based audit allocation, where auditors can focus on high-risk cases identified through composite scoring rather than random or quota-based selection. This significantly enhances the productivity of audit operations and reduces the chance of wasteful investigations.

Moreover, the predictive nature of TADS supports a preventive compliance model. Firms aware that advanced detection systems are in place may be more likely to report accurately, thereby fostering a culture of voluntary compliance. This aligns with global tax administration strategies emphasizing soft compliance and behavioral nudges.

The system’s policy simulation tools allow agencies to test the effects of proposed rule changes or enforcement thresholds on compliance patterns before formal adoption. This enhances evidence-based policymaking and supports adaptive regulatory design.

Lastly, TADS provides a framework for capacity augmentation. In many developing economies, tax officers are overburdened and under-resourced. By providing automated alerts, structured risk visualizations, and rule validation, the system acts as a digital co-auditor—freeing human officers to focus on complex legal analysis, taxpayer engagement, and institutional planning.

LIMITATIONS AND FUTURE PATHWAYS

While TADS represents a robust conceptual advancement, several challenges must be considered for future implementation. First, the effectiveness of the system depends on the availability and quality of data. In contexts where tax data is inconsistent, incomplete, or not digitized, the full potential of AI-based risk detection may not be realized. A preliminary investment in data integration and standardization is therefore essential.

Second, institutional readiness remains a bottleneck. Successful deployment of TADS will require trained personnel, IT infrastructure, inter-agency data sharing agreements, and governance structures that can monitor and refine the system over time. Without these elements, the system may face implementation delays or underperformance.

Third, the sociopolitical environment influences the acceptance of algorithmic oversight. In jurisdictions where public trust in institutions is low, or where tax enforcement is perceived as politically motivated, AI systems must be deployed with exceptional care to avoid exacerbating perceptions of unfairness.

Finally, deep learning models require continual monitoring to prevent concept drift—where the patterns learned by the model become outdated due to changes in taxpayer behavior, regulatory norms, or economic shocks. Future iterations of TADS should incorporate adaptive learning capabilities, governance oversight boards, and transparency reporting to ensure sustained efficacy and public confidence.

In summary, this study has explored the conceptual design and descriptive logic of the Tax Avoidance Detection System (TADS), a hybrid framework that integrates rule-based auditing principles with advanced artificial intelligence (AI) to strengthen public sector tax compliance oversight. Rooted in the realities of digital tax environments and complex avoidance strategies, TADS offers a system-level response to long-standing limitations in traditional compliance monitoring, particularly in jurisdictions constrained by resource fragmentation, manual audit processes, and low data integration capacity.

At its core, TADS is a response to the need for a more adaptive, scalable, and transparent approach to tax avoidance detection. Unlike static rule-based systems that depend solely on fixed thresholds or pre-defined patterns of non-compliance, the TADS architecture allows for both deterministic and probabilistic analysis. By combining legal rule sets with sequential pattern learning via LSTM neural networks, the system conceptually supports the detection of both explicit violations and more subtle, strategic avoidance behaviors. Importantly, its emphasis on explainability, audit traceability, and human-in-the-loop validation makes it particularly suitable for deployment in public institutions, where accountability and procedural fairness are non-negotiable.

The review of existing AI-driven tax detection systems in countries such as Australia, the United Kingdom, China, and Singapore revealed a global trend toward digitization, but also exposed limitations related to interoperability, deep learning adoption, and ethical oversight. TADS, in contrast, is designed to be jurisdiction-neutral—applicable across legal systems and scalable across different enforcement capacities. Its modular configuration allows tax authorities to adopt and configure components progressively, ensuring implementation feasibility even in developing or transitioning economies.

Furthermore, this study positions TADS as a contribution not only to the technical literature on compliance systems but also to the public governance discourse on algorithmic decision-making. As tax administrations grapple with balancing automation, discretion, and legal legitimacy, frameworks like TADS exemplify how AI can augment rather than replace human judgment, and how technology can be aligned with institutional values such as transparency, fairness, and responsiveness.

RECOMMENDATIONS

1. Invest in Digital Infrastructure and Data Governance

One of the foundational enablers for systems like TADS is a reliable, standardized, and secure data infrastructure. Many public tax agencies still operate in siloed environments, where taxpayer records are fragmented across departments, time periods, or formats. Governments must invest in interoperable data platforms, create enforceable data-sharing policies between agencies, and implement robust cybersecurity and privacy frameworks. Without such foundations, even the most sophisticated detection logic will suffer from poor data quality and low analytical reliability.

2. Adopt a Phased and Modular AI Strategy

For many jurisdictions—particularly those with constrained fiscal or technical capacity—a full-scale AI deployment may be impractical or counterproductive. The TADS model supports a phased implementation strategy, beginning with rule-based auditing modules that mirror current practices but add structure and automation. Over time, additional capabilities such as LSTM modeling, risk scoring, and behavioral simulation can be layered in. This incremental approach reduces risk, allows for internal capacity-building, and builds institutional confidence in AI-based tools.

3. Embed Legal and Ethical Oversight from the Outset

The use of AI in taxation, a domain directly involving citizen rights and financial penalties, raises sensitive ethical and legal questions. To safeguard against overreach, systems must be designed with built-in accountability mechanisms, including model documentation, redress procedures, audit logs, and explanation frameworks. Independent review boards or regulatory sandboxes could be employed to test systems before public deployment. Embedding such oversight early not only avoids legal conflicts but also fosters public trust and institutional credibility.

4. Develop Training and Institutional Capacity

No matter how powerful the analytics, AI systems require competent human actors to interpret, challenge, and act upon their outputs. Tax authorities should prioritize upskilling programs for auditors, compliance analysts, and policy staff to ensure that they can use, refine, and govern AI systems. Training should encompass not only technical usage but also data ethics, AI governance, and decision accountability. Institutional units responsible for digital transformation should be resourced with multidisciplinary teams, combining tax law, IT, data science, and administrative law expertise.

5. Encourage International Collaboration

Tax avoidance is inherently global. Multinational enterprises often exploit asymmetries in tax regimes, and emerging tax risks are increasingly cross-border in nature. To strengthen detection capabilities, national tax authorities should engage in regional cooperation, share AI methods, develop standardized risk indicators, and explore interoperable platforms for data exchange. Platforms such as the OECD’s Forum on Tax Administration or regional tax communities could support the harmonization of AI standards and promote learning between high- and low-capacity jurisdictions.

6. Advance Research and Pilot Testing

While this paper outlines a conceptual and descriptive framework, further empirical work is needed to validate and refine the system in practice. Future research could involve:

- Simulated testing using anonymized tax datasets,

- Performance comparisons between rule-only and hybrid detection models,

- Behavioral analysis of how AI-based risk flags influence audit decisions,

- Impact assessments on taxpayer behavior when AI systems are made visible or transparent.

These studies would provide evidence to support future iterations of TADS and help ensure that implementation is guided by both technical performance and real-world institutional dynamics.

As governments navigate the complexities of modern tax enforcement, marked by digital globalization, cross-border transactions, and increasingly agile avoidance strategies, conceptual tools like TADS represent a proactive evolution in governance capacity. This paper has laid out the descriptive foundation of such a system, integrating theoretical and practical elements from public finance, information systems, and ethical AI.

While actual development, deployment, and results remain outside the scope of this study, the descriptive analysis presented herein affirms the relevance and utility of AI-enhanced tax detection frameworks. With careful institutional planning, legal sensitivity, and ethical foresight, systems like TADS can help public agencies shift from reactive compliance models to proactive, intelligence-driven administration—ultimately improving equity, efficiency, and trust in public revenue systems.

REFERENCES

- Agrawal, A., Gans, J., & Goldfarb, A. (2018). Prediction machines: The simple economics of artificial intelligence. Harvard Business Review Press.

- Alm, J. (2019). What motivates tax compliance? Journal of Economic Surveys, 33(2), 353–388.

- Australian National Audit Office (ANAO). (2020). Administration of the Tax Avoidance Taskforce.

- Bhatia, R., & Sahu, R. (2022). Emerging trends in Indian GST compliance using data analytics. Journal of Public Sector Innovation, 9(3), 22–33.

- Chen, Y., Han, L., & Wang, Q. (2021). Deep learning applications in tax administration. Journal of Data Science and Policy, 3(2), 55–68.

- Chua, E., & Tan, W. (2021). Smart governance and AI in Southeast Asia: The case of IRAS Singapore. Asian Journal of Public Administration, 43(1), 89–104.

- Dang, Q. T., & Nguyen, H. T. (2022). AI adoption in tax administration: Challenges in developing countries. International Journal of Digital Policy, 4(1), 45–60.

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 13(3), 319–340.

- Gupta, A., Narayanan, S., & Zhou, M. (2023). Leveraging neural networks for financial compliance detection. AI in Government Review, 5(2), 101–117.

- Hochreiter, S., & Schmidhuber, J. (1997). Long short-term memory. Neural Computation, 9(8), 1735–1780.

- Kovvali, S., & Tan, D. (2021). Hybrid AI systems in regulatory intelligence. Government Technology Review, 8(1), 12–29.

- Lundberg, S. M., & Lee, S.-I. (2017). A unified approach to interpreting model predictions. In Advances in Neural Information Processing Systems (Vol. 30).

- Miller, J. (2023). Ethical risks in public sector AI: A case study of tax algorithms. Journal of Algorithmic Accountability, 12(1), 33–51.

- National Audit Office (NAO). (2022). Use of Data Analytics in HMRC.

- Nurunnabi, M. (2019). Tax evasion and avoidance: Empirical evidence from developing countries. Global Journal of Tax Administration, 1(1), 14–28.

- OECD(2019). Model Mandatory Disclosure Rules for CRS Avoidance Arrangements and Opaque Offshore Structures.

- OECD(2021). Recommendation of the Council on Artificial Intelligence.

- Rashid, A., Karim, N., & Liew, C. (2023). Structural constraints in tax collection across emerging economies. Fiscal Studies Review, 19(1), 77–91.

- Richards, M., & van Zeben, J. (2020). Algorithmic governance in public finance: Risks and opportunities. Government Analytics Review, 8(4), 79–92.

- Taylor, R., & Wong, J. (2021). Governance and AI: Enhancing transparency in digital tax systems. Public Policy and Technology Journal, 6(2), 44–59.

- Udo, S., & Adegbite, O. (2021). Digital transformation in Nigeria’s tax system: Challenges and prospects. African Journal of Public Administration, 7(2), 118–135.

- Venkatesh, V., & Bala, H. (2008). Technology acceptance model 3 and a research agenda on interventions. Decision Sciences, 39(2), 273–315.

- Wang, H., & Lee, J. (2021). Hybrid AI models in fiscal surveillance: A case for rule-learning convergence. Journal of Financial Forensics, 11(3), 65–81.

- Zhao, M., & Zhang, Y. (2022). Digital tax administration in China: Current practice and future directions. China Economic Review, 74, 101707.

- Zhou, L., Tran, M. D., & Lee, D. (2022). Deep learning in regulatory compliance: A systematic review. Journal of AI & Society, 37(1), 109–125.